Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.12 Billion |

| Market Size (2026) | USD 1.23 Billion |

| Market Size (2031) | USD 2.01 Billion |

| Growth Rate (2026 - 2031) | 10.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Flexible Office Space Market Analysis by Mordor Intelligence

The UAE Flexible Office Space Market size was valued at USD 1.12 billion in 2025 and is estimated to grow from USD 1.23 billion in 2026 to reach USD 2.01 billion by 2031, at a CAGR of 10.24% during the forecast period (2026-2031).

Healthy demand stems from rapid business formation in free zones, sustained inflows of foreign direct investment, and a nationwide pivot toward hybrid work settings that reward agile occupancy models. Operators are widening their footprints in premium towers across Dubai and Abu Dhabi, yet landlords report an accelerating shift toward smaller, fully furnished suites that compress initial capital outlays while preserving optionality around head-count swings. Competitive tension is intensifying as global brands such as WeWork and IWG face well-capitalized regional specialists that bundle bespoke fit-outs with concierge-level hospitality, enhancing retention in a market where lease terms average only 14 months. At the same time, government programs offering long-term visas for remote workers, coupled with corporate-tax exemptions in more than 50 free-zone districts, are widening the inbound funnel for international occupiers.

Key Report Takeaways

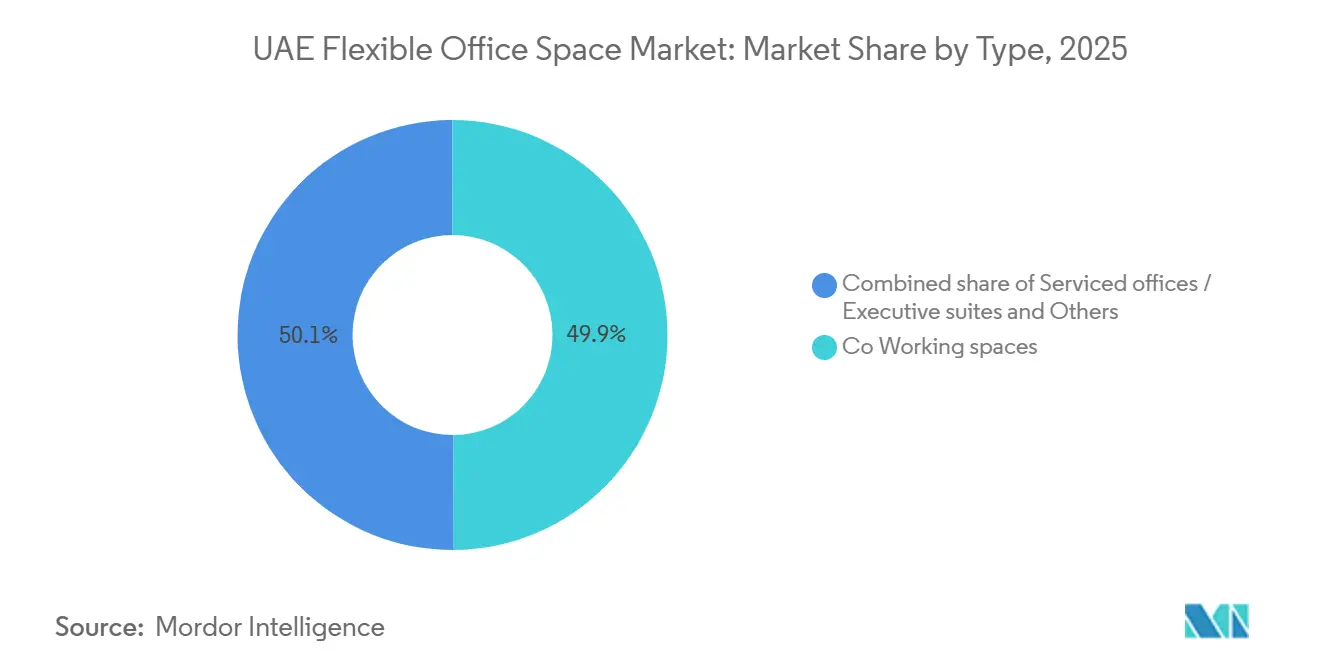

- By type, co-working space captured 49.9% of the UAE flexible office space market share in 2025. Serviced offices/executive suites are projected to expand at an 11.44% CAGR through 2031.

- By sector, information technology services accounted for a 40.9% of the UAE flexible office space market size in 2025. Banking and financial services post the fastest 2026-2031 CAGR at 11.51%.

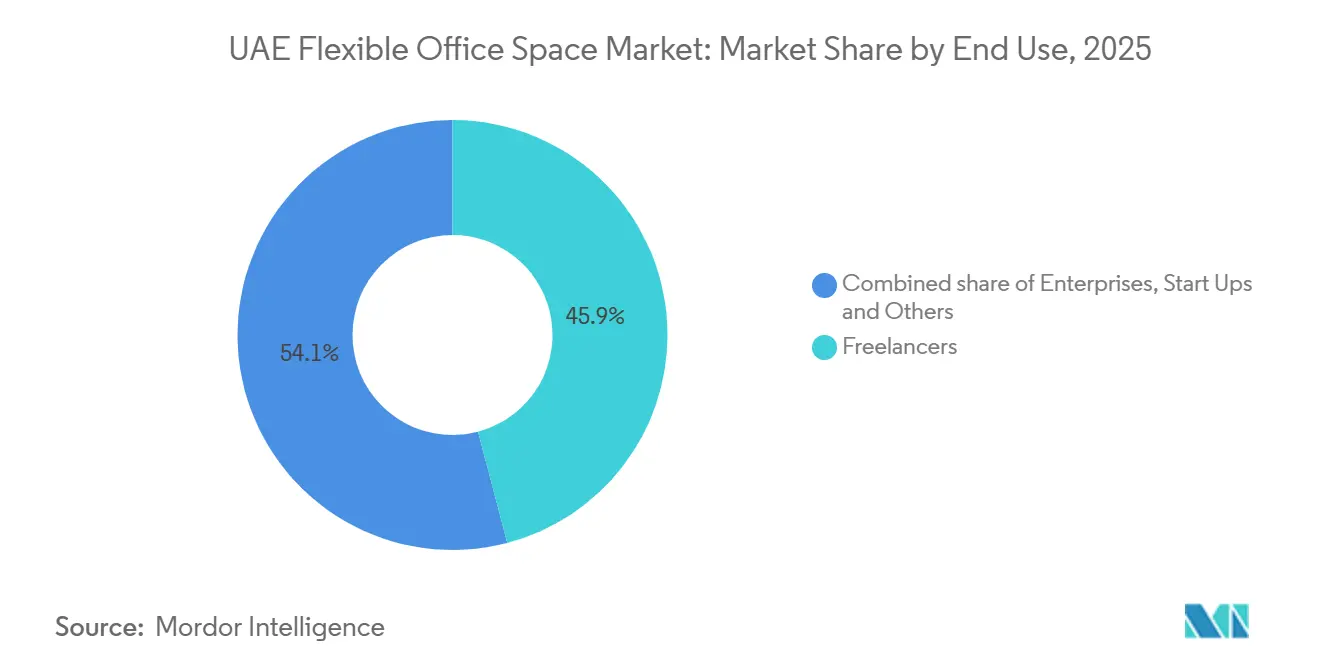

- By end use, freelancers held 45.9% of the UAE flexible office space market size in 2025, whereas start-ups led growth at an 11.71% CAGR to 2031.

- By city, Dubai contributed 67% of the UAE flexible office space market share in 2025, while Sharjah is poised for a 12.08% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Flexible Office Space Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate adoption of hybrid work models increases demand for flexible office solutions | +2.8% | Global, with accelerated uptake in Dubai and Abu Dhabi business districts | Short term (≤ 2 years) |

| Government initiatives and free-zone policies encourage flexible workspace expansion | +2.5% | National, with the strongest gains in Dubai, Abu Dhabi, and designated free zones | Medium term (2-4 years) |

| Rising foreign business inflows drive demand for short-term and scalable office space | +2.2% | National, with early gains in Dubai, followed by Abu Dhabi and Sharjah | Short term (≤ 2 years) |

| Dubai and Abu Dhabi position as premium hubs for flexible office space providers | +1.9% | Dubai and Abu Dhabi's core business districts | Medium term (2-4 years) |

| Growing preference for fully serviced and technology-enabled workspaces supports market growth | +1.6% | Global, spill-over to the UAE premium office clusters | Medium term (2-4 years) |

| Digital-nomad visas and remote-worker residency schemes attract international flexible workspace users | +1.4% | National, with early gains in Dubai, Abu Dhabi, and Sharjah, co-working hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Corporate Adoption of Hybrid Work Models Increases Demand for Flexible Office Solutions

Multinationals formalized split-week schedules to curb fixed real-estate costs, especially after Abu Dhabi’s 2025 employment update explicitly legalized hybrid arrangements. Financial-services and professional-services firms, traditionally wary of shared environments, now lease private suites inside free-zone-certified buildings equipped with biometric entry and segregated networks. Technology firms remain the largest tenant cohort, yet enterprise demand is diversifying, creating a bifurcated market of cost-driven hot desks and compliance-driven private floors. Operators that invested early in ISO-27001 data-security certification and on-site SOC monitoring now command enterprise premiums. Flexible lease clauses aligned with project-based staffing cycles further strengthen retention among procurement-savvy corporate occupiers.

Government Initiatives and Free-Zone Policies Encourage Flexible Workspace Expansion

A wave of reforms between 2024 and 2026 dismantled legacy restrictions on foreign ownership, slashed company-formation timelines, and bundled office packages with visas and banking introductions. Dubai Multi Commodities Centre and Abu Dhabi Global Market now compete on workspace quality rather than license fees, pressing operators to layer mentorship, accelerator access, and sector-specific events onto basic desk rentals. The Roads and Transport Authority went a step further in 2024 by opening coworking lounges inside Burjuman Metro Station, signaling that authorities view flexible workspace as part of public infrastructure.[1]Dubai Roads and Transport Authority, “RTA Launches Metro Coworking Hubs,” rta.ae Together, these moves trimmed incorporation-to-operation cycles from months to weeks and funneled a steady pipeline of new tenants into flexible offices. As free-zone one-stop shops mature, operators that can integrate compliance, legal, and market-entry support stand to capture durable, higher-margin contracts.

Rising foreign business inflows drive demand for short-term and scalable office space

Greenfield foreign direct investment reached USD 33.2 billion across 1,491 projects in 2025, with 418 classed as business-services deals that gravitate toward turnkey offices. Astrolabs capitalized by bundling coworking memberships with Saudi market-entry advisory, positioning the workspace as a launchpad rather than an overhead cost. Similar tie-ups between operators, banks, and free zones shorten entry lead times and boost desk absorption rates. As licensing reforms continue, inbound firms prioritize agility and ecosystem access over low rent, fueling premium occupancy even amid broader economic cyclicality. Early-stage operators that lock in bank and regulator partnerships gain a durable pipeline of foreign entrants.

Dubai and Abu Dhabi position as premium hubs for flexible office space providers

Grade-A addresses in Dubai International Financial Centre (DIFC) rented for USD 109-116 per square foot in 2025 after currency conversion, while Abu Dhabi’s Al Maryah Island averaged USD 49-71 per square foot, underscoring the reputational premium of free-zone locations. WeWork deepened its footprint at Hub71 in Abu Dhabi, co-locating with venture funds and regulators. Ecosystem density drives pricing power rather than décor, as proximity to accelerators and sovereign wealth funds shortens startup fundraising cycles and speeds up deal flow for financiers. Future supply, such as DIFC’s USD 5.4 billion Zabeel District slated for late-decade delivery, will further cluster financial tenants and heighten demand for branded flexible suites.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Oil-cycle-driven economic volatility affects corporate spending on flexible workspace leases | -1.5% | National, with heightened sensitivity in Abu Dhabi and energy-linked sectors | Long term (≥ 4 years) |

| Premium rental costs in prime business districts limit affordability for smaller firms | -1.2% | Dubai and Abu Dhabi prime business districts | Short term (≤ 2 years) |

| High market concentration in Dubai slows flexible office adoption in smaller emirates | -0.9% | Sharjah, Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain | Medium term (2-4 years) |

| Weak public transport connectivity to emerging suburban sites reduces accessibility and demand | -0.8% | Emerging suburban and secondary locations across all emirates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Oil-cycle-driven economic volatility affects corporate spending on flexible workspace leases

Historical downcycles highlight a clear correlation between crude-price collapses and deferred real-estate decisions across energy, construction, and banking cohorts. During the 2014-2016 slump, average corporate deal sizes in Dubai sank from 14,500 sq ft to 5,900 sq ft, while lettings above 10,000 sq ft slipped from 30% to below 12% of total transactions. The 2020 dual shock of COVID-19 and Brent plunging to USD 28 per barrel triggered ADNOC to mandate USD 2 billion in cost savings within its contractor ecosystem and ultimately cut 5,000 positions, producing a 9% vacancy spike in Abu Dhabi Grade-A assets. Although Brent stabilized above USD 69 in 2025, forward curves average only USD 63.6 for 2026, sustaining board-level caution toward long-duration occupancy commitments. This sensitivity injects a structural bias toward shorter leases, heightening revenue volatility for operators entrenched in oil-linked micro-markets.

Premium rental costs in prime business districts limit affordability for smaller firms

Headline rents for Grade-A space inside DIFC and ADGM averaged USD 65 per square foot in 2025, up 7% year on year despite broader regional softening. While enterprise occupiers absorb the surcharge in exchange for prestige and proximity to regulators, freelancers and seed-stage ventures face margin compression. Operators pass through part of the rent inflation via higher service-charge components, pushing all-in desk rates to USD 580 per month, well above the GCC peer average of USD 420. Cost-sensitive users therefore gravitate toward secondary clusters such as Barsha Heights or Al Quoz, where gross rents are 30%-40% lower but public-transport connectivity is weaker. Persistently elevated CBD rentals will cap penetration rates among budget-constrained customer segments, tempering the headline growth of the UAE flexible office space market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Serviced Suites Surge as Mid-Market Firms Seek Privacy

Coworking captured 49.9% of the UAE flexible office space market share in 2025, buoyed by freelancers and remote professionals who value low-commitment monthly plans and a collaborative atmosphere. Serviced offices and executive suites, however, are forecast to grow the fastest at an 11.44% CAGR through 2031 as mid-sized firms and regional headquarters opt for turnkey privacy without capital outlay. Demand tilts toward premium addresses inside DIFC and ADGM, where compliance-sensitive industries must satisfy regulator proximity and data-security mandates. The UAE flexible office space market size for private suites is projected to expand steadily as operators reconfigure entire floors into modular clusters that can be subdivided or combined within 48 hours, an agility that traditional landlords struggle to match. IWG’s headquarters product, launched in 2025, exemplifies this shift, with floor plates pre-cabled for 10 Gbps connectivity, biometric access, and dedicated reception, enabling tenants to move in within a week.

Operators face widening margin differentials. Hot-desk coworking remains price-elastic, with day passes around USD 10 after conversion, while branded private rooms command more than USD 1,400 per seat. This divide is encouraging dual-brand strategies, with Regus and Spaces targeting cost-sensitive freelancers, while headquarters and The Executive Centre focus on enterprise clients. Occupancy analytics inform dynamic pricing; if sensors detect weekend underutilization, operators release discounted passes via mobile apps to monetize slack capacity. Over 2026-2031, the UAE flexible office space market share of open-plan coworking is expected to slide modestly as privacy-seeking mid-market firms expand headcount, yet absolute desk numbers in communal areas will still grow given the overall market uptrend.

By Sector: BFSI Adoption Accelerates Inside Financial Free Zones

Information technology and IT-enabled services controlled 40.9% of 2025 sector demand, underscoring their remote-ready workflows and global client bases. Banking, financial services, and insurance is on course for an 11.51% CAGR through 2031, the quickest among all verticals, as foreign banks and fintech startups co-locate within regulatory sandboxes at ADGM and DIFC. The UAE flexible office space market size allocated to BFSI tenants is therefore set to widen, supported by sandbox waivers that let startups test products under relaxed capital rules while accessing advisory clinics housed in the same buildings. Operators meeting ISO-22301 business-continuity norms and offering segregated network VLANs capture premium lease rates from compliance-heavy clients.

Cross-sector fertilization deepens ecosystem value. Technology consultancies cluster near banks to pitch digital-core overhauls, law firms gain proximity to deal pipelines, and accounting practices secure audit engagements, all within the same flexible campus. This agglomeration strengthens tenant retention, as a fintech that starts with four hot desks often upgrades to a 20-seat private suite within a year, increasing the operator’s lifetime value. Targeted community programming, weekly RegTech breakfast briefings, AML (anti-money-laundering) workshops, or tokenization demos serve as a non-rent revenue stream and cements market leadership. Consequently, the UAE flexible office space market share attributable to compliance-driven sectors will climb even if absolute IT headcount remains high.

By End User: Venture-Backed Startups Stake the Next Growth Wave

Freelancers held 45.9% of 2025 occupancy as designers, consultants, and content creators capitalized on remote-worker residency visas and gig-economy heat. Startups and other emerging entities are projected to grow fastest at an 11.71% CAGR through 2031, propelled by sovereign wealth-fund accelerators and VC dry-powder chasing regional tech plays. The UAE flexible office space market size allocated to venture-backed companies expands in tandem with seed-round ticket sizes, which climbed to a median USD 1.1 million in 2025, according to Hub71 disclosures. Operators support this by offering scale-up pathways, where small-team pods transition into half-floor custom suites within the same building. Subsidized packages such as Hub71’s 100% rent rebate for the first year further reduce innovation costs and accelerate adoption.

Churn risks differ across cohorts. Freelancers display month-to-month volatility tied to contract pipelines, whereas funded startups often lock 12- to 24-month terms once product-market fit materializes. Enterprise demand is driving multi-city access passes that align with HR mobility policies. Providers are segmenting offerings with evening ‘Moonlighter’ memberships for side-gig workers, growth bundles for Series A companies that include AWS credits and UX mentorship, and corporate passports that provide global desk access. This tailored mix maximizes desk yield and cushions macro shocks, strengthening the UAE flexible office space market share position of diversified operators.

Geography Analysis

Dubai captured 67.0% of the UAE flexible office space market share in 2025. Dubai’s dominance stems from its tri-airport connectivity, liberal visa regimes, and dense cluster of financial, media, and technology free zones, translating into a resilient pipeline of global headquarters mandates and venture funding in 2026.[2]Dubai International Financial Centre, “Annual Report 2025,” difc.ae. IWG alone operates 30 Dubai sites, with day offices priced from USD 10 and private suites at DIFC commanding USD 1,441 per seat, illustrating the breadth of price tiers. Complementary public initiatives, such as metro-station coworking lounges, integrate workspace into daily commutes and smooth last-mile connectivity. Abu Dhabi leverages sovereign wealth-fund backing and ADGM’s common-law framework to attract asset managers, with 27 IWG locations offering rates 15%-20% below Dubai peers yet boasting comparable Grade-A fit-outs. The emirate’s 2025 move to codify hybrid work unlocked regulatory clarity, reinforcing demand among compliance-heavy sectors.

Sharjah is forecast to grow the fastest at an 12.08% CAGR through 2031. Sharjah garners attention as a cost-optimized node within the UAE flexible office space market, with floor rents often 30% under Dubai averages and a growing number of healthcare and education tenants anchoring demand. Ras Al Khaimah and Ajman remain nascent but court operators via land grants and mixed-use incentives, epitomized by the 233-key coliving-coworking venture announced in late 2024.[3]RAK Properties, “HIVE Coliving Press Release 2024,” rakproperties.ae While logistical links and ecosystem density trail Dubai, first movers can shape standards and capture loyalty among local SMEs that previously commuted cross-emirate. Overall, geographic diversification mitigates rent-inflation risk and positions operators to tap under-served industrial clusters as hybrid work permeates the broader economy.

Competitive Landscape

Competition is moderate, with IWG and WeWork holding the largest branded footprints, yet facing nimble regional specialists that differentiate through ecosystem partnerships rather than raw desk count. Homegrown operators such as Astrolabs, Letswork, and Nasab pivot from mere space provision to market-entry platforms, earning ancillary revenue from company registration, Saudi Iqama facilitation, or curated networking programs.

Technology has become a key competitive arena, with providers embedding IoT sensors and AI dashboards to track energy savings and occupancy, supporting the ESG reporting needs of Fortune 500 tenants. Strategic alliances, such as InfraX–Zoho’s IoT rollout and RTA’s metro coworking venture, are blurring the boundaries between public infrastructure and commercial workspace, raising entry barriers for newcomers without strong technology integration or policy partnerships.

White-space opportunities endure in suburban corridors and free zones serving manufacturing, logistics, and energy clusters. Providers experimenting with hybrid residential-workspace assets, such as the Ras Al Khaimah coliving scheme, may unlock latent demand among digital nomads and project-based consultants seeking bundled living costs. The market’s next consolidation wave is likely to hinge on acquisitions of single-site boutiques offering defensible community niches, enabling scale platforms to bolt on curated memberships without diluting brand cachet.

UAE Flexible Office Space Industry Leaders

WeWork

Regus Group

Letswork

Nook

Nasab

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Abu Dhabi’s Department of Economic Development streamlined remote-work visa rules, lowering paperwork for foreign professionals earning USD 3,500 monthly.

- August 2025: IWG launched three headquarters centers in Dubai’s Jumeirah Lakes Towers and Dubai Investment Park, targeting mid-market firms with private suites and enterprise-grade IT.

- June 2025: Astrolabs partnered with Saudi Awwal Bank to bundle workspace membership with Saudi company setup and banking services.

- April 2025: Abu Dhabi Global Market amended employment rules to explicitly allow hybrid and remote work, spurring flexible-office uptake among regulated entities.

UAE Flexible Office Space Market Report Scope

By Type

| Co-Working Space |

| Serviced offices/Executive suites |

| Others (Hybrid, Virtual Office) |

By Sector

| Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) |

| Business Consulting & Professional Service |

| Other Services (Retail, Lifesciences, Energy, Legal Services) |

By End Use

| Freelancers |

| Enterprises |

| Start Ups and Others |

By City

| Dubai |

| Abu Dhabi |

| Sharjah |

| Other Emirates (Ajman, Ras Al Khaimah, Fujairah, Umm Al Quwain) |

| By Type | Co-Working Space |

| Serviced offices/Executive suites | |

| Others (Hybrid, Virtual Office) | |

| By Sector | Information Technology (IT and ITES) |

| BFSI (Banking, Financial Services and Insurance) | |

| Business Consulting & Professional Service | |

| Other Services (Retail, Lifesciences, Energy, Legal Services) | |

| By End Use | Freelancers |

| Enterprises | |

| Start Ups and Others | |

| By City | Dubai |

| Abu Dhabi | |

| Sharjah | |

| Other Emirates (Ajman, Ras Al Khaimah, Fujairah, Umm Al Quwain) |

Key Questions Answered in the Report

How large will flexible office revenues in the UAE be by 2031?

Revenues are projected to reach USD 2.01 billion by 2031, reflecting a 10.24% CAGR from 2026.

Which workspace format is expanding the fastest?

Serviced offices/executive suites are forecast to grow at an 11.44% CAGR through 2031 as mid-sized firms seek turnkey privacy.

Why is Sharjah attracting flexible office operators?

Sharjah combines 30% lower office rents than Dubai, upgraded free-zones, and proximity to major logistics corridors, supporting a 12.08% CAGR outlook.

How are government policies influencing demand?

Free-zone reforms and remote-worker visas reduce incorporation friction and widen the tenant base to startups, freelancers, and foreign project teams.

What technologies are reshaping workspace offerings?

IoT sensors, AI occupancy analytics, and cloud-based access control shift the model toward service-level agreements on energy efficiency and data security.

Page last updated on: