Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

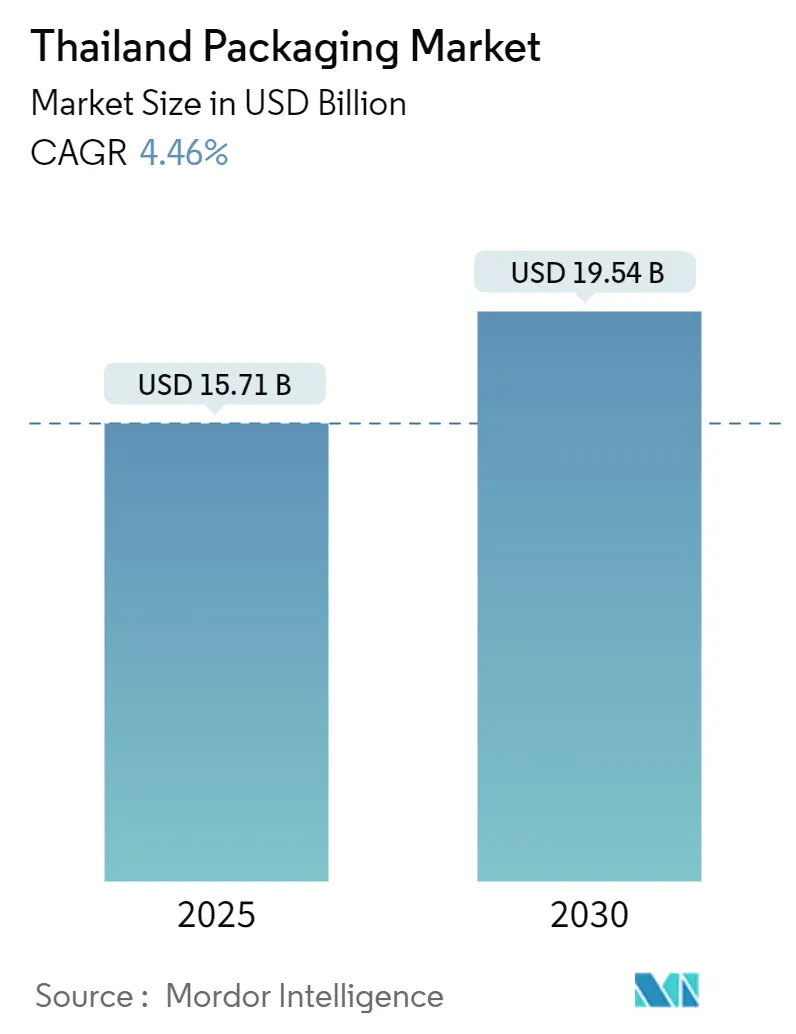

| Market Size (2025) | USD 15.71 Billion |

| Market Size (2030) | USD 19.54 Billion |

| Growth Rate (2025 - 2030) | 4.46% CAGR |

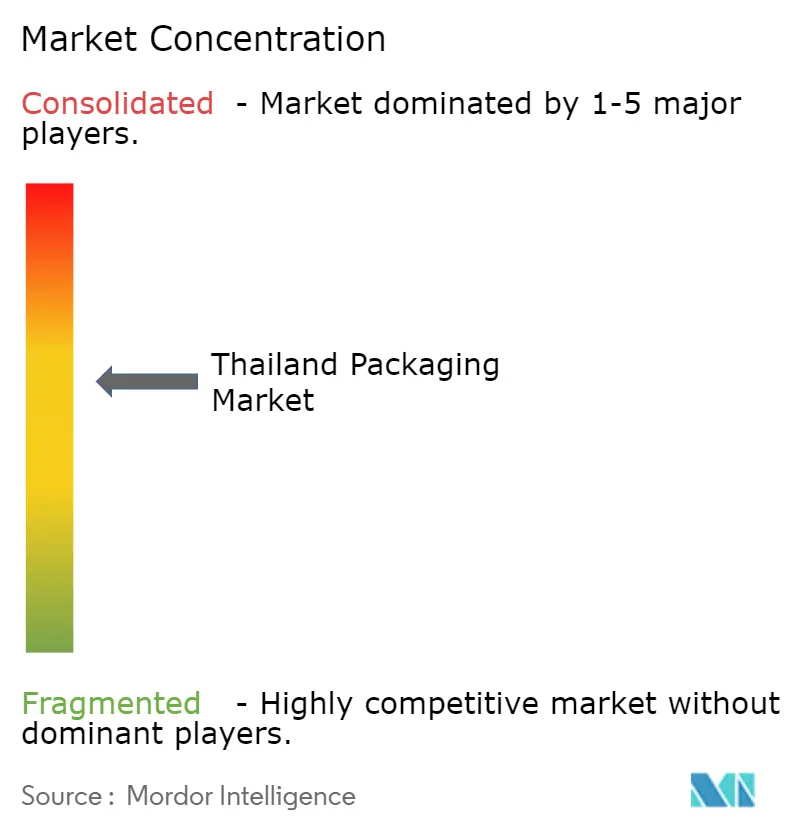

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thailand Packaging Market Analysis by Mordor Intelligence

Thailand's packaging market size stands at USD 15.71 billion in 2025 and is forecast to reach USD 19.54 billion by 2030, expanding at a 4.46% CAGR over the period. Robust foreign investment, valued 43% higher in the first four months of 2025, underpins rising demand for primary and secondary packs across the food, beverage, and fast-moving consumer goods sectors. Accelerated e-commerce growth, from USD 26.5 billion in 2023 toward USD 32 billion in 2025, is shifting preferences toward lightweight, flexible formats that lower logistics costs and improve unboxing safety. Circular-economy mandates anchored in the National 3R Strategy are steering material substitution toward paper, paperboard and food-grade rPET, while Board of Investment (BOI) incentives for automation help producers offset labor shortages and margin pressure. Against this backdrop, Thailand's packaging market participants face feedstock cost swings and single-use plastic restrictions, yet benefit from the country’s plan to rank among the world’s top 10 processed-food exporters by 2027.

Key Report Takeaways

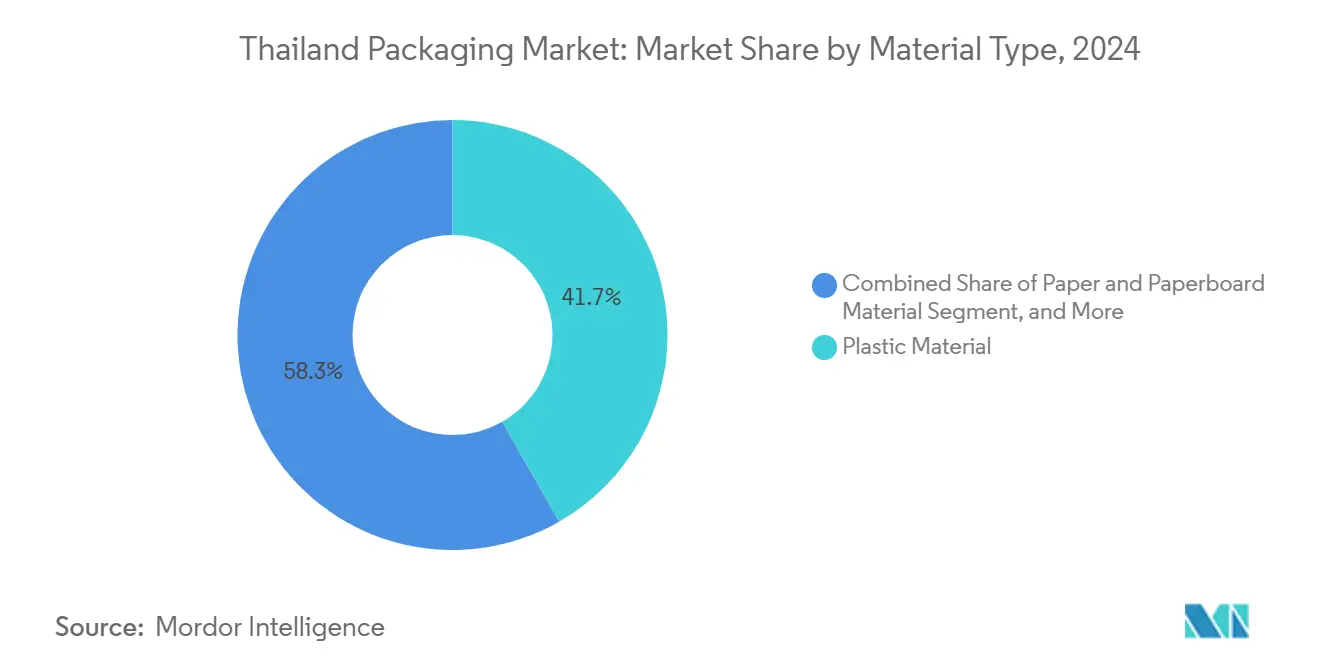

- By material type, the Thailand packaging market size for paper and paperboard is projected to grow at a 4.94% CAGR between 2025-2030.

- By product type, plastic products captured 44.23% of the Thailand packaging market share in 2024.

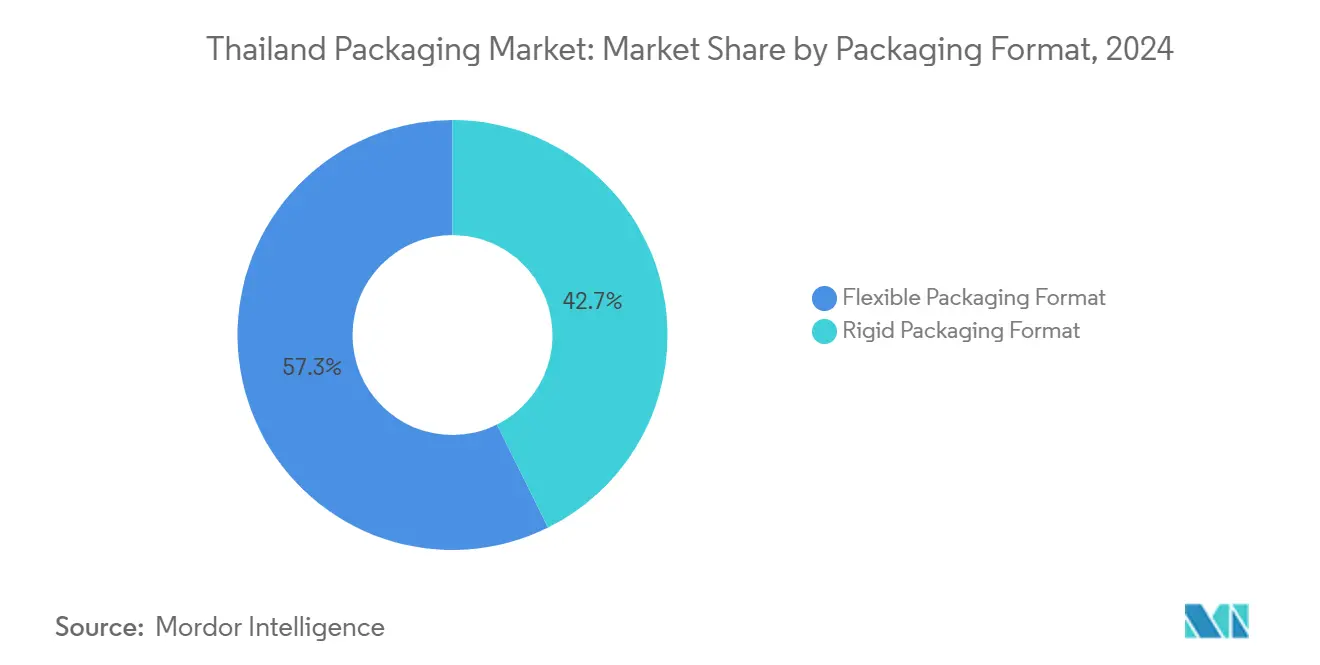

- By packaging format, the Thailand packaging market size for flexible packaging format is projected to grow at a 4.98% CAGR between 2025-2030.

- By end-user, food applications captured 29.45% of the Thailand packaging market share in 2024.

Thailand Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising food and beverage output | +1.2% | Central and Eastern Thailand | Medium term (2-4 years) |

| Growth of e-commerce and parcel volumes | +0.9% | Urban centers | Short term (≤ 2 years) |

| Demand for convenient and flexible packs | +0.8% | Nationwide | Medium term (2-4 years) |

| Sustainability and circular-economy mandates | +0.7% | Nationwide | Long term (≥ 4 years) |

| BOI incentives for packaging automation | +0.5% | Eastern Economic Corridor | Medium term (2-4 years) |

| Cannabis-infused food and beverage needs child-safe packs | +0.2% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Food and Beverage Output Drives Core Demand

The government’s goal of placing Thai processed foods among the global top-10 exporters by 2027, supported by 2022 food exports worth USD 38.8 billion, ensures sustained demand for bottles, cans, trays, and secondary corrugated packs. Capacity-utilization gains and agri-budget allocations intensify demand for hygienic, value-added packaging to extend shelf life. Brands also adopt recyclable structures to satisfy eco-labeling requirements. Consequently, Thailand's packaging market sees upstream investments in multilayer films and rPET pre-form lines that balance performance with lower carbon footprints.

E-commerce Expansion Reshapes Packaging Requirements

The online retail value leapt from USD 26.5 billion in 2023 toward USD 32 billion in 2025, with mobile commerce responsible for more than 80% of sales. Frequent orders: 71% of smartphone users buy online at least twice per month, driving parcel volumes that demand shock-resistant mailers and tamper-evident tapes. As B2C orders comprise 50% of e-commerce sales, brands shift toward flexible pouches and easy-open tear strips to elevate unboxing appeal. Digital payments topping USD 33 billion in 2023 further validate sustainable growth, while new platform regulations tighten label and traceability standards that favor QR-coded packs. These shifts anchor flexible formats at the forefront of Thailand's packaging market innovation.

Convenience-Driven Consumer Behavior Accelerates Flexible Formats

Urban households prioritize portability and single-serve SKUs, propelling pouch and stick-pack uptake. Ready-to-drink lines gain share even under sugar-tax pressure because smaller packs allow portion control and price accessibility. Restaurant rebound and tourism revival add volumes in sauces, condiments and on-the-go snacks. Smart codes on sachets connect consumers to provenance data and promotional content, enhancing engagement. Thus, flexible units amplify their 57.33% lead within the Thailand packaging market.

Government Sustainability Mandates Transform Industry Standards

Thailand's National 3R Strategy and National Master Plan for Waste Management establish regulatory frameworks that influence packaging material selection and design. The Agricultural Research Development Agency's research on food-grade recycled PET (rPET) aims to address the 834,500 tonnes of PET plastic produced annually in Thailand, focusing on developing recycling methods that comply with international food safety standards. These regulations align with ASEAN's circular economy framework, which facilitates regional plastic recycling innovations and waste management collaboration. The implementation of extended producer responsibility guidelines requires manufacturers to optimize packaging for recyclability while creating opportunities in the recycling industry. Packaging companies must also adhere to ISO 14001:2015 environmental management standards to remain competitive in domestic and international markets.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-use-plastic bans and eco taxes | -0.8% | Nationwide | Short term (≤ 2 years) |

| Volatile petrochemical resin prices | -0.6% | Nationwide | Short term (≤ 2 years) |

| Shortage of food-grade rPET feedstock | -0.4% | Nationwide | Medium term (2-4 years) |

| Low-cost import competition (VN and CN) | -0.5% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Single-Use-Plastic Restrictions Challenge Traditional Business Models

Municipal bans and an emerging extended-producer-responsibility regime force converters to upgrade to compostable, paper-based or multi-use designs, adding cost and complexity.[1]World Bank, “Thailand Trade | WITS Data,” worldbank.org Compliance varies by province, complicating planning. Small firms with limited R&D capacity struggle to meet rapid policy shifts, placing Thailand packaging market entrants at a scale disadvantage. Consumers continue to value convenience, creating tension between cost and eco performance.

Petrochemical Price Volatility Pressures Margin Sustainability

Thailand’s resin supply is closely tied to PTT’s refining and cracker economics; price spikes cascade quickly into film and bottle costs. Limited hedging among SMEs means margins compress during up-cycles. The nation still imports specialty resins, exposing the value chain to currency swings. Buyers push shorter contracts, elevating inventory risk for processors in Thailand packaging market.

Segment Analysis

By Material Type: Plastics Dominate While Paper Gains Momentum

Plastic held 41.73% of Thailand's packaging market share in 2024, anchored by domestic petrochemical integration. Yet single-use curbs and the National 3R Strategy are steering converters toward cartons and molded fiber. Paper and paperboard show the fastest 4.94% CAGR to 2030, supported by SCGP’s recycled-content lines and premium folding boxboard launches. Metal cans remain vital for beer and energy drinks, while container glass benefits from premium spirits positioning and ambitions to cut carbon through refill models.

The Thailand packaging market size for paper and paperboard is forecast to swell as e-grocers adopt curbside-recyclable boxes and cushioning. Converters experiment with aqueous coatings that rival plastics in moisture barrier yet remain repulpable. Bio-based polymers such as PLA also find niche adoption in foodservice. However, plastic grades with recycled content keep cost leadership, maintaining relevance in multilayer pouches and PET bottles that require high clarity and drop resistance.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Flexible and Rigid Plastics Split Growth Paths

Plastic products captured 44.23% of Thailand packaging market size in 2024, spanning PET bottles, HDPE closures, films and thermoforms. Rigid PET benefits from 61.5% share of bottled-water volumes; meanwhile, flexible plastic pouches win last-mile efficiency for sauces and detergents. Paper and paperboard products rise at a 4.56% CAGR on the back of e-commerce cartons. New barrier-coated paper cups replace polystyrene foam in quick-service restaurants, aligning with eco taxes.

Thailand packaging industry leaders co-develop returnable glass jars for premium condiments, tapping BG Container Glass’ capacity upgrades. Metal aerosols secure demand from hair-care and household insecticide brands seeking leak-proof formats. Overall, converters invest in multi-product portfolios to serve brand owner mandates for reduced unit weight and cradle-to-cradle recyclability.

By Packaging Format: Flexibles Extend Leadership

Flexible packs controlled 57.33% of Thailand's packaging market in 2024 and will grow at a 4.98% CAGR through 2030, propelled by laminate pouches, stand-up zippers, and courier mailers that cut freight costs. Their high surface-to-volume ratio supports vibrant graphics for online shelf impact, while downgauged films slash resin use. Rigid formats stay essential for carbonated drinks and pharmaceuticals demanding barrier integrity.

Producers incorporate mono-material PE or PP laminates that meet recycling-stream requirements without compromising seal performance. Active, humidity-absorbing sachets inside flexible bags extend snack freshness amid Thailand’s tropical climate. To curb leakage risk, e-commerce sellers adopt gusseted bags with laser-scored easy-tear openings, reinforcing the convenience edge.

By End-User Industry: Food Leads, Pharma Surges

Food applications commanded 29.45% of Thailand's packaging market share in 2024, bolstered by export-oriented canned tuna, rice, and fruit preparations. Sustainability-conscious importers push Thai packers toward FSC-certified paper labels and rPET thermoforms. Pharmaceuticals post a 4.67% CAGR thanks to expanded medical-device assembly and vaccine fill-finish lines that need sterile blister and vial packs.

Cosmetics and personal-care volumes rise on tourism arrivals, spawning sample-size sachets. Industrial lubricants retain steel drum usage, yet pilot composite IBCs for lighter export loads. Agriculture, driven by rice and durian exports, migrates to breathable woven PP sacks that preserve moisture balance. Collectively, these trends keep Thailand packaging market diversified across value chains.

Geography Analysis

Thailand packaging market growth centers in Greater Bangkok, home to large converting clusters and the main inland port. The Eastern Economic Corridor attracts 108 foreign investors as of April 2025, adding high-speed rail links that shorten container transit to Laem Chabang port.[2]Thai Government, “Official Statement ‘Together We Will Make It Through,’” thailand.prd.go.th Central provinces reap food-processing expansion, while Northern regions supply agro-commodities needing bulk sacks. Southern tourist hubs drive single-serve beverage and cosmetics packs for duty-free outlets.

Export-driven demand ties the sector to the United States, China and Japan, which together take 37% of Thai shipments, reinforcing global compliance needs. RCEP lowers tariffs but intensifies cost competition from Vietnam and China, where lower labor rates threaten commodity film producers. Domestic converters respond by automating lines under BOI tax incentives, boosting throughput and energy efficiency.

Single-use bans remain uneven; Bangkok tightens restrictions sooner than provincial towns, complicating nationwide SKU planning. Logistics infrastructure, including cold-chain warehouses, expands along the Eastern Seaboard to support seafood exports, stimulating insulated EPS alternative packs. Flood-prone areas in the Chao Phraya Basin prompt adoption of waterproof corrugated board, safeguarding shipped goods during monsoon season. These geographic nuances create micro-markets within Thailand packaging market, requiring adaptable supply strategies.

Competitive Landscape

Thailand packaging market displays moderate fragmentation. Top domestic players led by SCG Packaging and BG Container Glass combine for roughly 25% of total revenue, while numerous mid-tier converters serve niche substrates. SCGP’s THB 129,398 million (USD 3,669 million) revenue in 2023 includes fund acquisitions in Europe that widen its printing and bag-in-box expertise. BG Container Glass positions itself as a total-solutions supplier, adding flexible lines to complement bottles.

International entrants such as Crown Holdings expand beverage-can capacity to capture ASEAN consumption growth.[3]Crown Holdings, “Annual Report 2023,” sec.gov Resin majors PTTGC and SCG Chemicals introduce recycled and bio-polymer grades to hedge against virgin-resin volatility, offering converters turnkey materials that help meet Net-Zero commitments. Financiers like Kasikornbank channel ESG loans toward automation retrofits, easing capital constraints for SMEs.

Strategic moves center on boosting rPET supply. Indorama Ventures partners with Dhunseri and Varun Beverages to build 100 kt/year Indian recycling plants that secure feedstock pipelines for Southeast Asian bottlers. Meanwhile, NS-Siam United Steel invests THB 2 billion (USD 0.05 billion) to lift tinplate output 25%, anticipating higher food-can orders. Competitive advantage increasingly derives from ISO 14001-certified plants and in-house design studios capable of rapid artwork change-overs for e-commerce SKUs.

Thailand Packaging Industry Leaders

-

SCG Packaging Public Co. Ltd

-

BG Container Glass Public Co. Ltd

-

TPAC Packaging Public Co. Ltd

-

Thai Beverage Can Co. Ltd

-

TBPI Public Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Kasikornbank prioritizes ESG loans for packaging automation within corporate-lending portfolio.

- November 2024: SCG Chemicals rolls out SCGC Green Polymer, an eco-polymer family aligned with circular-economy targets.

- September 2024: Indorama Ventures sets up joint-venture rPET plants totaling 100 kt/year capacity to meet 30% recycled-content rules.

- July 2024: PTG Energy releases Sustainability Report 2023, outlining waste-to-power initiatives influencing lubricant-pack needs.

Thailand Packaging Market Report Scope

Packaging is the process of enclosing or containing a product in bottles, plastic bags, wrappers, paper cartons, boxes, etc. It serves the purpose of displaying useful information about the product, including its contents, weight, size, price, constituents, and necessary instructions for usage and storage. Packaging helps reduce the risk of wastage, spoilage, leakage, and evaporation during transportation and storage.

The Thai packaging market is segmented by packaging material (plastic, paper, paperboard, glass, and metal), packaging type (flexible packaging (pouches, bags, and packaging films), rigid packaging (bottles and jars, corrugated boxes and folding cartons, metal cans, drums, and bulk containers)), and end user (food, beverage, beauty and personal care, industrial, pharmaceutical, and other end users). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Material Type

| Paper and Paperboard | |

| Plastic | Polypropylene (PP) |

| HDPE and LDPE | |

| PET | |

| PVC | |

| PS | |

| Other Plastics | |

| Metal | |

| Container Glass |

By Product Type

| Paper and Paperboard Product | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | ||

| Single-use Paper Products | ||

| Other Paper and Paperboard Types | ||

| Plastic Product | Rigid Plastics | Bottles and Jars |

| Caps and Closures | ||

| Bulk-grade Products | ||

| Other Rigid Plastics | ||

| Flexible Plastics | Pouches | |

| Bags | ||

| Films and Wraps | ||

| Other Flexible Plastics | ||

| Metal Product | Cans | |

| Caps and Closures | ||

| Aerosol Containers | ||

| Other Metal Products | ||

| Container Glass Product | Bottles | |

| Jars | ||

By Packaging Format

| Rigid Packaging Format |

| Flexible Packaging Format |

By End-user Industry

| Food |

| Beverage |

| Pharmaceutical and Medical |

| Personal Care and Cosmetics |

| Industrial and Chemical |

| Agriculture |

| Automotive |

| Other End-user Industries |

| By Material Type | Paper and Paperboard | ||

| Plastic | Polypropylene (PP) | ||

| HDPE and LDPE | |||

| PET | |||

| PVC | |||

| PS | |||

| Other Plastics | |||

| Metal | |||

| Container Glass | |||

| By Product Type | Paper and Paperboard Product | Folding Carton and Rigid Boxes | |

| Corrugated Boxes and Containers | |||

| Single-use Paper Products | |||

| Other Paper and Paperboard Types | |||

| Plastic Product | Rigid Plastics | Bottles and Jars | |

| Caps and Closures | |||

| Bulk-grade Products | |||

| Other Rigid Plastics | |||

| Flexible Plastics | Pouches | ||

| Bags | |||

| Films and Wraps | |||

| Other Flexible Plastics | |||

| Metal Product | Cans | ||

| Caps and Closures | |||

| Aerosol Containers | |||

| Other Metal Products | |||

| Container Glass Product | Bottles | ||

| Jars | |||

| By Packaging Format | Rigid Packaging Format | ||

| Flexible Packaging Format | |||

| By End-user Industry | Food | ||

| Beverage | |||

| Pharmaceutical and Medical | |||

| Personal Care and Cosmetics | |||

| Industrial and Chemical | |||

| Agriculture | |||

| Automotive | |||

| Other End-user Industries | |||

Key Questions Answered in the Report

How large is the Thailand packaging market in 2025?

Thailand packaging market size is USD 15.71 billion in 2025 and is forecast to reach USD 19.54 billion by 2030 at a 4.46% CAGR.

Which packaging format is growing fastest in Thailand?

Flexible formats, already at 57.33% share in 2024, are advancing at a 4.98% CAGR through 2030 owing to e-commerce logistics and consumer convenience.

What materials are displacing traditional plastics?

Paper & paperboard, growing at 4.94% CAGR, plus rPET and bio-based polymers are gaining traction under National 3R Strategy mandates.

Which end-use sector leads demand?

Food applications account for 29.45% of overall demand, driven by Thailand’s ambition to rank among the top-10 processed-food exporters by 2027.

How are regulators shaping packaging design?

Single-use-plastic bans and extended-producer-responsibility rules compel converters to adopt recyclable structures and invest in certified environmental-management systems.

What opportunities exist for foreign investors?

BOI tax holidays and automation incentives in the Eastern Economic Corridor encourage investment in high-efficiency lines and rPET recycling infrastructure.

Page last updated on: