Market Overview

| Study Period | 2019 - 2030 |

|---|---|

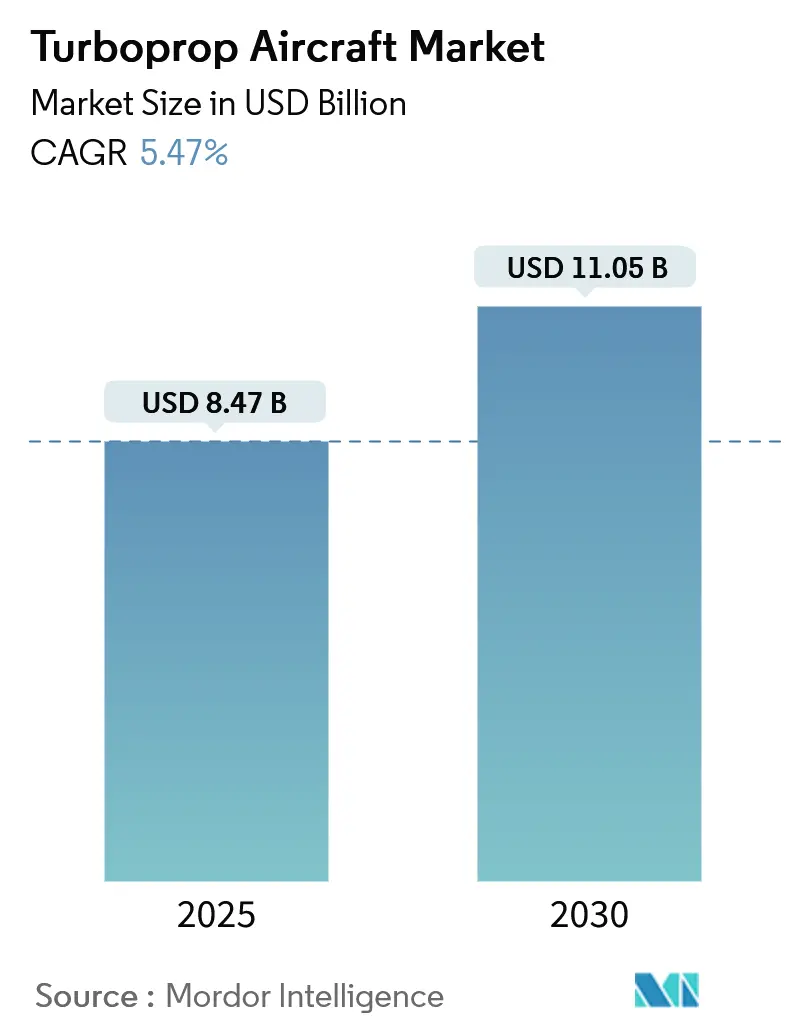

| Market Size (2025) | USD 8.47 Billion |

| Market Size (2030) | USD 11.05 Billion |

| Growth Rate (2025 - 2030) | 5.47% CAGR |

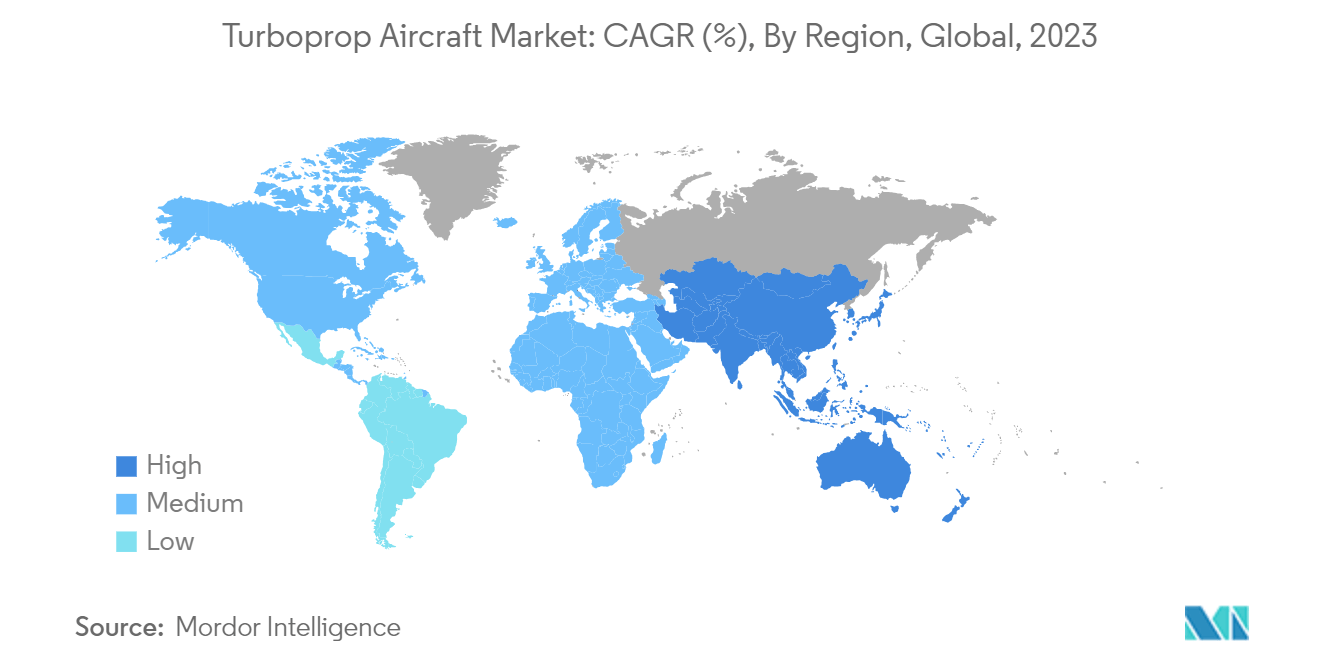

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Turboprop Aircraft Market Analysis by Mordor Intelligence

The Turboprop Aircraft Market size is estimated at USD 8.47 billion in 2025, and is expected to reach USD 11.05 billion by 2030, at a CAGR of 5.47% during the forecast period (2025-2030).

Turboprop aircraft excel in short-distance, low-altitude flights, making them a preferred choice for regional air passenger traffic. As airlines introduce new regional routes, the demand for these aircraft rises, propelling market growth. Armed forces are modernizing their fleets in the military sector by replacing aging transport and training aircraft with newer, more advanced models. This shift is set to boost the market further during the forecast period.

One of the primary drivers of the turboprop market is the increasing demand for regional connectivity. As economies develop, especially in emerging markets, the need for efficient, cost-effective short-haul travel rises. Turboprop aircrafts, known for their fuel efficiency and suitability for shorter routes, are well-suited to meet this demand. Furthermore, ongoing advancements in turboprop technology, such as innovations in engine efficiency, lightweight materials, and avionics, enhance the aircraft's performance, safety, and environmental footprint. This, in turn, makes them more appealing to operators looking to modernize their fleets.

Moreover, the market is witnessing a push from the growing emphasis on sustainable aviation. Turboprop aircraft, being more fuel-efficient than their jet counterparts, produce lower carbon emissions, aligning well with global environmental goals. As regulatory bodies tighten emissions standards, airlines are increasingly turning to turboprops to meet these requirements while maintaining operational efficiency.

However, the market does face challenges. Notably, competition from regional jets, which offer faster travel times and are favored for longer routes, poses a threat. Additionally, the relatively higher noise levels of turboprop engines compared to jets can be a concern, especially in noise-sensitive regions and urban airports. These factors may influence airlines' decisions when selecting aircraft for their fleets.

Despite these challenges, the market sees a significant opportunity in regional air cargo. The surge in e-commerce and the subsequent demand for swift, reliable delivery services are fueling the need for efficient cargo transportation solutions. Turboprop aircraft, with their ability to operate from shorter runways and remote locations, are well-suited for this task. By leveraging this versatility, manufacturers and operators can tap into the growing logistics and express delivery market, opening new revenue streams and enhancing market penetration.

Global Turboprop Aircraft Market Trends and Insights

Military Segment to Dominate Market Share During the Forecast Period

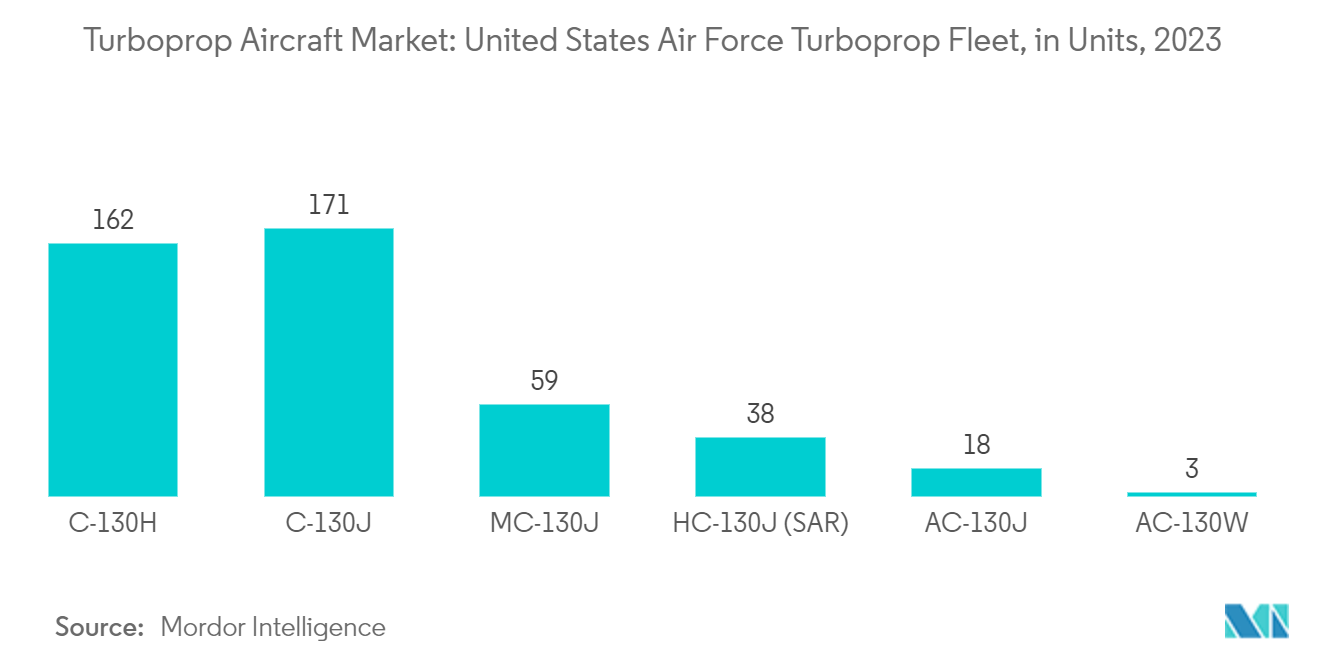

In 2023, the military segment held a significant market share, largely driven by large turboprop aircraft like the A400M and C-130J deliveries. For instance, the Airbus A400M Atlas, a four-engine turboprop transport aircraft, was developed to replace older European transport aircraft. These turboprops, beyond transport, find deployment in a wide array of combat and non-combat roles.

These aircraft are pivotal in various military applications, including surveillance, reconnaissance, transport, and training. Their versatility, cost-efficiency, and operational capabilities make them globally indispensable assets for armed forces. With technological advancements, modern military turboprops are increasingly equipped with sophisticated avionics, enhanced payload capacities, and improved performance metrics, further solidifying their role in military operations.

Strategically, compared to jet-powered aircraft, the cost-effective operation and maintenance of turboprops is a significant advantage. Their ability to operate from shorter, less-prepared runways makes them ideal for diverse and challenging environments, enhancing their utility in various military missions. Moreover, amidst ongoing geopolitical tensions and global defense modernization programs, investments in upgrading and expanding military turboprop fleets are on the rise. The adaptability of these aircraft for multiple roles-from tactical transport to maritime patrol-ensures their continued relevance and demand in military applications.

Various procurement programs by armed forces worldwide, aimed at enhancing their aerial capabilities through fleet modernization, are set to drive the market's growth. For example, in November 2023, Textron Aviation secured a substantial USD 100 million contract with the US Army Contracting Command under the Foreign Military Sales (FMS) program, providing various turboprop aircraft models, including the Cessna SkyCourier, Cessna Grand Caravan EX, and Beechcraft King Air.

North America to Dominate Market Share During the Forecast Period

North America currently leads the market and is poised to maintain its dominance, driven by the increasing demand for turboprop fleets in the US for commercial, military, and general aviation. While the region has fewer turboprop aircraft for passenger transport, commercial operators are acquiring new ones for cargo transportation. North America's well-established aviation infrastructure and high demand for regional air connectivity drive substantial investments in turboprop aircraft.

Major airlines in the US and Canada leverage turboprops for their fuel efficiency and operational cost-effectiveness, especially on short-haul and regional routes. This adoption is further bolstered by the region's robust air travel network and numerous regional airports, ideal for turboprop operations. The US military, particularly, relies on turboprop aircraft for various missions, from tactical airlift to intelligence, surveillance, and reconnaissance, given their versatility, operational capabilities, and lower costs than jets.

Additionally, North America's leading turboprop manufacturers and a well-developed supply chain enhance the region's capacity to produce and maintain advanced turboprop aircraft, ensuring a steady supply both domestically and internationally. The region's strong private aviation culture, coupled with a large number of private pilots and owners, further drives demand for turboprop aircraft for personal and business use.

Favourable regulations and access to financing options make it easier for individuals and businesses to invest in turboprop aircraft, further solidifying North America's market dominance. For instance, in June 2023, Embraer's 20-year Market Outlook highlighted a robust demand for new turboprop aircraft in the US commercial aviation sector, projecting a need for 2,210 new turboprops globally, with a significant portion destined for North America, driven by the region's growing need for regional connectivity and a shift towards more fuel-efficient aircraft.

Competitive Landscape

The turboprop aircraft market is semi-consolidated, with several key players holding significant market shares. Notable players include ATR, Airbus SE, Textron Aviation Inc., Pilatus Aircraft Ltd, and Lockheed Martin Corporation. Textron Aviation Inc., through its Beechcraft and Cessna brands, offers a diverse range of turboprops catering to commercial and general aviation. Pilatus Aircraft, known for its PC-12 and PC-24 models, targets niche markets, especially in private and special mission operations, leveraging its reputation for high performance and versatility.

These companies expand globally, forming partnerships with regional airlines and defense contractors to tap into emerging markets and secure long-term contracts. These key players maintain a competitive edge in the dynamic turboprop aircraft market by aligning their strategies with market demands and technological trends. For instance, Embraer, in the next two years, is set to develop a new executive or commercial aircraft, a separate effort from its potential longer-term development of aircraft with novel propulsion systems. Additionally, under its Energia program, Embraer is exploring the development of four aircraft with new propulsion technologies, with two featuring hybrid-electric systems and two powered by hydrogen fuel cells.

Turboprop Aircraft Industry Leaders

-

Airbus SE

-

ATR

-

Lockheed Martin Corporation

-

Textron Aviation Inc.

-

Pilatus Aircraft Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2024: Avation PLC and ATR inked a 10 ATR 72-600s deal, extending purchase rights for an additional 24 until 2034. These aircraft, fully compatible with sustainable aviation fuel (SAF), are scheduled for delivery between the last quarter of 2025 and the first quarter of 2028, aligning with airline demand and ATR's production capacity.

- May 2023: The Ministry of Defence of Malaysia awarded Leonardo S.p.A. a contract to supply two ATR 72 MPA (Maritime Patrol Aircraft) platforms.

Global Turboprop Aircraft Market Report Scope

Turboprop aircraft have one or more gas-turbine engines connected to a gearbox that will turn the propeller to enable the movement of the aircraft on the ground and through the air.

The turboprop plans market is segmented by application and geography. The market is segmented based on application into military aviation, commercial aviation, and general aviation. The report also covers the market sizes and forecasts for the weapons and ammunition market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

Application

| Military Aviation |

| Commercial Aviation |

| General Aviation |

Geography

| North America | United States |

| Canada | |

| Europe | United Kingdom |

| France | |

| Germany | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Latin America | Brazil |

| Rest of Latin America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Egypt | |

| Rest of Middle East and Africa |

| Application | Military Aviation | |

| Commercial Aviation | ||

| General Aviation | ||

| Geography | North America | United States |

| Canada | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Latin America | Brazil | |

| Rest of Latin America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Turboprop Aircraft Market?

The Turboprop Aircraft Market size is expected to reach USD 8.47 billion in 2025 and grow at a CAGR of 5.47% to reach USD 11.05 billion by 2030.

What is the current Turboprop Aircraft Market size?

In 2025, the Turboprop Aircraft Market size is expected to reach USD 8.47 billion.

Who are the key players in Turboprop Aircraft Market?

Airbus SE, ATR, Lockheed Martin Corporation, Textron Aviation Inc. and Pilatus Aircraft Ltd. are the major companies operating in the Turboprop Aircraft Market.

Which is the fastest growing region in Turboprop Aircraft Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Turboprop Aircraft Market?

In 2025, the North America accounts for the largest market share in Turboprop Aircraft Market.

What years does this Turboprop Aircraft Market cover, and what was the market size in 2024?

In 2024, the Turboprop Aircraft Market size was estimated at USD 8.01 billion. The report covers the Turboprop Aircraft Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Turboprop Aircraft Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: