Market Trends of Transparent Conductive Films Industry

Indium Tin Oxide (ITO) on Glass to Dominate the Market

- Indium tin oxide is a ternary composition of indium, tin, and oxygen in various proportions, and depending upon the oxygen content, it can be described as an alloy or a ceramic. In preparation of indium tin oxide, almost 45% of indium is used.

- It is widely used as transparent conducting oxide owing to its optical transparency and electrical conductivity, and it can be deposited as a thin film.

- Indium tin oxide on glass is highly transparent and possesses excellent electrical conductivity. It offers excellent light transmittance from the visible to the near-infrared range.

- Superior properties of indium tin oxide on glass, such as low micro roughness, excellent homogeneity of the electrical surface resistance, reflection for infrared wavelengths, excellent coating adhesion and abrasion resistance, and high uniformity of optical transmittance, making it ideal for thermal conductive films.

- Indium tin oxide on glass includes various applications such as LED and OLED displays, micro structuring applications, heat-able microscope slides, and coverslips for medical technology. It can also be applied as circuit substrates for electronics, optical and conductive transparent coatings for touch screen and touch-sensitive display technology, conductive coatings for transparent electrodes, organic solar cells, infrared mirrors, reflective infrared filters, de-icing windows and anodes for organic LEDs (OLED).

- ITO thin films for glass substrates are increasingly used in glass windows to conserve energy.

- However, indium oxide coatings are not recommended for continued exposure to temperatures more than 300°F or 150°C in oxygen or air atmospheres, which may result in undesired changes in resistivity. ITO is considered brittle, lacks flexibility, and the fabrication process involves high temperatures and a vacuum. Therefore, it is relatively slow and not cost-effective, likely decreasing the demand for ITO on glass films in the coming years.

- Moreover, indium, the main material of ITO films, is a rare metal and unevenly distributed. Therefore, there is a risk in terms of stable supply, as well as the issue of increasing prices.

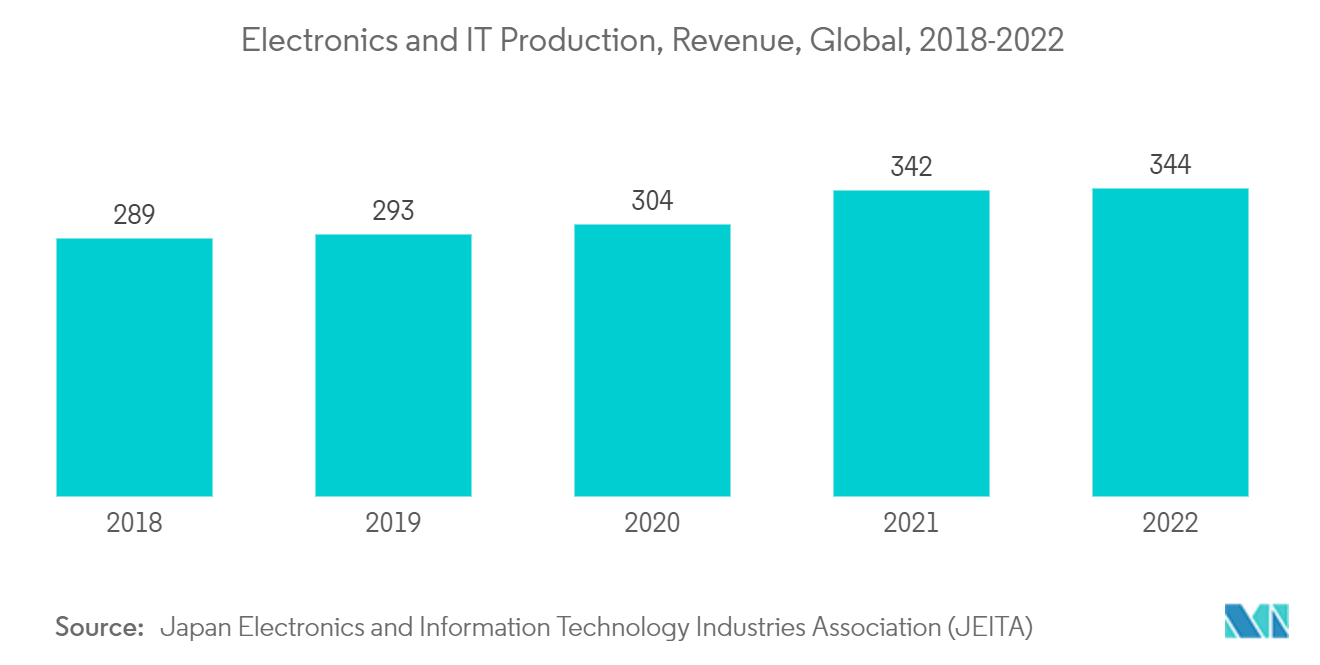

- According to the Japan Electronics and Information Technology Industries Association (JEITA), the production by the global electronics and IT industry was estimated at USD 3,436.8 billion in 2022, registering a growth rate of 1% year on year, compared to USD 3,360.2 billion in 2021. Moreover, the industry is expected to reach USD 3,436.8 billion, with a growth rate of 3% year on year, by 2023.

- Globally, the demand for smartphones is increasing at a significant rate. According to the Telefonaktiebolaget LM Ericsson, the number of smartphone subscriptions globally was estimated to reach 7,690 million by 2027 from 6,259 million in 2021. This factor will support the favorable demand for using transparent conductive films from electronics applications.

- While there is significant work on thin metal nanowire grids, conductive polymers, carbon nanotubes, and graphene to develop transparent conducting oxides with lower sheet resistances for higher speed performance, projections still suggest a significant demand for ITO based films owing to its properties in the coming years.

Understand The Key Trends Shaping This Market

Download PDF

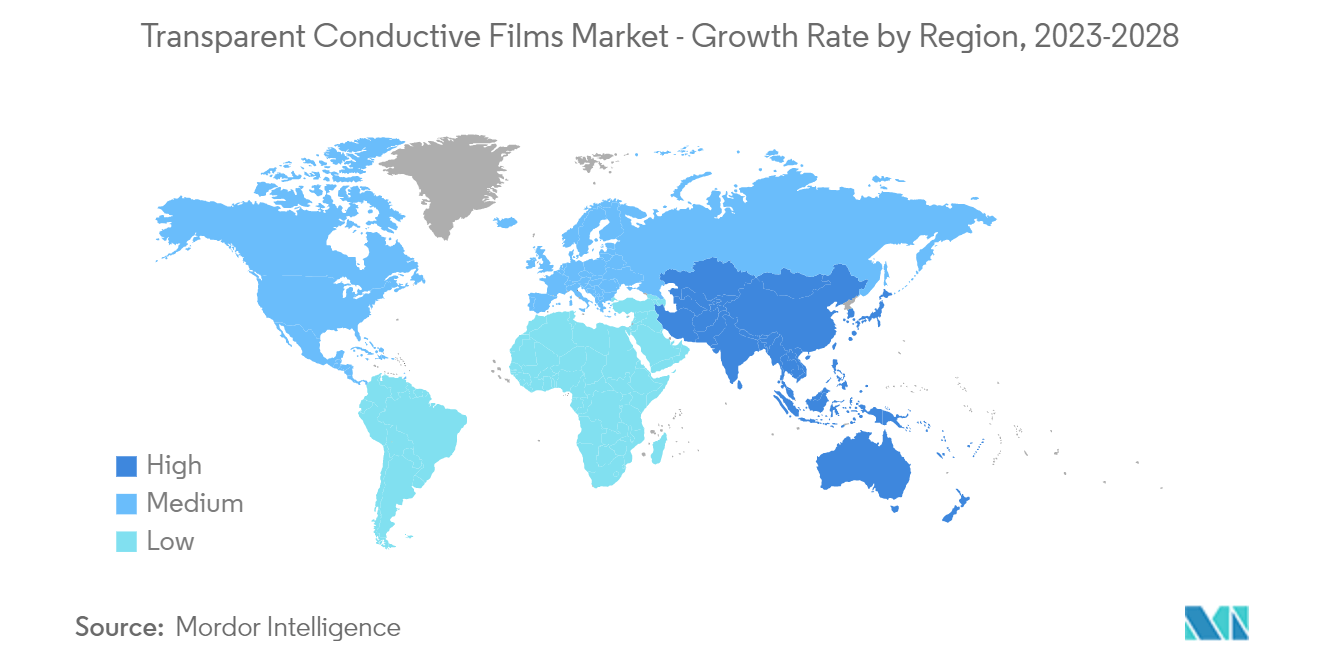

China to Dominate the Asia-Pacific Market

- China is the world's largest economy in terms of PPP (purchasing power parity). However, when calculated in terms of nominal GDP, it is the second-largest economy. The country's growth slowed in the past few years, and it recorded 6% GDP growth in 2019, the slowest rate in the country's economic history since 1990. This growth rate is moderating due to the maturing of China's economy and tensions over the country's trade disputes with the United States.

- The demand for transparent conductive films from the electronics industry is also very high owing to the advantage of producing versatile shape products and complex models using injection molding that fits the electronics industry's needs. China is the largest base for electronics production in the world. China is actively manufacturing electronic products, such as smartphones, TVs, wires, cables, portable computing devices, gaming systems, and other personal devices.

- The continuous income growth resulted in a rise in the population's per capita disposable income, which is expected to benefit the demand for electronic goods in China. The expansion of the middle and high-income populations is expected to propel the demand for electronics. According to the National Bureau of Statistics of China, the revenue in the consumer electronics and household appliances segment is expected to show an annual growth rate of 2.04%, resulting in a projected market volume of USD 175,670 million by 2025.

- China embarked on strategic initiatives like the 'Made in China 2025' plan to benefit from the extensive demand scenario. Under this, the Chinese government announced its goal to reach an output of USD 305 billion by 2030 and meet 80% of its domestic demand.

- A similar trend as that in the smartphone market is also observed in the laptop market. The production shift is less drastic than that of smartphones, but many laptop manufacturers are planning to move their manufacturing bases out of China. HP is planning to move almost one-third of its capacity from China to other Asian countries.

- China is also looking to dramatically increase the proportion of solar energy in its power mix. It is expected to create a huge demand for transparent conductive films in the country during the forecast period.

- However, COVID-19 downsized the demand for electronics in China, and this trend is expected to continue even after the pandemic during the forecast period. Such factors are expected to slow down this industry's demand for transparent conductive films.

Get Analysis on Important Geographic Markets

Download PDF