Tonic Water Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

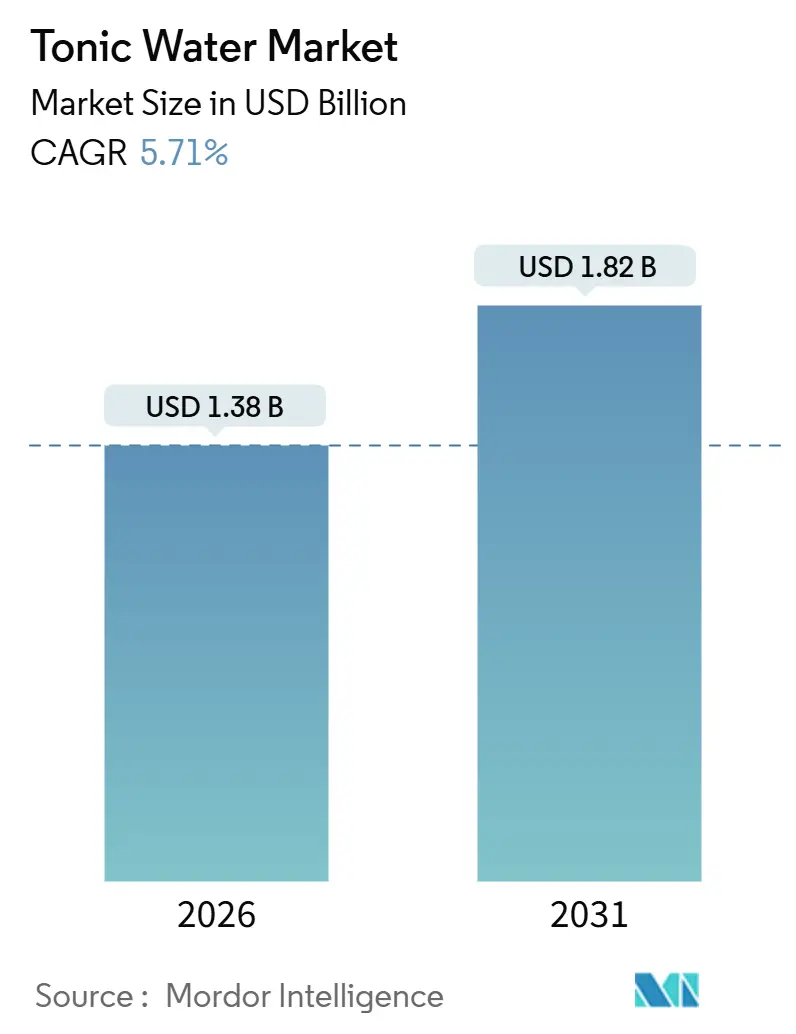

| Market Size (2026) | USD 1.38 Billion |

| Market Size (2031) | USD 1.82 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

