Thailand Oral Anti-Diabetic Drug Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

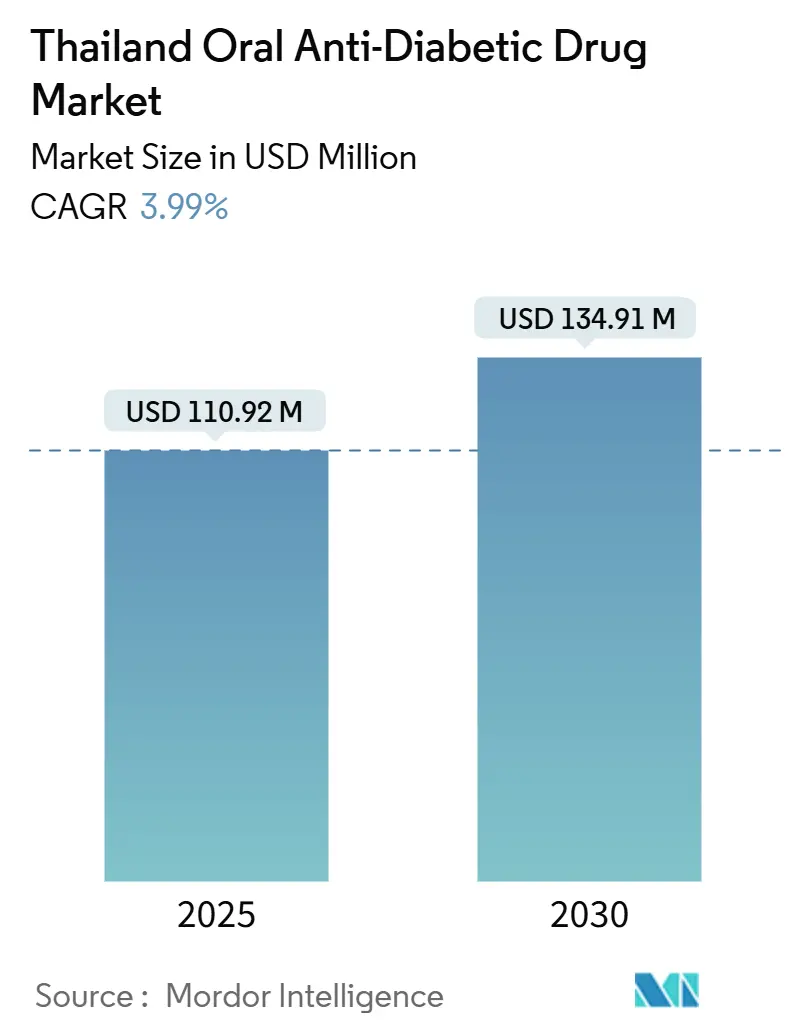

| Market Size (2025) | USD 110.92 Million |

| Market Size (2030) | USD 134.91 Million |

| Growth Rate (2025 - 2030) | 3.99% CAGR |

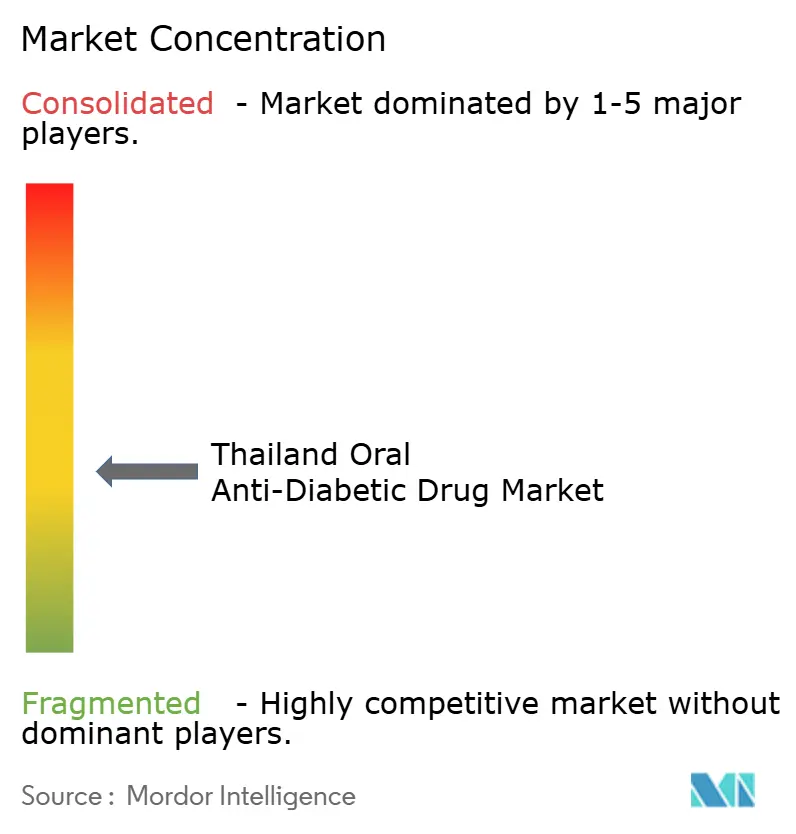

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thailand Oral Anti-Diabetic Drug Market Analysis by Mordor Intelligence

The Thailand oral anti-diabetic drug market reached USD 110.92 million in 2025 and is forecast to attain USD 134.91 million by 2030, advancing at a 3.99% CAGR. This steady expansion is supported by Thailand’s shift to value-based universal healthcare, its rapidly aging population, and the clinical preference for cardio-protective drug classes [1]National Health Security Office, “Universal Coverage Scheme: Treatment Anywhere Roll-Out,” nhso.go.th . Digital health infrastructure, medical tourism demand, and local contract manufacturing capabilities further enlarge the Thailand oral anti-diabetic drug market, while health-technology assessment (HTA)–led price caps temper premium pricing. Intensifying competition among global innovators and domestic generic makers encourages combination therapies, extended-release formulations, and real-world evidence generation to secure formulary positions. Online pharmacies and telemedicine platforms widen geographic reach, lifting adherence and enabling differentiated patient‐support programs that underpin revenue growth across therapeutic classes.

Key Report Takeaways

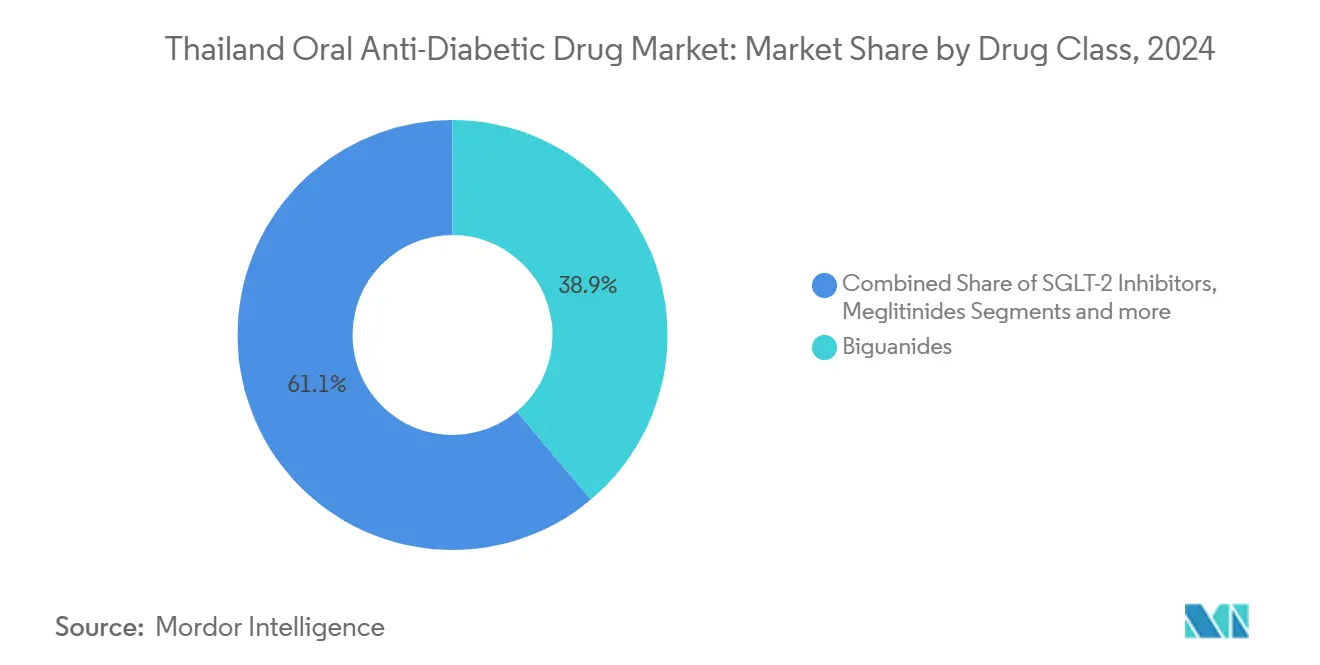

- By drug class, biguanides led with 38.88% of the Thailand oral anti-diabetic drug market share in 2024, whereas SGLT-2 inhibitors are projected to grow at 4.65% CAGR through 2030.

- By age group, adults accounted for 66.45% share of the Thailand oral anti-diabetic drug market size in 2024, while the geriatric cohort is expanding at a 4.67% CAGR to 2030.

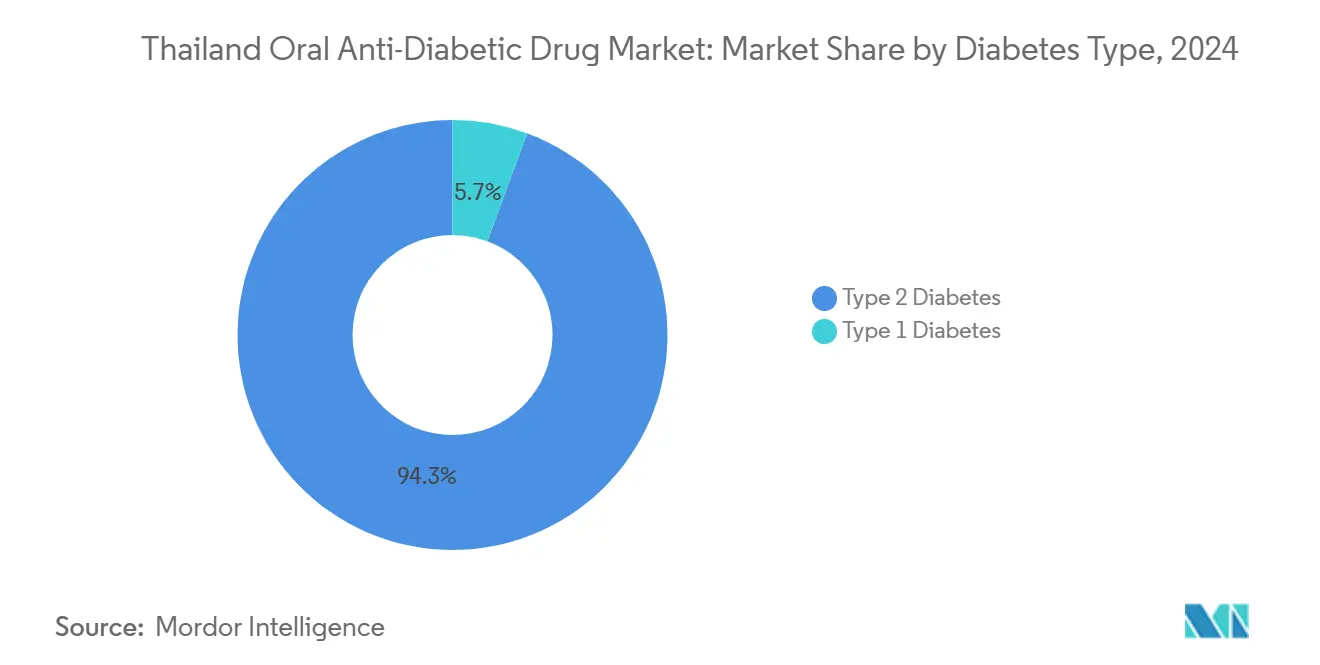

- By diabetes type, type 2 diabetes held 94.34% of the Thailand oral anti-diabetic drug market size in 2024 and posts the fastest 4.72% CAGR to 2030.

- By distribution channel, hospital pharmacies captured 68.39% of the Thailand oral anti-diabetic drug market share in 2024; online pharmacies record the highest 4.89% CAGR through 2030.

Thailand Oral Anti-Diabetic Drug Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging-Population Driven T2DM Prevalence Uptick | +1.2% | National, concentrated in urban centers | Long term (≥ 4 years) |

| Universal Coverage Scheme Drug Reimbursement Expansion | +0.8% | National, with enhanced rural access | Medium term (2-4 years) |

| Cardiovascular-Outcome Data Favouring SGLT-2 & GLP-1 Classes | +0.6% | National, physician-driven adoption | Medium term (2-4 years) |

| Rapid Retail-Pharmacy Channel Growth In Provincial Cities | +0.4% | Provincial cities, rural expansion | Short term (≤ 2 years) |

| E-Commerce Pharmacies & Tele-Consult Start-Ups For Chronic Care | +0.3% | Urban centers, expanding to rural | Short term (≤ 2 years) |

| Local Contract-Manufacturing Cost Advantage For Generics | +0.2% | National, export potential | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging-Population Driven T2DM Prevalence Uptick

Twenty percent of Thais are already over 60 years, and epidemiological surveys confirm that age beyond 50 correlates strongly with impaired fasting glucose and insulin resistance [2]Worawut Siriwattana, “Prevalence of Impaired Glucose Tolerance in Thai Older Adults,” SSRN, ssrn.com . Pharmaceutical firms therefore prioritize extended-release biguanides and lower-dose SGLT-2 inhibitor combinations that reduce pill burden while improving kidney and cardiovascular outcomes. Geriatric-focused dosing schedules lower hypoglycemia risk and are increasingly embedded in hospital formularies that serve Bangkok megahospital networks and emerging provincial centres.

Universal Coverage Scheme Drug Reimbursement Expansion

The 2024 pivot from “Treating All Diseases” to “Treatment Anywhere” connects 5,000 public health units through shared electronic records. Broader reimbursement for novel molecules narrows urban–rural treatment gaps, lifts physician willingness to prescribe SGLT-2 inhibitors, and underpins adherence programs delivered via tele-consults and remote monitoring. Pharmaceutical companies leverage this framework to negotiate outcomes-based agreements that reward real-world HbA1c improvements and hospitalization avoidance.

Cardiovascular-Outcome Data Favouring SGLT-2 & GLP-1 Classes

Thai hospital registries report a 41% reduction in major kidney events among SGLT-2 users relative to conventional therapy, reinforcing recent guideline revisions that position SGLT-2 inhibitors ahead of sulfonylureas for high-risk patients [3]Supattra Hunsuwan, "Real-world effectiveness and safety of sodium-glucose co-transporter 2 inhibitors in chronic kidney disease," Scientific Reports, nature.com. Cost-utility models show incremental lifetime gains of 0.42–0.52 years despite higher annual drug costs, a profile that resonates with HTA committees when weighed against dialysis avoidance.

Rapid Retail-Pharmacy Channel Growth in Provincial Cities

Investment incentives in the Eastern Economic Corridor catalyse chain-pharmacy build-outs that shorten travel times for chronic refills across Chonburi, Rayong, and Chachoengsao provinces. Cloud-linked dispensing systems allow pharmacists to verify e-prescriptions from tertiary centres, boosting medication pick-up rates and fuelling volume growth for the Thailand oral anti-diabetic drug market in formerly underserved districts.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| HTA-Driven Price Caps For Novel Molecules | -0.7% | National, affecting premium therapies | Medium term (2-4 years) |

| High Generic Penetration Squeezing Branded Margins | -0.5% | National, intensifying competition | Long term (≥ 4 years) |

| Persistently Low Medication-Adherence Rates Outside Bangkok | -0.4% | Provincial and rural areas | Medium term (2-4 years) |

| Rising Incidence Of Skin & Urogenital ADR-Related Recalls | -0.3% | National, class-specific impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

HTA-Driven Price Caps For Novel Molecules

Thai FDA appraisal panels demand robust cost-effectiveness dossiers before listing SGLT-2 or GLP-1 agents on the National Essential Medicines List. Ceiling prices agreed in 2025 slash launch premiums by as much as 30%, challenging innovators to bundle clinical-monitoring apps and nurse-led coaching to maintain value perception.

High Generic Penetration Squeezing Branded Margins

Generics constitute 30% of domestic production yet capture over 60% of metformin and sulfonylurea volumes, compressing incumbent margins. Innovators counter by pivoting to triple-fixed combinations and age-tailored oral dispersible tablets that extend lifecycle exclusivity.

Segment Analysis

By Drug Class: Cardiometabolic Benefits Propel SGLT-2 Uptake

Biguanides retained a 38.88% lead in 2024, underscoring metformin’s entrenched first-line status within the Thailand oral anti-diabetic drug market. SGLT-2 inhibitors, however, post a 4.65% CAGR to 2030 as cardiology societies endorse their reno-protective credentials. Utilization accelerates in urban tertiary hospitals where integrated cardio-metabolic clinics track eGFR decline and upgrade therapy proactively. Sulfonylureas decline amid hypoglycemia concerns, while DPP-4 inhibitors plateau as a tolerable but less cardio-centric option.

Clinical audit data show that SGLT-2 addition trimmed HbA1c by 1.1 percentage points and reduced annual hospitalization by 12% against a conventional biguanide-sulfonylurea backbone. These gains justify higher daily therapy costs and reinforce listing decisions across private insurer formularies. Consequently, the Thailand oral anti-diabetic drug market size for SGLT-2 therapies is forecast to climb from USD 27.6 million in 2025 to USD 34.6 million in 2030, while the class’s Thailand oral anti-diabetic drug market share edges up by 230 basis points.

Note: Segment shares of all individual segments available upon report purchase

By Age Group: Geriatric Care Pathways Take Center Stage

Adults generated 66.45% of 2024 revenues, yet the 60+ cohort expands fastest at 4.67% CAGR. Polypharmacy risk management guides prescribers toward once-daily fixed combinations that fuse metformin with SGLT-2 inhibitors or DPP-4 inhibitors, shrink pill burden, and mitigate renal strain.

Digital nutrition counseling offered through universal-coverage portals tailors meal plans for older adults, refining glycemic control and moderating weight. Consequently, the Thailand oral anti-diabetic drug market size attributable to geriatric users is expected to rise from USD 36.2 million in 2025 to USD 45.4 million in 2030. Pilot adherence programs in Chiang Mai and Khon Kaen achieve 15 percentage-point improvements, signalling considerable upside if replicated nationwide.

By Diabetes Type: Type 2 Dominance Shapes Therapy Mix

Type 2 diabetes accounted for 94.34% revenue share in 2024 and advances at 4.72% CAGR on the back of urbanisation, dietary westernisation, and sedentary lifestyles. Clinical diet surveys link daily soft-drink intake exceeding 500 ml with a 2.1-fold rise in progression to pharmacotherapy, prompting preventive education embedded in school curricula.

Thailand oral anti-diabetic drug industry innovators therefore design starter packs that bundle metformin XR with lifestyle-tracking apps, aiming to delay escalation to insulin. The Thailand oral anti-diabetic drug market size for type 2 therapies is projected at USD 128.1 million by 2030, while type 1 sales remain marginal yet stable, supported by paediatric specialty centres in Bangkok.

By Distribution Channel: Digital Convenience Redraws Supply Chains

Hospital pharmacies maintained 68.39% share in 2024, reflecting Thailand’s physician-led dispensing model. Nevertheless, online pharmacies accelerate at 4.89% CAGR, buoyed by NHSO-approved tele-consult services launched in January 2024. AI-enabled verification engines authenticate e-scripts, curbing counterfeit risks and winning regulator endorsement.

Rural households in Nakhon Phanom and Satun use drone delivery pilots that reduce refill times by 48 hours versus postal dispatch, lifting satisfaction scores. The Thailand oral anti-diabetic drug market size flowing through online channels is set to surpass USD 9 million in 2030, while hospital channels grow modestly as chronic-care pathways decant stable patients to community settings.

Geography Analysis

Bangkok’s contiguous provinces represent the highest per-capita consumption of premium SGLT-2 and GLP-1 therapies, underpinned by specialist endocrinology hubs and private insurer coverage. Yet the 2024 “Treatment Anywhere” policy is flattening historic access disparities by reimbursing oral anti-diabetics across 5,000 interconnected public facilities nationwide. Provincial pharmacy chains in the Eastern Economic Corridor post double-digit same-store sales growth as migrant industrial workers enrol in employer-funded screening programs.

The north and northeast exhibit elevated prevalence rates, with Kalasin Province surveys indicating poor glycaemic control in nearly 80% of diagnosed patients. Tele-endocrinology sessions streamed from Chiang Mai University Hospital cut follow-up appointment travel costs by USD 23 per visit, encouraging adherence. Community health volunteers equipped with point-of-care HbA1c devices capture village-level data that feed into NHSO dashboards, enabling targeted stock re-allocation to avert shortages.

Remote islands and highland districts still suffer under-screening. Drone-enabled medicine drop-offs trialled on Koh Chang demonstrate feasibility under monsoon conditions, with 100% on-time delivery during the 2024 pilot. As 5G towers proliferate, digital adherence nudges and refill reminders reach formerly offline seniors, broadening the Thailand oral anti-diabetic drug market beyond urban strongholds.

Competitive Landscape

The market remains moderately fragmented, balancing patented innovators with aggressive generic entrants. Multinationals such as AstraZeneca, Boehringer Ingelheim, and Novo Nordisk differentiate through cardio-renal evidence and clinician-education grants, whereas domestic manufacturers including the Government Pharmaceutical Organization and Siam Bioscience emphasize affordability and local supply security.

Strategic moves in 2024-2025 include AstraZeneca’s local fill-and-finish partnership for dapagliflozin, slicing logistics costs by 12% and meeting HTA affordability thresholds. Meanwhile, Siam Bioscience invested USD 42 million in a continuous-manufacturing line for metformin XR, expanding annual capacity by 90 million tablets and securing WHO pre-qualification.

Digital service bundling defines the new front line. Boehringer Ingelheim integrates its remote-coaching app with NHSO tele-consult modules, recording a 17% uplift in 90-day persistence rates. Takeda pilots blockchain-backed supply-chain tracing for its alogliptin franchise, assuring authenticity to e-pharmacy consumers and deflecting parallel-trade erosion. These converging trends reshape competitive moats from molecule patents to data ecosystems and patient-experience design.

Thailand Oral Anti-Diabetic Drug Industry Leaders

-

Astrazeneca

-

Astellas

-

Eli Lilly

-

Sanofi

-

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: LG Chem introduced Zemidapa (gemigliptin/dapagliflozin) dual therapy in Thailand, underscoring its global expansion strategy.

- May 2025: Mitsubishi Tanabe launched CANAGLU 100 mg SGLT-2 inhibitor nationwide.

- October 2024: Thailand mandated re-registration of legacy drug licences in ASEAN Common Technical Dossier format to modernize compliance.

Thailand Oral Anti-Diabetic Drug Market Report Scope

Orally administered antihyperglycemic drugs reduce blood glucose levels. They are often used in type 2 diabetes care. The Thailand Oral Anti-Diabetic Drug Market is segmented into drugs (Biguanides, Alpha-glucosidase inhibitors, Dopamine-D2 receptor agonists, Sodium-glucose Cotransport-2 (SGLT-2) inhibitor, Dipeptidyl Peptidase-4 (DPP-4) Inhibitors, Sulfonylureas, and Meglitinides). The report offers the market size in value terms in USD for all the abovementioned segments.

| Biguanides |

| Sulfonylureas |

| Meglitinides |

| Thiazolidinediones |

| Alpha-Glucosidase Inhibitors |

| DPP-4 Inhibitors |

| SGLT-2 Inhibitors |

| Others |

| Adults |

| Pediatric |

| Geriatric |

| Type 1 Diabetes |

| Type 2 Diabetes |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| By Drug Class | Biguanides |

| Sulfonylureas | |

| Meglitinides | |

| Thiazolidinediones | |

| Alpha-Glucosidase Inhibitors | |

| DPP-4 Inhibitors | |

| SGLT-2 Inhibitors | |

| Others | |

| By Age Group | Adults |

| Pediatric | |

| Geriatric | |

| By Diabetes Type | Type 1 Diabetes |

| Type 2 Diabetes | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies | |

| Online Pharmacies |

Key Questions Answered in the Report

What is the current size of the Thailand oral anti-diabetic drug market?

The Thailand oral anti-diabetic drug market size stands at USD 110.92 million in 2025 and is on track to reach USD 134.91 million by 2030.

Which drug class is growing fastest in Thailand?

SGLT-2 inhibitors post the fastest 4.65% CAGR owing to their proven cardiovascular and renal benefits.

How big is the geriatric opportunity?

Geriatric patients generate roughly one-third of 2025 revenue but advance at a 4.67% CAGR, reflecting Thailand’s rapid aging.

What role do online pharmacies play?

Online channels, boosted by NHSO telemedicine, grow at 4.89% CAGR and should surpass USD 9 million in sales by 2030.

How do HTA price caps affect new diabetes drugs?

HTA evaluations compress launch premiums by up to 30%, compelling innovators to justify value through outcome-based contracts and digital-care add-ons.

Which regions outside Bangkok show the most growth potential?

Provincial cities in the Eastern Economic Corridor and northern highlands drive incremental demand as pharmacy networks and tele-endocrinology services expand.

Page last updated on: