Thin Film Encapsulation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

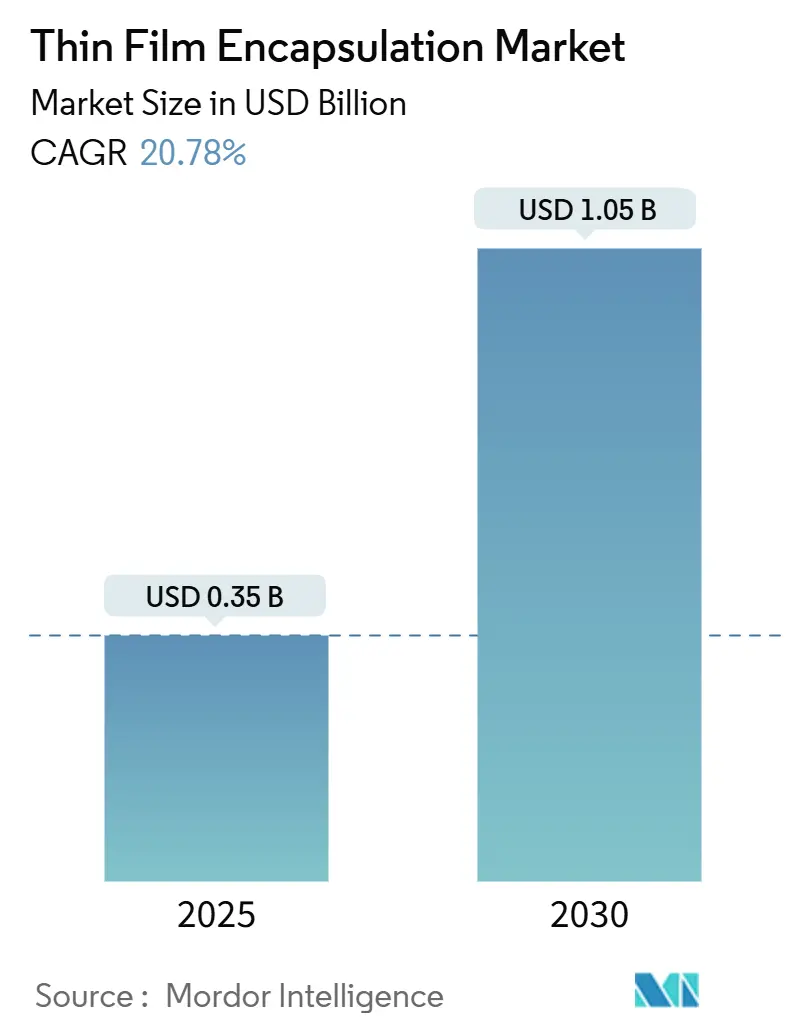

| Market Size (2025) | USD 0.35 Billion |

| Market Size (2030) | USD 1.05 Billion |

| Growth Rate (2025 - 2030) | 20.78% CAGR |

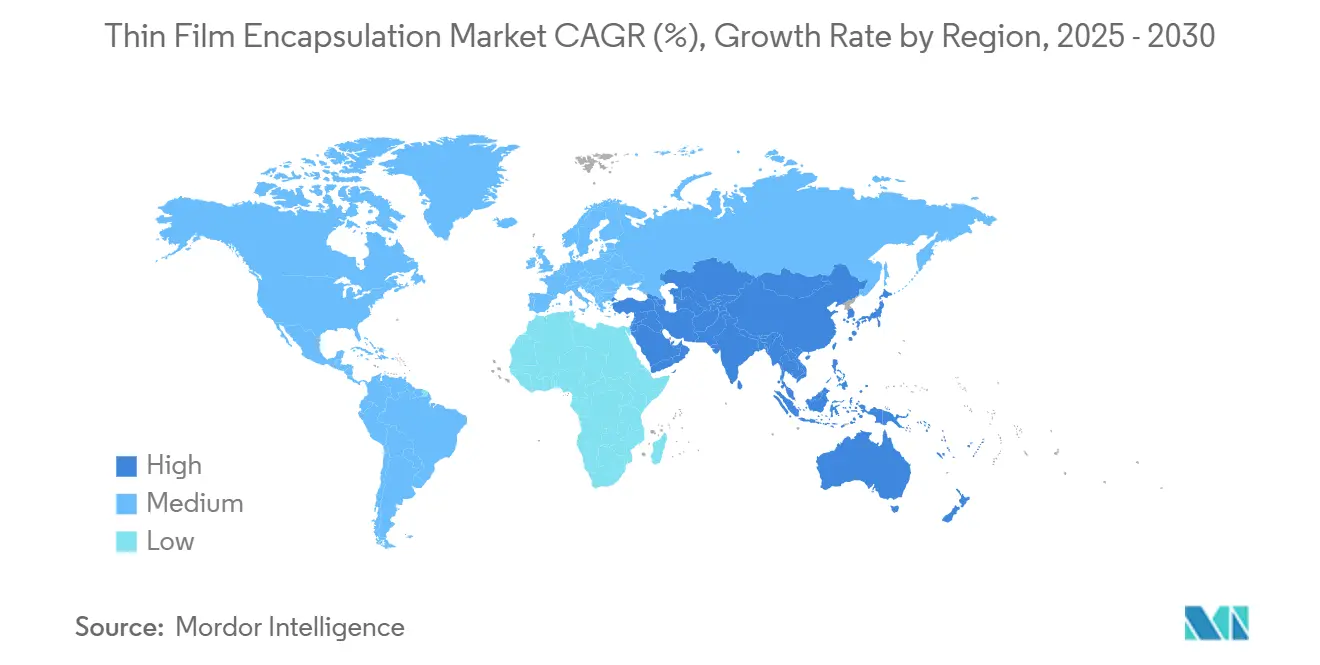

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

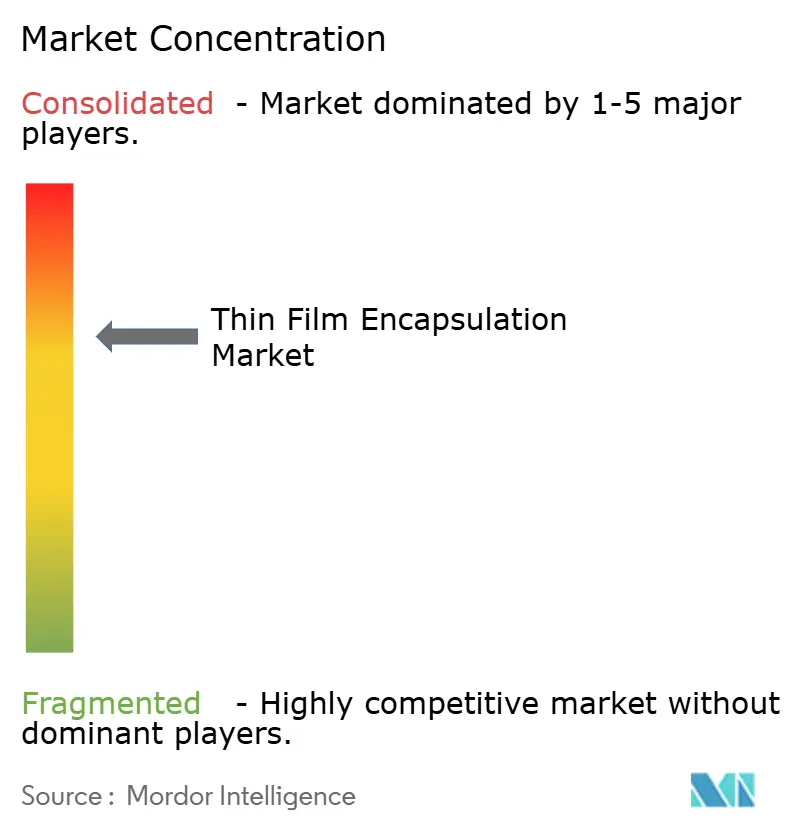

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thin Film Encapsulation Market Analysis by Mordor Intelligence

The thin film encapsulation market size was valued at USD 0.35 billion in 2025 and is forecast to reach USD 1.05 billion by 2030, reflecting a robust 20.78% CAGR. Rapid adoption of flexible OLED displays, surging demand for bendable consumer devices, and aggressive capacity additions in Asia-Pacific have kept the growth trajectory steep. Manufacturers are prioritizing atomic layer deposition (ALD) barriers that achieve water-vapor transmission rates below 10⁻⁶ g/m²/day, enabling longer device lifetimes while preserving form-factor flexibility. Automotive mandates for curved cockpit displays and medical certification of roll-to-roll ALD films are widening application scope, even as precursor shortages and capital-intensive Gen-6 ALD lines present headwinds. Competitive intensity is rising as Chinese firms, buoyed by “New Display” subsidies, scale output and erode Korean dominance.[1]Chae-Yeon Kim, “Samsung ups smaller OLED workforce to fend off Chinese rivals,” KED Global, kedglobal.com

Key Report Takeaways

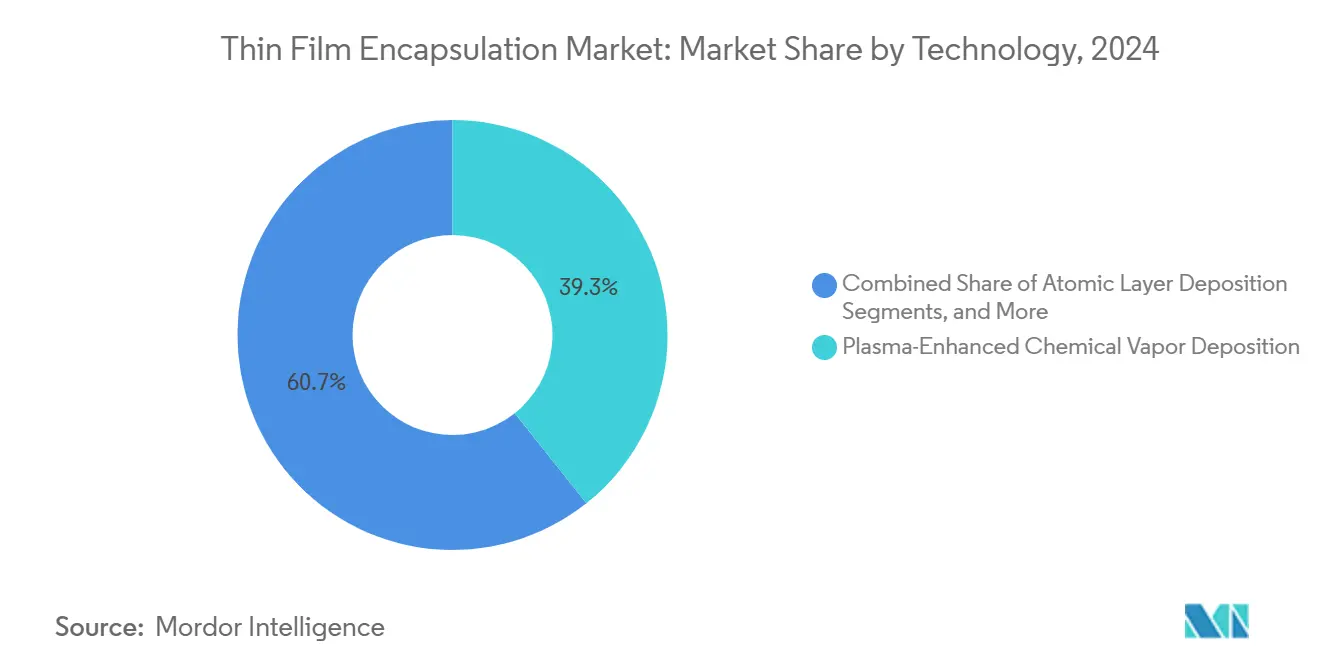

- By technology, plasma-enhanced chemical vapor deposition led with 39.3% of the thin film encapsulation market share in 2024, while ALD is advancing at 26.4% CAGR through 2030.

- By layer structure, hybrid multi-layer barriers accounted for 47.3% of the thin film encapsulation market size in 2024; single-layer solutions are expanding at 29.1% CAGR.

- By application, flexible OLED displays held 61.4% revenue share in 2024, whereas automotive displays and lighting post the fastest 32.8% CAGR to 2030.

- By deposition equipment type, cluster PECVD systems captured 46.3% share of the thin film encapsulation market size in 2024; ALD reactors mark the quickest 34.2% CAGR.

- By end-use industry, consumer electronics dominated with a 74.5% share in 2024, while healthcare and wearables registered a 31.2% CAGR by 2030.

- By geography, Asia-Pacific commanded 69.5% of the thin film encapsulation market share in 2024; the Middle East and Africa region is projected to climb at 27.2% CAGR between 2025-2030.

Global Thin Film Encapsulation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AMOLED capacity expansions in South Korea and China | +5.2% | Asia-Pacific, spillover to North America | Medium term (2-4 years) |

| Automotive curved-display mandates in the EU and NA | +4.8% | Europe, North America | Medium term (2-4 years) |

| Roll-to-roll ALD unlocking certified medical wearables | +3.9% | Global, early uptake in North America and Europe | Long term (≥ 4 years) |

| EU carbon-neutral BIPV push boosting inorganic barriers | +2.6% | Europe, spillover to North America | Long term (≥ 4 years) |

| SID award-winning low-temp ALD enabling foldables | +2.4% | Global, early adoption in Asia-Pacific | Short term (≤ 2 years) |

| China “New Display” subsidies covering encapsulation CapEx | +2.1% | Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

| Source: Mordor Intelligence | |||

AMOLED capacity expansions in South Korea and China are fueling ALD-TFE tool orders

Samsung Display allocated USD 3 billion for an 8.6-generation IT OLED line targeting 2026 production, while BOE committed USD 8.7 billion for a comparable plant. These projects multiplied purchase orders for ALD encapsulation tools because the technology offers uniform, pinhole-free barriers at low temperatures, a necessity for next-generation IT and automotive panels. Heightened competition has revived Korean shipment leadership but simultaneously broadened ALD demand across Asia-Pacific foundries.

Automotive curved-display mandates in the EU and North America

Regulatory guidance favoring seamless instrument clusters has sparked accelerated design-ins of curved OLED dashboards. These modules need encapsulation stacks that withstand vibration, UV exposure, and -40 °C cycling. Samsung’s adoption of tandem OLED with advanced moisture barriers exemplified the shift, positioning the firm to capture revenue as total automotive display spend is forecast to overtake monitor panel sales by 2026.

Roll-to-roll ALD unlocking certified medical wearables

Pilot web lines achieved detection-limit water-vapor transmission rates at 0.25 m/min coating speed, enabling textiles that remain operational after bending, washing, and prolonged skin contact. Such performance satisfied global medical approval pathways, opening mass production of e-textiles for continuous vital-sign monitoring.

EU carbon-neutral BIPV push boosting inorganic barriers

The EU Strategic Research and Innovation Agenda prioritized long-life building-integrated photovoltaics, forcing module makers to adopt ALD-based inorganic barriers that secure 25-year lifetimes against moisture and UV stress. Demand for transparent, durable coatings is consequently rising in Europe’s construction supply chain.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CapEx of Gen-6 ALD cluster lines | -3.1% | Global, highest in emerging markets | Medium term (2-4 years) |

| Reliability failures under −40 °C automotive cycling | -2.3% | Europe, North America | Short term (≤ 2 years) |

| Competition from ultra-thin flexible glass | -1.8% | Global | Long term (≥ 4 years) |

| Precursor supply bottlenecks (e.g., DEZ) | -1.5% | Global, highest in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

| Source: Mordor Intelligence | |||

High CapEx of Gen-6 ALD cluster lines

Next-generation ALD stacks demand more than USD 100 million per line, sidelining mid-tier producers and slowing technology diffusion. Many Asian fabs still amortize older cluster tools, complicating upgrade economics even where yield benefits are clear. This cost barrier delays uniform adoption of best-in-class encapsulation across the thin film encapsulation market.

Reliability failures under −40 °C automotive cycling

Delamination and crack propagation in hybrid barriers remain common when panels face rapid thermal cycling from cabin heat to winter cold. Failures expose organic layers to moisture, curtailing display lifespan. Ongoing material research and development now integrates stress-release organics, but at a premium manufacturing cost, tempering automotive revenue expansion.

Segment Analysis

By Technology: ALD drives next-level barrier integrity

ALD recorded a 26.4% CAGR outlook while PECVD held 39.3% revenue in 2024, illustrating a transition phase within the thin film encapsulation market. ALD films reached water-vapor rates at 10⁻⁶ g/m²/day that extend OLED life spans and support foldable substrates.[2]Wei Zhang et al., “Thin Film Encapsulation for OLED via ALD,” Journal of Materials Research, cambridge.org Roll-to-roll ALD upgraded throughput to web speeds suitable for wearable production, while spatial ALD is overcoming substrate-size limits. PECVD remains preferred for rigid panels needing high volume. VTE and OVPD continue in niche emissive stacks where material compatibility overrides barrier extremity. Low-temperature ALD chemistries awarded by SID in 2023 unlocked polyimide substrates for mass foldables, deepening the technology mix. Consequently, ALD tool providers enjoy record order backlogs, lifting regional supplier ecosystems across South Korea, China, and the United States.

The thin film encapsulation market continues to rely on PECVD for cost-sensitive SKUs because the reactors integrate seamlessly with legacy TFT lines. Inkjet encapsulation printing, spearheaded by Kateeva, decreased organic material waste and enabled patterned barriers for smartwatch dials. VTE retains relevance for small-area microdisplays where device yield trumps throughput. With spatial ALD crossing 15 gen substrates in pilot tests, the competitive landscape between PECVD and ALD is expected to tighten, driving hybrid production floors that leverage both methods.

Note: Segment shares of all individual segments available upon report purchase

By Layer Structure: hybrids maintain dominance while single-layer surges

Hybrid stacks combining parylene C with ALD Al₂O₃ secured 47.3% sales in 2024, thanks to a proven balance of stress relief and moisture blocking. These dyads achieved sub-10⁵ g/m²/day WVTR while sustaining flex cycles exceeding 10,000 bends, a specification demanded by premium smartphones. Single-layer barriers, however, now post the fastest 29.1% CAGR because silbione-blended hybrimer films offer comparable protection at half the deposition sequence length, cutting takt time for rollable panels.

Inorganic multi-layers deliver unmatched oxygen resistance but risk crack formation under tensile stress, limiting adoption in foldables. Organic multi-layers excel in bendability yet rarely reach lifetime targets alone. Commercial lines consequently calibrate layer architecture by product class: smartphones accept hybrid dyads, automotive clusters need triple inorganic caps, while e-textiles increasingly lean on advanced organic chemistries. Component suppliers respond with modular material kits that harmonize refractive index, modulus, and stickiness across adjoining layers, ensuring line reliability beyond 90% yield.

By Application: flexible displays prevail as vehicles accelerate

Flexible OLEDs captured 61.4% of 2024 revenue within the thin film encapsulation market. Their dominance stemmed from major smartphone and notebook launches that mandated sub-10⁵ g/m²/day barriers without adding bulk thickness. Commercial foldables extended panel lifetime beyond 200,000 opens when paired with hybrid dyads, validating mass retail readiness.

Automotive displays represent the most explosive application with a 32.8% CAGR. Curved dashboards and transparent HUD modules require tandem OLED stacks plus resilient encapsulation, a niche that Samsung, LG Display, and BOE aggressively pursued through bespoke tooling contracts. MicroLED and quantum-dot integrations are emerging; encapsulation pockets produced via maskless lithography shield each sub-pixel isotropically, promising 8K HDR clusters for AR and cockpit usage. Thin-film solar modules, printable sensors, and wearables also absorb barrier innovation, but at smaller absolute volumes.

By Deposition Equipment Type: cluster PECVD retains volume leadership

Cluster PECVD tools generated 46.3% of 2024 equipment sales owing to their high-throughput capability and compatibility with existing fab layouts. Integrated load-lock and transfer arms minimized particle risk, boosting panel yield for rigid TVs and monitors. Meanwhile, ALD reactors expanded by 34.2% CAGR as spatial reactor designs improved wafer-equivalent per hour counts threefold, challenging PECVD cost equations.

Inkjet encapsulation printers addressed material wastage by depositing organics only where needed, lowering the bill of materials in smartwatch lines. Roll-to-roll vacuum systems became crucial for e-textile and sensor webs where substrate lengths exceed 300 m. Laser-assisted repair stations, though niche, salvaged defective large-area panels, improving overall equipment effectiveness. Vendors increasingly bundle software analytics, enabling predictive maintenance, elevating uptime expectations in hyper-competitive fabs.

Note: Segment shares of all individual segments available upon report purchase

By End-Use Industry: consumer electronics dominates, healthcare rises

Smartphones, tablets, and notebooks formed 74.5% of the thin film encapsulation market revenue in 2024 as flagship models shifted from rigid to flexible AMOLED. Fierce competition among handset OEMs pushed display makers to secure best-in-class barriers, reinforcing continuous investments in ALD and hybrid organic films.

Healthcare and wearables, though smaller, observe a 31.2% CAGR because ultrathin barriers enable skin-compatible patches and implantable sensors requiring impermeability over multi-year service lives. Automotive adoption outpaces the overall panel market, while renewable-energy modules benefit from ALD caps that prolong outdoor reliability. Industrial and aerospace niches specify the toughest barrier metrics, often commanding premium margins and specialized service contracts.

Geography Analysis

Asia-Pacific retained 69.5% revenue share in 2024, driven by South Korea’s and China’s fab expansions and integrated supply ecosystems. Government incentives covering encapsulation capital costs accelerated ALD cluster installations, while Korean players pivoted toward high-value products and tandem stacks to defend margins. Regional tooling and chemical suppliers co-located near fabs, shortening qualification cycles and reinforcing dominance across the thin film encapsulation market.

Europe posted healthy gains built on automotive and BIPV demand. Strict EU vehicle safety directives accelerated curved OLED cockpit adoption, and carbon-neutral building rules spurred ALD barrier uptake in solar façades.[3]European Technology and Innovation Platform for Photovoltaics, “Strategic Research and Innovation Agenda,” eera-pv.eu Research consortia advanced low-temperature ALD precursors, aligning performance with circular-economy objectives.

The Middle East and Africa exhibited the highest 27.2% CAGR outlook from a small base, as nations like the UAE and Saudi Arabia funded electronics clusters to diversify their economies. Harsh desert climates necessitated robust encapsulation for display and solar products, creating premium demand for ALD-based inorganic layers. Technology transfer partnerships with Asian OEMs seeded local capacity, reducing single-region dependency for global brands.

North America maintained influence through materials science leadership and equipment exports despite limited panel production. Automotive mandates and quantum-dot microLED research and development anchored demand for specialized barrier know-how, while roll-to-roll ALD startups leveraged venture funding to commercialize wearable lines. Regional fabs collaborated with universities on machine-learning process control, enhancing film uniformity and throughput.

Competitive Landscape

Market concentration was moderate as leading panel makers in South Korea and China vied for share, yet Western firms shaped material and tool innovation. China’s subsidies lowered entry barriers, prompting capacity waves and squeezing equipment lead times.

Strategic alliances tightened: Merck added low-temperature silicon materials under its liviFlex™ umbrella to pair with Applied Materials’ new ALD cluster platform, allowing joint tool-chemistry demonstrations at customer sites. LG Display partnered with an automaker on custom encapsulated OLED dashboards capable of surviving −40 °C cycling, reflecting vertically integrated solution selling.

White-space revenue emerged in medical wearables and microLED AR glasses. Specialists patented maskless lithography quantum-dot pockets to deliver isotropic sealing and fine patterning.[4]Resul Ozdemir et al., “Quantum dot patterning and encapsulation,” ACS Applied Materials and Interfaces, hal.umontpellier.fr Forge Nano showcased machine-learning ALD controls that slashed cycle times, a differentiator for high-mix fabs. As applications diversify, suppliers segment portfolios by end-market certification, possibly increasing fragmentation even while headline consolidation among tier-one panel makers persists.

Thin Film Encapsulation Industry Leaders

-

Samsung SDI Co.,Ltd.

-

Applied Materials, Inc.

-

Kateeva

-

Veeco Instruments Inc.

-

LG Chem Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Samsung Display adopted tandem OLED stacks for automotive panels, integrating advanced encapsulation to extend durability in harsh car interiors.

- April 2025: Visionox earmarked USD 690 million for a flexible AMOLED research and development hub in Kunshan, with significant encapsulation investments for AR, VR, and automotive lines.

- March 2025: Merck KGaA expanded liviFlex™ with new low-temperature ALD silicon chemistries targeting free-form displays.

- February 2025: Applied Materials released a high-throughput ALD tool tuned for flexible-display encapsulation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Thin-film encapsulation is defined in our study as the multilayer stack of alternating inorganic and organic barrier films applied over moisture-sensitive electronic components, most notably flexible OLED displays, thin-film photovoltaics, emerging micro-LEDs, and printed sensors, to block oxygen and water vapor ingress below 10-6 g m-2 day-1 thresholds.

Scope exclusion (clarified): rigid glass-covered OLEDs and discrete desiccant can packages are outside the market boundary.

Segmentation Overview

- By Technology

- Plasma-Enhanced Chemical Vapor Deposition (PECVD)

- Atomic Layer Deposition (ALD)

- Inkjet Printing

- Vacuum Thermal Evaporation (VTE)

- Organic Vapor Phase Deposition (OVPD)

- Roll-to-Roll ALD

- Other Emerging Techniques (Parylene, Sol-Gel)

- By Layer Structure

- Inorganic Multilayer Barriers

- Organic Multilayer Barriers

- Hybrid (Organic+Inorganic) Barriers

- Single-Layer Encapsulation

- By Application

- Flexible OLED Displays

- Thin-Film Photovoltaics

- Flexible OLED Lighting

- Wearable and Medical Electronics

- Automotive Displays and Lighting

- Quantum-Dot and MicroLED Devices

- Printed Sensors and IoT Devices

- By Deposition Equipment Type

- Cluster PECVD Systems

- Inkjet Encapsulation Printers

- ALD Reactors

- Roll-to-Roll Vacuum Systems

- Laser-Assisted Deposition Tools

- By End-Use Industry

- Consumer Electronics

- Renewable Energy

- Automotive and Transportation

- Healthcare and Wearables

- Industrial and Aerospace

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Italy

- Rest of Europe

- Asia-Pacific

- China

- South Korea

- Japan

- India

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with deposition tool engineers, OLED stretch-cell line managers across Asia, and European automotive-display procurement heads allowed us to validate typical layer thickness, yield loss, and forward ASP moves. Follow-up surveys with wearable-device OEMs in North America helped us sense-check demand pools and refine regional penetration rates.

Desk Research

Our analysts first mapped global supply using open customs data, Korean and Chinese OLED export statistics, and quarterly OLED capacity trackers published by industry trade bodies such as SEMI, Korea Display Association, and China Optoelectronics Association. Patent analytics drawn from Questel highlighted deposition breakthroughs, while PECVD and ALD tool shipment tallies from government trade dashboards, together with company 10-Ks and investor decks, grounded the equipment side of the model. We also reviewed academic journals (SID Digest, Solar RRL) and procurement portals that list roll-to-roll vacuum systems prices, giving credible average-selling-price (ASP) markers. Company financials accessed through D&B Hoovers and news flows on Dow Jones Factiva filled temporal gaps. The sources named are illustrative; many additional publications were examined to corroborate figures and assumptions.

Market-Sizing & Forecasting

A top-down reconstruction that begins with installed Gen-5-to-Gen-8 flexible OLED capacity, shipment utilization, and square-meter film demand yields the first cut. Results are then stress-tested through selective bottom-up checks, cluster PECVD tool deliveries, sampled ALD reactor ASP × volume, and inkjet encapsulation printer sales to align totals. Key variables in the model include substrate utilization ramps, layer-thickness road maps, average barrier-stack ASP, flexible panel yield curves, regulatory incentives for roll-to-roll PV, and seasonality in premium-smartphone launches. Multivariate regression, anchored on capacity growth and ASP compression, projects demand to 2030; scenario analysis adjusts for upside in micro-LED adoption. Any bottom-up data voids are bridged using weighted regional proxies informed by primary interviews.

Data Validation & Update Cycle

Outputs pass three-tier analyst peer review, variance checks against historical import data and quarterly earnings signals, and final sign-off. Mordor refreshes every twelve months and issues interim revisions when material events, major fab expansions or technology node shifts, occur; a last-minute sweep ensures clients receive the freshest baseline.

Why Mordor's Thin Film Encapsulation Baseline Commands Reliability

Published estimates diverge because each firm chooses its own boundary, conversion rates, and refresh cadence.

Key gap drivers include whether photovoltaic films are counted, how ASP erosion is projected, and the frequency with which new Gen-8 fabs are added. Some providers rely on tool-maker revenue extrapolation alone or freeze exchange rates, whereas our model blends capacity trackers, ASP audits, and annual updates, giving balanced figures. External 2024-2025 values span USD 0.13 billion to USD 0.38 billion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.35 B (2025) | Mordor Intelligence | - |

| USD 0.377 B (2025) | Global Consultancy A | Counts deposition-equipment revenue only, omits downstream device stacking |

| USD 0.132 B (2024) | Industry Journal B | Limits scope to OLED displays, excludes photovoltaics and micro-LEDs; earlier base year |

| USD 0.200 B (2025) | Consulting Firm C | Excludes roll-to-roll ALD and medical wearables; partial regional coverage |

In short, by grounding our numbers in capacity utilization, verified ASPs, and an annual refresh, Mordor delivers a transparent, repeatable baseline decision-makers can trust.

Key Questions Answered in the Report

What is driving the rapid growth of the thin film encapsulation market?

High demand for flexible OLED displays, increased automotive adoption of curved dashboards, and rising medical wearable production are together pushing the market toward a 20.78% CAGR through 2030.

Which technology segment is expanding fastest within thin film encapsulation?

Atomic layer deposition is projected to grow at 26.4% CAGR because it delivers pinhole-free barriers at low temperatures suitable for foldable and automotive panels.

How significant is Asia-Pacific in thin film encapsulation manufacturing?

Asia-Pacific accounted for 69.5% of 2024 revenue, supported by large-scale fabs in South Korea and China and government incentives covering encapsulation equipment investments.

Why are single-layer barriers gaining traction despite hybrid dominance?

Material breakthroughs such as silbione-blended hybrimer films achieve ultra-low moisture rates while simplifying process steps, fueling a 29.1% CAGR for single-layer solutions.

What are the main constraints on thin film encapsulation adoption in automotive displays?

The report covers the Thin Film Encapsulation Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Thin Film Encapsulation Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: