Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

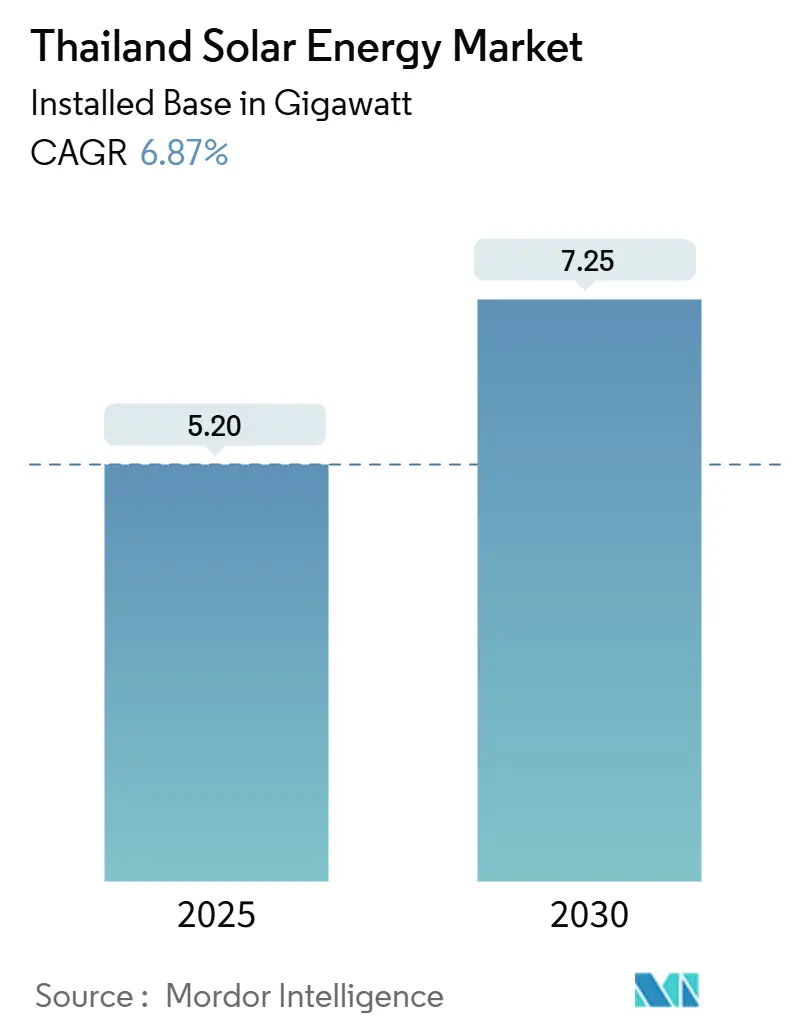

| Market Volume (2025) | 5.20 gigawatt |

| Market Volume (2030) | 7.25 gigawatt |

| Growth Rate (2025 - 2030) | 6.87% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thailand Solar Energy Market Analysis by Mordor Intelligence

The Thailand Solar Energy Market size in terms of installed base is expected to grow from 5.20 gigawatt in 2025 to 7.25 gigawatt by 2030, at a CAGR of 6.87% during the forecast period (2025-2030).

Continued tariff pressure, renewable energy policy targets, and declining photovoltaic costs position the Thai solar energy market for steady growth, despite grid infrastructure bottlenecks. A 2,000 MW direct power purchase pilot, approved in 2024, is opening an alternative procurement pathway for data centers and large manufacturers, which shortens sales cycles for independent power producers. Module prices that fell to USD 0.10–0.12 per watt in 2024 trimmed commercial payback periods to five to seven years, enhancing bankability across all customer classes. Floating-solar hybrid projects planned for nine hydroelectric reservoirs will add 2.7 GW of incremental capacity, circumventing land-acquisition hurdles that limit the use of ground-mounted sites. Solar leasing models and simplified licensing for systems below 1 MW are driving a residential installation boom in Bangkok and peri-urban provinces, signaling broader democratization of solar access.

Key Report Takeaways

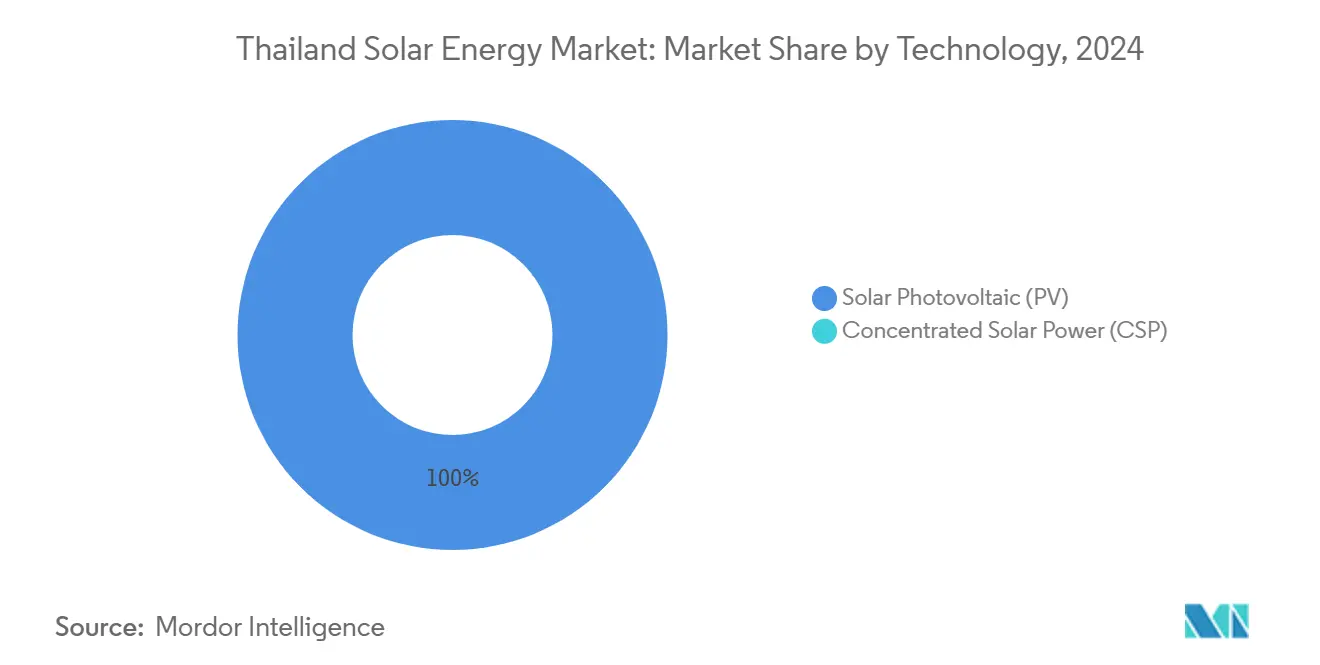

- By 2024, photovoltaic systems had captured 100% of the market share, while concentrated solar power remained commercially inactive.

- By grid type, on-grid systems held 90.4% of the Thailand solar energy market share in 2024, whereas the off-grid segment is forecast to post a 9.6% CAGR through 2030.

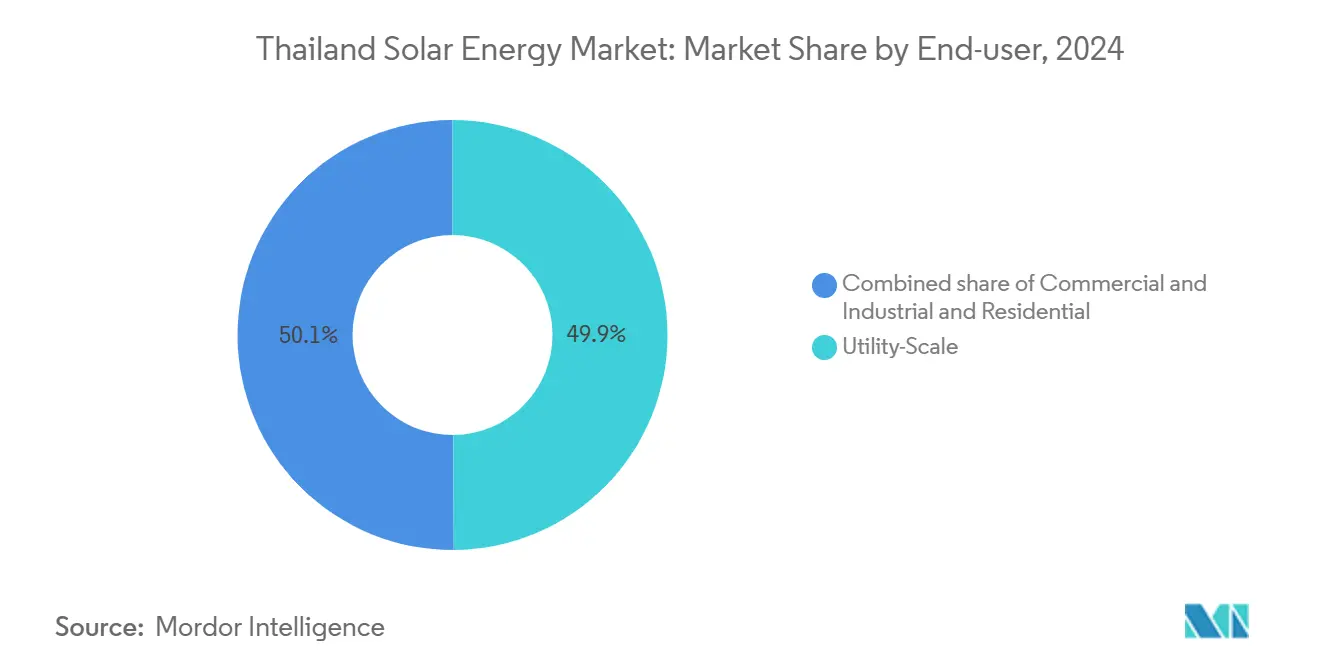

- By end-user, utility-scale assets accounted for 49.9% of the Thailand solar energy market size in 2024, yet residential rooftops are advancing at a 10.8% CAGR, the fastest pace among all categories.

Thailand Solar Energy Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising retail-grid tariffs and price swings | 1.80% | Industrial zones in Rayong, Chonburi, Samut Prakan | Medium term (2–4 years) |

| Rapid cost drop in bifacial and TOPCon PV | 1.50% | Nationwide, most visible in utility-scale bids | Short term (≤ 2 years) |

| Direct PPA pilot for commercial buyers | 1.30% | Bangkok Metropolitan Region and Eastern Economic Corridor | Medium term (2–4 years) |

| Government push for 2.7 GW floating hybrids | 0.90% | Central and Northern dam sites | Long term (≥ 4 years) |

| Agro-photovoltaic land-use programs | 0.60% | Northeastern farming provinces | Long term (≥ 4 years) |

| Growing demand for green RECs | 0.70% | Export-oriented factories in the Eastern Economic Corridor | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Retail-Grid Tariffs and Electricity-Price Volatility

Retail tariffs remained at THB 4.15–4.18 per kWh in 2024; however, the Electricity Generating Authority of Thailand reported cumulative losses of nearly THB 98 billion, suggesting an 8–12% tariff hike by late 2025 is likely. Manufacturers in the Eastern Economic Corridor now view rooftop solar as a hedge against gas price swings, as a typical 1 MW installation pays for itself within seven years. Data from the Energy Policy and Planning Office show that gas-fired units still supply about 60% of the grid's electricity, linking tariffs to spot LNG imports. Commercial buyers facing European Union carbon-border fees have accelerated solar procurement to protect export margins. The resulting demand is giving the Thai solar energy market fresh momentum across both on-site and third-party financed systems.

Rapid Cost Decline of Bifacial and TOPCon PV Modules

Average bifacial module prices declined to USD 0.10–0.12 per watt in 2024, while TOPCon cells achieved 24–25% efficiencies at only marginally higher costs. Developers now negotiate multi-year supply contracts, locking in component prices to 2027 and stabilizing levelized energy costs. Lower capital intensity has enabled smaller rooftops to achieve five-year paybacks even under net-billing. Oversupply in Chinese factories diverted products to Southeast Asia, further pushing down local prices. Although United States antidumping tariffs on Thai-assembled panels reshuffled export channels in 2024, domestic oversupply created broader price relief for local projects.

Direct PPA Pilot Opening Commercial and Industrial Demand

The Energy Regulatory Commission authorized a 2,000 MW direct-purchase pilot that allows data centers and factories to contract electricity from independent producers at prices 10–15% lower than grid retail rates. Draft third-party-access codes, due to be finalized by mid-2025, will codify wheeling charges and metering rules. Bangkok’s data-center cluster, which already consumes 150–200 MW, is expected to claim early allocations. Automotive suppliers in Rayong and electronics manufacturers in Samut Prakan have expressed interest, citing the ability to secure renewable energy for Scope 2 emission accounting. Direct PPAs therefore create a strong offtake pipeline that should accelerate the Thailand solar energy market.

Government Push for 2.7 GW Floating-Solar Hybrids

Sixteen floating-solar projects, totaling 2.7 GW, will be installed across nine hydro reservoirs, leveraging 12,000 hectares of water surface area managed. The 24 MW Ubolratana array commenced commercial operations in March 2024 and achieved a 5–8% higher energy yield, thanks to water cooling that keeps panel temperatures lower. The 205 MW Bhumibol Dam tender, which opened in March 2025, has attracted consortium bids pairing Thai developers with international EPC firms. Floating designs avoid land-acquisition disputes, while coupling with hydropower improves ramping flexibility in the national grid. A feed-in tariff of THB 2.8331 per kWh for solar-plus-battery hybrids underpins project economics.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-cycle grid-connection approvals & curtailment risks | -0.8% | National, with acute bottlenecks in Bangkok Metropolitan Region and Eastern Economic Corridor | Medium term (2-4 years) |

| Saturated feeders in Bangkok & Eastern Economic Corridor | -0.6% | Bangkok, Samut Prakan, Chonburi, and Rayong provinces | Short term (≤ 2 years) |

| Rising import tariffs on Thai modules in US/EU markets | -0.5% | National impact on export-oriented manufacturers; indirect effect on domestic pricing and supply chain | Medium term (2-4 years) |

| Limited domestic Li-ion cell production for BESS | -0.4% | National, with concentrated impact on hybrid solar-plus-storage projects in utility-scale and C&I segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Long-Cycle Grid-Connection Approvals and Curtailment Risks

Developers report approval times of six to eighteen months because utilities must conduct voltage-stability studies and substation-capacity reviews before granting interconnection. Projects larger than 10 MW also require environmental impact assessments and National Energy Policy Council sign-offs, which extend pre-construction periods and increase holding costs. In 2024, curtailment events totaled up to fifty hours in feeders where solar penetration exceeded 18% of daytime demand. Absent real-time pricing or mandatory storage, over-generation causes forced shutdowns that undermine project revenue. These obstacles shave nearly one percentage point off forecast growth.

Saturated Feeders in Bangkok and Eastern Economic Corridor

Distribution circuits serving Bangkok’s business district and nearby industrial estates already run at 85–95% capacity during sunny midday periods. The Metropolitan Electricity Authority has planned THB 45 billion of substation upgrades, yet construction lags behind solar deployment. Developers often self-finance feeder reinforcements at USD 150,000–300,000 per MW, raising project capital requirements. Small and medium enterprises, therefore, face longer waits and higher costs than large corporates. Without accelerated grid investment, feeder saturation will continue to constrain rooftop installations in the densest load centers.

Segment Analysis

By Technology Photovoltaic Dominance Continues

Photovoltaic systems accounted for 100% of the installed capacity in 2024 and are expected to expand at a 6.9% growth rate through 2030. The Thailand solar energy market size for photovoltaic technology reached 4.85 GW in 2024 and is expected to reach 7.25 GW by 2030, maintaining a significant share, as concentrated solar power remains economically impractical under Thailand’s humid climate.[1]Department of Alternative Energy Development and Efficiency, “Solar PV Status Report 2024,” dede.go.th Bifacial modules that capture reflected irradiance are quickly becoming standard in floating-solar tenders, with the Ubolratana project registering 5–8% higher output than monofacial arrays. TOPCon cells, which offer 24–25% conversion efficiency, are overtaking PERC modules in utility-scale bids where land constraints justify premium pricing.

