Thalassemia Treatment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

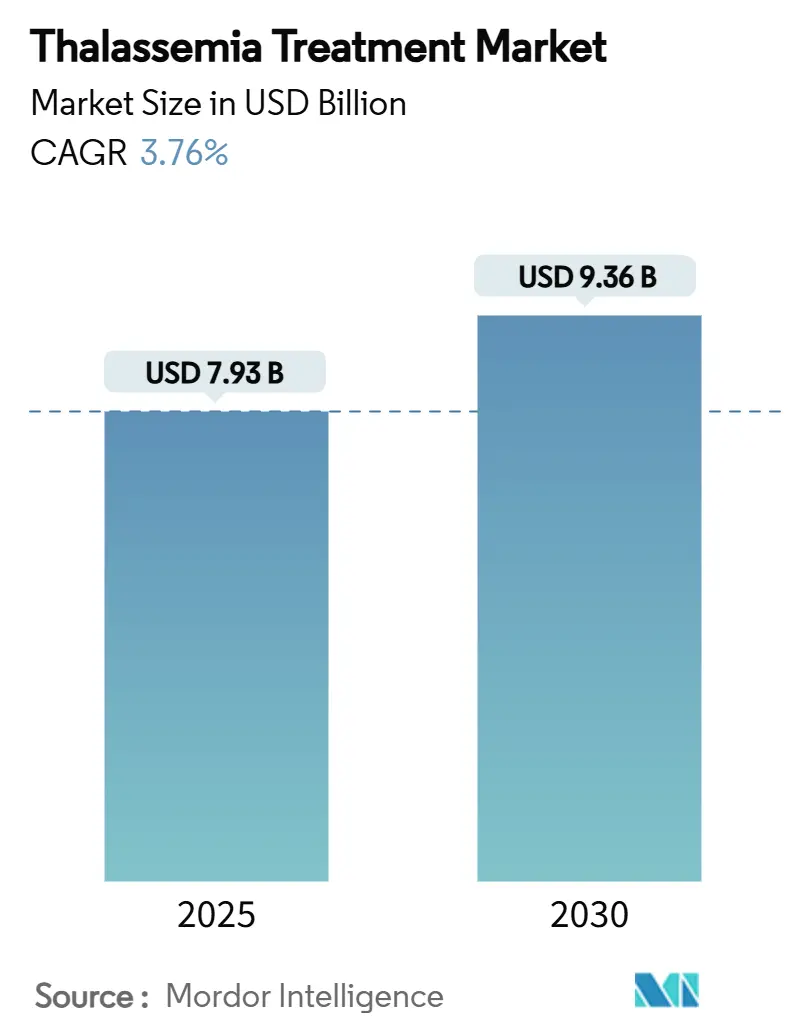

| Market Size (2025) | USD 7.93 Billion |

| Market Size (2030) | USD 9.36 Billion |

| Growth Rate (2025 - 2030) | 3.76% CAGR |

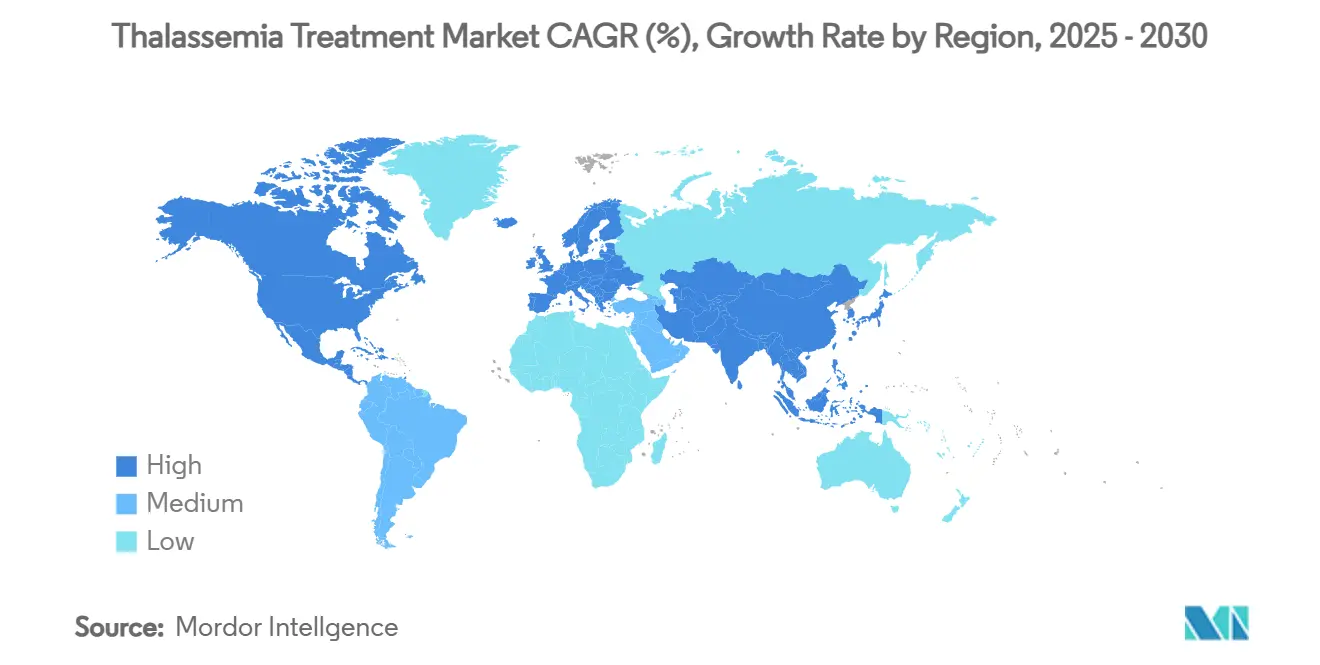

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thalassemia Treatment Market Analysis by Mordor Intelligence

The thalassemia treatment market size stood at USD 7.93 billion in 2025 and is forecast to reach USD 9.36 billion by 2030, reflecting a 3.76% CAGR. The thalassemia treatment market continues moving from supportive care to curative gene-editing solutions following the landmark approvals of CASGEVY and ZYNTEGLO in major economies FDA. Consistent demand from roughly 300,000 patients worldwide who live with severe forms of the disorder underpins revenue stability, even as curative options begin to narrow, transfusion volumes BDgene. Novel therapies, AI-enabled diagnostics and specialty clinic infrastructure are reshaping how payers, providers and manufacturers allocate resources inside the thalassemia treatment market. Investor confidence remains high, as illustrated by Carlyle and SK Capital’s purchase agreement for Bluebird Bio that hinges on ambitious USD 600 million sales milestones by 2027 Bluebird Bio. At the same time, access and affordability pressures—especially the USD 2.2 million list price for gene therapy—temper near-term adoption, forcing health systems to weigh large up-front payments against USD 5.4 million lifetime costs of conventional care HemaSphere.

Key Report Takeaways

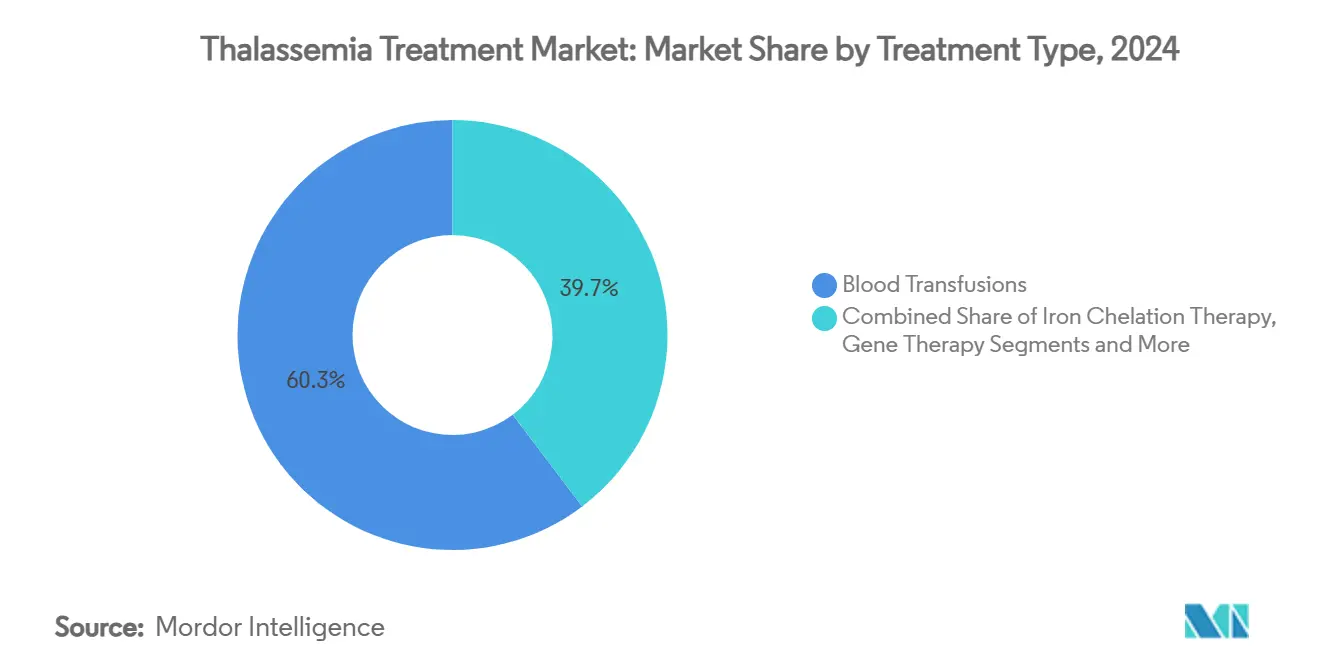

- By treatment type, blood transfusions dominated with a 60.3% share of the thalassemia treatment market in 2024, while gene therapy is on course for the fastest 13.3% CAGR through 2030.

- By disease type, beta thalassemia held 71.8% of thalassemia treatment market share in 2024; beta thalassemia major exhibits the quickest 9.5% expansion outlook to 2030.

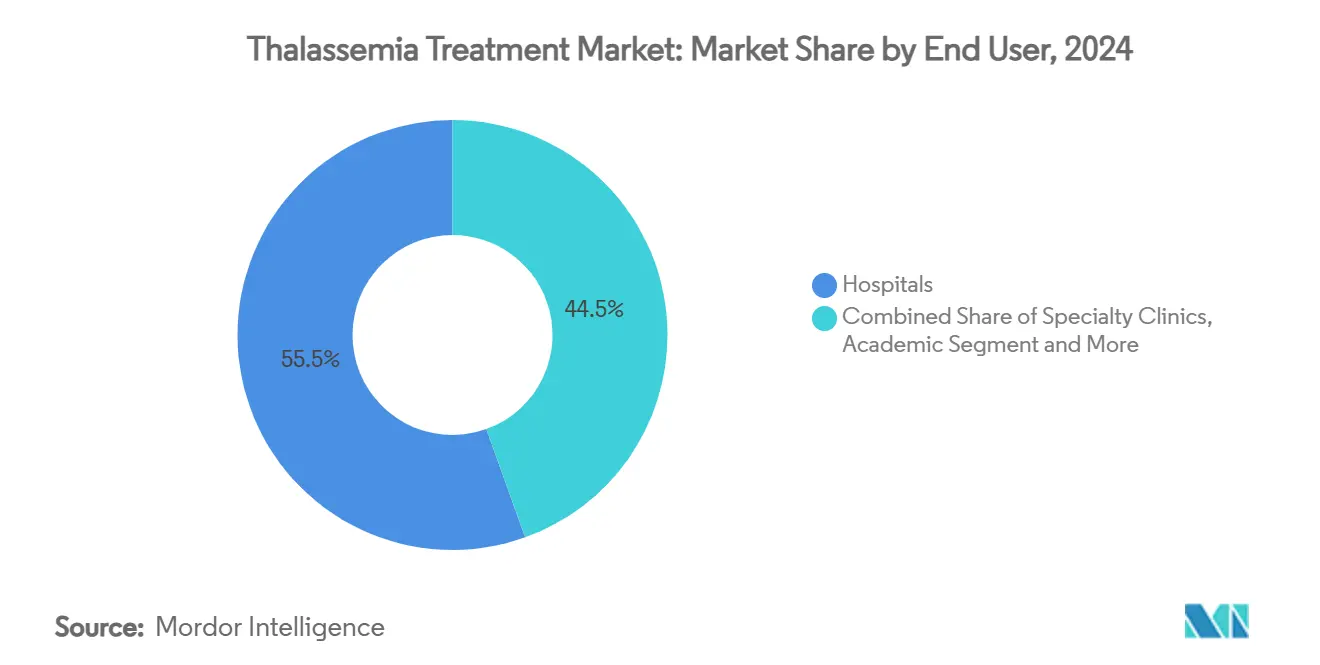

- By end user, hospitals accounted for 55.5% revenue in 2024, yet specialty clinics post an 8.5% CAGR as the preferred sites for gene-therapy delivery.

- By geography, Asia Pacific captured 48.5% of the thalassemia treatment market in 2024, whereas the Middle East & Africa region is projected to climb at a 7.3% CAGR through 2030.

Global Thalassemia Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Thalassemia | +0.80% | Global, concentrated in Mediterranean, South Asia, Southeast Asia | Long term (≥ 4 years) |

| Increasing Awareness & Screening Programmes | +0.60% | Asia Pacific, Middle East & Africa, with expansion to North America & EU | Medium term (2-4 years) |

| Regulatory Approvals Of Advanced Gene Therapies | +1.20% | North America & EU primary, expanding to Asia Pacific | Short term (≤ 2 years) |

| Inclusion Of Thalassemia In Newborn Genomic Panels | +0.40% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Low-Cost Oral Iron Chelators Improving Adherence | +0.30% | Global, particularly impactful in emerging markets | Medium term (2-4 years) |

| AI-Driven Blood-Match Algorithms Lowering Allo-Immunisation | +0.20% | Global, with faster adoption in technology-advanced healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Thalassemia

China hosts 47.48 million carriers and reports more than 20,000 affected births every year.[1]University of California San Francisco, “Global Burden of Thalassemia,” ucsf.eduComprehensive genetic screening uncovers additional undiagnosed cases and keeps the thalassemia treatment market expanding. Comparable patterns emerge in the Philippines, where 69.22% of tested individuals are positive, and alpha thalassemia dominates 65.77% of those in. High carrier frequencies of roughly 5% for alpha and 4% for beta thalassemia in southern China demand robust treatment capacity. In the Mediterranean, incidence varies widely—36.8 cases per 100,000 in southern countries versus 15.9 per 100,000 farther north, HAL Science. Together, these epidemiological realities secure long-run volume for every major therapy class.

Increasing Awareness & Screening Programmes

Newborn initiatives deliver earlier diagnoses and reshape patient funnels into the thalassemia treatment market. Saudi Arabia screened 5,715 babies and flagged 25.7% as positive, increasing the number of eligible patients for counseling and therapy. Denmark’s 16-year run saw diagnostic exams rise fivefold and yielded 5,142 trait and 136 intermediate/major confirmations.[2]HemaSphere Editorial Board, “Carrier Screening Outcomes in the Philippines,” hemspherejournal.com Iowa’s two-decade data set proves hemoglobinopathy screening’s maturing relevance. The WHO’s prevention-first playbook reduced incidence across Cyprus, Greece, and Italy, showing that screening and prenatal counseling complement rather than diminish downstream therapy demand.

Regulatory Approvals of Advanced Gene Therapies

The FDA’s 2024 clearance of CASGEVY introduced CRISPR gene editing as a practical cure for transfusion-dependent beta thalassemia AABB. Ninety-one percent of recipients achieved transfusion independence, a result echoed by EMA’s conditional approval, where 39 of 42 patients sustained hemoglobin above 9 g/dL EMA. Vertex opened nine centers to deliver the product and priced treatment at USD 2.2 million, a figure benchmarked against lifetime costs of USD 5.4 million. Late-stage candidates such as BDgene’s lentiviral therapy signal a pipeline on track to widen over the forecast period. Regulatory endorsements, therefore, accelerate market uptake and cement payer frameworks.

Inclusion of Thalassemia in Newborn Genomic Panels

Genomic screens bundle thalassemia with a broad set of diseases, using long-read sequencing to detect complex variants. Molecular Cytogenetics. Discovery of the αααα280 duplication in Chinese families, Orphanet Journal illustrated how next-generation methods sharpen diagnostic accuracy, modify counseling, and steer care early in life.[3]Orphanet Journal of Rare Diseases, “Discovery of αααα280 duplication in Chinese families,” biomedcentral.com Falling per-sample costs make these panels viable for population-scale programs, reinforcing the thalassemia treatment market’s patient base far into the future.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Curative Therapies | -0.90% | Global, particularly impactful in emerging markets | Short term (≤ 2 years) |

| Limited Voluntary Blood-Donor Pools | -0.50% | Global, with acute shortages in developing regions | Medium term (2-4 years) |

| Vector-Manufacturing Capacity Bottlenecks | -0.70% | North America & EU primary, expanding to Asia Pacific | Short term (≤ 2 years) |

| Regulatory Uncertainty For Genome-Edited Therapies | -0.40% | Global, with varying approval timelines across regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Curative Therapies

A list price of USD 2.2 million per gene-therapy infusion challenges immediate affordability. Conventional management costs USD 5.4 million spread across decades, yet budgeting models struggle with a single-year outlay. Bluebird Bio’s slow uptake and resulting USD 3.00 per-share buyout confirm how financing hurdles hinder adoption. Payers demand rigorous health-economic dossiers, pushing manufacturers toward installment plans or outcome-based contracts that remain nascent in most regions.

Limited Voluntary Blood-Donor Pools

Thalassemia patients may need multiple transfusions each week, but the donor supply remains inconsistent. Companies such as RedC Biotech are testing lab-grown red blood cells as a scalable solution for HospiMedica. Early-stage Israeli work on stem-cell-derived universal red cells shows promise, Ynet News, while the RESTORE trial studies their real-world efficacy. AI-driven matching cuts allo-immunisation, yet global expansion will take several years, leaving near-term gaps in traditional supply chains.

Segment Analysis

By Treatment Type: Gene Therapy Disrupts Traditional Paradigms

The thalassemia treatment market size for the gene-therapy segment is forecast to expand at 13.3% CAGR, reflecting its capacity to end lifelong transfusion needs in 91% of treated patients. Blood transfusions still account for a 60.3% slice of the thalassemia treatment market, underscoring their indispensability for those not yet eligible for curative solutions. Combination iron chelation reduced serum ferritin by 34.99% after one year, maintaining relevance for transfusion-dependent patients. Stem-cell transplantation delivers 85-90% thalassemia-free survival for low-risk profiles at UCSF but remains limited by donor compatibility. Luspatercept yielded ≥33% transfusion reduction in 21% of BELIEVE trial participants Reblozyl Pro, positioning it as a bridge therapy. Folic-acid supplementation improves hemoglobin and bone-pain scores in beta thalassemia minor, Evidence-Based Practice, though its role in major disease remains supplementary. Collectively, these modalities coexist, but the momentum clearly favors gene-editing platforms that redefine the risk-benefit equation for payers and patients.

Demand for sustainability is reinforced by manufacturing capacity expansion at nine authorized CASGEVY centers. Yet the thalassemia treatment market size attributed to transfusions will contract gradually as curative uptake rises. Iron chelation manufacturers, led by Novartis and Apotex, are therefore launching adherence-enhancing formulations to defend revenue. Transition dynamics, along with luspatercept’s proven quality-of-life gains, signal an ecosystem in flux rather than immediate displacement of legacy options.

Note: Segment shares of all individual segments available upon report purchase

By Disease Type: Beta Thalassemia Dominance Drives Innovation

Beta thalassemia owns 71.8% of the thalassemia treatment market share in 2024 and leads growth at 9.5% CAGR as the most severe phenotype spurs aggressive therapy adoption. CASGEVY and ZYNTEGLO specifically target this cohort, rationalising their premium pricing. Alpha thalassemia, prevalent in Southeast Asia, has fewer options, though Bristol Myers Squibb’s Phase 2 luspatercept program for HbH disease marks progress for HemaSphere. Mutation diversity, such as the -α3.7 deletion responsible for 69.2% of Saudi cases, complicates universal solutions, reinforcing the need for genotype-specific approaches.

Beta thalassemia’s outsized burden attracts disproportionate R&D, leaving a therapeutic gap for alpha variants. Yet newborn screening in high-incidence geographies identifies alpha carriers earlier, ensuring that the thalassemia treatment market remains diverse. As fetal hemoglobin modulation strategies show promise for both subtypes, product pipelines may converge, but commercial priorities currently rest with beta-focused programs that match higher severity and willingness-to-pay profiles.

By End User: Specialty Clinics Emerge as Gene Therapy Hubs

Hospitals held 55.5% revenue in 2024 by delivering transfusions and multidisciplinary care. As autologous cell therapies reach commercial scale, specialty clinics record an 8.5% CAGR, reflecting stringent facility and staff requirements. Nine CASGEVY centers spotlight the hub model, with hospitals feeding candidates into specialized units for conditioning, infusion, and monitoring at Vertex Pharmaceuticals. Academic sites remain critical to clinical trials; UCSF leads registries and mitapivat investigations.

Smartphone hemoglobin prediction systems with MAE 1.34 and MSE 2.85 BMC Medical Informatics support remote management, allowing clinics to space in-person visits. Nursing protocols for stem-cell transplantation in China boosted discharge readiness and satisfaction scores. Together, these developments illustrate a distributed yet integrated care architecture, aligning with value-based reimbursement trends across the thalassemia treatment industry.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia Pacific’s 48.5% share of the thalassemia treatment market stems from endemic carrier rates and improved funding for diagnostics. China alone lifts demand through 47.48 million carriers and an expanding network of treatment centers UCSF. The thalassemia treatment market size in Asia Pacific is projected to widen as provincial reimbursements now cover parts of gene-therapy cost for eligible children. Middle East & Africa, though smaller, posts the fastest 7.3% CAGR thanks to Saudi Arabia’s high newborn positivity and public-health commitment HemaSphere. Regional insurers increasingly authorise luspatercept as an intermediate measure, bridging systemic capacity gaps.

Europe benefits from decades of prevention, yet still harbors concentrated patient pools in Italy, Greece and Cyprus where screening reduced incidence but not existing caseloads HAL Science. The United States accelerates adoption following January 2024 FDA approvals, with insurers evaluating outcomes-based instalments for curative products AABB. Latin America and parts of South Asia remain under-diagnosed; as awareness grows, newly identified patients will enlarge the global thalassemia treatment market.

Healthcare expenditure disparities create unequal access, but technology transfer initiatives, long-term loan financing and donor-supported infrastructure programs intend to narrow the gap. The geography mix therefore sustains a two-speed market: advanced economies drive premium gene-therapy revenue while emerging regions continue anchoring transfusion and iron-chelation volumes.

Competitive Landscape

Moderate fragmentation persists as incumbents guard established categories and biotechs carve out the curative frontier. Novartis and Apotex still dominate iron chelation with Exjade and Ferriprox, but margins erode as generic deferiprone expands. Vertex Pharmaceuticals and CRISPR Therapeutics command the nascent gene-editing niche with CASGEVY, challenged by Bluebird Bio’s ZYNTEGLO and BDgene’s coming lentiviral entrant BioSpace. Carlyle and SK Capital’s acquisition of Bluebird signalled private-equity conviction that commercial hurdles can be solved with more capital and operational discipline.

Bristol Myers Squibb leverages to bridge transfusion dependence and curative therapies, illustrating how large firms diversify approaches. Technology differentiation also surfaces in AI-based monitoring tools; automated MRI iron-load quantification achieved 96% sensitivity and 98% specificity, HemaSphere, giving vendors analytics-as-a-service revenue lines. White-space remains in alpha-thalassemia therapeutics, presenting entry points for agile biotechs. Overall, the thalassemia treatment market rewards companies that align manufacturing, reimbursement, and logistics in addition to clinical performance.

Price dynamics add competitive tension. CASGEVY’s USD 2.2 million level set the ceiling, but pay-for-results contracts may compress average realizations. Meanwhile, CSL’s Ferinject faces European generics Live Mint, reminding investors that volume markets can turn rapid growth into price pressure. Strategy in this environment centers on portfolio breadth, manufacturing know-how, and payer engagement—capabilities that differentiate sustainable leaders from single-asset specialists.

Thalassemia Treatment Industry Leaders

Bluebird Bio

Novartis AG

ApoPharma Inc

Bellicum Pharmaceuticals

Pfizer, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Agios Pharmaceuticals received FDA acceptance of a supplemental NDA for PYRUKYND (mitapivat) in adult thalassemia, marking the first oral disease-modifying therapy aimed at chronic anemia.

- January 2025: Bluebird Bio closed its sale to Carlyle and SK Capital at USD 3.00 per share plus contingent value rights worth USD 6.84 if sales hit USD 600 million by 2027.

- December 2024: Bristol Myers Squibb reported long-term luspatercept data at ASH 2024, highlighting iron-overload improvement and better fatigue scores in beta-thalassemia.

- August 2024: NICE approved CASGEVY for NHS coverage at seven UK centers, opening access to roughly 460 eligible patients.

Global Thalassemia Treatment Market Report Scope

As per the scope of the report thalassemia is a blood disorder passed down through families in which the body makes an abnormal form or insufficient amount of hemoglobin. This report is segmented by Treatment Type, by Disease Type, by End-User, and by Geography.

| Blood Transfusions |

| Iron Chelation Therapy |

| Gene Therapy |

| Haematopoietic Stem-Cell Transplantation |

| Luspatercept & Erythroid-maturation Agents |

| Folic Acid & supportive supplements |

| Others |

| Alpha thalassemia |

| Beta thalassemia |

| Hospitals |

| Specialty Clinics |

| Academic & Research Institutes |

| Home-care settings |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Blood Transfusions | |

| Iron Chelation Therapy | ||

| Gene Therapy | ||

| Haematopoietic Stem-Cell Transplantation | ||

| Luspatercept & Erythroid-maturation Agents | ||

| Folic Acid & supportive supplements | ||

| Others | ||

| By Disease Type | Alpha thalassemia | |

| Beta thalassemia | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Academic & Research Institutes | ||

| Home-care settings | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the thalassemia treatment market?

The thalassemia treatment market size reached USD 7.93 billion in 2025 and is projected to hit USD 9.36 billion by 2030.

How fast is the gene-therapy segment growing?

Gene therapy is expanding at a 13.3% CAGR through 2030, the fastest among all treatment categories, owing to CASGEVY and ZYNTEGLO approvals.

Which region leads thalassemia treatment revenue?

Asia Pacific generated 48.5% of global revenue in 2024, reflecting high carrier prevalence and growing access to advanced therapies.

Why are specialty clinics gaining traction?

Specialty clinics post an 8.5% CAGR because autologous gene-editing therapies require dedicated facilities, trained staff and strict quality controls.

What barriers limit curative therapy adoption?

Up-front pricing of USD 2.2 million per treatment and limited reimbursement structures slow widespread uptake despite long-term cost advantages.