Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

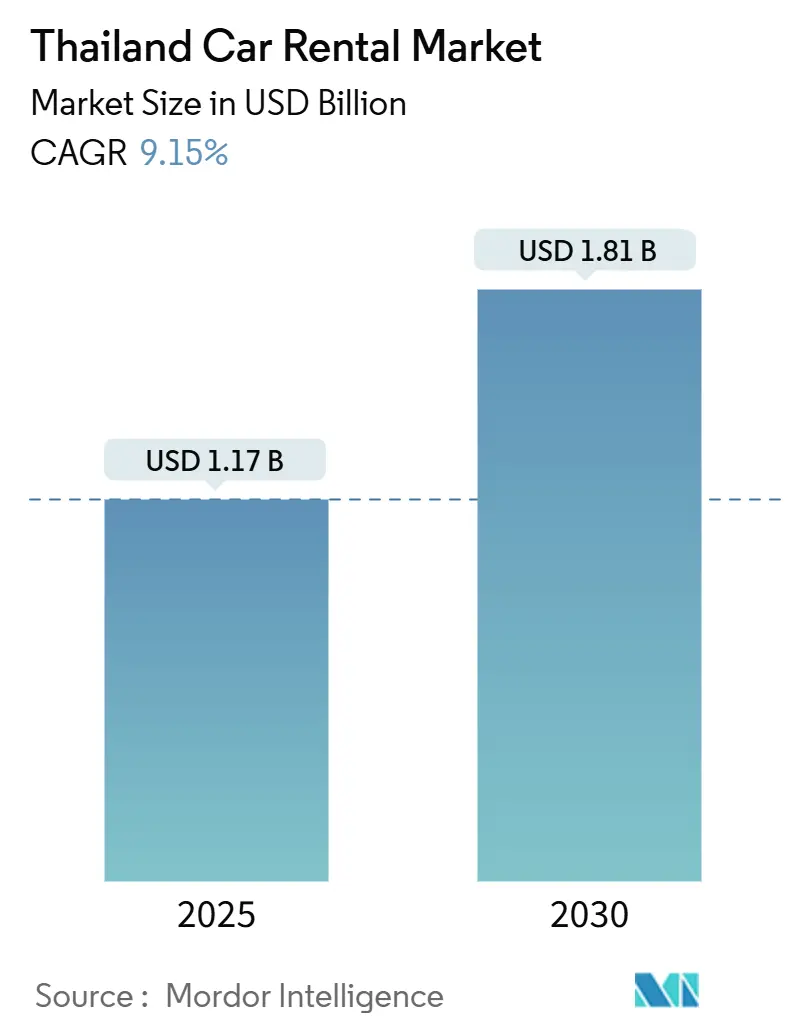

| Market Size (2025) | USD 1.17 Billion |

| Market Size (2030) | USD 1.81 Billion |

| Growth Rate (2025 - 2030) | 9.15% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thailand Car Rental Market Analysis by Mordor Intelligence

The Thailand Car Rental Market size is estimated at USD 1.17 billion in 2025, and is expected to reach USD 1.81 billion by 2030, at a CAGR of 9.15% during the forecast period (2025-2030). This rapid expansion is fueled by a tourism rebound, digital booking proliferation, and pro-EV policies reshaping fleet economics. Visa-free entry schemes, airport capacity upgrades, and widening low-cost carrier networks concentrate demand in gateway cities while unlocking secondary destinations. Digital platforms account for over three-fifths of reservations, and their price-comparison features heighten competitive pressure on brick-and-mortar outlets. Government incentives, cutting EV import duties by up to two-fifths lower the total cost of ownership for electrified fleets, and charging infrastructure investments narrow range-anxiety gaps. Ride-hailing super-apps impose substitution pressure, yet self-drive tourism demand—especially among Chinese visitors—keeps the Thailand car rentals market growing.

Key Report Takeaways

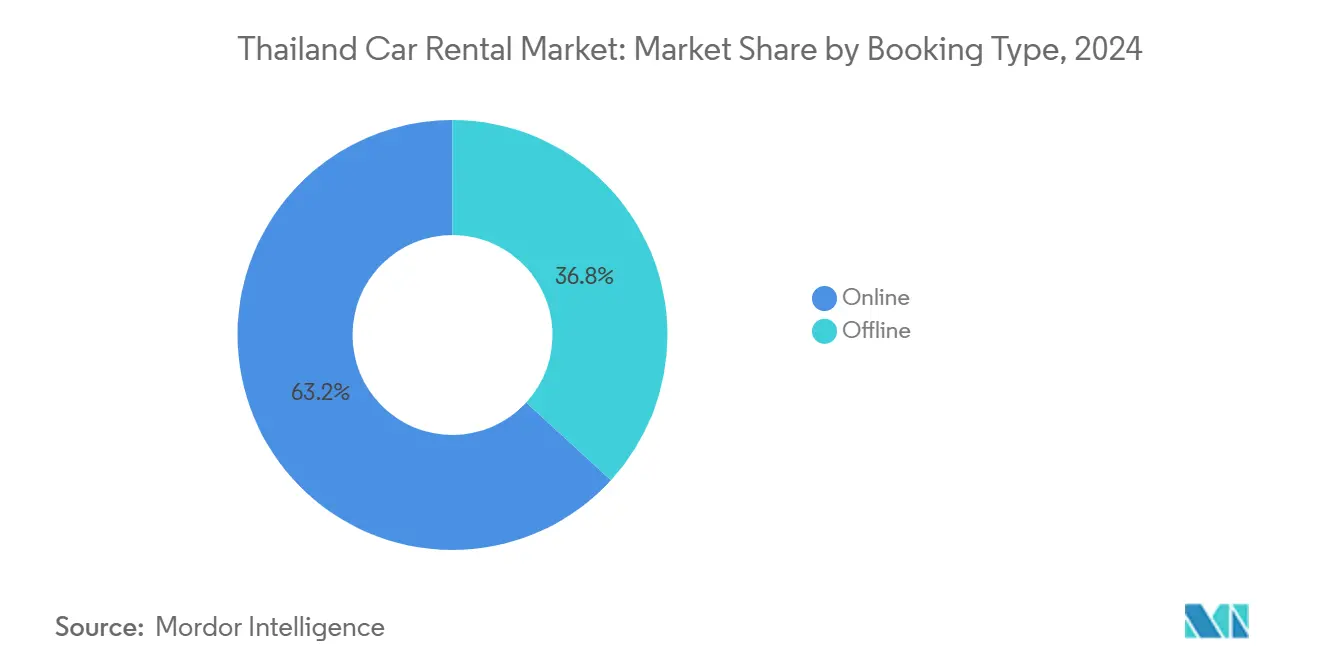

- By booking type, online channels led the Thailand car rentals market with 63.16% of the share in 2024; online channels are forecast to expand at a 9.18% CAGR during the forecast period (2025-2030).

- By rental duration, short-term rentals commanded 71.26% of the Thailand car rentals market size in 2024, while long-term contracts post the highest projected CAGR at 9.31% during the forecast period (2025-2030).

- By application, leisure travel held a 65.47% share of the Thailand car rentals market size in 2024; business travel is advancing at a 9.33% CAGR during the forecast period (2025-2030).

- By vehicle class, economy and mini cars captured 48.72% of Thailand's car rentals market share in 2024, whereas SUVs and MPVs recorded a 9.21% CAGR during the forecast period (2025-2030).

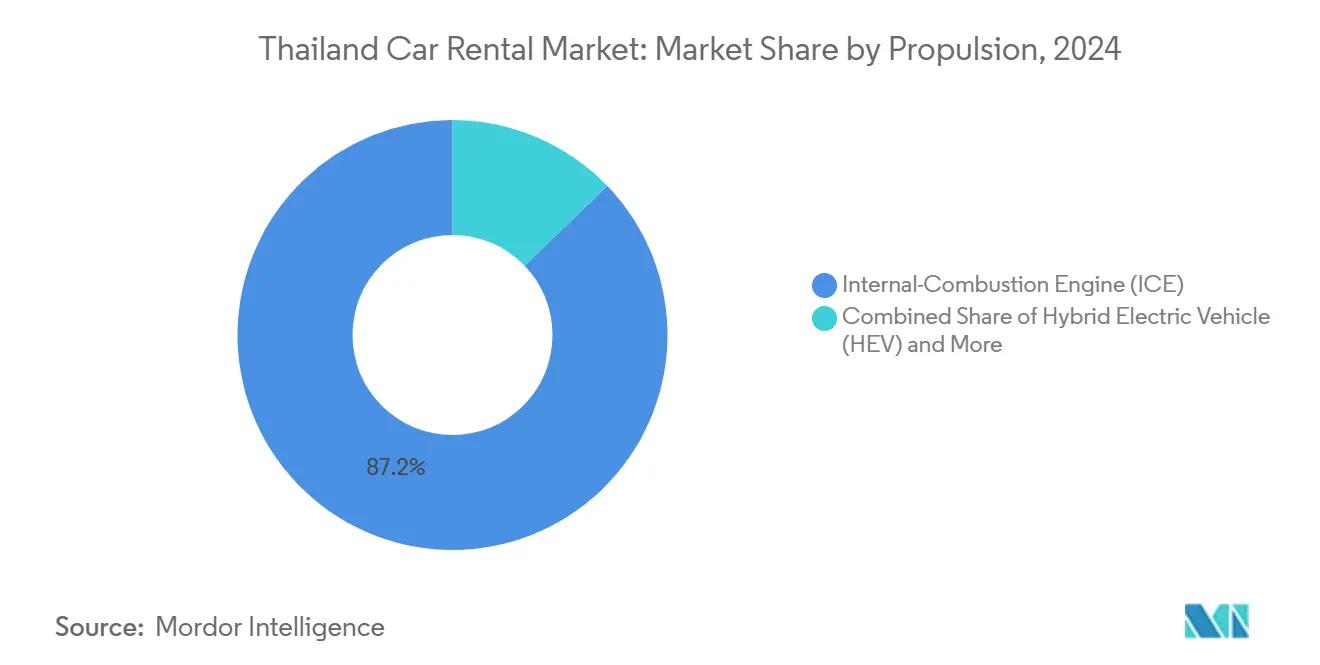

- By propulsion, internal-combustion fleets still dominate with 87.15% share in 2024; battery EV rentals expand at a 9.26% CAGR during the forecast period (2025-2030), the fastest among all drivetrain categories.

- By channel, airport counters held 68.31% of Thailand's car rentals market share in 2024; downtown and off-airport outlets grew at a 9.28% CAGR during the forecast period (2025-2030), as domestic demand deepened.

Thailand Car Rental Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tourism Rebound | +2.1% | National, with concentrations in Bangkok, Phuket, and Chiang Mai | Short term (≤ 2 years) |

| Rise Of Digital Booking | +1.8% | Global, strongest in urban centers and airport locations | Medium term (2-4 years) |

| Surge In Chinese Self-Drive Tourism | +1.5% | National, with emphasis on tourist corridors and scenic routes | Short term (≤ 2 years) |

| Expansion Of Low-Cost Carriers To Secondary Airports | +1.3% | Regional, focusing on secondary cities and emerging destinations | Medium term (2-4 years) |

| Government EV-Rental Purchase Incentive Programme | +1.2% | National, with early adoption in Bangkok and major cities | Long term (≥ 4 years) |

| Blockchain-Based Deposit Systems | +0.6% | Global, led by technology-forward operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tourism Rebound & Visa-Free Schemes

Thailand’s foreign-visitor target for 2025 underpins immediate rental demand, with Chinese arrivals rebounding in 2024 after visa-free measures[1]“TAT expects 39.4 million visitor arrivals in 2025,” Tourism Authority of Thailand, tatnews.org . In April 2024, the Royal Thai Government granted a temporary tourist visa exemption to Russian passport holders, permitting stays of up to 60 days from May 1 to July 31, 2024. This move sought to enhance tourist arrivals. Additionally, domestic trips have spurred demand, helping operators manage seasonality. In response to post-pandemic safety concerns, the Tourism Authority of Thailand (TAT) partnered with Baidu for AI-driven marketing, aiming to restore traveler confidence. This collaboration also underscored the importance of car rentals as a flexible mobility option. Meanwhile, expansions at Suvarnabhumi and Don Mueang airports are poised to support continued volume growth.

Rise of Digital Booking & Price-Comparison Platforms

With a massive internet penetration and mobile-SIM density, Thailand ranks among Southeast Asia’s most connected travel markets[2]“Digital 2025 connectivity report,” National Broadcasting and Telecommunications Commission, nbtc.go.th. Thailand's car rental and travel tech platforms are rapidly evolving, focusing on digital convenience and fee-free models. Rent Connected streamlines bookings via e-wallets like LINE Pay and ShopeePay, while Robinhood Travel supports small accommodation providers with real-time inventory access through its commission-free marketplace. Krungsri Auto's GO app integrates vehicle financing with travel needs, and machine-learning-driven dynamic pricing is reducing the reliance on traditional rental desks, reshaping consumer behavior.

Surge in Chinese Self-Drive Tourism

Behavioral studies show perceived control correlates strongly with Chinese tourists’ intention to choose Thailand, making self-drive options a key facilitator. Chinese tourists spend an average of 6,600 baht per person daily during 6-8 night stays, with positive signals emerging as flight bookings have risen by 5% compared to 2024 and 30 additional weekly flights have been added for Golden Week from cities including Shanghai, Guangzhou, Chengdu, and Kunming. Payment friction caused by card sanctions has led operators to pilot QR-code and e-wallet solutions aligned with Alipay and WeChat ecosystems. Safety messaging via the TAT-Baidu AI alliance mitigates occasional border-zone incidents, keeping the Thailand car rentals market resilient to sentiment swings.

Expansion of Low-Cost Carriers to Secondary Airports

Thai AirAsia’s new routes from Bangkok to Buriram, Surat Thani, and Narathiwat starting July 2025 illustrate the airline-led push into underserved cities[3]“New domestic and international routes,” AirAsia, airasia.com . Six additional airports approved by the Transport Ministry will diffuse visitor flows away from the Bangkok–Phuket–Chiang Mai triangle. Upgrades such as Trang Airport’s capacity rise exponentially, which encourages operators like Drive Car Rental to deploy fleets in emerging gateways. This distribution supports regional tourism goals and lifts vehicle-days-rented in the Thailand car rentals market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Fleet Acquisition | -1.9% | Global, with an acute impact on the premium and EV segments | Short term (≤ 2 years) |

| Competition From Ride-Hailing Apps | -1.4% | National, concentrated in urban centers and tourist areas | Medium term (2-4 years) |

| Stricter Fleet-Financing | -1.1% | National, affecting both operators and consumers | Short term (≤ 2 years) |

| Sparse Charging Infrastructure | -0.8% | National, with rural and intercity gaps most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Fleet Acquisition & Maintenance Costs

New-vehicle sales fell drastically in 2024, a 15-year low, as household debt reached around four-fifths of GDP and banks tightened credit. EV price attrition, driven by Chinese OEM discounts up to THB 340,000, blurs the residual-value outlook, raising the total cost of ownership. J.D. Power recorded four-fifths of Thai owners reporting issues in 2025, amplifying maintenance outlays. These pressures compress margins even as demand swells in the Thailand car rentals market.

Competition From Ride-Hailing & Super-Apps

Companies such as Grab's mobility segment has rapidly expanded, fueled by a vast user base and a suite of integrated services spanning transportation, food delivery, and digital payments. The platform's growing appeal to tourists—underscored by a notable rise in travel-related users—underscores its sway over short-term rental choices. Bundled perks and added convenience are nudging users toward on-demand rides. Even with workforce cuts for cost efficiency, Grab's robust network effects and agile pricing strategies are upending conventional car rental paradigms in Thailand, putting legacy operators on the defensive in their quest for high utilization rates.

Segment Analysis

By Booking Type: Digital Channels Cement Leadership

Online reservations contributed 63.16% share in Thailand car rentals market size in 2024 and is expected to compound at 9.18% through 2030. Web and app portals offer instant confirmation, promo codes, and multilingual support that mirror airline-style UX. Rent Connected and Krungsri Auto's GO app exemplify the shift in Thailand's car rental market toward integrated, data-driven models that enhance customer value and challenge traditional structures. Offline desks remain vital for walk-ins, insurance replacements, and rural travelers who prefer human interaction. Still, sustained LTE and 5G coverage make mobile the dominant purchase path across Bangkok, Phuket, and Chiang Mai. Therefore, the Thailand car rentals market hinges on API-ready reservation engines and AI chatbots that cut service friction.

Traditional agencies confront disintermediation as meta-search engines publish real-time rates from 100+ brands, resetting price expectations among tourists arriving at Suvarnabhumi’s new SAT-1 terminal. For locals, loyalty programs linked to e-wallets such as LINE Pay anchor repeat bookings. Dynamic pricing models can adjust fleet deployment to spike events like Songkran or the Chinese New Year, protecting yields even when occupancy surges. Operators who still rely on phone reservations face rising opportunity costs and struggle to monetize ancillaries such as collision-damage-waivers online, keeping the Thailand car rentals market tilted toward tech-savvy providers.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Rental Duration: Long-Term Contracts Ascend

Due to inbound tourism peaks, short-term demand accounted for 71.26% of Thailand's car rental market share in 2024. Yet long-term tenures will grow faster at 9.31% CAGR as companies favor asset-light mobility solutions. In Thailand, corporate car rental contracts, typically spanning three to five years, ensure stable utilization and reduce seasonal fluctuations. These long-term packages, offering services like insurance, maintenance, and taxes, cater to both economy and premium segments, providing a flexible and reliable alternative to vehicle ownership for expatriates and project-based professionals.

High household debt and stricter auto-loan approvals divert some middle-income residents from outright purchases toward subscription-like rentals. Government projects within the Eastern Economic Corridor require shuttle solutions for executives commuting between industrial parks and Bangkok. Fleet providers specializing in long-term contracts report lower vehicle turnover costs and better remarketing margins. As macro headwinds linger, the Thailand car rentals industry expects risk-adjusted returns to improve in this segment.

By Application: Business Travel Gains Momentum

Leisure tourists accounts for 65.47% share in Thailand Car Rental Market in 2024, yet corporate mobility is expected to grow at a 9.33% CAGR until 2030. Multinational investments in logistics, data centers, and manufacturing across Greater Bangkok lift weekday rental volumes. Projects such as Laem Chabang Port Phase 3 and the Bangkok–Nakhon Ratchasima high-speed rail trigger demand for multi-month vehicles. Business renters pay higher daily tariffs and prefer mid-size sedans or SUVs with telematics features.

Conference tourism, revived under the “MICE to Meet You Again” campaign, reinforces weekday demand that complements weekend leisure pick-ups. Companies outsource fleet management to avoid depreciation exposure and to meet ESG targets through EV adoption. These factors broaden the Thailand car rental market beyond purely seasonal tourist flows.

By Vehicle Class: SUV Preference Intensifies

Economy cars accounts for 48.72% share in the Thailand Car Rental Market in 2024, SUVs expecyed to grow at a 9.21% CAGR during the forecast period (2025-2030), tracking disposable-income gains and family travel patterns. High-demand SUV models, such as the Toyota Fortuner and MG Maxus, command premium daily rates due to their profitability per kilometer and suitability for rugged drives. Their features, including ground clearance, spacious interiors, and ample luggage capacity, make them the preferred choice for travelers seeking comfort and reliability on secondary airport routes to remote destinations.

Compact crossovers also dominate influencer-driven road-trip itineraries on Chinese social platforms. As the supply of hybrids broadens, SUVs gain incremental fuel-efficiency advantages, closing the cost gap with smaller sedans. Fleet managers are reallocating capital toward versatile categories that raise revenue per booking within the Thailand car rentals market.

By Propulsion: EV Transition Picks Up Speed

Internal Combustion Engine (ICE) captured 87.15% of rentals in 2024, where BEV will set the pace at 9.26% CAGR through 2030. Thailand's EV 3.5 program is reducing the cost gap between electric and gasoline vehicles, making EVs more appealing due to lower per-kilometer expenses. However, while Bangkok has a strong fast-charging network, uneven highway infrastructure remains a challenge for long-distance EV adoption.

Hybrid offerings provide a bridge technology, complying with new excise tiers that reward CO2 emissions below 120 g/km. Chinese OEM investments guarantee a local supply pipeline, reducing lead times. EV rentals are, therefore, poised to become a branding differentiator in the Thailand car rental market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Rental Channel: Downtown Outlets Gain Ground

Airports held a 68.31% share in 2024, riding on millions of projected arrivals next year. The ongoing upgrades will lift the throughput of a huge number of passengers by 2030, and established operators like Thai Rent A Car occupy prime terminal real estate. However, downtown branches enjoy 9.28% CAGR as domestic tourism scales and locals seek flexible mobility for provincial trips.

Secondary airports in Mukdahan and Bueng Kan, as well as new motorway links, improve one-way rental economics. Downtown counters also cater to monthly business clients and expatriates who reside long-term in Bangkok’s Sukhumvit and Sathorn districts. Diversifying presence across channels mitigates exposure to airline volatility and aligns with the omnichannel expectations defining the Thailand car rentals market.

Geography Analysis

Bangkok and its metropolitan region dominate the Thailand car rentals market, anchored by Suvarnabhumi and Don Mueang airports, whose combined expansions will elevate capacity to 185 million passengers annually by 2030. The capital’s huge internet penetration allows digital-first operators to scale faster than physical-desk rivals. Strong corporate demand from headquarters in the Sathorn-Silom districts keeps mid-week utilization high, while weekend leisure trips leak into adjacent provinces like Kanchanaburi, aided by expressway connectivity.

Southern Thailand's tourism hubs—Phuket, Krabi, and Koh Samui—are experiencing rapid growth due to new low-cost carrier routes and interconnected island circuits via ferries. Phuket, in particular, is seeing increased rental activity, with its airport preparing for a third terminal to meet rising demand. Higher rental rates in these areas, especially during peak seasons, are driven by limited vehicle availability. To address growing family-group travel during school holidays, rental companies are reallocating SUVs and MPVs to align with regional demand.

Northern clusters around Chiang Mai exhibit robust domestic preference, reinforced by Nan Airport’s THB 3.8 billion upgrade, enabling Airbus A321 and Boeing B737-900 operations. Cultural festivals and cooler climate seasons sustain year-round demand. The Eastern Economic Corridor, with U-Tapao Airport’s expansion, emerges as an industrial travel node, driving weekday business rentals. Northeastern provinces remain nascent yet stand to gain from six new airports that extend tourism circuits. Collectively, these shifts distribute opportunities more evenly across the Thailand car rentals market.

Competitive Landscape

The Thailand car rentals market features moderate fragmentation: the top five brands capture more than half of the market share across airport counters and online platforms. International operators—Hertz, Enterprise, Sixt, and Avis Budget—capitalize on global reservation systems and loyalty programs. Local stalwarts like Thai Rent A Car and Chic Car Rent leverage localized pricing and deep knowledge of domestic travel patterns.

Technology presents the key battleground. Aggregators like Rent Connected integrate 100+ suppliers, offering real-time fleet visibility and multi-wallet payments that challenge proprietary booking engines. BMW Thailand’s Omise partnership showcases advanced tokenization, enabling in-vehicle upsells including toll payments and insurance add-ons. White-space competition centers on EV rentals; players aligning early with government incentives can carve premium niches.

Super-apps led by Grab exert substitution pressure yet create partnership avenues for last-mile drop-offs and bundled packages. Fleet electrification, regional airport entry, and long-term corporate contracts differentiate growth trajectories. Digital maturity and fleet-mix agility drive competitive positioning in Thailand's car rentals market.

Thailand Car Rental Industry Leaders

-

Sixt SE

-

Avis Budget Group

-

Thai Rent A Car

-

Europcar Mobility Group

-

Hertz Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: U Power Limited, the world's first battery swapping technology firm inked a pivotal joint venture deal via its Thai arm, "U SWAP." Partnering with SUSCO Public, a top-tier listed energy firm in Thailand, this alliance aims to harness the unique strengths of both entities. Their joint mission: to champion the rollout of a smart battery swapping system for electric vehicles (EVs) across Thailand.

- March 2025: Thai AirAsia adds three domestic routes from Bangkok Suvarnabhumi to Buriram, Narathiwat, and Surat Thani starting July 2025, broadening regional travel corridors.

- February 2025: Krungsri Auto has announced its business performance for 2024, highlighting a 7% growth in digital loans. The company also achieved a significant milestone by exceeding 4.4 million users on its GO by Krungsri Auto application. This growth underscores Krungsri Auto's commitment to leveraging digital platforms to enhance customer experience and expand its market presence.

Thailand Car Rental Market Report Scope

A car rental service is a business that temporarily uses vehicles for individuals or companies for a specified period, usually ranging from a few hours to several days. Customers can rent a vehicle for various purposes, such as travel, leisure, or business, paying a fee that typically covers the rental period and mileage.

The scope of the car rental market in Thailand is segmented by booking type, rental duration, and application. By booking type, the market is segmented into online and offline. By rental duration, the market is segmented into short-term and long-term. By application, the market is segmented into tourism and commuting. The report offers the market size in value (USD) and forecasts for all the above segments.

By Booking Type

| Online |

| Offline |

By Rental Duration

| Short-term |

| Long-term |

By Application

| Leisure / Tourism |

| Commuting / Business |

By Vehicle Class

| Economy & Mini |

| Compact & Mid-size |

| SUV & MPV |

| Luxury & Premium |

By Propulsion

| Internal-Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) |

| Battery Electric Vehicle (BEV) |

By Rental Channel

| Airport |

| Downtown / Off-airport |

| By Booking Type | Online |

| Offline | |

| By Rental Duration | Short-term |

| Long-term | |

| By Application | Leisure / Tourism |

| Commuting / Business | |

| By Vehicle Class | Economy & Mini |

| Compact & Mid-size | |

| SUV & MPV | |

| Luxury & Premium | |

| By Propulsion | Internal-Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) | |

| Battery Electric Vehicle (BEV) | |

| By Rental Channel | Airport |

| Downtown / Off-airport |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the Thailand car rentals market in 2030?

The sector is expected to reach USD 1.81 billion by 2030, up from USD 1.17 billion in 2025.

How fast is the market growing?

It is expanding at a 9.15% CAGR over the 2025-2030 forecast period.

Which booking channel holds the largest share?

Online platforms commanded 63.16% of total bookings in 2024 and continue to grow.

What role do electric vehicles play in fleet growth?

Battery EV rentals are the fastest-growing propulsion segment, posting a 9.26% CAGR underpinned by government incentives.

How significant are airport locations for rental companies?

Airport counters captured 68.31% of 2024 revenue, but downtown outlets are gaining at a 9.28% CAGR.

Who are the leading players?

Global brands like Hertz, Enterprise, Sixt, and Avis Budget compete with Thai Rent A Car, Chic Car Rent, and digital aggregator Rent Connected.

Page last updated on: