Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 2.72 Billion |

| Market Size (2031) | USD 3.74 Billion |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thailand Luxury Goods Market Analysis by Mordor Intelligence

The Thailand luxury goods market size stands at USD 2.72 billion in 2026 and is projected to reach USD 3.74 billion by 2031, reflecting a 6.6% CAGR as the nation consolidates its role as Southeast Asia’s premium‐consumption hub. Thailand's luxury goods market is buoyed by a steady recovery in inbound tourism, rising disposable incomes among Gen-Z, ongoing investments in flagship malls, and the introduction of a long-stay visa program. These factors are driving both traffic and spending, particularly in high-margin categories. While average transaction values face inflationary pressures, strategies like multi-brand retail curation, omnichannel shopping experiences, and influencer-led promotions are broadening the domestic market's reach. Expatriates and medical tourists are increasingly viewing investment-grade jewelry, Swiss watches, and bespoke accessories as portable stores of value. Although challenges like counterfeit proliferation, price sensitivity among the mass affluent, and a subdued demand from Chinese group tours temper volume growth, they haven't derailed the medium-term expansion of Thailand's luxury goods market.

Key Report Takeaways

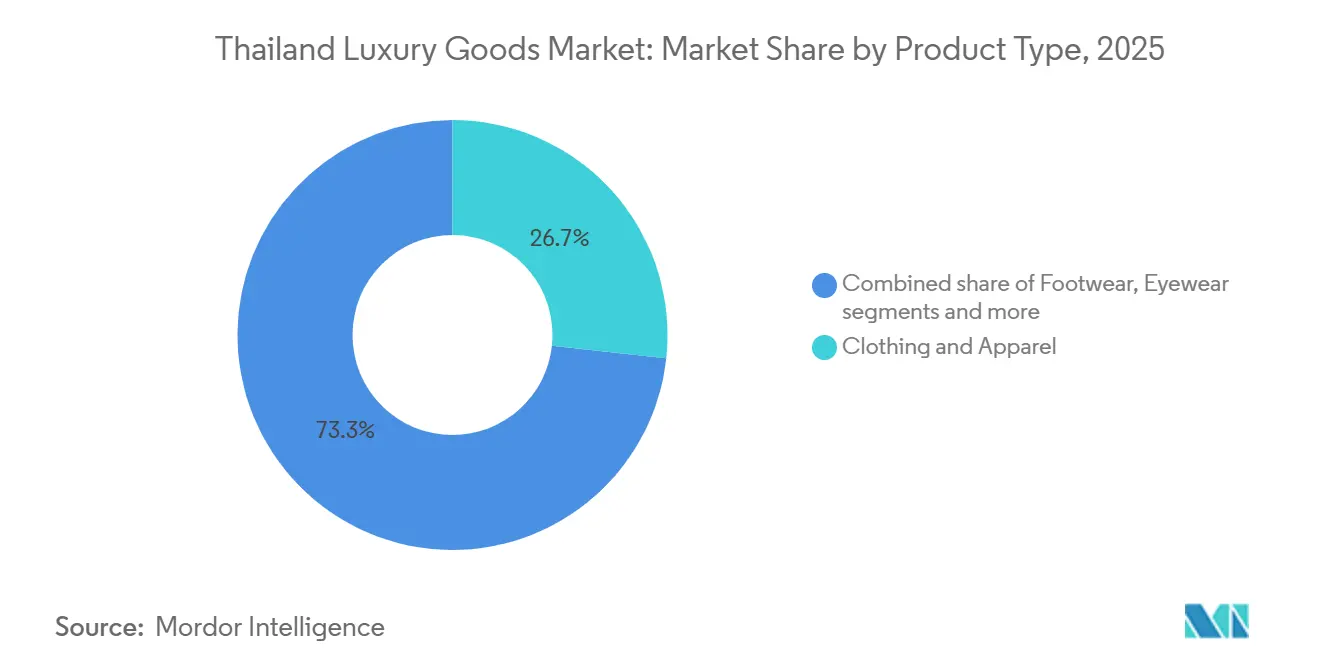

- By product type, clothing and apparel led with 26.73% of the Thailand luxury goods market share in 2025, while jewelry is projected to expand at a 6.96% CAGR through 2031.

- By end user, women generated 57.32% of 2025 revenue, whereas men represent the fastest-growing segment at a 7.32% CAGR to 2031.

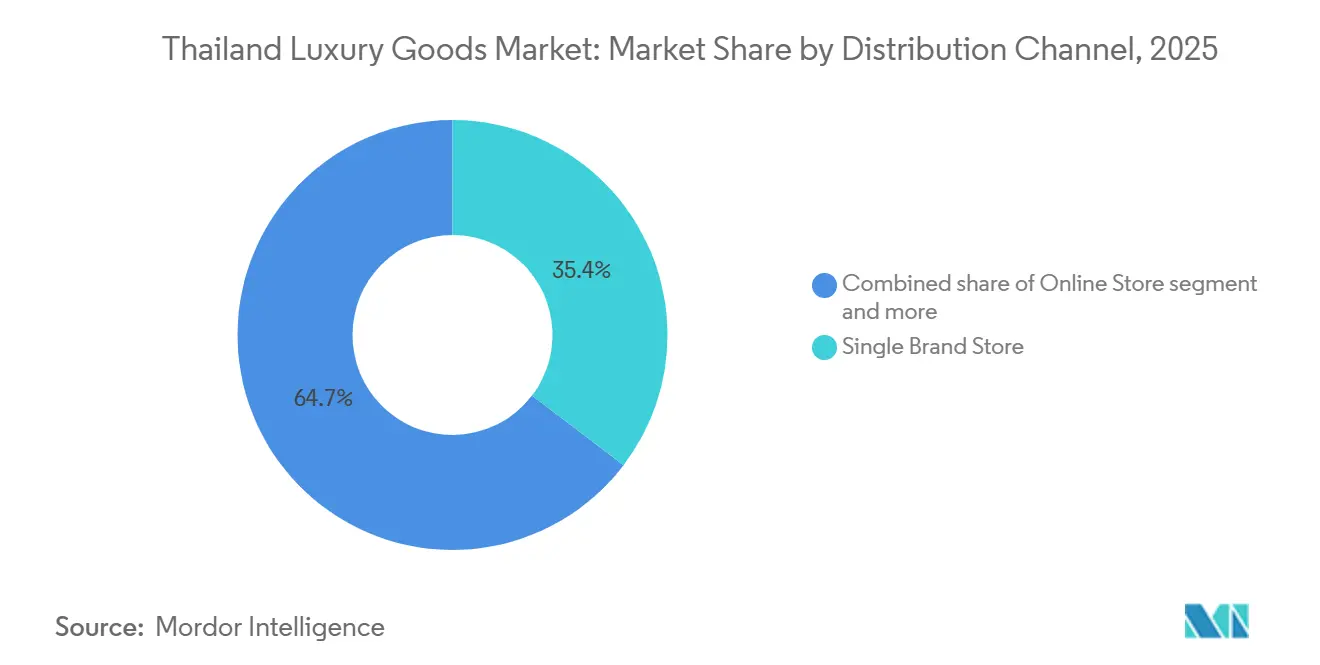

- By distribution channel, single-brand boutiques held 35.35% of 2025 sales, yet multi-brand stores are forecast to outpace with a 7.86% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Luxury Goods Market Trends and Insights

Drivers Impact Table

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising affluence among Gen-Z and young professionals | +1.2% | National, with concentration in Bangkok, Chiang Mai, Phuket | Medium term (2-4 years) |

| Inbound tourism rebound and flagship mall boom | +1.8% | National, with peak impact in Bangkok, Phuket, Pattaya, Chiang Mai | Short term (≤ 2 years) |

| Social-commerce and celebrity influence surge | +0.9% | National, with digital-native adoption in urban centers | Medium term (2-4 years) |

| Sustainability-led material innovation | +0.6% | Global, with early adoption in Bangkok luxury districts | Long term (≥ 4 years) |

| Visa-free long-stay programmes attracting HNW expats | +0.7% | National, with concentration in Bangkok, Phuket, Samui, Chiang Mai | Medium term (2-4 years) |

| Medical-tourism hubs driving Middle-East luxury spend | +0.5% | Bangkok, Phuket, Pattaya medical clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising affluence among gen-Z and young professionals

As of 2024, data from the Thailand Board of Investment reveals that individuals aged 15-24 constitute 12.24% of the nation's total population[1]Source: Thailand Board of Investment, "Thailand in Brief," boi.go.th. This demographic is reshaping consumption patterns, favoring experiential luxury and digital-first brand interactions over traditional status symbols. In response, brands are shifting focus from heritage narratives to highlight product utility, sustainability, and resale value qualities that resonate with a generation wary of overt displays of wealth. Demand for luxury goods among Thai men is surging at a 7.32% CAGR, fueled by young professionals who view watches, leather goods, and grooming products as markers of career success. According to the Bangkok Post, Gen-Z's discretionary spending on experiences rose to 56% in 2024, up from 45% in 2023. This trend underscores the need for luxury brands to weave in food and beverage, wellness, and cultural elements into their retail spaces. In a move highlighting this shift, Jim Thompson is channeling THB 100-150 million (USD 2.9-4.3 million) over the next 3-5 years to boost its store count from 25 to 30-35. This includes a prominent 500-square-meter duplex at One Bangkok and the introduction of a Maison Jim Thompson homeware line by 2026, signaling a strategic pivot towards lifestyle ecosystems to capture Gen-Z's loyalty.

Inbound tourism rebound and flagship mall boom

Thailand's luxury goods market is thriving, buoyed by a resurgence in tourism. The government, aiming high, targets 39 million international visitors and a foreign tourism revenue of 2.23 trillion baht by 2025, as highlighted by its public relations department in May 2025[2]Source: Thailand Public Relations Department, "Thailand targets High-Value Travelers for Long-Haul Tourism Growth," prd.go.th. The Tourism Authority of Thailand (TAT) Newsroom reports a significant milestone: over 35 million visitors graced Thailand in 2024, underscoring the nation's tourism revival[3]Source: Tourism Authority of Thailand Newsroom, "Thailand Welcomes Over 35 Million Visitors in 2024: A Milestone Paving the Way for 2025," tatnews.org. This resurgence has revitalized traffic at airport duty-free shops, resort boutiques, and urban flagship stores. Illustrating the trend, Central Group's THB 21 billion "The Central", King Power's "One Bangkok", and Prada's expansive 597-square-meter flagship in Central Phuket showcase the collaborative investments of developers and brands. They're keenly targeting a growing mix of tourists, predominantly from the Middle East, India, and independent travelers from China. Resort destinations are elevating their offerings, evident with bespoke services like Cartier's custom eyewear lounge, solidifying their premium market stance. Prime malls in Bangkok are witnessing double-digit rent growth, a testament to landlords' confidence in Thailand's luxury goods market. These strategic investments are not only drawing in tourists but also appealing to resident expatriates, fueling a surge in near-term sales.

Social-commerce and celebrity influence surge

In 2024, Thailand's social-commerce sector reached a valuation of USD 7.5 billion. Dominating the scene, TikTok Shop, Facebook Marketplace, and Instagram Shopping collectively represented 60% of the nation's online luxury sales. Celebrity-led live-stream auctions boasted conversion rates three times higher than traditional e-commerce, shrinking brand-awareness timelines from years to mere months. Luxury brands are now dedicating as much as 30% of their digital budgets to influencer collaborations. This strategy not only accelerates market entry for budding Thai designers but also hinges on the success of their viral product drops. Cafés like Ralph's Coffee have transformed into social-media hotspots, enhancing customer engagement and promoting cross-selling. This vibrant channel is reshaping distribution dynamics in Thailand's luxury goods market, all while pushing brands to safeguard their equity in an environment driven by fleeting trends.

Sustainability-led material innovation

Kering's Environmental Profit and Loss accounting and LVMH's Life 360 program are steering Thai leather and textile suppliers towards traceability and eco-friendly processes, emphasizing the importance of reducing environmental impact across the supply chain. Hermès's trial of mycelium-based alternatives hints at a significant shift in material sourcing, with the potential to redefine supply contracts and industry standards by 2027. Supporting this shift, government entities like the Designated Areas for Sustainable Tourism Administration (DASTA) are bolstering sustainable practices through policy initiatives, further sculpting Thailand's reputation as a conscientious luxury destination[4]Source: Designated Areas for Sustainable Tourism Administration, “DASTA promotes sustainable tourism at Thailand Tourism Forum 2025,” dasta.or.th. Local entities are capitalizing on Thailand's THB 50 billion Bio-Circular-Green incentives to bolster sustainable production, reduce dependency on imports, and safeguard against tariff and logistics disruptions, ensuring resilience in the face of global uncertainties. Jim Thompson's silk, dyed naturally using traditional methods, is being marketed as a heritage-rich, eco-friendly choice for luxury hotels, blending cultural authenticity with sustainability. Collectively, these moves are setting a new standard of sustainability in Thailand's luxury goods arena, aligning with global trends and consumer expectations for environmentally responsible practices.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit goods | -0.8% | National, with concentration in Bangkok, Pattaya tourist districts | Short term (≤ 2 years) |

| Price-sensitive mass affluent segment | -0.6% | National, with higher impact in secondary cities | Medium term (2-4 years) |

| Macroeconomic and inflation volatility | -0.5% | National, with spillover from global economic cycles | Short term (≤ 2 years) |

| Lagging return of Chinese group tours and FX swings | -0.7% | Bangkok, Phuket, Chiang Mai tourist hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit goods

In 2023-2024, authorities seized 4.2 million counterfeit luxury items in Thailand, valued at a staggering THB 12 billion. These fakes siphoned off 8-12% of the market's addressable demand, significantly undermining brand equity and consumer trust. Key vendors have established operations in prominent locations such as Chatuchak, MBK Center, and Patpong, leveraging Thailand's strategic logistics network to facilitate the import of counterfeit goods from China and Vietnam. While blockchain-based authentication solutions, like LVMH's Aura, provide a robust defense against counterfeits, they come at an added cost of USD 5-10 per item. This additional expense tightens profit margins, particularly for entry-level luxury products, making it challenging for brands to maintain competitive pricing. Customs officers, already stretched thin, inspect approximately 2 million parcels monthly, limiting their ability to curb the influx of counterfeit goods effectively. Consequently, counterfeiting continues to pose a significant challenge to Thailand's luxury goods market, emphasizing the critical need for scalable technological innovations and strengthened legal frameworks to address this persistent issue.

Lagging return of Chinese group tours and FX swings

In 2024, Chinese arrivals hit 6.7 million, marking a 40% dip from 2019 figures. This decline reflects the ongoing challenges in the recovery of international travel from China. Concurrently, a depreciation in the yuan led to a 15-18% drop in per-capita luxury spending, further impacting the overall market. While group tours have traditionally accounted for 60% of Chinese visitors, their muted presence has tilted the demographic towards independent travelers, who tend to spend less on duty-free items. This shift in traveler composition has altered spending patterns, requiring brands to adapt their strategies. Brands are now tasked with adjusting their assortments to cater to Middle Eastern and Southeast Asian tourists, given the distinct category preferences of these groups, which differ significantly from those of Chinese tourists. Furthermore, currency volatility has added a layer of complexity to pricing strategies. Absorbing foreign exchange (FX) losses might help maintain volume, but it comes at the cost of profitability, forcing brands to carefully balance pricing and margins. As organized Chinese travel continues its path to normalization, Thailand's luxury goods market grapples with a foundational yet restrained demand, highlighting the need for strategic agility in navigating these evolving dynamics.

Segment Analysis

By Product Type: Portable Assets Reshape Luxury Mix

In 2025, clothing and apparel dominated Thailand's luxury goods market, seizing 26.73% of total sales, driven by robust demand from both local consumers and tourists in pursuit of premium fashion. Leather goods, seen as aspirational entry points, trailed closely with about 22% of the category's value, thanks to the enduring allure of designer bags and accessories that convey status without exorbitant price tags. Meanwhile, luxury footwear and eyewear capitalized on the rising athleisure and wellness trends. Notably, sneaker resale volumes surged by 18% in 2024, as collectors eagerly pursued limited drops. Swiss mechanical watches, witnessing double-digit volume increases, emerged as coveted safe-haven investments amidst economic fluctuations. These segments, anchored by urban retail expansions and deepening e-commerce penetration in Bangkok and other tourist hotspots, collectively bolster the market's stability.

Jewelry emerged as the fastest-growing segment in Thailand's luxury market, boasting a 6.96% CAGR through 2031. Expatriates, medical tourists, and locals gravitated towards high-value pieces, viewing them as hedges against currency fluctuations, all while honoring a cultural affinity for gold. Duty-free operators sweetened the deal with gemstone-grading kiosks and private viewing lounges, enhancing accessibility at key airports and resorts. Beauty and personal care mirrored this growth with a steady 6.2% rise, driven by K-beauty trends and targeted omnichannel strategies from giants like Estée Lauder and L’Oréal, focusing on younger audiences. Brands capitalized on scarcity, rolling out limited-edition sneaker collaborations and custom eyewear. Apparel, facing slowdowns, pivoted to upcycled fabrics, appealing to eco-conscious shoppers. Watches, bolstered by events like Bangkok Watch Week, reinforced their investment status, underscoring Thailand's burgeoning prominence as a luxury horology hub in the region.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Male Demand Narrows the Gender Gap

In 2025, women commanded a dominant 57.32% share of Thailand's luxury goods market, driven by a robust appetite for high-end beauty, fashion, and accessories. This demand is deeply rooted in cultural gifting traditions and amplified by social media. High-net-worth women are gravitating towards ultra-premium handbags and exquisite jewelry. In contrast, the mass-affluent demographic leans towards accessible beauty products and small leather goods. This trend is further buoyed by omnichannel expansions from luxury giants like Dior and Chanel. To cement loyalty and enhance lifestyle appeal, these brands are curating in-store experiences, integrating wellness events, and cultural activations. With the backing of e-commerce growth and influencer partnerships, especially on platforms like Instagram and TikTok, female buyers remain the bedrock of market volumes. Their steadfast presence bolsters the market's resilience, even as tourism rebounds and disposable incomes rise.

Men are emerging as the fastest-growing demographic in Thailand's luxury goods arena, boasting a 7.32% CAGR projected through 2031. Executives are increasingly viewing luxury accessories as essential career assets, while younger professionals are leaning into self-expression. Men's grooming is gaining traction, bolstered by department-store shop-in-shops and TikTok tutorials. Meanwhile, bespoke suits, niche fragrances, and minimalist jewelry have seen their unisex share rise to 15%, up from 11% in 2023. Boutiques are introducing male-focused lounges, offering private fittings to encourage repeat visits. Merchandising is adapting, with a shift towards larger footwear sizes and darker color palettes. Unisex sneaker collaborations are further blurring gender lines, generating a buzz in social commerce and driving double-digit growth in select categories. In response, retailers are onboarding specialized stylists, positioning men to steadily increase their market share as societal perceptions evolve.

By Distribution Channel: Curation Beats Control

In 2025, single-brand boutiques dominated Thailand's luxury goods market, accounting for 35.35% of the revenue. These boutiques, located in prime Bangkok districts, offer exclusive experiences like VIP lounges and customization services, fostering deep brand loyalty among affluent shoppers. They differentiate themselves from aggregated retail formats through immersive storytelling, art installations, and private events. High-net-worth locals and tourists are drawn to the intimacy and prestige of standalone outlets. For instance, Louis Vuitton’s ‘LV The Place Bangkok’ seamlessly blends shopping with dining and exhibitions. As rent pressures mount in key corridors, brands are increasingly turning to shorter-term pop-ups. This strategy allows them to gauge demand before committing to flagship stores, ensuring flexibility in response to evolving consumer paths. The dominance of this channel endures, primarily due to its ability to curate premium atmospheres that remain elusive in multi-brand environments.

Department stores and duty-free complexes are emerging as the fastest-growing distribution channels in Thailand's luxury market. They're projected to expand at a 7.86% CAGR through 2031. This growth is driven by a shift in footfall towards these venues, seen as one-stop discovery hubs for time-poor shoppers. Multi-brand operators, leveraging data analytics and co-marketing funds, now aggregate over 550 labels. This strategy simplifies access for shoppers and boosts inventory turnover, especially in high-traffic locations like Central Park Bangkok and One Bangkok. Meanwhile, duty-free restructuring is channeling investments into urban and airport hotspots. This move capitalizes on surges in tourism and the allure of tax exemptions for luxury categories. Additionally, curated concept stores within these duty-free spaces are providing emerging Thai designers with accelerated exposure, all without the burden of heavy capital investments. The interplay between these channels not only ensures a broad market reach but also maintains a boutique-like personalization, fueling the overall expansion of the market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2025, Bangkok's 200-plus luxury boutiques, spanning Central Embassy, Siam Paragon, and ICONSIAM, accounted for 55% of the city's sales. By late 2026, the upcoming Central will add another 1.1 million m² of mixed-use space, including retail, dining, and entertainment options, further enhancing the city's appeal as a luxury shopping destination. The city enjoys a boost from Suvarnabhumi airport's 60 million annual passengers, which ensures a steady influx of international visitors, and the Long-Term Resident visa, which channels expatriate spending towards high-end retail. Landlords, seizing the momentum in Thailand's luxury goods market, have hiked prime rents by 8-12%, solidifying downtown's status as the nation's luxury epicenter and attracting global brands seeking premium retail spaces.

Phuket, with 18% of the national sales, is projected to grow at an annual rate of 8.2% until 2031. This growth is fueled by resort tourism, yacht chartering, and medical procedures, all seamlessly blending with luxury shopping. Central Phuket's recent renovation introduced Prada's largest store in Thailand and Tiffany & Co.'s first resort boutique, highlighting brands' growing interest in leisure-centric formats. The island's appeal is further enhanced by its reputation as a high-end destination, offering exclusive experiences such as private yacht tours and luxury wellness retreats. Duty-free shops and watch specialists are enhancing their offerings, integrating tax-refund desks and private-viewing apartments to attract Middle Eastern and European patients seeking luxury during their recovery, thereby creating a unique shopping experience tailored to affluent international visitors.

Pattaya and Chiang Mai, holding a combined 15% of the market, are expanding their presence. Real estate upgrades are boosting average room rates, drawing in more affluent travelers. Pattaya is leveraging its coastal location to attract luxury travelers through upscale resorts and beachfront developments. Chiang Mai is weaving its heritage into silk workshops and wellness retreats, turning artisanal experiences into boutique spending opportunities. The city is also positioning itself as a cultural hub, offering curated experiences that appeal to high-net-worth individuals seeking authenticity. While secondary cities like Udon Thani and Khon Kaen currently account for only single-digit shares, the introduction of high-speed rail by 2028 is poised to invigorate the northeastern corridors, increasing foot traffic in Thailand's luxury market. Retailers are eyeing pop-up rotations in these emerging nodes, viewing them as a strategic, capital-light move for a first-mover advantage, while also testing the market potential in these regions before committing to permanent establishments.

Competitive Landscape

Thailand's luxury goods market exhibits moderate fragmentation, with LVMH, Kering, and Richemont dominating, collectively accounting for the majority of sales, while local heritage and niche designers capture the remainder. LVMH bolsters its position with experiential ventures like Dior’s “Gold House,” a luxury concept space designed to enhance customer engagement, and a resort-centric expansion in Phuket, which caters to high-net-worth tourists. Kering, aiming at Gen-Z, integrates augmented-reality try-ons and mobile-styling apps in Gucci and Saint Laurent to provide an interactive shopping experience, while Bottega Veneta appeals to expatriates with its emphasis on understated craftsmanship and timeless designs. Richemont taps into Thailand’s horology culture, unveiling Cartier’s bespoke eyewear lounge to attract affluent clientele and hosting exclusive collector events at Siam Paragon to strengthen brand loyalty.

Central Group broadens its horizons with a stake in Selfridges, using this leverage to introduce Central Park as a first-in-Thailand offering, thereby enhancing its global footprint. King Power, in collaboration with Avolta, harnesses international loyalty data to tailor offers across 18 nations, enhancing its network effects and creating a seamless shopping experience for international travelers. Thai brands like Jim Thompson, Sretsis, and Disaya harness the power of social commerce to break beyond domestic confines, championing sustainability and bold design as their unique selling propositions to appeal to a global audience.

In this competitive landscape, where mere products no longer guarantee market share, tools like blockchain authentication, VIP salons, and cross-border loyalty engines have become essential assets in Thailand's luxury goods arena. These innovations not only enhance customer trust and exclusivity but also provide brands with a competitive edge in a rapidly evolving market. By adopting these advanced strategies, luxury brands in Thailand are redefining customer experiences and setting new benchmarks for the industry.

Thailand Luxury Goods Industry Leaders

-

LVMH Moët Hennessy Louis Vuitton SE

-

Kering SA

-

Chanel SA

-

Hermès International SA

-

Prada SpA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: EMSPHERE luxury shopping center opened in Bangkok’s Sukhumvit district, bringing flagship stores from Gucci, Louis Vuitton, and Prada under one roof with integrated entertainment venues and mass-transit links.

- August 2024: Cortina Watch Thailand launched the luxury watch shopping experience by seamlessly integrating digital and in-store services. Customers can now explore the refreshed in-store collections online, verify stock availability at nearby boutiques, and place orders for in-store pickup. Furthermore, they can schedule personalized consultations with watch specialists through a convenient contact form.

- August 2024: Prada opened its largest Thai boutique at Central Phuket, spanning 597 m2. The store features a distinctive design with curved glass panels and triangular patterns that offer panoramic views of the interior space, where the latest collections are displayed.

- March 2024: Louis Vuitton launched ‘LV The Place Bangkok’, a 360-degree concept combining retail, dining, and exhibitions at Gaysorn Amarin.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Thailand's luxury goods market as sales of premium-priced personal items, such as fashion, leatherware, watches, jewelry, eyewear, and prestige beauty, sold domestically to residents or visitors and captured at final retail value.

Scope excludes premium automobiles, fine wines and spirits, luxury real estate, and experiential products such as five-star hotels.

Segmentation Overview

-

By Product Type

- Clothing and Apparel

- Footwear

- Eyewear

- Leather Goods

- Jewelry

- Watches

- Beauty and Personal care

-

End User

- Men

- Women

- Unisex

-

Distrubution Channel

- Single Brand Stores

- Multi Brand Stores

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed Bangkok concession managers, duty-free operators in Phuket, regional brand executives, and affluent millennial shoppers. These conversations clarified real sell-out growth, online share, and average basket size, filling gaps that secondary data could not address.

Desk Research

We began with open statistics from the Bank of Thailand, Customs Department import codes for HS 42, 61-64, and 71, Tourism Authority visitor-spend dashboards, and Thai Retailers Association trend notes. Company filings accessed via D&B Hoovers, store counts in Dow Jones Factiva, and economic tables from the World Bank helped us benchmark channel footprints and average prices. Questel patent alerts and trade-press coverage of flagship store openings supplied product-cycle clues and seasonality markers. The sources listed illustrate our approach; many further references supported data collection and validation.

Market-Sizing & Forecasting

A top-down build reconciled import values, tourist receipts, and re-export leakage to estimate domestic retail sales, followed by selective bottom-up checks of flagship revenues and sampled ASP × unit volumes to fine-tune totals. Key inputs include inbound tourist arrivals, per-capita disposable income, luxury floor-space additions, brand price inflation, social-commerce penetration, and gray-market dilution rates. We fitted a multivariate regression to historic sales and applied an ARIMA overlay for 2025-2030 projections, stress-testing assumptions through scenario workshops with interviewees. Where store counts were missing, rolling three-year averages from comparable brands bridged the data gap.

Data Validation & Update Cycle

Model outputs undergo variance checks against VAT refund tallies and duty-free receipts before a senior analyst signs off. Our report refreshes annually, with interim updates triggered by material events, ensuring clients receive the latest vetted view.

Why Our Thailand Luxury Goods Baseline Commands Reliability

Published estimates often diverge because each firm selects its own scope, pricing filters, and update rhythm.

By anchoring on verified border trade, tourist spend, and live store metrics, Mordor's disciplined model delivers a balanced midpoint between optimistic channel revenues and narrow fashion-only counts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.63 B (2025) | Mordor Intelligence | - |

| USD 3.20 B (2024) | Regional Consultancy A | Includes automobiles and fine foods; relies on wholesale invoices, limited primary checks |

| USD 3.40 B (2024) | Trade Journal B | Uses online consumer panels without duty-free adjustment |

| USD 8.00 B (2024) | Industry Association C | Bundles jewelry retail and luxury housing; no allowance for counterfeit share |

The comparison shows that our transparent scope, variable selection, and yearly refresh make Mordor's baseline the dependable choice for decision-makers seeking traceable, repeatable numbers.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Thailand luxury goods market?

The Thailand luxury goods market size reached USD 2.72 billion in 2026 and is expected to hit USD 3.74 billion by 2031.

Which product category is growing the fastest in Thai luxury retail?

Jewelry leads with a 6.96% CAGR through 2031 as high-net-worth expatriates and medical tourists favor portable investment pieces.

Why are multi-brand stores gaining share over single-brand boutiques?

Curated assortments, lower search costs, and experiential anchors in projects like Central Park are driving a 7.86% CAGR for multi-brand formats.

What factors constrain near-term growth prospects?

Counterfeit proliferation and a slower rebound of Chinese group tours curb volume, offsetting some gains from tourism and Gen-Z affluence.