Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

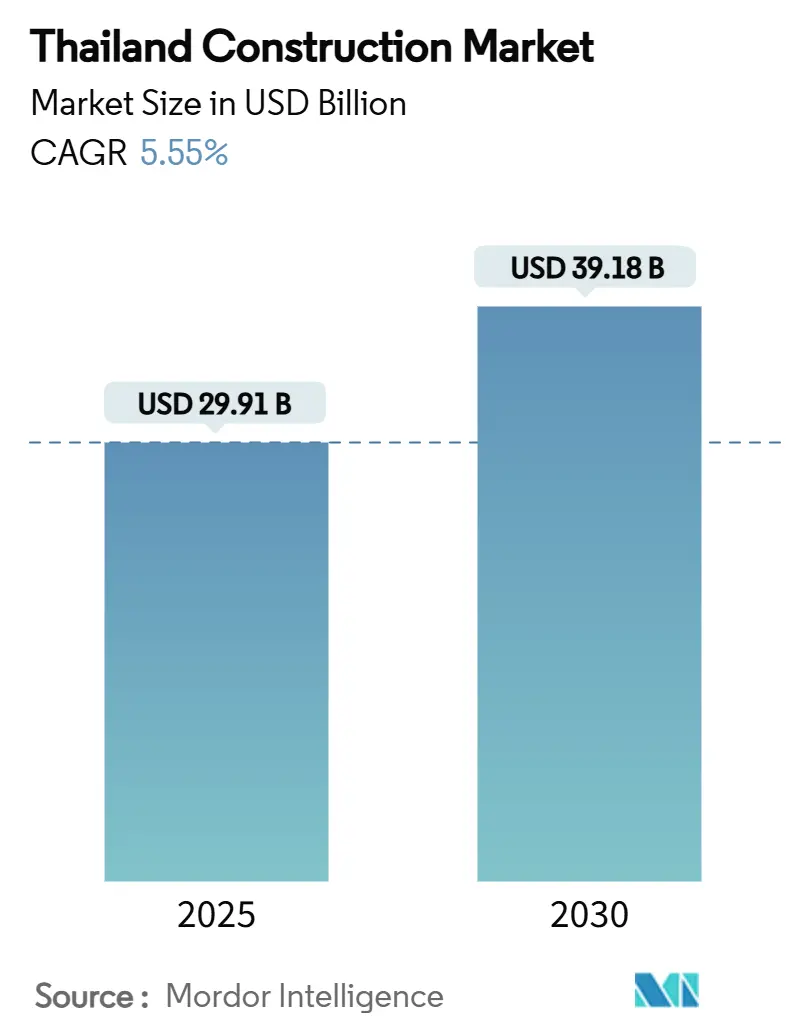

| Market Size (2025) | USD 29.91 Billion |

| Market Size (2030) | USD 39.18 Billion |

| Growth Rate (2025 - 2030) | 5.55% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thailand Construction Market Analysis by Mordor Intelligence

The Thailand Construction Market size is estimated at USD 29.91 billion in 2025, and is expected to reach USD 39.18 billion by 2030, at a CAGR of 5.55% during the forecast period (2025-2030). Underpinning this expansion is the government’s USD 75.7 billion nationwide transport upgrade, the USD 14.1 billion Land Bridge corridor, and a wave of private mixed-use schemes that anchor Bangkok and secondary cities as regional logistics and tourism hubs. Large projects such as the USD 9.6 billion Thai-China high-speed rail second phase, the USD 430 million U-Tapao second runway, and the USD 3.9 billion 2025 infrastructure package keep orderbooks full for established contractors while signalling reliable cashflow visibility to suppliers. At the same time, renovation, digital design tools, and low-carbon materials reshape project economics, giving investors fresh opportunities to extract value from Thailand’s ageing building stock. Supply-side obstacles—tight skilled labour, condo oversupply and cost inflation—temper near-term momentum but also accelerate adoption of prefabrication and sustainable construction solutions, setting the Thailand construction market on a structurally stronger footing through 2030[1]Ministry of Transport, “2025–2026 Infrastructure Investment Plan,” Ministry of Transport, mot.go.th.

Key Report Takeaways

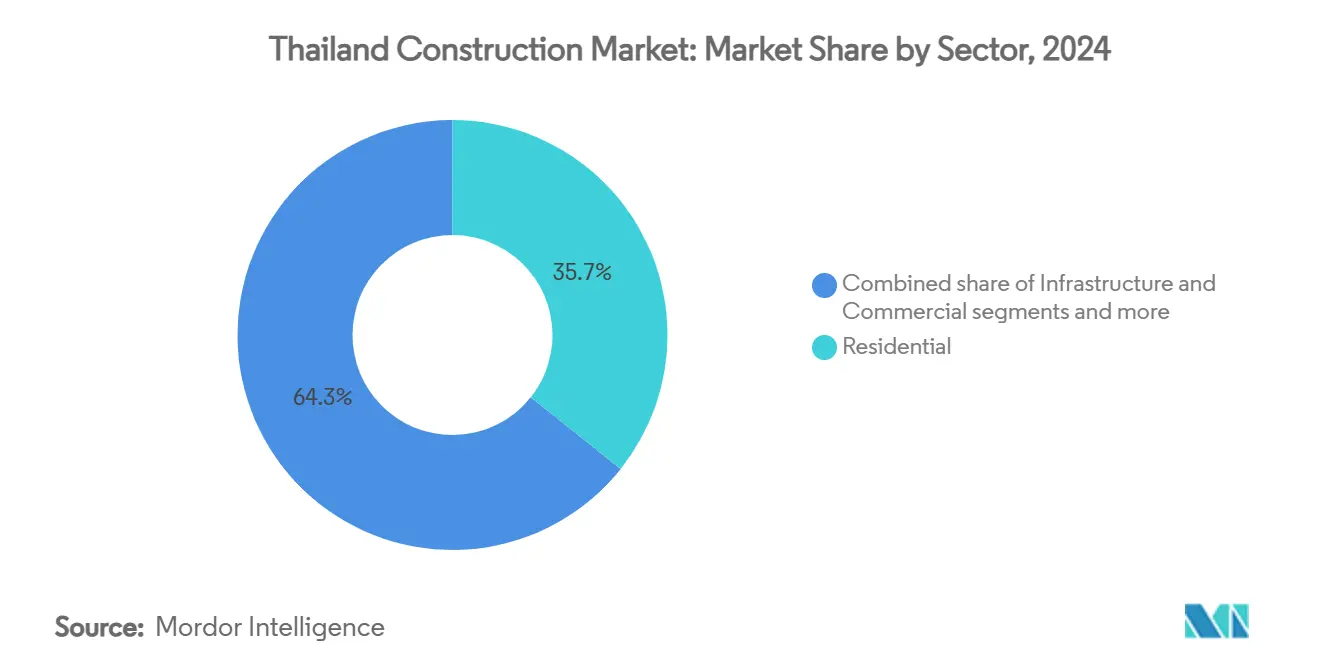

- By sector, residential led with 35.7% of Thailand construction market share in 2024, while infrastructure is advancing at a 6.03% CAGR to 2030.

- By construction type, new construction accounted for 74.1% of Thailand construction market size in 2024; renovation is projected to expand at 6.17% CAGR between 2025-2030.

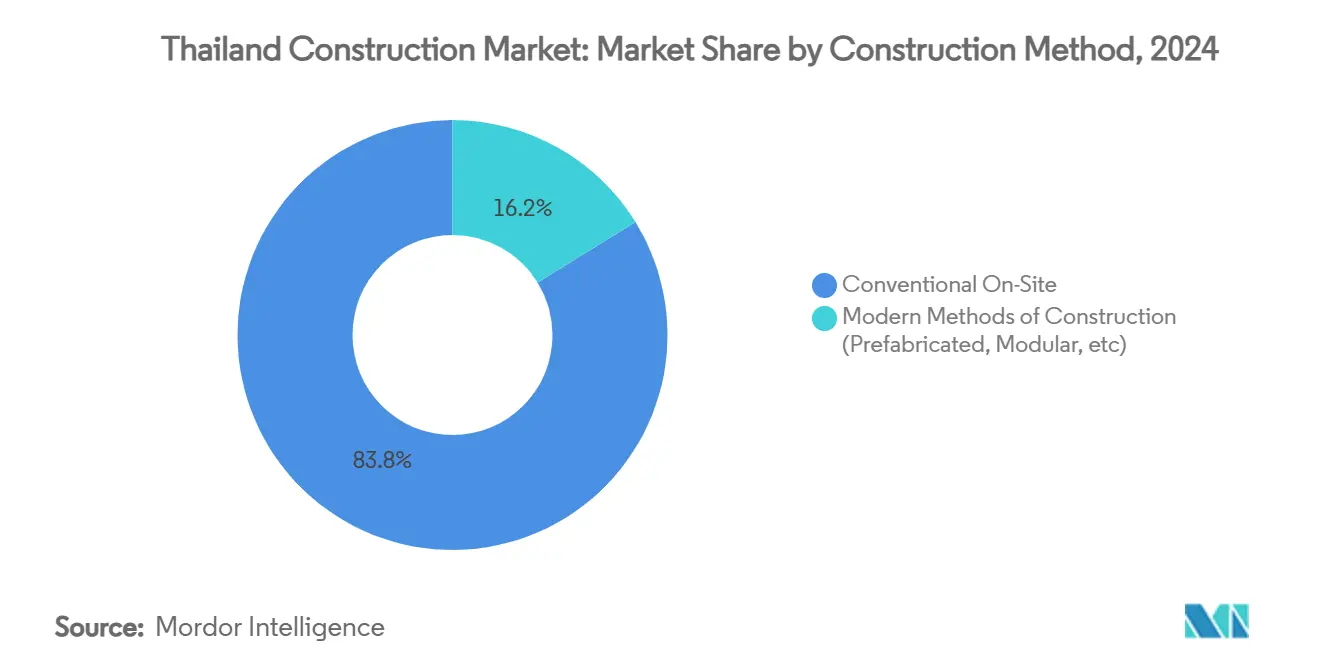

- By construction method, conventional on-site techniques commanded 83.8% share of Thailand construction market size in 2024, yet modern methods are forecast to grow 6.30% per year.

- By investment source, the private segment held 60.2% of Thailand construction market share in 2024 and is growing at a 6.41% CAGR.

- By city, Bangkok contributed 41.6% of Thailand construction market activity in 2024, whereas Chiang Mai registers the fastest 6.65% CAGR to 2030.

Thailand Construction Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Major infrastructure rollouts (rail, airports, mass transit) | +1.2% | Nationwide, focus on EEC & Bangkok | Long term (≥ 4 years) |

| Public–private partnership push in highways, bridges & ports | +0.8% | Nationwide, early gains in EEC | Medium term (2-4 years) |

| Mixed-use & transit-oriented developments | +0.6% | Bangkok, Phuket, Pattaya, Chiang Mai | Medium term (2-4 years) |

| Renewable power and grid expansion | +0.5% | Northeast & South | Long term (≥ 4 years) |

| Urban residential demand in Bangkok & secondary cities | +0.4% | BMA, Chiang Mai, Phuket | Short term (≤ 2 years) |

| Digital construction tools adoption | +0.3% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Major infrastructure rollouts drive nationwide construction surge

A record USD 3.9 billion budget covering 223 projects in 2025 anchors public spending, with rail, road and aviation schemes dominating award pipelines. The USD 9.6 billion Thai-China high-speed rail link and the USD 430 million U-Tapao runway illustrate the revenue visibility such mega-projects create for tier-one contractors while cementing Thailand’s role as an ASEAN logistics node. Long delivery schedules stretching beyond 2030 assure multi-year demand for civil works, signalling permanence in the Thailand construction market.

Public–private partnerships accelerate project delivery

A maturing PPP law has unlocked USD 30.8 billion in planned investment and already approved USD 13.3 billion of priority schemes. Laem Chabang Port Phase 3 combines 47% public and 53% private capital to lift annual container handling to 18 million TEU, showcasing risk-sharing structures that attract technology-rich foreign operators and ensure timetable discipline. This framework injects predictable cash flows into the Thailand construction market while sparing the public balance sheet[2]Government Public Relations Department, “Laem Chabang Port Phase 3 PPP Framework,” Government Public Relations Department, thailand.prd.go.th.

Mixed-use developments transform urban landscapes

Developers are rolling out fully integrated retail-office-residential clusters that answer consumer demand for convenience and higher land productivity. Central Pattana’s USD 424 million programme across 2024-2026 and the USD 127 million Central Krabi site typify projects that spread beyond Bangkok into tourism corridors. Such schemes diversify revenue streams for builders, encourage transit-oriented planning and elevate design standards, thereby enriching the Thailand construction market.

Renewable energy construction expands grid infrastructure

The national goal of 50% renewable generation by 2037 underwrites continual demand for solar farms, wind arrays and battery storage. The Asian Development Bank’s USD 820 million loan covering 12 projects exemplifies the scale of capital flowing into clean-energy civil works. Grid extensions in rural northeast and southern provinces require sophisticated engineering, broadening opportunities for specialised EPC firms within the Thailand construction market.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled labor shortages and rising wages driving up costs and extending schedules | -0.9% | National, most acute in Bangkok and EEC regions | Short term (≤ 2 years) |

| Weak apartment sales in Bangkok causing cancellations and slower launches | -0.7% | Bangkok Metropolitan Area, with spillover to secondary cities | Medium term (2-4 years) |

| Land acquisition and environmental reviews delaying permission processes | -0.5% | National, particularly affecting infrastructure and industrial projects | Medium term (2-4 years) |

| Rising global material prices and logistics challenges squeezing contractor margins | -0.4% | National, with higher impact on import-dependent projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled labour shortages constrain project execution

Tight domestic talent pools and rising wages have pushed contractors to source foreign workers, yet permit approvals still lag demand, stretching schedules and eroding margins. Larger firms mitigate the crunch through in-house training and mechanisation, while smaller builders struggle to meet timetable guarantees, dampening the Thailand construction market’s near-term pace.

Bangkok apartment oversupply dampens residential construction

An inventory of 235,000 unsold condominiums forces developers to curb new launches, shifting focus from high-rise towers to landed housing formats. Earthquake-related safety concerns and elevated household debt cap new mortgage uptake, prolonging absorption cycles and muting residential starts inside the core Bangkok market.

Segment Analysis

By Sector: Infrastructure Leads Growth Despite Residential Dominance

The residential segment captured 35.7% of Thailand's construction market share in 2024, fuelled by urban population gains and lifestyle shifts. Yet infrastructure is the outright growth engine, forecast at 6.03% CAGR through 2030 as Thailand chases regional logistics leadership. Passenger rail corridors, airport runways, and expressways dominate award lists, reflecting a clear policy pivot toward connectivity. Illustrative is the Thai-China high-speed rail second phase, budgeted at USD 9.6 billion, and the three-airport high-speed link that ties Don Mueang, Suvarnabhumi, and U-Tapao for tourism flows. These corridors promise long-term revenue to civil contractors and unlock new catchment areas for property developers.

Commercial construction rebounds on tourism and mixed-use initiatives. Central Pattana’s USD 424 million multi-city programme underlines retail-hospitality resurgence, while emerging co-working and life-science labs diversify demand. Industrial facilities tied to the Eastern Economic Corridor benefit from electronics, automotive, and advanced biotech tenants, reinforcing infrastructure-induced spill-overs inside the Thailand construction market.

Infrastructure’s momentum rests on guaranteed public funding and the PPP pipeline that has already approved USD 13.3 billion of port, highway and rail packages. Renewable power plants and grid upgrades complement transport schemes, broadening contractor scopes and smoothing cyclicality. Consequently, infrastructure’s rising slice of Thailand construction market size is poised to outstrip residential by the decade’s close.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Construction Type: Renovation Gains Momentum Amid New Construction Dominance

New construction accounted for 74.1% of Thailand's construction market size in 2024, mirroring the country’s continuing build-out of transport links and greenfield real estate. Landmark examples include the USD 14.1 billion first phase of the Land Bridge and the USD 429 million second runway at U-Tapao International Airport. Greenfield projects create immediate bulk demand for structural steel, cement, and heavy equipment, locking in volume for material suppliers.

Renovation, although smaller, is the fastest-growing slice at a 6.17% CAGR to 2030. Bangkok’s ageing office towers, 1990s-era condominiums, and provincial hotels are moving into their first major refurbishment cycle. Corporate ESG targets and higher utility tariffs spur energy-efficiency retrofits that rely on insulated façades, LED upgrades, and smart-building controls. SCG’s 63% share of low-carbon cement output positions the company to capitalise on this wave, giving renovation a strategic environmental overlay within the Thailand construction market.

Property owners value renovation for speed to market and lower regulatory hurdles, especially in dense central locations where land is scarce. As renovation share rises, design consultants and specialised contractors stand to benefit from steady workflow, while material makers pivot portfolios toward green certifications to defend pricing power.

By Construction Method: Modern Methods Challenge Conventional Dominance

Conventional on-site techniques held an 83.8% command of Thailand construction market size in 2024, enabled by historically ample labour pools and entrenched supply chains. Cast-in-place concrete retains popularity for mid-rise buildings and infrastructure pilings. However, wage pressure and labour scarcity lend urgency to mechanised solutions. Contractors now deploy precast segmental bridges—pioneered in Sakhon Nakhon Province—to compress timelines by up to 30%.

Modern Methods of Construction, paced to grow 6.30% yearly, encompass volumetric modular hotel rooms for Phuket resorts and factory-made wall panels for affordable housing on Bangkok’s outskirts. CPAC 3D-printed structural elements help reduce material waste and speed site assembly, suggesting the traditional-to-modern shift will accelerate post-2026. Government infrastructure tenders increasingly specify BIM coordination, nudging even late adopters to digitise, thereby raising baseline productivity across the Thailand construction market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Investment Source: Private Sector Drives Growth

The private segment captured 60.2% of Thailand construction market share in 2024 and is projected to advance 6.41% CAGR through 2030. Industrial estate operator WHA Corporation reported 61% revenue growth on robust land sales, reinforcing investor appetite within the Eastern Economic Corridor. Mixed-use developers and hotel chains leverage REITs and corporate bonds for capital, ensuring a broad funding base that keeps shovels moving even when public budgets tighten.

Public investment remains the strategic backbone, underwriting megaprojects like the USD 75.7 billion transport masterplan. The PPP framework blends both sources, delivering predictable returns to sponsors and de-risking state balance sheets. High-profile awards such as Laem Chabang Port Phase 3 attest to the model’s success and cement Thailand’s reputation as an investment-friendly hub. As private balance sheets scale, funding diversity further insulates the Thailand construction market from cyclical shocks.

Geography Analysis

Bangkok continues to anchor the Thailand construction market with a 41.6% share in 2024, reflecting ongoing mass-transit expansion, premium office refurbishments, and landmark retail projects. Average house prices climbed 22% year-on-year as land scarcity and higher build standards lifted development costs, even while unsold condominium inventory tempered new high-rise launches. Contractors focus on transit-adjacent plots, green retrofits, and public works that reinforce the city’s role as an administrative and commercial nerve centre.

Chiang Mai is the standout growth pocket, registering a 6.65% CAGR through 2030 on the back of secondary-city empowerment policies. The new U.S. Consulate complex showcases international confidence, while local authorities prioritise smart-city infrastructure, sustainability codes, and heritage preservation. This balanced approach attracts lifestyle-seekers, universities, and light-manufacturing investors, broadening construction demand beyond tourism[3]U.S. Department of State, “Construction of New U.S. Consulate General Chiang Mai,” U.S. Department of State, state.gov.

Phuket, Pattaya, and the rest of Thailand contribute meaningful upside through resort rebuilds, industrial estate rollouts, and renewable-energy plants. Central Pattana’s USD 127 million Central Krabi complex demonstrates mixed-use momentum in tourist corridors, whereas the Saeng Thai Phalangngan solar array in Udon Thani signals how clean-energy investment spreads civil-works contracts into rural provinces. Collectively these regions reduce economic concentration risk and ensure a multi-node growth model for the Thailand construction market.

Competitive Landscape

The Thailand Construction Market is moderately fragmented, with no player holding more than a low-double-digit share and the top five unlikely to exceed 35% combined revenue. Domestic majors—Italian-Thai Development, Ch. Karnchang and Sino-Thai Engineering—leverage long agency ties and multi-disciplinary capability to secure complex rail and airport packages. Heightened scrutiny on foreign contractors after a 2025 project collapse is expected to tighten qualification rules, rewarding firms with proven local safety records.

Strategic moves revolve around technology and sustainability. SCG has lifted low-carbon cement to 63% of output and advanced 3D-printing applications, signalling a portfolio shift towards green materials. WHA Corporation nearly doubled Q1 2024 land transfers to ride electronics reshoring, while Central Pattana launched a multi-city USD 424 million programme to capture tourism recovery and retail densification. Such investments create avenues for subcontractors in façade engineering, smart-building systems and green-certified interiors across the Thailand construction market.

Geographic diversification becomes a common hedge. Contractors court provincial opportunities in Chiang Mai, Khon Kaen and coastal logistics corridors, where competition is thinner and municipal planners offer incentives. Renewable EPC specialists and prefab start-ups enter the market, targeting solar farms and hotel pods that require rapid deployment. Traditional builders respond with alliances, digital site monitoring and integrated design-build packages to remain competitive.

Thailand Construction Industry Leaders

-

Italian-Thai Development PCL

-

Sino-Thai Engineering & Construction PCL

-

Ch. Karnchang PCL

-

Unique Engineering & Construction PCL

-

TTCL Public Company Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Central Pattana outlined a USD 424 million mixed-use expansion across 2024-2026, headlined by the USD 127 million Central Krabi project.

- April 2025: Cabinet advanced the USD 14.1 billion Land Bridge, inviting global bids with construction slated for Q3 2026 start.

- July 2025: GMTP LNG-terminal joint venture signed an EPCC superstructure contract with the POSCO E&C–CAZ consortium for Map Ta Phut Phase 3, locking in international partners to deliver Thailand’s next 8 Mtpa import gate

- February 2025: Phase 2 of the Thai-Chinese high-speed rail gained approval with a USD 9.6 billion budget and bidding to open later this year.

Thailand Construction Market Report Scope

The Thailand construction market covers the growing construction projects in different sectors, like commercial construction, residential construction, industrial construction, infrastructure (transportation construction), and energy and utility construction.

The Thailand Construction Market is segmented by Sector (Residential, Commercial, Industrial, Infrastructure (Transportation), Energy, and Utilities) by Type (New Construction, Additions, Alteration).

The report offers market size and forecasts for Thailand's Construction Market in value (USD) for all the above segments.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Major Cities

| Bangkok |

| Phuket |

| Pattaya |

| Chiang Mai |

| Rest of Thailand |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Major Cities | Bangkok | |

| Phuket | ||

| Pattaya | ||

| Chiang Mai | ||

| Rest of Thailand | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the Thailand construction market?

The market is valued at USD 28.34 billion in 2024 and is projected to reach USD 39.18 billion by 2030.

Which sector holds the largest share of Thailand’s construction activity?

Residential construction leads with 35.7% of total market value in 2024, driven by ongoing urbanization and housing demand in Bangkok and secondary cities.

What is the fastest-growing segment within the market?

Infrastructure construction is expanding at a 6.03% CAGR through 2030, supported by high-speed rail, airport, and port projects.

How significant is private investment in Thailand’s construction industry?

Private capital accounts for 60.2% of construction activity and is forecast to grow at a 6.41% CAGR, reflecting strong business confidence and a mature PPP framework.

Which geographic area is registering the quickest construction growth?

Chiang Mai shows the highest growth pace, with a 6.65% CAGR projected between 2025 and 2030, as secondary-city development gains momentum.

What share of projects still rely on conventional on-site construction?

Conventional on-site methods represent 83.8% of current activity, although modern, prefabricated techniques are gaining ground at a 6.30% CAGR.

Page last updated on: