Market Size of Thin Wafer Processing And Dicing Equipment Industry

| Study Period | 2019 - 2029 |

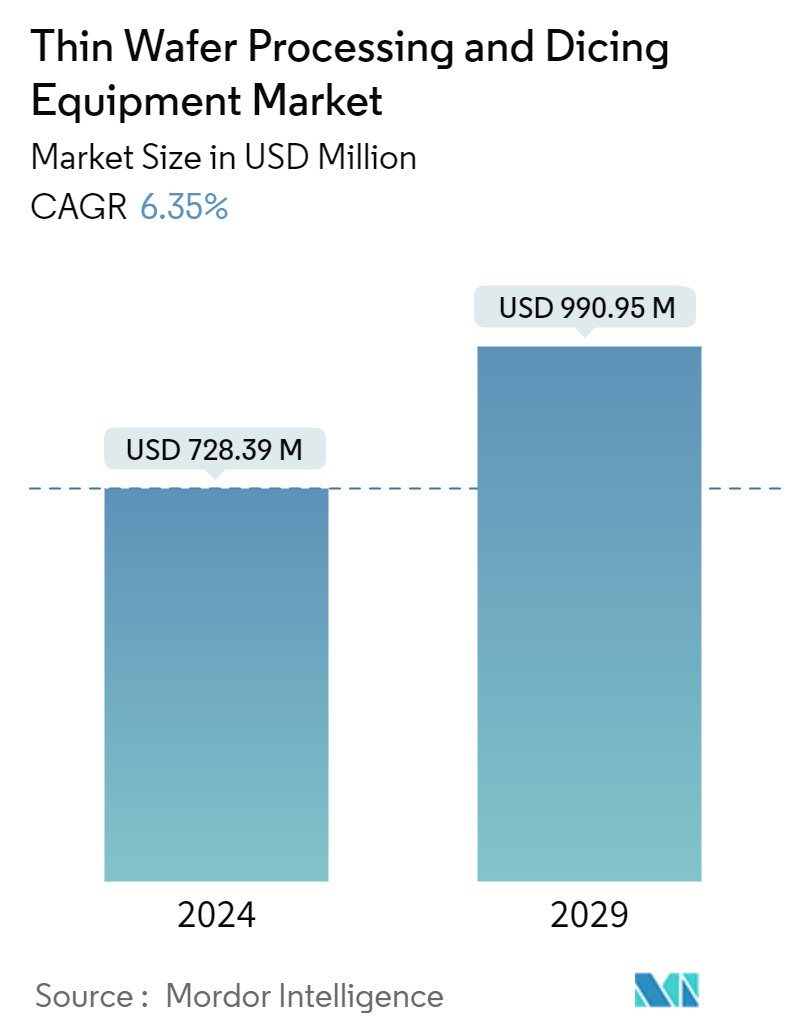

| Market Size (2024) | USD 728.39 Million |

| Market Size (2029) | USD 990.95 Million |

| CAGR (2024 - 2029) | 6.35 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Thin Wafer Processing And Dicing Equipment Market Analysis

The Thin Wafer Processing And Dicing Equipment Market size is estimated at USD 728.39 million in 2024, and is expected to reach USD 990.95 million by 2029, growing at a CAGR of 6.35% during the forecast period (2024-2029).

- The increasing efforts to make electronic packaging highly resourceful due to the enormous demand for electronic components owing to amplified usage have made electronic packaging useful in a myriad of applications. These factors are driving the growth of the semiconductor and IC packaging market.

- One of the major factors expected to boost the demand for thin wafer processing and dicing equipment in the coming years is the growing demand for three-dimensional integrated circuits, which are widely used in miniature semiconductor devices such as memory cards, smartphones, smart cards, and various computing devices.

- Three-dimensional circuits are becoming more popular in multiple space-constrained applications, such as portable consumer electronics, sensors, MEMS, and industrial products because they improve overall product performance in terms of speed, durability, low power consumption, and lightweight memory.

- Due to the widespread availability of low-cost cloud computing solutions, the expanding use of server and data center systems across various enterprises and industries is likely to fuel demand for logic devices like microprocessors and digital signal processors. In addition, as the number of IoT-enabled linked devices grows, the utilization of microprocessors also increases. Thin wafers are increasingly employed in these devices to enable effective temperature management and enhance performance. Such factors are responsible for the growth of the market.

- Silicon wafers have long been used as a fabrication platform in microelectronics and MEMS. The silicon-on-insulator substrate is a unique variation of the standard silicon wafer. Two silicon wafers are glued together using a bond layer of silicon dioxide with a thickness of about 1-2 μm to make these wafers. One silicon wafer gets flattened down to 10-50 μm in thickness. The application will determine the exact thickness of the coating.

- The cost of building state-of-the-art thin wafer foundries has increased exponentially, which puts pressure on the market. The number of semiconductor manufacturers has consolidated in recent times. Performance boosts are slowing down, making specialized thin wafers increasingly attractive. The design decisions that enable thin wafers to be universal may be sub-optimal for some computing tasks.

- Various developments in semiconductor research further create opportunities for the market. For instance, in April 2023, Rapidus officially joined Imec’s Core Partner Program, marking a significant stride in sustainable collaboration with Imec in advanced semiconductor research. This move reinforced their commitment to long-term collaboration and advancement in the semiconductor domain.

Thin Wafer Processing And Dicing Equipment Industry Segmentation

The need for miniaturization toward small-sized, high-performing, and low-cost device configurations has created the need for thin wafers. Most of these reach below 100 µm or even 50 µm for applications such as memory and power devices. Moreover, wafer dicing is the process of separating the die from a semiconductor wafer after the wafer has been processed.

The thin wafer processing & dicing equipment market is segmented by equipment type (thinning equipment and dicing equipment [blade dicing, laser ablation, stealth dicing, and plasma dicing]), application (memory and logic, MEMS devices, power devices, CMOS image sensors, RFID, and others), wafer thickness (750 µm, 120 µm, and 50 µm), wafer size (less than 4 inches, 5 inches and 6 inches, 8 inches, and 12 inches), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). The report offers the market sizes and forecasts for all the above segments in value terms (USD).

| By Equipment Type | ||||||

| Thinning Equipment | ||||||

|

| By Application | |

| Memory and Logic (TSV) | |

| MEMS Devices | |

| Power Devices | |

| CMOS Image Sensors | |

| RFID | |

| Others |

| By Wafer Thickness | |

| 750 micrometers | |

| 120 micrometers | |

| 50 micrometers |

| By Wafer Size | |

| Less than 4 inches | |

| 5 inches and 6 inches | |

| 8 inches | |

| 12 inches |

| By Geography*** | |

| North America | |

| Europe | |

| Asia | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Thin Wafer Processing And Dicing Equipment Market Size Summary

The Thin Wafer Processing and Dicing Equipment Market is poised for significant growth, driven by the increasing demand for compact and efficient electronic devices. This demand is largely fueled by the rise of three-dimensional integrated circuits, which are essential for enhancing the performance of miniature semiconductor devices used in smartphones, memory cards, and various computing devices. The market is also benefiting from the expanding use of server and data center systems, propelled by the availability of cost-effective cloud computing solutions. As the number of IoT-enabled devices continues to rise, the need for thin wafers to improve temperature management and performance in these devices is becoming more pronounced. Despite challenges such as the high cost of establishing advanced thin wafer foundries and the global slowdown in demand due to the COVID-19 pandemic, the market is expected to experience a robust growth trajectory.

Regionally, the Asia Pacific stands out as the largest and fastest-growing semiconductor market, with countries like China, South Korea, and Singapore driving demand for consumer electronics. The region's growth is supported by strategic acquisitions and government incentives, particularly in China, which has seen a rise in market players focusing on expansion through mergers and acquisitions. Japan remains a key player in the semiconductor industry, with significant contributions from major manufacturers and suppliers of critical materials. Meanwhile, initiatives like the Quad Alliance's semiconductor supply chain project aim to enhance supply chain security and capacity in the Asia Pacific. In India, government efforts to develop a self-sufficient semiconductor ecosystem are underway, further bolstering the market's growth prospects. Despite the presence of few major players and challenges in manufacturing processes, ongoing innovations and research and development efforts are maintaining a competitive edge in the market.

Thin Wafer Processing And Dicing Equipment Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness Porter's Five Forces Analysis

-

1.2.1 Threat of New Entrants

-

1.2.2 Bargaining Power of Buyers

-

1.2.3 Bargaining Power of Suppliers

-

1.2.4 Threat of Substitute Products

-

1.2.5 Intensity of Competitive Rivalry

-

-

1.3 Industry Value Chain Analysis

-

1.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Equipment Type

-

2.1.1 Thinning Equipment

-

2.1.2 Dicing Equipment

-

2.1.2.1 Blade Dicing

-

2.1.2.2 Laser Ablation

-

2.1.2.3 Stealth Dicing

-

2.1.2.4 Plasma Dicing

-

-

-

2.2 By Application

-

2.2.1 Memory and Logic (TSV)

-

2.2.2 MEMS Devices

-

2.2.3 Power Devices

-

2.2.4 CMOS Image Sensors

-

2.2.5 RFID

-

2.2.6 Others

-

-

2.3 By Wafer Thickness

-

2.3.1 750 micrometers

-

2.3.2 120 micrometers

-

2.3.3 50 micrometers

-

-

2.4 By Wafer Size

-

2.4.1 Less than 4 inches

-

2.4.2 5 inches and 6 inches

-

2.4.3 8 inches

-

2.4.4 12 inches

-

-

2.5 By Geography***

-

2.5.1 North America

-

2.5.2 Europe

-

2.5.3 Asia

-

2.5.4 Australia and New Zealand

-

2.5.5 Latin America

-

2.5.6 Middle East and Africa

-

-

Thin Wafer Processing And Dicing Equipment Market Size FAQs

How big is the Thin Wafer Processing And Dicing Equipment Market?

The Thin Wafer Processing And Dicing Equipment Market size is expected to reach USD 728.39 million in 2024 and grow at a CAGR of 6.35% to reach USD 990.95 million by 2029.

What is the current Thin Wafer Processing And Dicing Equipment Market size?

In 2024, the Thin Wafer Processing And Dicing Equipment Market size is expected to reach USD 728.39 million.