Continuous cost declines widen the economic gap between photovoltaic and concentrated solar power, which needs direct-normal-irradiance levels rarely achieved in the monsoon season. The Ministry of Energy’s 2024 feed-in-tariff schedule excludes concentrated solar power, effectively cementing photovoltaics’ monopoly. Looking forward, International Energy Agency data project module prices dropping another 15–20% by 2027, ensuring photovoltaic technologies remain the only commercially viable solar option in Thailand.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Grid Type Off-Grid Uptake Accelerates

On-grid installations accounted for 90.4% of capacity in 2024, primarily driven by utility-scale farms and commercial rooftops located near Bangkok. The Thailand solar energy market share for off-grid systems is currently small, yet the off-grid segment is forecast to outpace the overall market at a 9.6% CAGR through 2030. Northern and Northeastern provinces lead the way in off-grid adoption, where rural electrification costs exceed USD 50,000 per kilometer. Agro-photovoltaic pilots, which pair solar panels with crop cultivation, add farm revenue while powering irrigation, improving debt service coverage, and shortening paybacks.[2]Kasetsart University, “Agro-PV Field Trial Results,” ku.ac.th

Net-billing, introduced in 2024, still compensates prosumers at wholesale rates that support paybacks of three to five years in high-tariff zones. The Metropolitan Electricity Authority reduced the approval time for sub-1 MW rooftops to thirty days, resulting in a 40% increase in applications last year. Off-grid systems also serve industrial estates facing curtailment risk or inadequate feeder capacity, underpinning the strongest near-term growth.

By End-User Residential Growth Leads

Utility-scale assets retained 49.9% of installed capacity in 2024, yet residential rooftops are forecast to post a 10.8% CAGR to 2030, the fastest expansion among all segments. The Thailand solar energy market size for residential installations stood at 68.2 MW in September 2024 and is growing rapidly, driven by zero-upfront-cost leasing contracts. Middle-income homeowners in Bangkok, Chiang Mai, and Phuket now qualify for third-party financed systems that promise bill savings from the very first day.

Commercial and industrial users occupy the middle ground. Data centers in Bangkok and Chonburi already consume 150–200 MW and are early adopters of solar-plus-battery PPA contracts. Automotive suppliers in Rayong and electronics plants in Samut Prakan line up for direct-PPA allocations that can cut power costs by up to 15%. Despite slower growth, utility-scale projects continue to anchor the sector through large floating-solar tenders and ground-mounted farms, which multilateral lenders finance.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Central Thailand, including the Bangkok Metropolitan Region, hosted approximately 35% of the installed capacity in 2024, thanks to its dense commercial and industrial loads.[3]Industrial Estate Authority of Thailand, “Industrial Estate Solar Adoption Survey,” ieat.go.th The Eastern Economic Corridor contributed another 28% and remains the primary destination for new rooftop and ground-mounted projects because export-oriented factories demand low-carbon power. Northern provinces, such as Chiang Mai and Lampang, have emerged as agro-photovoltaic hubs, where elevated arrays coexist with rice and vegetable crops, thereby reducing land-use conflicts.

Floating-solar hybrids slated for nine dam reservoirs across Central and Northern regions will redistribute capacity over the forecast horizon. The 205 MW Bhumibol Dam project in Tak and the 158 MW Srinakarin Dam array in Kanchanaburi will shift development inland, easing grid pressure on Bangkok. Saturated feeders in the capital currently operate at up to 95% during midday generation peaks and limit new rooftop interconnections until substation upgrades finish by 2028.

Northeastern provinces garner attention through agro-photovoltaic pilots that pair crop shading benefits with electricity sales. Kasetsart University trials in Nakhon Ratchasima have shown that elevated panels cut water demand and produce more than 1 MWh per rai annually. The Department of Alternative Energy Development and Efficiency is targeting up to 800 MW of such capacity by 2028, attracted by land costs that are three to four times lower than in Central Thailand. Southern resort provinces like Phuket also adopt rooftop solar on hotels, though monsoon clouds limit capacity factors to 14–16% compared with 18–20% in Central and Northeastern zones.

Competitive Landscape

Domestic developers SPCG, BCPG, Thai Solar Energy, B.Grimm Power, and Energy Absolute jointly control approximately 60% of the utility-scale capacity, resulting in a moderate level of concentration in the Thai solar energy market. These incumbents differentiate through vertical integration and regional diversification: Energy Absolute is building a 5 GWh battery plant, while BCPG invests in Japanese and Philippine assets to hedge domestic exposure. Utility-scale bids are increasingly favoring bifacial panels to boost energy yield on limited land, benefiting Chinese suppliers JinkoSolar, Trina Solar, and LONGi, which dominate component imports.

Huawei and Sungrow retain a combined 55–60% share of inverter sales by offering integrated energy management software that helps projects meet grid support requirements. The imposition of United States antidumping duties on Thai-assembled modules forced exporters to divert output toward domestic and ASEAN markets, intensifying price competition for local projects.[4]Electrical and Electronics Institute of Thailand, “Certified PV Modules List,” eei.or.th Compliance testing under IEC 61215 and IEC 61730 is conducted by the Electrical and Electronics Institute of Thailand, creating a baseline for quality assurance across the supply chain.

White-space opportunities lie in commercial and industrial rooftops, where the 2,000 MW direct-PPA pilot remains undersubscribed because many developers hesitate over regulatory timing. Residential leasing firms and agro-photovoltaic specialists are also emerging. Their novel business models lower financing barriers and expand addressable demand, challenging traditional utility-scale players to adapt.

Thailand Solar Energy Industry Leaders

-

Energy Absolute Public Company Limited

-

SPCG Public Company Limited

-

Thai Solar Energy PLC

-

BCPG Public Company Limited (BCPG)

-

B.Grimm Power PLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Actis-backed Levanta Renewables has acquired a 91 MW operational solar portfolio in Thailand. The portfolio spans 10 sites in the Suphanburi and Kanchanaburi provinces and generates approximately 155 GWh of electricity annually under long-term power purchase agreements (PPAs) with the Provincial Electricity Authority (PEA).

- July 2025: CleanMax Energy (Thailand) has secured USD 45 million in debt financing from the International Finance Corporation (IFC) to promote solar power adoption in Thailand's commercial and industrial (C&I) sectors. Announced in July 2025, the investment aims to provide businesses with reliable and affordable clean energy, supporting the country's renewable energy goals.

- November 2024: Gulf Renewable Energy Company Limited, a subsidiary of Gulf Energy Development Public Company Limited (Gulf), has secured a USD 820 million loan from the Asian Development Bank (ADB) to finance the construction of 12 renewable energy projects in Thailand.

Thailand Solar Energy Market Report Scope

Solar power is the conversion of solar energy into thermal or electrical energy. Solar energy is the cleanest and most abundant renewable energy source accessible, and it may be used to generate electricity, provide light or a comfortable interior environment, and heat water for home, commercial, or industrial purposes.

The Thailand solar energy market is segmented by technology, grid type, and end-user. By technology, the market is segmented into solar photovoltaic (PV) and concentrated solar power (CSP). By grid type, the market is segmented into On-Grid and Off-Grid. By end user, the market is segmented into utility-scale, commercial and industrial (C&I), and residential. For each segment, the market size and forecasts are based on installed capacity.

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What capacity target does the Power Development Plan set for renewables in Thailand by 2037?

The plan calls for renewables to supply 51% of the national electricity mix by 2037, up from 20% in 2023.

How fast is the off-grid solar segment expected to grow through 2030?

Off-grid projects are projected to expand at a 9.6% CAGR, outpacing the overall market.

Why are floating-solar hybrids attractive for Thailand?

They utilize reservoir surfaces, avoid land-acquisition conflicts, and benefit from hydro coupling that reduces curtailment.

What is the main operational hurdle for new utility-scale projects near Bangkok?

Grid-connection approvals can take up to eighteen months because many feeders are already saturated.

How do direct PPAs benefit industrial buyers?

They allow factories and data centers to contract renewable power at prices 10–15% below retail tariffs while meeting emission-disclosure rules.

Which technology currently holds the entire market share in Thailand’s solar sector?

Photovoltaic technology accounts for 100% of installed capacity, with concentrated solar power absent due to unfavorable climate conditions.

Page last updated on: