UAE Commercial Vehicles Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

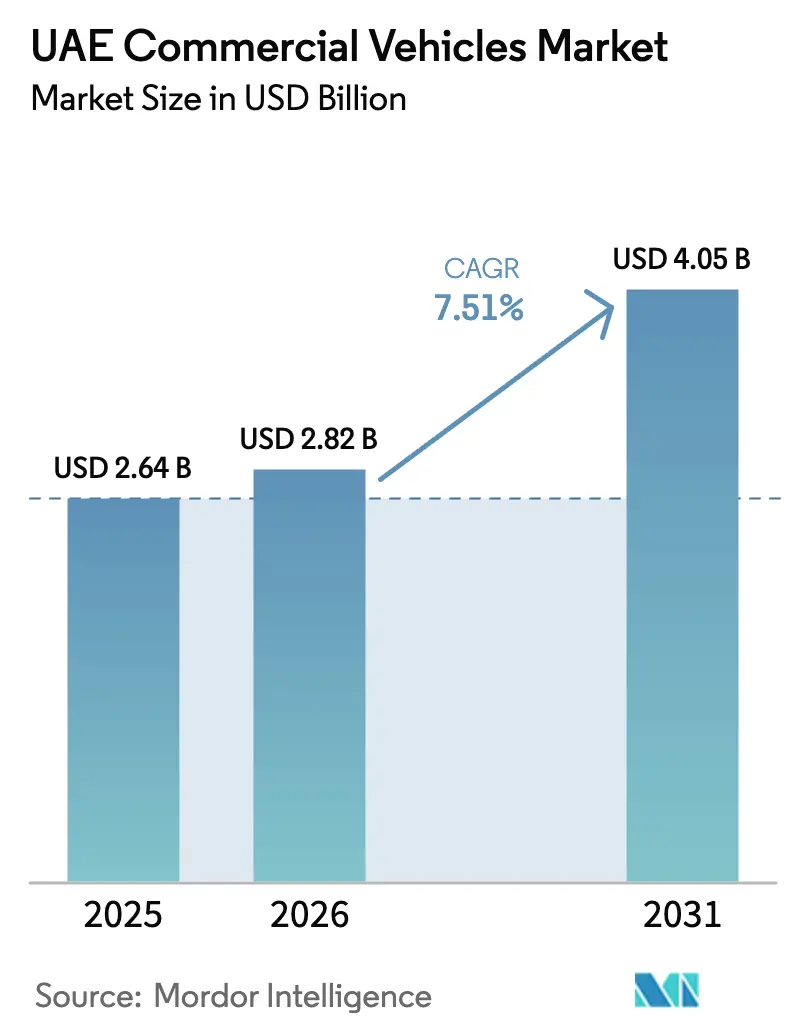

| Base Year Market Size (2025) | USD 2.64 Billion |

| Market Size (2026) | USD 2.82 Billion |

| Market Size (2031) | USD 4.05 Billion |

| Growth Rate (2026 - 2031) | 7.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Commercial Vehicles Market Analysis by Mordor Intelligence

The UAE commercial vehicles market size was valued at USD 2.64 billion in 2025 and estimated to grow from USD 2.82 billion in 2026 to reach USD 4.05 billion by 2031, at a CAGR of 7.51% during the forecast period (2026-2031). Three major shifts - Etihad Rail's establishment of an extensive freight spine, the meteoric rise of e-commerce, and proactive public-sector electrification mandates - are reshaping the landscape of fleet procurement and diversifying vehicle demand. Rail connectivity is now centralizing heavy-duty truck operations around key corridors, while Dubai's online retail market, anticipated to grow significantly in the coming years, is driving demand for light commercial vans and Class 1 pickups on busy hub-and-spoke routes. At the same time, the National Climate Change Plan is hastening the adoption of electric buses and hybrid trucks, urging municipalities to secure subsidies before they diminish. Consequently, fleet operators in the UAE are recalibrating their strategies, juggling payload flexibility, propulsion choices, and compliance demands.

Key Report Takeaways

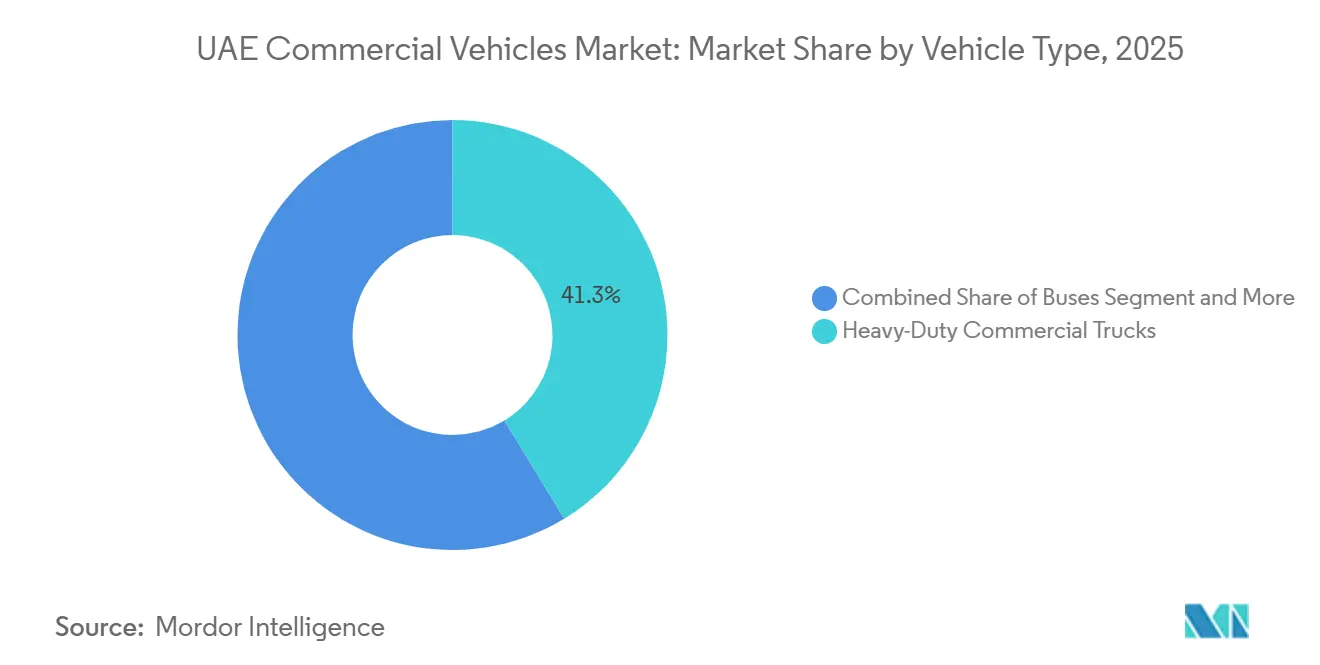

- By vehicle type, heavy-duty commercial trucks held 41.27% of the UAE commercial vehicles market share in 2025, whereas buses will post the fastest vehicle-type growth at 7.55% CAGR through 2031.

- By propulsion type, electric propulsion will record the sharpest growth at 7.61% CAGR, even though internal combustion engines retained 63.37% of the overall propulsion mix in 2025.

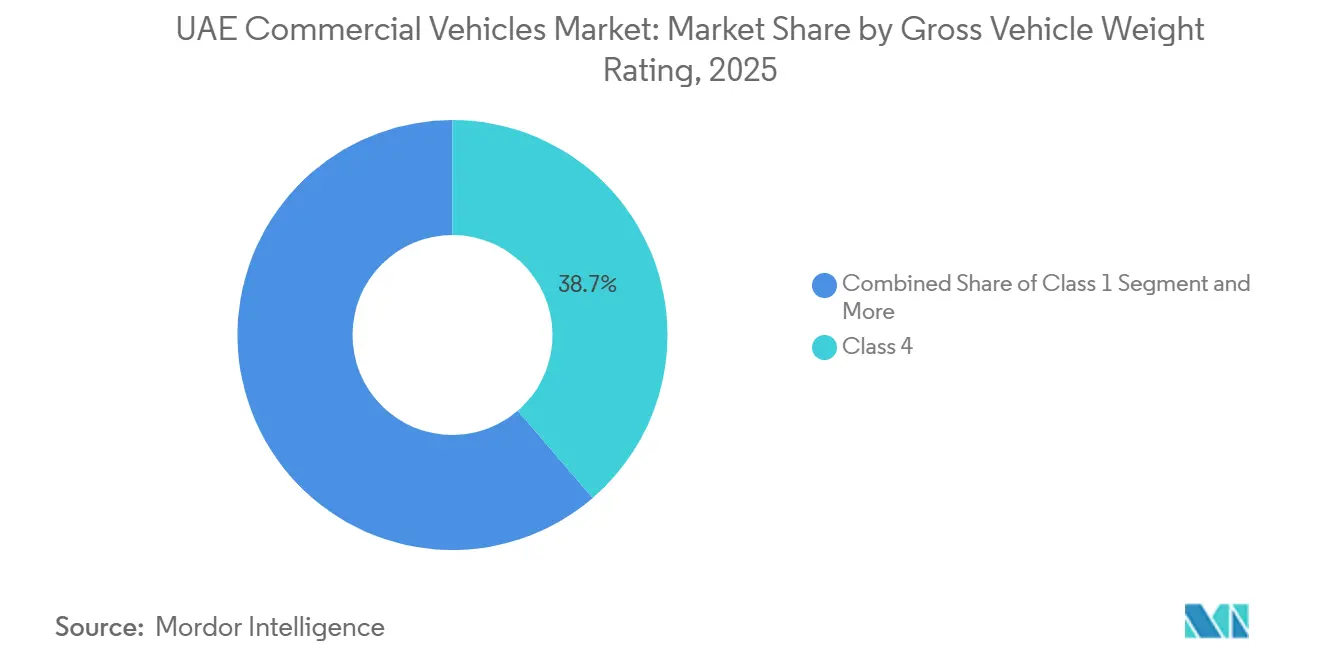

- By gross vehicle weight rating, Class 4 vehicles (7.5–16 tonnes) accounted for 38.71% of the UAE commercial vehicles market size in 2025, but Class 1 pickups are forecast to expand at a 7.64% CAGR between 2026 and 2031.

- By end-use industry, logistics and e-commerce commanded 53.27% share of the UAE commercial vehicles market size in 2025, yet public transport is projected to advance at 7.59% CAGR through 2031.

- By region, Dubai captured 43.37% of regional demand in 2025; it is also set to deliver the highest regional CAGR at 7.57% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Commercial Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multimodal Freight Corridors (Etihad Rail Connection) | +2.1% | National, strongest in Abu Dhabi and Northern Emirates | Medium term (2-4 years) |

| Rapid Urbanization and E-Commerce Boom | +1.8% | Dubai, Abu Dhabi, Sharjah | Short term (≤ 2 years) |

| Public-Sector Fleet Electrification Targets | +1.5% | Dubai, Abu Dhabi | Long term (≥ 4 years) |

| Expo City Dubai Logistics Legacy | +1.2% | Dubai, spillover to Sharjah | Medium term (2-4 years) |

| High Residual-Value Financing Packages by OEM Captives | +1.0% | National | Short term (≤ 2 years) |

| Dedicated "Smart and Autonomous Vehicle" Sandbox Zones | +0.8% | Dubai, potential spillover to Abu Dhabi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Multimodal Freight Corridors (Etihad Rail Connection)

Etihad Rail’s completion in 2024 is expected to shift long-haul tonnage from roads to rail, thereby narrowing truck operations to high-utilization shuttles between ports, rail depots, and distribution centers. Fleet operators can now defer heavy-duty truck replacement by an extra year or so, creating a bow-wave of synchronized end-of-life assets in 2027–2028. The rail spine also unlocks industrial zones in Ras Al Khaimah and Fujairah, stimulating incremental demand for construction and municipal vehicles in those emirates. Compliance with ISO 668 intermodal standards is fast becoming mandatory for carriers bidding on contracts tied to the rail network, further concentrating market power in the UAE commercial vehicles market [1]“Etihad Rail Completes National Network,” Etihad Rail, etihadrail.ae .

Rapid Urbanization and E-Commerce Boom

In metropolitan Dubai and Abu Dhabi, the push for same-day delivery is shortening the replacement cycles for light commercial vans and Class 1 pickups, often by a significant margin compared to historical norms. Fulfillment centers located around Expo City Dubai and Dubai South enable carriers to reach urban consumers in a very short time. This efficiency is driving operators to expand their fleets, even with high asset utilization. There's a noticeable spillover demand into Sharjah, fueled by a significant rise in cross-emirate e-commerce flows, which in turn has increased the kilometers light-duty vehicles travel on shared corridors. Larger logistics players are capitalizing on scale advantages, securing vehicles at highly competitive financing rates. In contrast, smaller firms grapple with much higher leasing costs, creating a pronounced barrier to entry. Highlighting the capital intensity needed to stay competitive, dnata has made a notable investment in a large warehouse at Dubai South [2]“dnata Opens New Warehouse at Dubai South,” dnata, dnata.com .

Public-Sector Fleet Electrification Targets

By the middle of the century, federal and emirate authorities aim for a significant transition, with a majority of buses becoming electric and a substantial portion of trucks being either plug-in or hybrid. However, with subsidy windows encouraging faster procurement, the focus is on the near term. In recent years, Dubai's RTA has placed a substantial order for buses, which prominently included several electric units from Zhongtong. This move highlights the public's willingness to accommodate the current premium on total cost of ownership. Meanwhile, Abu Dhabi's Green Bus Programme, which introduced electric and fuel-cell buses, is serving as a platform to validate these technologies for private fleets. Operators delaying adoption risk being excluded from municipal tenders, which now require zero-emission vehicles as a qualification. The Road2.0 initiative, starting with a pilot of commercial electric vehicles and aiming for significant expansion in the future, underscores a steep learning curve that benefits early adopters in the UAE's commercial vehicle landscape [3]“RTA Awards AED 1.1 Billion Bus Contract,” Roads & Transport Authority, rta.ae.

Expo City Dubai Logistics Legacy

Expo City’s master plan converts the former World Expo grounds into a permanent logistics and technology hub linked to Al Maktoum International Airport and Jebel Ali Port. Dedicated freight lanes and a 15-kilometer autonomous-vehicle zone pull medium-duty refrigerated trucks and light vans into dense urban loops that promise sub-30-minute delivery times in southern Dubai. On-site hydrogen production via DEWA’s 1.25-megawatt PEM electrolyser offers a proof-of-concept for fuel-cell fleets, helping alleviate range anxiety. The model is now influencing Sharjah and Abu Dhabi, both of which have announced logistics parks with similar multimodal connectivity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver-Shortage Wage Inflation | -0.9% | National | Medium term (2-4 years) |

| Growing Rental and Ride-Share Penetration | -0.7% | Dubai, Abu Dhabi | Short term (≤ 2 years) |

| Delayed Hydrogen-Refuelling Roll-Out | -0.6% | National | Long term (≥ 4 years) |

| Cargo-Only VAT Loophole Sunset (2027) | -0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Driver-Shortage Wage Inflation

In 2025, heavy-truck driver wages experienced a significant increase compared to the previous year, putting pressure on operating margins for carriers bound by long-term contracts, which were priced based on older cost assumptions. Additionally, retention programs, incorporating housing allowances and bonuses, have further escalated costs for carriers. While interest in autonomous trucks is on the rise, regulatory frameworks are still confined to a limited autonomous zone in Dubai, primarily catering to passengers. Consequently, this labor bottleneck is causing delays in project timelines, particularly in the construction and municipal services sectors.

Growing Rental and Ride-Share Penetration

Fleet-rental platforms are enabling small logistics firms to swap fixed capital outlays for variable operating expenses. This shift has led to a significant decline in outright unit sales. In the UAE commercial vehicles market, a single rental vehicle, serving multiple lessees over its economic life, dampens net new demand. Rental operators, securing substantial volume discounts from original equipment manufacturers, challenge the residual-value assumptions of captive-finance arms. This, in turn, inflates the total cost of ownership for retail buyers. Furthermore, the shared-fleet model is hastening the adoption of telematics and predictive maintenance. Rental companies, by amortizing this technology across vast asset pools, are widening the efficiency gap compared to owner-operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Buses Lead Electrification Wave

Buses recorded the fastest growth trajectory, advancing at 7.55% CAGR through 2031 on the back of municipal orders that prioritize zero-emission fleets. RTA’s 2025 contract for multiple units, including 40 electric Zhongtong models, marks a significant commitment. Meanwhile, heavy-duty trucks retained 41.27% of the UAE commercial vehicles market in 2025, owing to the continuing dominance of port-to-hinterland freight and construction haulage. Etihad Rail’s expansion is expected to redirect part of long-haul cargo to rail, moderating heavy-duty truck demand but intensifying usage in first- and last-mile roles.

Light commercial vans and pickups remain indispensable for e-commerce fulfillment. Electric entrants such as the Dongfeng EV400, distributed by Al Masaood from April 2024, demonstrate a rising appetite for low-emission configurations. Public bus electrification is also lowering technology-risk perceptions across private fleets, easing future adoption across other vehicle classes. Complementary hydrogen bus pilots in Abu Dhabi hedge against infrastructure bottlenecks, while improved maintenance networks help close the total-cost-of-ownership gap between electric and diesel options in the UAE commercial vehicles market.

By Propulsion Type: Electric Variants Outpace Internal Combustion Engine

Electric propulsion is projected to grow at a 7.61% CAGR through 2031, the steepest rise among all propulsion categories, yet diesel and CNG engines still claimed 63.37% of 2025 deliveries. The Road2.0 program’s target of massive electric commercial vehicles by 2030 translates into an annual rise in registrations, especially for urban delivery and municipal fleets. Battery-electric trucks and buses are penetrating shorter-range operations, evidenced by DHL’s deployment of the Mercedes-Benz eActros 300 and BEEAH Group’s use of eEconic refuse trucks.

Fuel-cell models face infrastructure constraints because ADNOC’s Masdar City H2GO station remains the only high-speed green hydrogen pump. Hybrid and plug-in hybrid powertrains fill the interim gap, offering operational flexibility while range anxiety and charging-time challenges remain unresolved. Tata Motors and Ashok Leyland’s 2025 Gulf launches, which include Euro 6-compliant and electric variants, illustrate intensifying competition within the UAE commercial vehicles market as propulsion technologies diversify.

By Gross Vehicle Weight Rating: Class 1 Pickups Surge

Class 1 vehicles below 1.8 tonnes are poised to climb at a 7.64% CAGR through 2031 as last-mile delivery and utility services multiply in dense urban centers. Conversely, Class 4 trucks (7.5–16 tonnes) held 38.71% of 2025 demand but face deceleration as rail shifts reduce long-haul trucking mileage on inter-emirate routes. Class 2 and Class 3 trucks maintain relevance for mid-range urban freight.

Class 5 heavy vehicles exceed 16 tonnes and tackle port-to-hinterland freight. Volvo’s FMX, unveiled in May 2025 with a 58-tonne gross rating, underscores payload maximization trends. Ton-class bifurcation is clear: operators either downsize to nimble vans for inner-city work or upsize to high-capacity rigs for fewer but heavier trips, squeezing medium-duty volumes. Weight-station enforcement by Abu Dhabi’s Integrated Transport Centre reinforces compliance, prompting right-sizing strategies across the UAE commercial vehicles market.

By End-Use Industry: Public Transport Gains Momentum

Logistics and e-commerce represented 53.27% of 2025 demand as online retail expanded and industrial output rebounded. However, public transport is on track to deliver the fastest segmental CAGR at 7.59% through 2031, driven by large-scale bus procurement and mandated zero-emission targets. Construction and mining demand remains cyclical but benefits from municipal vehicle modernization, as seen in Abu Dhabi’s adoption of high-tech cleaning trucks by the end of 2025.

Electric public bus fleets create economies of scale for charging infrastructure that adjacent private segments can leverage. Hydrogen bus trials supplement battery-electric deployments, building optionality for routes where depot charging is unfeasible. Logistics firms, seeing municipal electrification success, have begun adding electric delivery vans where maintenance savings offset the 10%-to-20% cost premium. This reinforcement loop accelerates technology diffusion within the UAE commercial vehicles market.

Geography Analysis

Dubai dominated with 43.37% of 2025 demand and is forecast to expand at a 7.57% CAGR through 2031. Jebel Ali Port processed a huge customs declaration in 2022, and Dubai Customs cleared an average of 260 trucks daily through Hatta Border in the first half of 2023, underscoring throughput intensity. RTA’s front-loaded bus procurement and the 15-kilometer autonomous-vehicle zone position the emirate as a regulatory sandbox that accelerates technology adoption.

Abu Dhabi trails in volume yet leads in zero-emission initiatives. The Green Bus Programme placed Volvo battery-electric and Hyundai fuel-cell buses into service in 2025, supported by ADNOC’s Masdar City hydrogen station. By the end of 2025, hundreds of smart municipal vehicles had been deployed, underscoring continued public investment. Sharjah captures spillover logistics volumes due to proximity to Dubai’s southern logistics belt and operates Mercedes-Benz eEconic refuse trucks through BEEAH Group.

Industrial corridors unlocked by Etihad Rail extend modern fleet requirements into Ras Al Khaimah, Fujairah, and Ajman. Northern-emirate operators now face ISO 668 compliance mandates when bidding on national freight contracts, further integrating those markets into the broader UAE commercial vehicles market.

Competitive Landscape

European giants - Mercedes-Benz, Volvo, Scania, and MAN - continue to dominate the heavy-duty and premium bus sectors, leveraging legacy distributor partnerships and offering residual-value guarantees. Meanwhile, Chinese manufacturers are swiftly making inroads, particularly in the lower-tonnage and electric segments. In early 2024, Al Masaood, through its exclusive Dongfeng distributorship, rolled out an electric truck alongside diesel pickups. Concurrently, King Long and Foton broadened their minibus and school bus portfolios via local agents. Data from AutoData highlighted a significant surge in demand for Chinese brands over the past year, elevating their market share from a modest presence to a more notable position.

Japanese manufacturers, including Hino, Isuzu, and Mitsubishi Fuso, are emphasizing fuel efficiency and durability in the medium-duty segment. Al Habtoor Motors recently received recognition for its performance as a distributor, underscoring the brand's solid market presence. The technological arena has emerged as the primary battleground. In mid-2025, Einride rolled out an upgraded electric truck for DP World Dubai, eyeing a broader vision of deploying a substantial number of electric and autonomous vehicles within its Falcon Rise grid. Meanwhile, nimble players like Switch Mobility are carving a niche by offering comprehensive electrification solutions, encompassing vehicles, charging infrastructure, and maintenance services.

Potential growth areas include electric light commercial vans, fuel-cell trucks for intercity transport (especially as hydrogen retailing gains traction), and the integration of autonomous vehicles in line with Dubai's sandbox regulations. OEMs that can finance ISO 668-compliant trailers and container chassis stand to gain a significant procurement advantage. Navigating these strategic niches could be the key to securing a competitive edge in the UAE's commercial vehicle landscape.

UAE Commercial Vehicles Industry Leaders

Mercedes Benz Group

Volvo Group

Tata Motors

Dongfeng Commercial Vehicle Company Limited

Volkswagen AG (MAN Truck & Trucks)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Baidu Apollo Go established its first overseas “Apollo Go Park” in Dubai to manage a planned fleet of 1,000 autonomous vehicles.

- March 2025: BYD recently introduced the T5 light-duty truck, ETH8 medium-duty truck, and B12 all-electric bus, specifically designed to cater to the needs of Gulf fleets. These vehicles aim to enhance operational efficiency and promote sustainable transportation solutions in the region.

UAE Commercial Vehicles Market Report Scope

The scope of the report includes Vehicle Type (Buses, Heavy-Duty Commercial Trucks, Medium-Duty Commercial Trucks, Light Commercial Pick-Up Trucks, and Light Commercial Vans), Propulsion (Electric and Internal Combustion Engine), Gross Vehicle Weight Rating (Class 1, Class 2, Class 3, Class 4, and Class 5), End-Use Industry (Logistics and E-Commerce, Construction and Mining, Public Transport, Utilities and Minicipal Services, and Others (Agriculture and Retail)), and By Region (Abu Dhabi, Dubai, Sharaj, Rest of United Arab Emirates.

| Buses |

| Heavy-Duty Commercial Trucks |

| Medium-Duty Commercial Trucks |

| Light Commercial Pick-up Trucks |

| Light Commercial Vans |

| Electric | Battery Electric |

| Fuel-cell Electric | |

| Hybrid Electric | |

| Plug-in Hybrid Electric | |

| Internal Combustion Engine (ICE) | Diesel |

| Compressed Natural Gas (CNG) | |

| Gasoline | |

| Liquefied Petroleum Gas (LPG) |

| Class 1 (Below 1.8 t) |

| Class 2 (1.8–3.5 t) |

| Class 3 (3.5–7.5 t) |

| Class 4 (7.5–16 t) |

| Class 5 (Above 16 t) |

| Logistics & E-commerce |

| Construction & Mining |

| Public Transport |

| Utilities & Municipal Services |

| Others (Agriculture, Retail) |

| Abu Dhabi |

| Dubai |

| Sharjah |

| Rest of United Arab Emirates |

| By Vehicle Type | Buses | |

| Heavy-Duty Commercial Trucks | ||

| Medium-Duty Commercial Trucks | ||

| Light Commercial Pick-up Trucks | ||

| Light Commercial Vans | ||

| By Propulsion Type | Electric | Battery Electric |

| Fuel-cell Electric | ||

| Hybrid Electric | ||

| Plug-in Hybrid Electric | ||

| Internal Combustion Engine (ICE) | Diesel | |

| Compressed Natural Gas (CNG) | ||

| Gasoline | ||

| Liquefied Petroleum Gas (LPG) | ||

| By Gross Vehicle Weight Rating (Tonnage Class) | Class 1 (Below 1.8 t) | |

| Class 2 (1.8–3.5 t) | ||

| Class 3 (3.5–7.5 t) | ||

| Class 4 (7.5–16 t) | ||

| Class 5 (Above 16 t) | ||

| By End-Use Industry | Logistics & E-commerce | |

| Construction & Mining | ||

| Public Transport | ||

| Utilities & Municipal Services | ||

| Others (Agriculture, Retail) | ||

| By Region | Abu Dhabi | |

| Dubai | ||

| Sharjah | ||

| Rest of United Arab Emirates | ||

Key Questions Answered in the Report

How large is the UAE commercial vehicles market in 2026?

The UAE commercial vehicles market size stood at USD 2.82 billion in 2026 and is forecast to reach USD 4.05 billion by 2031.

What is the projected growth rate for commercial vehicle sales in the UAE?

Overall demand is expected to rise at a 7.51% CAGR between 2026 and 2031.

Which vehicle type will expand fastest in the near term?

Buses, propelled by municipal electrification programs, are forecast to grow at a 7.55% CAGR through 2031.

How are electric models performing compared with diesel units?

Electric variants are the fastest growing propulsion class, with a 7.61% CAGR forecast, even though diesel still dominates absolute volumes.

Which emirate is leading the adoption of zero-emission fleets?

Abu Dhabi is advancing rapidly through its Green Bus Programme and the UAE’s first high-speed hydrogen station at Masdar City.

What is the main competitive threat to established OEMs?

Rapid gains by Chinese brands and technology-centric entrants offering turnkey electrification and autonomous solutions are reshaping competitive dynamics.

Page last updated on: