Packaging in India Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

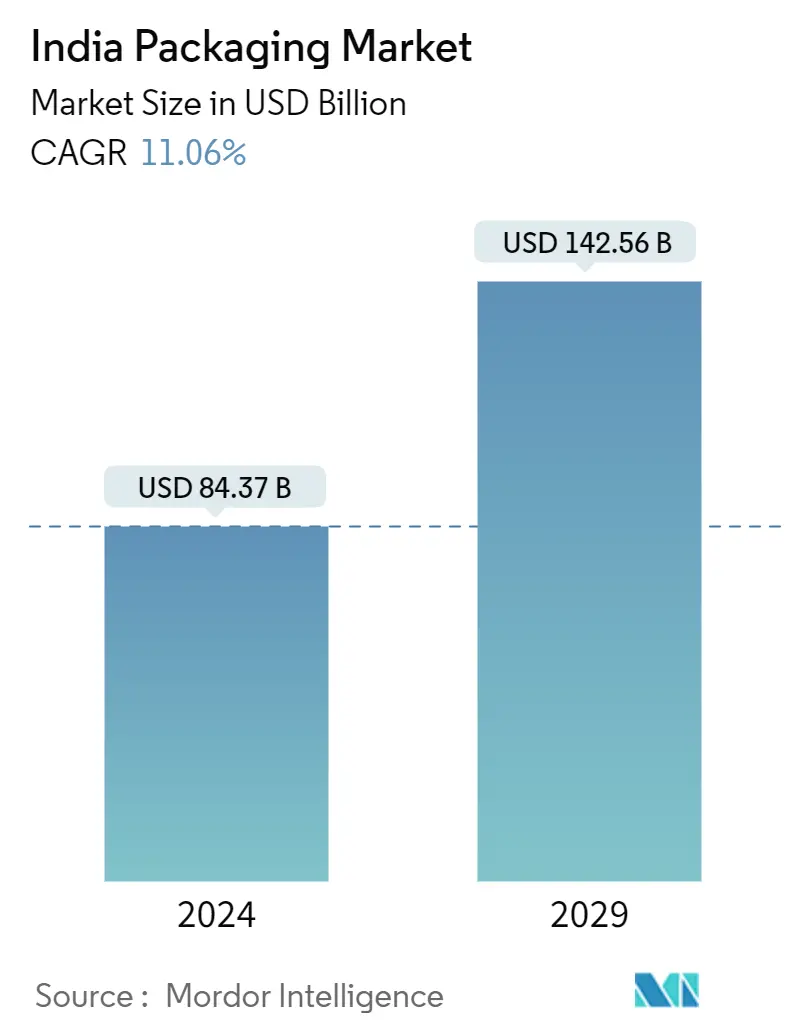

| Market Size (2024) | USD 84.37 Billion |

| Market Size (2029) | USD 142.56 Billion |

| CAGR (2024 - 2029) | 11.06 % |

| Market Concentration | Medium |

Major Players.webp)

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Packaging in India Market Analysis

The India Packaging Market size is estimated at USD 84.37 billion in 2024, and is expected to reach USD 142.56 billion by 2029, growing at a CAGR of 11.06% during the forecast period (2024-2029).

- The demand for packaging in India has expanded drastically, spurred by the rapid growth in consumer markets, especially in processed food, personal care, and pharmaceutical end-user industries. Packaging is India's one of the fastest growing sectors. Over the last few years, the industry has been a key driver of technology and innovation, contributing to various manufacturing sectors, including agriculture and the fast-moving consumer goods (FMCG). The packaging industry is driven by the factors such as rising population, increasing income levels, and changing lifestyles are anticipated to drive consumption across various industries leading to higher demand for packaging product solutions. Moreover, demand from the rural sector for packaged products is fueled by the growing media penetration through the Internet and television.

- The packaging industry in India is diverse and serves a diverse range of products and industries. Companies have established manufacturing facilities in the country and used these domestic facilities as a base to export to other nations due to the government's positive promotion of the Make in India policy. The government has implemented a plan to lower tax rates for new manufacturing businesses to transform India into a global manufacturing hub. In addition, the government intends to further level the playing field in the industry by launching several initiatives to support the growth of packaging and technological advancements, in addition to the need for domestic businesses to compete with multinational corporations.

- The packaging industry is paramount and vital in the international goods trade. Packaging may be classified based on its type of use, which is primary packaging, secondary packaging, tertiary packaging, and ancillary packaging. It is also segregated based on the types of materials used, such as plastic, paper, paperboard, glass, and metals. Packaging is used across different end-user sectors in a wide range of industries, such as food and beverage, healthcare, and cosmetics, among other end-user industries. The study also analyzes the packaging machinery sector in the Indian packaging sector landscape.

- The market is expected to be significantly challenged due to fluctuation in raw materials pricing, dynamic changes in regulatory standards, growing environmental concerns, limited effective recycling of mixed plastic waste, ineffective plastic recovery, and a lack of modern and advanced machinery in India for the packaging sector. The volatile trend in crude oil and demand for polymers in competing applications has increased pressure on input costs that fluctuate raw materials prices. Recent disruptions due to Russia's invasion of Ukraine and China's stringent Zero COVID-19 policy caused substantial supply chain difficulties and aggravated the challenges for the packaging sector in India.

- After the pandemic, there has been a lot of demand for packaging designs that are easy to sell and have a strong sustainability story. This crucial trend has significantly contributed to the rapid transformation of the packaging industry. Prior, shoppers were price-sensitive, be that as it may, with the pandemic ruling its dread, the center has moved to health and hygiene. Product categories have changed significantly due to this emphasis on hygienic packaging. Customers are willing to spend more on a product if they believe it meets all packaging requirements.

Packaging in India Market Trends

Food Industry is Expected to Hold the Largest Share in the Market

- According to the India Brand Equity Foundation (IBEF) in India, the Food and Grocery market contributes almost 70% of the total retail sales. Departmental retail stores in the urban food market and unit packaging n in the rural food markets are key drivers of flexible packaging in the country. According to USDA Foreign Agricultural Service, the number of traditional retail grocery outlets across India in 2021 was 12.79 million and was expected to surpass 13.05 million by mid of 2023. The growing retail market is expected to boost the demand for flexible packaging in the food segment.

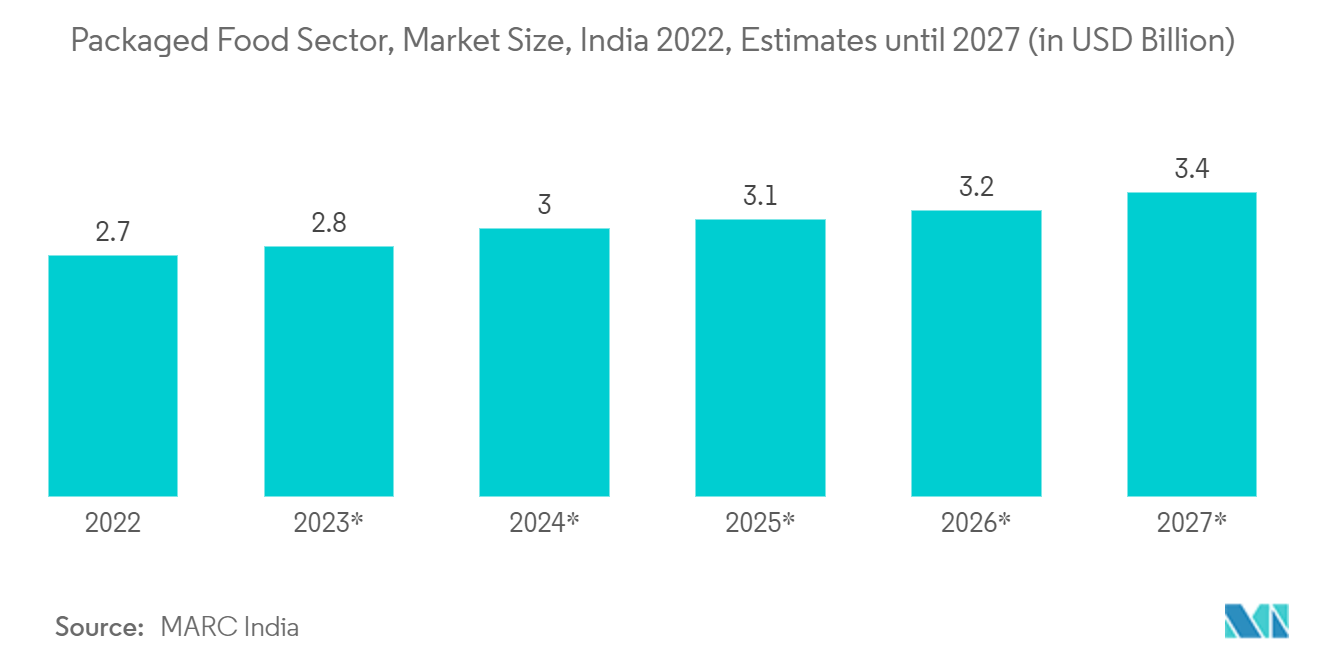

- Furthermore, with the outbreak of COVID-19, the online ordering food segment witnessed significant growth in the country as the country was under lockdown, which resulted in a sudden boom in the online food sector and packed food products. The market size of packed food products drastically increased and is also expected to grow to USD 3.4 billion by 2027, as per the reports of MARC India. Major food delivery players across India, such as Swiggy and Zomato, expanded their base to tier two and tier three cities. Containers, such as bowls, trays, and containers, increased prominently.

- In addition, the Department for Promotion of Industry and Internal Trade of the Government of India formed a private, nonprofit organization known as Open Network for Digital Commerce to create open networks for e-commerce. In April 2022, it was established. Any network-enabled app is expected to be able to identify and interact with local commerce across significant categories like supermarkets, food delivery, hotel booking, travel bookings, and more due to this open network.

- The drive to go sustainable has pushed many folding carton manufacturers to launch new products in the market. The packaging solution providers also aim to launch innovative products for the dairy segment. In March 2022, SIG India launched a similar aluminum-free folding carton aseptic packaging to tap into the rising demand for carton-packaged milk products in the country.

Paper Packaging to Have Significant Market Share

- The paper packaging business witnessed growth over the last decade due to changes in substrate choice, new market expansion, ownership dynamics, and government initiatives to ban plastic. Sustainability and environmental issues continue to be emphasized, and various innovations catering to paper packaging are expected to drive the market's growth in India.

- Packaging product in paper packaging comprises folding cartons, corrugated boxes, paper bags, and liquid paperboard. With the considerable increase in organized retail, the demand for paper packaging is anticipated to increase due to the rapid increase in supermarkets and modern shopping centers. In June 2022, the Central Pollution Control Board (CPCB), a federal agency under the Ministry of the Environment, released a list of steps to outlaw specific single-use plastic products by June 2022. Such measures are anticipated to drive the demand for paper packaging in the country.

- During the COVID-19 pandemic, the Indian e-commerce industry witnessed significant growth in the volume of online orders due to restrictions imposed on the movement of people and the shutdown of physical stores. People across the country increasingly bought online groceries, food items, and daily essentials while also purchasing merchandise online. Corrugated packaging materials significantly transported food, medicines, and medical equipment, which accelerated due to the rise in online deliveries.

- High prices of key input material, kraft paper, led to increased rates of corrugated boxes in India. This is expected to hamper the market's growth in the forecast period. For instance, in February 2022, the Kerala Corrugated Box Manufacturers Association (KeCBMA) proposed increasing the prices of corrugated boxes due to the sharp increase in the cost of essential input materials used for the manufacturing of corrugated boxes such as duplex board and kraft paper. The association said that the cost of kraft paper, the essential raw material used for manufacturing corrugated boxes, increased by more than INR 5 i.e. more than 6 US Cent in the last two months. The emerging situation forced the association to increase the prices of corrugated boxes.

- As sustainability grows, consumers are increasingly looking for 'green' products. For instance, Air India and the Indian Railways are replacing plastic packaging with eco-friendly paper and planning to use wooden cutlery to take a step toward sustainability. Many brands are basing their packaging choices on the environmental implications that accompany them by shifting away from single-use packaging and toward using compostable, recyclable, and reusable materials.

- For instance, Godrej Consumer Product Ltd. committed to a sustainability target until 2025 to adopt a circular economy and ensure efficient use of resources. This initiative includes 100% use of recyclable, reusable, or compostable packaging and 10% use of post-consumer recycled content in plastic packaging. Adopting an optimized packaging infrastructure can enhance brand appeal and increase the demand for sustainable packing solutions.

Packaging in India Industry Overview

India's packaging industry is moderately fragmented due to the several players competing to improve their market share. With the rising demand for packaging applications and technological advancement across the Indian economy, many companies are increasing their market presence by expanding their business footprint across various end-user markets.

In February 2023, under the slogan "YiPPee! - A Better World," ITC Limited's YiPPee! announced the introduction of "Terra By YiPPee!" a new waste upcycling initiative scheme. The "Terra By YiPPee!" business uses recyclable wrappers and reuses a variety of recycled YiPPee! wrapper to make eco-friendly lifestyle items, including laptop sleeves, totes, and stationery pouches.

In September 2022, Cosmo First Limited (previously Cosmo Films Limited) commenced the production of specialized BOPET (Biaxially - Oriented Polyethylene Terephthalate) Films) in Aurangabad, Maharashtra. The business previously announced setting up a new production line producing specialized BOPET (biaxially oriented polyethylene terephthalate) films with a capacity of 30,000 MT annually for installation in Aurangabad.

Packaging in India Market Leaders

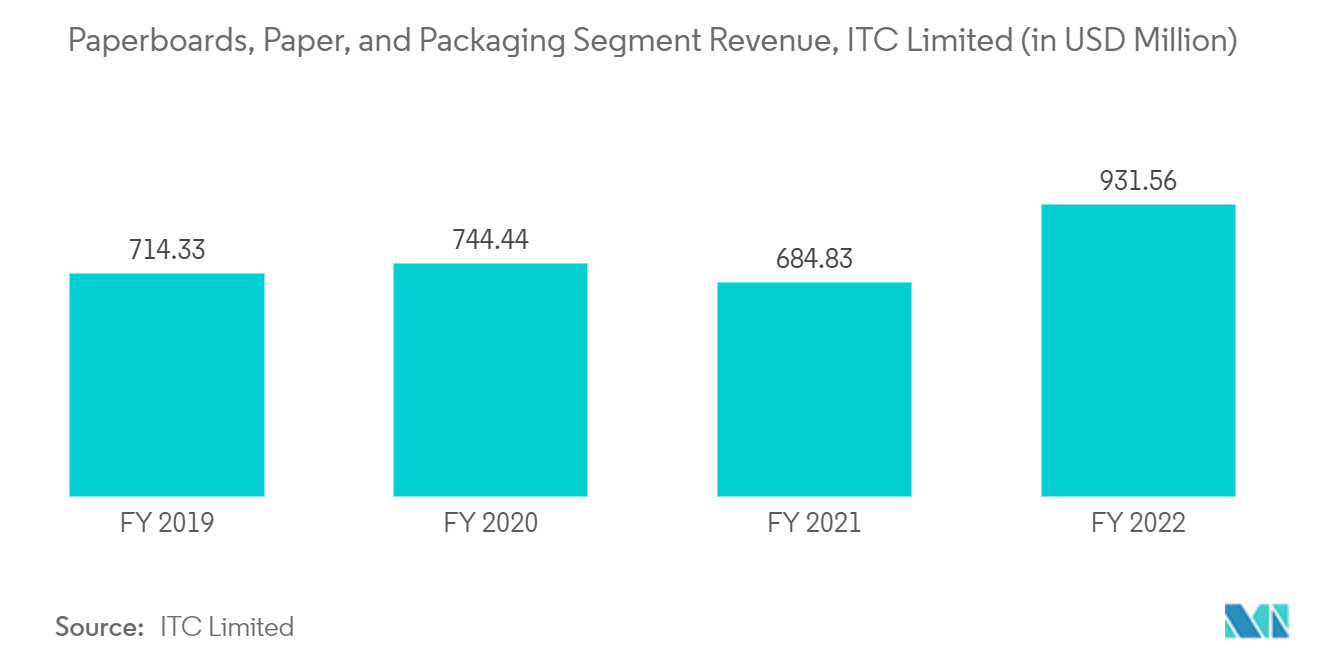

ITC Limited

Jindal Poly Films Limited

Berry Global Inc.

Uflex Limited

Ball India (Ball Corporation)

*Disclaimer: Major Players sorted in no particular order

Packaging in India Market News

- February 2023: Cosmetics and hair care brand Revlon developed a new package for its 'Top Speed' hair color range exclusively for the Indian market. The brand unveiled a new visual identity for products across India in the coming years.

- May 2022: Huhtamaki set up its first recycling plant in Maharashtra, India, as part of its CloseTheLoopinitiative. The site is spread across 2,000 square meters and has recyclers around 1,600 kg of post-consumer-used flexible plastic waste daily since it became fully operational. The recycling plant was set up with an investment of USD 1.18 million as part of the Huhtamaki Foundation's CloseTheLoopinitiative to tackle post-consumer waste and deliver a valuable secondary resource material. It was expected to process post-consumer waste to create resin to produce refined compounds for use in household products for consumers in India.

Packaging in India Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. PACKAGING INDUSTRY OVERVIEW IN INDIA

4.1 Market Overview

4.2 Composition of Packaging Sector in India - Analysis of Establishments

4.3 End-user Analysis

4.4 Analysis of the Share of Imports in the Packaging Sector (Historical and Current)

4.5 Market Ecosystem Analysis

5. SECTORAL PERFORMANCE AND MARKET ENTRY PARAMETERS

5.1 Analysis of Key Economic Indicators and Trade Flows w.r.t. Packaging Industry in India

5.2 Analysis of the Key Foreign Investments in the Packaging Sector in India

5.3 Trade Scenario Analysis - Coverage of the Key Packaging Products Based on the Relevant hs Codes

5.4 Routes to Entry into the Indian Packaging Sector

5.5 Overall Profitability of the Packaging Sector in India

5.6 Assessment of COVID-19 Impact on the Paper Packaging Market

5.7 Key Strategic Imperatives for Prospective Entrants into India

6. MARKET DYNAMICS

6.1 Market Drivers

6.1.1 Rise of the Organized Retail and E-commerce Sector

6.1.2 Increasing Demand for Sustainable and Recyclable Packaging

6.2 Market Challenges

6.2.1 Shortage and Rising Cost of Raw Material

6.2.2 Non-availability of Skilled Manpower

6.3 Focus Toward Development of Intelligent Packaging

6.4 Assessment of the Impact of COVID-19 on the Packaging Industry in India

7. KEY THEMES IN THE PACKAGING INDUSTRY IN INDIA

7.1 Role of E-commerce in Driving the Packaging Sector

7.2 Major Pharmaceutical Packaging Vendors Foraying into India

7.3 Role of Sustainability in the Food and Beverage Packaging Market

7.4 Emergence of Closed-loop Solutions in the Retail Sector

8. MARKET SEGMENTATION

8.1 By Material Type

8.1.1 Plastic

8.1.1.1 Plastic Type - Summary

8.1.1.1.1 Rigid Plastic Packaging

8.1.1.1.2 Flexible Plastic Packaging

8.1.1.2 End-user

8.1.1.2.1 Food

8.1.1.2.2 Beverage

8.1.1.2.3 Cosmetics and Personal Care

8.1.1.2.4 Industrial

8.1.1.2.5 Pharmaceutical and Healthcare

8.1.1.2.6 Other End-users

8.1.2 Paper

8.1.2.1 Paper Type - Summary

8.1.2.1.1 Folding Carton

8.1.2.1.2 Corrugated Boxes

8.1.2.1.3 Paper Bags and Liquid Paperboard

8.1.2.2 End-user

8.1.2.2.1 Food and Beverage

8.1.2.2.2 Retail and E-commerce

8.1.2.2.3 Industrial

8.1.2.2.4 Personal Care & Cosmetics

8.1.2.2.5 Other End-users

8.1.3 Container Glass

8.1.3.1 Container Glass - Summary

8.1.3.2 End-user

8.1.3.2.1 Food

8.1.3.2.2 Beverage

8.1.3.2.2.1 Alcoholic

8.1.3.2.2.2 Non-alcoholic

8.1.3.2.3 Personal Care and Cosmetics

8.1.3.2.4 Healthcare

8.1.4 Metal Cans and Containers

8.1.4.1 Metal Cans and Containers - Summary

8.1.4.2 End-user

8.1.4.2.1 Food

8.1.4.2.2 Beverage

8.1.4.2.3 Paints and Chemicals

8.1.4.2.4 Industrial

8.1.4.2.5 Other End-users

9. SUMMARY OF PACKAGING MACHINERY SECTOR IN INDIA

9.1 Current Market Scenario

9.2 Analysis of the Share of Imports (Based on hs Codes) and Key Import Regulations and Parameters

9.3 Addressable Market for Packaging Machinery in India

9.4 End-user Trends and Insights

9.5 Coverage on the Few Packaging Machine Vendors in the Country

9.5.1 Gempac (Sam Packaging Innovations Pvt. Ltd)

9.5.2 IPK Packaging (India) Private Limited

9.5.3 Nichrome Packaging Solutions

9.5.4 Pakona Engineers (India) Private Limited

9.5.5 Pack Leader Machinery Inc.

9.5.6 Shruti Flexipack Pvt. Ltd.

10. COMPETITIVE LANDSCAPE

10.1 Company Profiles - Analysis of Top Five Glass Container Packaging Manufacturers in India

10.1.1 Schott Poonawalla Private Limited

10.1.2 Gerresheimer AG

10.1.3 Agi Glaspac (HSIL Limited)

10.1.4 PGP Glass Private Limited (Piramal Glass)

10.1.5 Hindustan National Glass & Industries Limited (HNGIL)

10.2 Company Profiles - Analysis of Top Five Folding Carton Packaging Manufacturers in India

10.2.1 ITC Limited

10.2.2 JK Paper Ltd

10.2.3 Emami Paper Mills Limited (Emami Group)

10.2.4 Canpac SA

10.2.5 Velpack Pvt. Ltd.

10.3 Company Profiles - Analysis of Top Five Corrugated Box Manufacturers in India

10.3.1 Westrock India

10.3.2 OJI India Packaging Pvt. Ltd.

10.3.3 KCL Limited

10.3.4 Trident Paper Box Industries

10.3.5 Packman Packaging Private Limited

10.4 Company Profiles - Analysis of Top Five Rigid Packaging Manufacturers in India

10.4.1 Hitech Plast (Hitech Group)

10.4.2 Schoeller Allibert

10.4.3 Berry Global Inc.

10.4.4 Aptar Group Inc.

10.4.5 Manjushree Technopack Ltd.

10.5 Company Profiles - Analysis of Top Five Flexible Plastic Packaging Manufacturers

10.5.1 Jindal Poly Films Limited

10.5.2 TCPL Packaging Limited

10.5.3 Uflex Limited

10.5.4 Polyplex Corporation Limited

10.5.5 Cosmo Films Ltd. (Cosmo First Limited)

10.6 Company Profiles - Analysis of Top Five Metal can Manufacturers in India

10.6.1 Hindustan Tin Works Ltd.

10.6.2 Ball India (Ball Corporation)

10.6.3 AI Packaging Limited

10.6.4 Zenith Tins Pvt. Ltd.

10.6.5 Kaira can Company Limited

10.7 Company Profiles - Analysis of Paper Bags and Liquid Board Vendors

10.7.1 Asepto (Uflex Limited)

10.7.2 Tetra-pak India Private Limited

10.7.3 Megaplast India Pvt. Ltd.

10.7.4 Bag Master

10.7.5 The Bag Smiths

11. CURRENT RECYCLING TRENDS IN INDIA

12. MARKET OUTLOOK

Packaging in India Industry Segmentation

Packaging is defined as the process of providing a protective and informative covering to the product such that it protects the product during material handling, storage, and movement and also provides useful information to all the related supply chain partners about the content of the package. Its application can extend from primary, secondary, and tertiary to ancillary packaging.

The India Packaging Market is segmented by material (Plastic, Paper, Container glass, Metal Can and Container), by End-user (Food and Beverage, Retail and E-commerce, Paints and Chemicals, Industrial, Personal Care & Cosmetics, and Other End-users). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Material Type | ||||||||||||||

| ||||||||||||||

| ||||||||||||||

| ||||||||||||||

|

Packaging in India Market Research FAQs

How big is the India Packaging Market?

The India Packaging Market size is expected to reach USD 84.37 billion in 2024 and grow at a CAGR of 11.06% to reach USD 142.56 billion by 2029.

What is the current India Packaging Market size?

In 2024, the India Packaging Market size is expected to reach USD 84.37 billion.

Who are the key players in India Packaging Market?

ITC Limited, Jindal Poly Films Limited, Berry Global Inc., Uflex Limited and Ball India (Ball Corporation) are the major companies operating in the India Packaging Market.

What years does this India Packaging Market cover, and what was the market size in 2023?

In 2023, the India Packaging Market size was estimated at USD 75.04 billion. The report covers the India Packaging Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the India Packaging Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

What are the key challenges faced by the Packaging Industry in India?

The key challenges faced by the Packaging Industry in India: a) Fluctuations in raw material prices b) Regulatory compliance regarding food safety and packaging standards, and c) Managing waste generated from packaging

India Packaging Industry Report

The India Packaging Market is on a significant growth trajectory, propelled by the e-commerce boom, technological advancements, and changing consumer preferences. This market, embracing materials like plastics, paper, metal, and glass, serves diverse industries such as food processing, pharmaceuticals, and personal care. The e-commerce surge has spiked demand for both rigid and flexible packaging, steering the market towards sustainable solutions. Government initiatives promoting the 'Make in India' policy and technological progress have further fueled growth. The industry is also moving towards innovative packaging that enhances the customer experience, particularly in the food and beverage sector, which dominates the market. With a strong emphasis on sustainability, paper packaging is emerging as a preferred eco-friendly option. Supported by consumer trends, innovation, and government policies, the India Packaging Market is set for ongoing expansion, playing a crucial role in the nation's manufacturing and retail landscapes. For detailed market insights, including share, size, and growth forecasts, Mordor Intelligence™ offers a comprehensive analysis and free report PDF download.