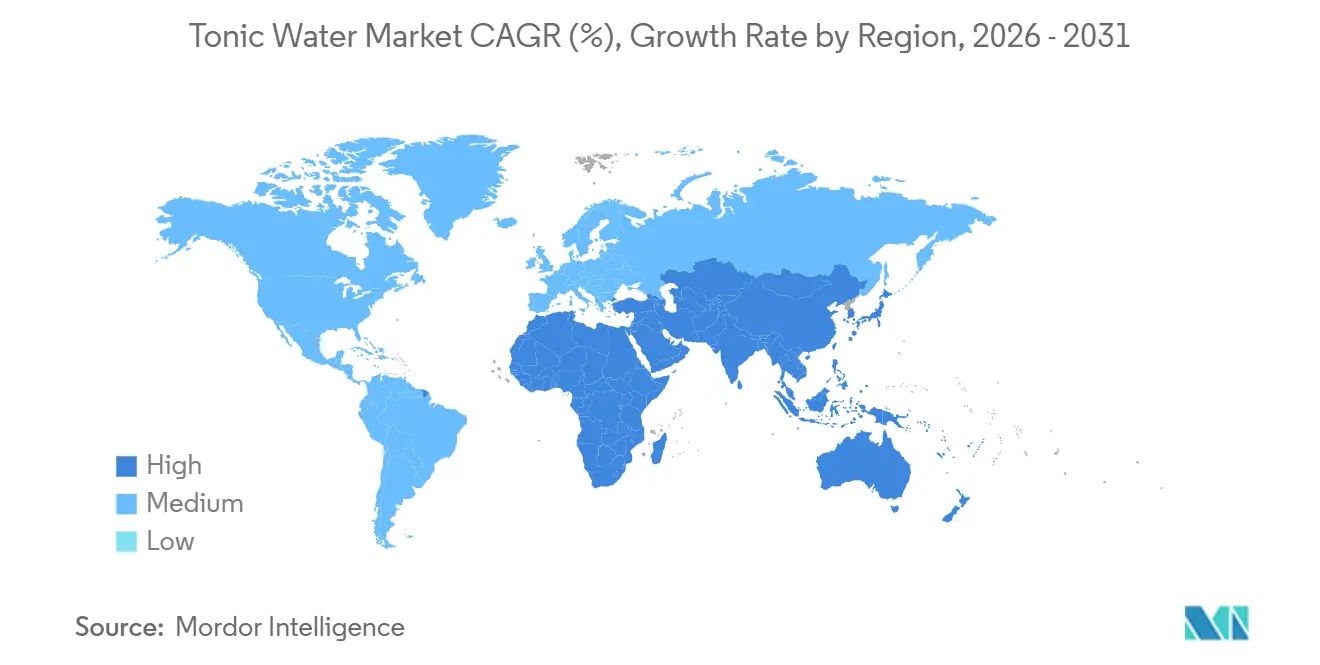

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

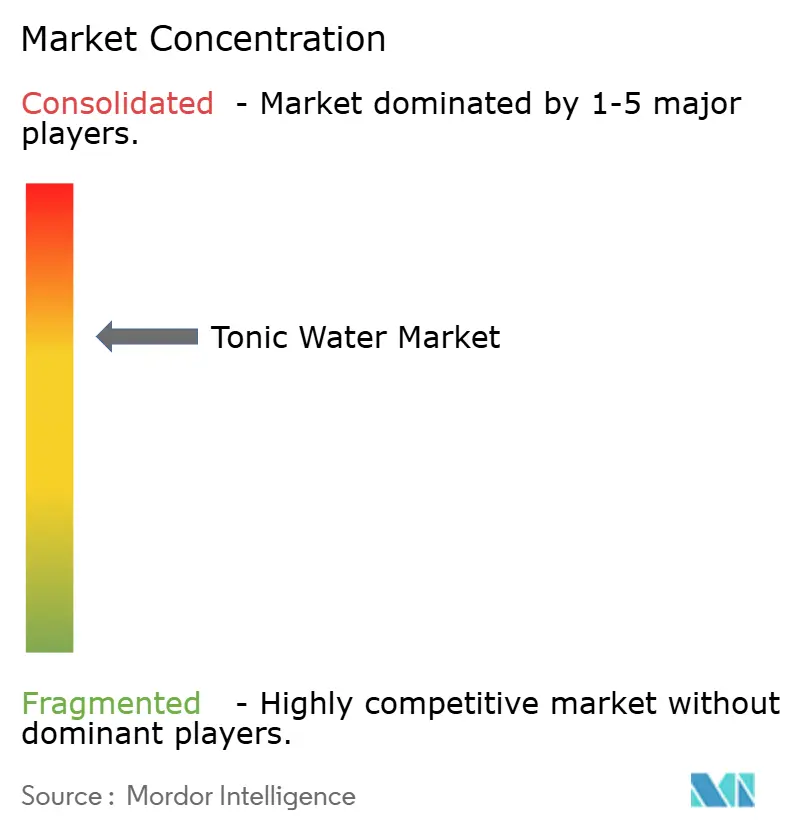

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Tonic Water Market Analysis by Mordor Intelligence

The tonic water market size is USD 1.38 billion in 2026 and it is projected to reach USD 1.82 billion by 2031, advancing at a 5.71% CAGR over 2026-2031. Premium home-mixology, a growing sober-curious demographic, and an uptick in craft distilleries are driving robust growth by expanding the customer base and diversifying product offerings. Premium positioning acts as a buffer against rising shelf prices, even as sugar taxes come into play, ensuring that brands maintain their value perception among consumers. Meanwhile, the introduction of metal cans and slimline variants resonates with health-conscious consumers, offering convenience and aligning with wellness trends[1]Source: Metal Packaging Europe, "Global Survey: Circularity Enters the Public Vocabulary", metalpackagingeurope.org. Major beverage corporations are either acquiring mixer specialists or forming distribution partnerships, seeking to capitalize on higher profit margins and navigate regulatory challenges more easily than in the beer and spirits sectors. However, brands face challenges from private-label encroachments, which intensify competition, and potential quinine supply issues, which could disrupt production and increase costs, adding further pressure to the market.

Key Report Takeaways

- By product type, regular tonic held 47.12% of the 2025 Tonic Water market share while light variants are forecast to expand at 7.91% CAGR through 2031 in the United Kingdom.

- By packaging, metal cans captured a leading 58.58% share in 2025 and are projected to grow at 6.3% CAGR worldwide through 2031.

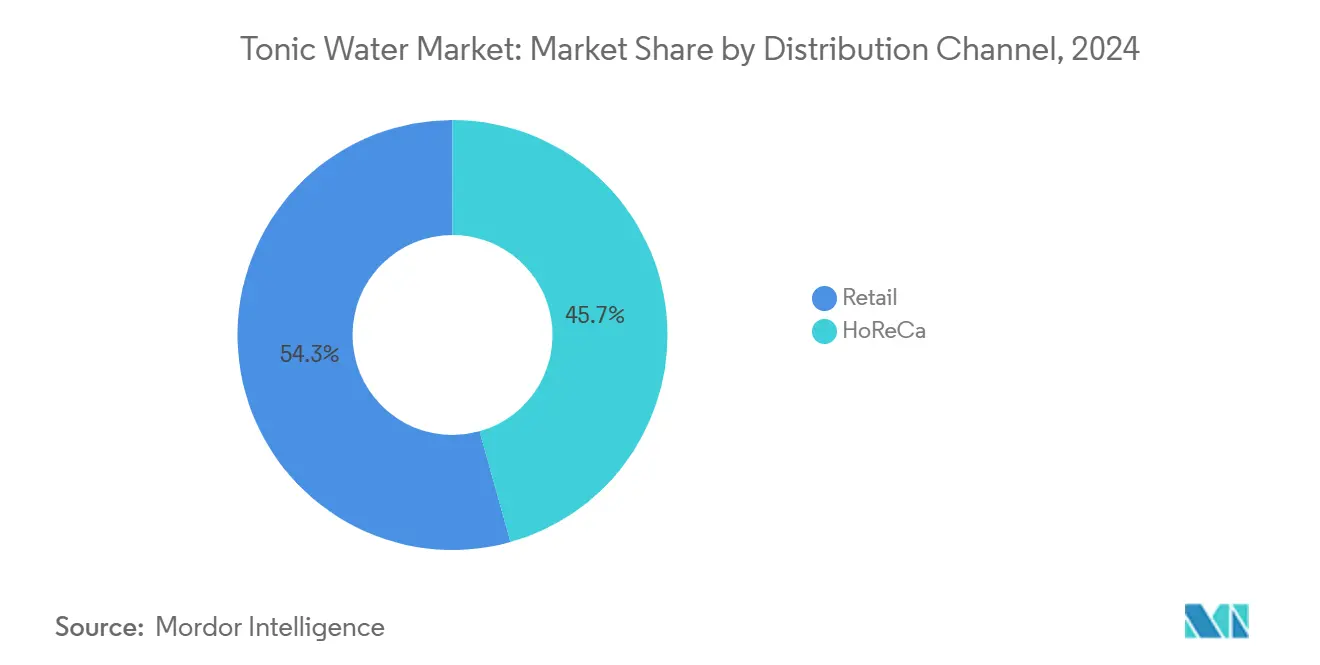

- By distribution channel, retail controlled 54.34% of 2025 value but HoReCa is advancing at 6.55% CAGR across North America.

- By geography, Europe dominated with 37.14% share in 2025 whereas Asia-Pacific is set to log the fastest 8.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tonic Water Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization of at-home mixology culture | +1.2% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Growing low-/no-alcohol sober-curious trend | +0.9% | United States, United Kingdom, Australia, urban India and China | Short term (≤ 2 years) |

| Craft gin distillery expansion | +0.7% | Japan, South Korea, Vietnam, Brazil, Mexico | Long term (≥ 4 years) |

| Rising e-commerce alcohol marketplaces | +0.8% | China, United States, European Union | Short term (≤ 2 years) |

| Novel botanical quinine substitutes | +0.5% | Europe, North America | Long term (≥ 4 years) |

| Easing of RTD cocktail delivery rules | +0.6% | California, Texas, Pennsylvania, Washington DC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premiumization of at-home mixology culture

Consumers are now crafting bar-quality drinks at home, seeking mixers that boast the same botanical intricacies as those in upscale lounges. A Bacardi survey in 2024 revealed that 62% of U.S[2]. drinkers purchased bar tools or premium spirits for home use, underscoring a notable shift from bar-centric to home-based cocktail preparation. This trend highlights a growing consumer preference for premiumization and personalization in their drinking experiences. Brands, by investing in design-centric glass bottles and weaving in heritage narratives, have successfully commanded a 40-60% premium on tonics. These strategies not only enhance brand perception but also cater to the evolving tastes of consumers who value aesthetics and storytelling. While a home-prepared gin-and-tonic sets one back about USD 3-4, ordering the same at a bar costs roughly USD 12-15. This price disparity has fueled demand, even amidst tightening disposable incomes, ensuring the Tonic Water market remains resilient to broader economic fluctuations.

Growing low/no-alcohol sober-curious trend

For many adults, moderation has evolved from a fleeting phase of abstinence to a deliberate lifestyle choice. In Q1 2025, Circana highlighted that U.S. retail sales of low- and no-alcohol beverages surged by 8.2%, outpacing the growth of traditional soft drinks. This growth reflects a broader shift in consumer preferences toward healthier and more mindful drinking habits. Tonic's intricate bitterness now finds favor in moments once reserved for beer or spirits, offering a sophisticated alternative for social and casual drinking occasions. In 2024, retailers boosted shelf space for premium mixers by 22%, a clear testament to their confidence in the category's potential for expansion and profitability. Notably, younger Gen Z drinkers, consuming 30% less alcohol than Millennials did at the same age, are poised to drive sustained growth in the Tonic Water market, as their preferences align with the rising demand for non-alcoholic and premium beverage options.

Craft gin distillery expansion in emerging markets

In 2024, Suntory, a prominent Japanese group, poured JPY 6.5 billion into boosting gin production in Osaka, aiming to meet the growing demand for premium spirits. Meanwhile, Ki No Bi invested EUR 25 million to expand its operations in Kyoto, further solidifying its position in the high-end gin market. Concurrently, projects in Vietnam and Brazil are cultivating regional cocktail hubs, drawing premium tonics into local bars and enhancing the overall cocktail culture. Collaborations between distillers and mixer brands not only reduce acquisition costs but also play a crucial role in educating a new wave of consumers about premium mixers and spirits. With licenses for craft distilleries in Brazil and Mexico witnessing a 15% annual surge from 2022 to 2024, the tonic market found a broader audience, benefiting from the increasing popularity of craft spirits. Such partnerships firmly position the Tonic Water market within the narrative of a rapidly expanding spirits industry, highlighting its integral role in the evolving beverage landscape.

Rising penetration of e-commerce alcohol marketplaces

With the permanent legalization of online alcohol sales, brands can now sidestep the challenges of limited shelf space, enabling them to reach consumers directly without relying on traditional retail channels. In 2024, China's platforms Douyin and Xiaohongshu accounted for 18% of online beverage sales, prominently featuring tonic in influencer-led cocktail demonstrations, which have become a key driver of consumer engagement and product discovery. Fever-Tree, in 2024, launched its direct-to-consumer site, providing subscriptions that not only ensure consistent sales volume but also offer detailed shopper insights, helping the company refine its marketing strategies. The inclusion of bundled garnishes and higher average order values boosts margins, even after accounting for shipping expenses, making the direct-to-consumer model highly profitable. Thanks to these digital advancements, the Tonic Water market is outpacing growth seen in traditional grocery outlets, highlighting the shift in consumer purchasing behavior toward online platforms.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sugar-tax induced retail price inflation | -0.6% | United Kingdom, Mexico, South Africa, wider European Union | Short term (≤ 2 years) |

| Carbonation-related sustainability scrutiny | -0.4% | Europe, North America, major Asian cities | Medium term (2-4 years) |

| Cinchona bark supply-chain pressure | -0.5% | Dependent importers of DRC and Indonesian bark | Long term (≥ 4 years) |

| Private-label encroachment in supermarkets | -0.8% | United States, Western Europe, developing Asia-Pacific modern trade | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sugar-tax induced retail price inflation

More than 50 jurisdictions have implemented taxes on sugary drinks, aiming to curb sugar consumption and promote healthier choices. In the fiscal year 2023-2024, the U.K.'s Soft Drinks Industry Levy generated a revenue of GBP 340 million, prompting regular tonic brands to either reformulate their products to reduce sugar content or raise their shelf prices to offset the tax burden[2]Source: HM Revenues and Customs, "Soft Drinks Industry Levy statistics", gov.uk. In 2024, South Africa's Health Promotion Levy resulted in an 11% increase in beverage prices, impacting consumer purchasing behavior. Mexico's tightened enforcement of the IEPS led to a 6% decline in regular tonic volumes as consumers opted for cheaper alternatives, highlighting the sensitivity of this market to price changes. While brands positioned as premium can absorb these taxes due to their higher price points and perceived value, mass-market players are increasingly turning to reformulations with sugar substitutes like stevia or monk fruit. However, these alternatives often introduce aftertaste challenges, which can affect consumer acceptance and brand loyalty.

Carbonation-related sustainability scrutiny

CO₂ emissions from beverages constitute about 2% of Coca-Cola's Scope 3 emissions. In response, the company is investing in advanced gas-recovery systems designed to capture CO₂ during the fermentation process, aiming to reduce its environmental impact. Meanwhile, shutdowns at European fertilizer plants in 2024 have significantly curtailed the industrial CO₂ supply, leading to cost increases of up to 20% and creating challenges for manufacturers reliant on this input. Tonic water, for instance, requires 3.5 to 4.0 volumes of CO₂, which is higher than the amount needed for standard sodas. This heightened requirement makes the elevated input prices a considerable strain on profit margins for producers. With the EU's Carbon Border Adjustment Mechanism set to be implemented in 2026, imports with high embedded carbon will face taxes. This regulatory change is likely to push brands to accelerate local sourcing strategies to mitigate costs and comply with environmental standards. Additionally, a 2024 poll conducted by the European Environment Agency revealed that 29% of consumers are inclined to reduce their carbonated drink purchases due to environmental concerns, signaling a potential shift in consumer behavior that could impact market dynamics.

Segment Analysis

By Type: Light Variants Outpace Traditional Formulations

In 2025, regular tonic water clinched a dominant 47.12% market share, solidifying its status as the go-to mixer for gin and vodka cocktails in both bars and homes. Its widespread appeal is attributed to its signature bold quinine profile, harmoniously balanced with sweetness, making it a reliable companion for premium spirits. In Brazil and Mexico, where cultural preferences lean towards indulgent flavors, a sweeter profile commands an even more impressive 62% local market share. Brands capitalize on this reliability, ensuring consistent availability in supermarkets and HoReCa channels, which in turn drives high unit volumes. Standard formulas, offering 70-80 calories per 200 ml, cater to everyday refreshment needs without compromising on calorie counts. This segment's robust revenue underscores its foundational role in the tonic water market.

Light and slimline tonics are emerging as the fastest-growing category, boasting a 7.91% CAGR projected through 2031. This surge is largely driven by the imposition of sugar taxes, a growing emphasis on wellness, and a rising number of calorie-conscious consumers. Following levy hikes, the United Kingdom witnessed a 14% spike in light tonic volumes in 2024. Fever-Tree’s Naturally Light range alone raked in a notable GBP 42 million, accounting for 18% of the company's total revenue. These lighter variants, achieving just 20-30 calories per 200 ml, utilize blends of stevia, erythritol, and cane sugar to maintain both mouthfeel and effervescence. Meanwhile, Asia-Pacific showcases its regional innovation with yuzu-infused low-cal options, and slimline variants are making their mark in HoReCa placements, striking a balance between flavor and calorie count. While functional additions like vitamins promise health benefits, they grapple with regulatory challenges concerning health claims, underscoring the industry's emphasis on transparency. Given this momentum, low-cal tonics are poised to seize a larger slice of the premium market in an increasingly health-conscious landscape.

Note: Segment shares of all individual segments available upon report purchase

By Packaging: Cans Dominate on Sustainability and Convenience

In 2025, metal cans captured a commanding 58.58% share of the global tonic water volume, thanks to their lightweight nature and near-infinite recyclability, which significantly reduce both environmental impact and logistics costs. Data from the Aluminum Association highlights that beverage cans now boast a remarkable 73% recycled content. Furthermore, these cans can be remelted and returned to the market in just 60 days, a pace that outstrips other formats. Fever-Tree has strategically pivoted to 250 ml can formats in the U.S., U.K., and Australia, aiming at single-serve occasions and notably reducing breakage losses associated with glass. With established filling lines and a familiar presence, cans ensure swift movement in both retail and HoReCa channels. They effectively maintain carbonation and the distinctive quinine bite, bolstering their premium mixer status without compromising on flavor. This dominance in volume not only underscores a commitment to sustainability but also highlights efficiency in a price-sensitive supply chain.

Looking ahead, the metal can segment is projected to grow at a 6.3% CAGR through 2031, outpacing both PET and glass, driven by an escalating demand for eco-friendly packaging. Brands are leveraging the portability of cans for on-the-go mixology. Moreover, innovations such as smart NFC closures and QR codes are being adopted for provenance tracking, bolstering authenticity claims. While glass maintains its prestigious allure in table service, boasting a heritage appeal, it comes with a caveat: 30-40% higher shipping premiums and inherent fragility risks. PET faces challenges regarding recycling rates, yet lightweight rPET variants are carving out a niche in the market. The superior barrier properties of cans against light and oxygen ensure tonic quality is preserved longer, resonating with quality-conscious consumers. This trajectory firmly establishes metal cans as the vanguard of innovation in the Tonic Water market, seamlessly merging sustainability with functional excellence.

By Distribution Channel: HoReCa Leads Growth as On-Premise Recovers

In 2025, retail channels accounted for 54.34% of tonic water sales, underscoring their pivotal role in the market. Supermarkets, convenience stores, and mass merchants, with their widespread accessibility, drive daily purchases. This retail dominance mirrors consumer preferences for one-stop shopping, where mixers are conveniently paired with spirits and garnishes. Such habits ensure robust sales across both urban and suburban areas. The scale of retail not only supports promotional strategies but also enhances visibility through end-cap displays, particularly boosting impulse buys for regular and light tonic variants. Brands like Fever-Tree capitalize on shelf space, educating consumers about the nuances of premium quinine profiles compared to commodity alternatives. With predictable restocking cycles and enticing loyalty programs, retail solidifies its position in maintaining consistent demand. This leadership in revenue not only underscores retail's significance but also acts as a buffer against fluctuations in more experiential market segments.

HoReCa, encompassing bars, restaurants, and hotels, is swiftly regaining its footing is expanding at 6.55% CAGR through 2026-2031. On-premise visits in developed markets surged by 8% in 2024, fueled by a renewed urban dining enthusiasm. The National Restaurant Association highlights that 90% of fine-dining establishments are focusing on in-house traffic[3]Source: National Restaurant Association, "State of the Restaurant Industry 2025", restaurant.org. Additionally, 75% of patrons at cocktail venues express enthusiasm for tasting events that spotlight premium mixers. With operators marking up cocktails by 300-400%, there's a clear incentive for trade-ups to high-margin tonics, enhancing both drink quality and profitability. E-commerce, bolstered by a surge in home delivery following legal reforms in various U.S. states, plays a complementary role. Fever-Tree’s subscription club not only secures volumes but also drives R&D through insights on consumer preferences. Specialty outlets, including duty-free shops and gourmet grocers, strategically target travelers and gift-givers, facilitating brand discovery. Collectively, these dynamics broaden market access routes, positioning non-retail channels for a swift share increase.

Geography Analysis

In 2024, Europe held a 37.14% market share, led by the U.K., Germany, and Spain, where gin-and-tonic traditions are deeply woven into the social fabric. Within soft drinks market, tonic water enjoys a premium, with Fever-Tree often commanding prices 40-60% higher than mainstream mixers. However, sugar levies in the U.K. and France have steered consumers towards zero-calorie options, creating opportunities for reformulated products. The strong presence of private labels keeps branded companies on their toes, driving them towards innovation and aggressive marketing to maintain their competitive edge. This dynamic environment has encouraged brands to focus on premiumization and health-oriented offerings to cater to evolving consumer preferences.

Asia-Pacific is on track to grow at a robust 8.34% CAGR, reaching 2030. As urban incomes rise and Western cocktail culture takes root in China, India, and Southeast Asia, consumption occasions multiply, particularly in urban centers where younger demographics are adopting these trends. Suntory's plant upgrades and HiteJinro's expansion in Vietnam highlight regional spirits companies co-developing tonic pairings, enhancing their appeal to local tastes and preferences. In Japan, convenience stores serve as testing grounds for botanical tonics targeting health-conscious consumers, reflecting a growing demand for functional beverages. Meanwhile, India's push for sugar reduction accelerates the acceptance of stevia-sweetened tonics, with local manufacturers increasingly aligning their portfolios with government policies and consumer health trends.

North America experiences steady, albeit modest, growth. Fever-Tree's partnership with Molson Coors opens doors to a 550-member sales force and enhanced supermarket visibility, enabling deeper market penetration. In California, Texas, and Pennsylvania, new regulations permit RTD cocktail deliveries, presenting Schweppes with a chance to introduce canned gin-and-tonic products and expand its footprint in the ready-to-drink segment. While Mexico's sugar tax limits regular tonic sales, there's potential for revival through flavor innovations and functional marketing, as brands explore ways to meet consumer demand for healthier and more diverse options. Meanwhile, South America, the Middle East, and Africa, though in nascent stages, are witnessing double-digit growth as urbanization and tourism introduce global bar trends to emerging cities. These regions are increasingly becoming focal points for international brands seeking to tap into untapped markets and capitalize on the growing interest in premium beverages.

Competitive Landscape

The tonic water market is moderately concentrated. At the premium end, Fever-Tree, Schweppes (owned by The Coca-Cola Company), and Fentimans capitalize on botanical transparency and culinary collaborations to differentiate themselves. These brands emphasize high-quality ingredients and partnerships with chefs and mixologists to appeal to discerning consumers. Meanwhile, private labels from Tesco, Carrefour, and Walmart, priced 25-35% lower, are gaining traction by offering affordable alternatives without compromising on quality. They achieve near-craft quality by employing the same contract packers as their premium counterparts.

Smaller players like East Imperial and Double Dutch are making waves by focusing on direct-to-consumer sales, weaving compelling botanical narratives, and launching limited editions. These disruptors leverage storytelling and exclusivity to build loyal customer bases and carve out niches in an otherwise competitive market. Technology is reshaping the competitive landscape; for instance, Fever-Tree's blockchain initiative monitors cinchona sourcing, addressing sustainability concerns and enhancing transparency in its supply chain. Such initiatives are becoming increasingly important as consumers demand more accountability from brands.

In 2024, patent applications surged by 18% for innovations like flavor-masking in zero-calorie sweeteners and carbon-capture carbonation. This uptick signals a trend towards heightened entry barriers, driven by proprietary technologies that provide competitive advantages. While the tonic water market remains fragmented, allowing space for regional players to thrive, advantages like strong brand equity, secure supply chains, and robust distribution channels are becoming critical for sustained growth and market leadership.

Tonic Water Industry Leaders

-

Keurig Dr Pepper, Inc.

-

The Coca-Cola Company (Schweppes)

-

Fevertree Drinks PLC

-

PepsiCo Inc.

-

Carlsberg Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Double Dutch unveiled its Riviera Tonic Water, a Mediterranean-inspired blend featuring aromatic thyme, rosemary, bittersweet wormwood, and zesty lemon, all atop its celebrated Indian Tonic base. Aimed at the UK on-trade hospitality sector, this premium offering caters to the rising demand for botanical, coastal serves in bars and restaurants.

- July 2025: responding to a burgeoning demand for premium offerings, UNDONE made its U.S. debut. The brand rolled out its patented dealcoholized spirits, sparkling wines, and ready-to-drinks (RTDs) at competitive prices, championing authentic taste and inclusivity for the 'sober-curious' demographic.

- April 2025: Chuala, renowned for its award-winning tonic water, forged a partnership with Best Brands Inc., a prominent beverage distributor, to broaden its distribution across Tennessee. This strategic alliance is set to bolster Chuala's presence in bars, restaurants, and retail outlets, enhancing both on- and off-premise availability.

- January 2025: Franklin & Sons, in a bid to amplify its footprint in the U.S., teamed up with Empire Distributors, marking its entry into Georgia and Colorado. This partnership not only brought their premium tonics and mixers to major cities like Atlanta and Denver but also reinforced their presence in Tennessee and North Carolina, ensuring wider availability in bars and homes.

Global Tonic Water Market Report Scope

Tonic water is a carbonated drink in which quinine gets dissolved. Tonic water is used as a mixer with gin or other alcoholic beverages. The market is segmented by Product type, distribution channels, and geography. Based on product type, the market is segmented into regular tonic water, low-calorie tonic water, and slimline tonic water. Based on the packaging type, the market is segmented into metal cans, PET/Glass Bottles, and others.Based on the distribution channel, the market is segmented into retail and HoReCa. The market is geographically segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa.

| Regular Tonic Water |

| Low-Calorie Tonic Water |

| Slimline/Light Tonic Water |

| PET/Glass Bottles |

| Metal Can |

| HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Regular Tonic Water | |

| Low-Calorie Tonic Water | ||

| Slimline/Light Tonic Water | ||

| By Packaging Type | PET/Glass Bottles | |

| Metal Can | ||

| By Distribution Channel | HoReCa | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Tonic Water Market?

The Tonic Water Market size is expected to reach USD 1.39 billion in 2025 and grow at a CAGR of 7.45% to reach USD 1.99 billion by 2030.

What is the current Tonic Water Market size?

In 2025, the Tonic Water Market size is expected to reach USD 1.39 billion.

Who are the key players in Tonic Water Market?

Keurig Dr Pepper, Inc., Fentimans Ltd, The Coca-Cola Company (Schweppes), East Imperial Beverage Corporation and Fevertree Drinks PLC are the major companies operating in the Tonic Water Market.

Which is the fastest growing region in Tonic Water Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Tonic Water Market?

In 2025, the Europe accounts for the largest market share in Tonic Water Market.

What years does this Tonic Water Market cover, and what was the market size in 2024?

In 2024, the Tonic Water Market size was estimated at USD 1.29 billion. The report covers the Tonic Water Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Tonic Water Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.