Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

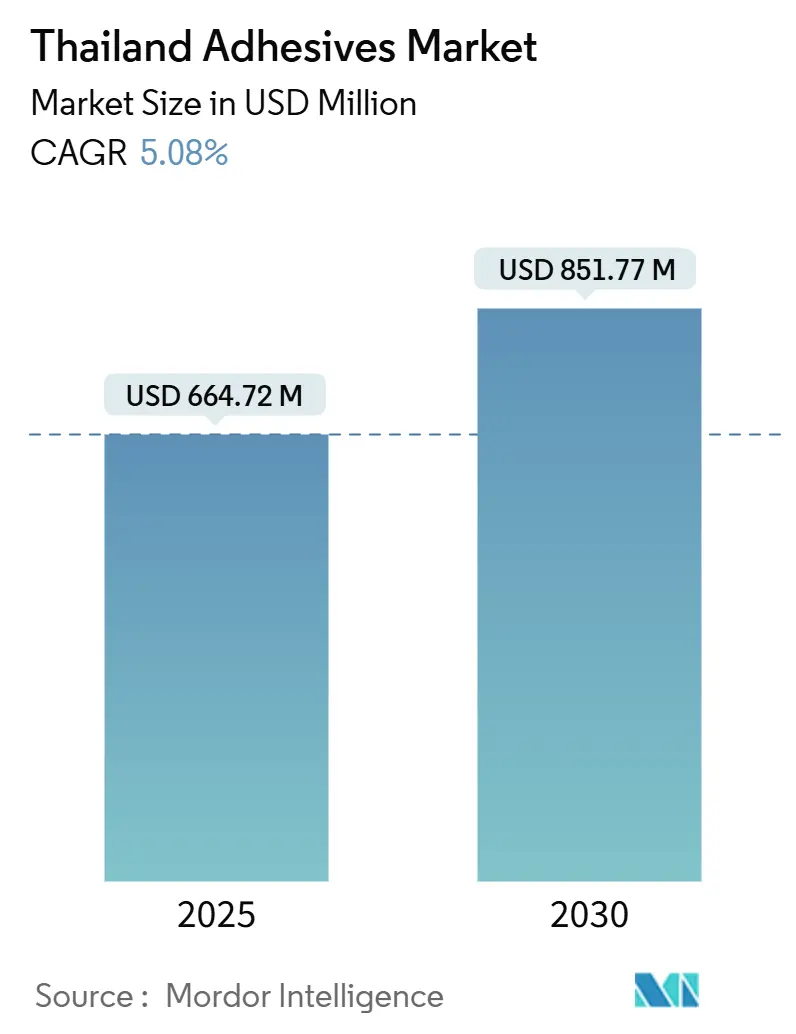

| Market Size (2025) | USD 664.72 Million |

| Market Size (2030) | USD 851.77 Million |

| Growth Rate (2025 - 2030) | 5.08% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thailand Adhesives Market Analysis by Mordor Intelligence

The Thailand Adhesives Market size is estimated at USD 664.72 million in 2025, and is expected to reach USD 851.77 million by 2030, at a CAGR of 5.08% during the forecast period (2025-2030). The current expansion is anchored in large-scale infrastructure projects inside the Eastern Economic Corridor (EEC), aggressive electric-vehicle localization, and fast-growing e-commerce fulfillment, which convert directly into higher demand for construction, automotive, and packaging bonding solutions. Thailand’s well-established petrochemical base ensures relatively secure raw-material availability, while the policy commitment to greener manufacturing pushes converters toward water-borne and hot-melt chemistries. Local subsidiaries of global majors such as Sika, Henkel, and 3M continue to upgrade plant capabilities, and domestic players expand through technology-transfer deals to serve advanced electronics and battery applications. Downside pressures include volatile naphtha-based feedstock costs and the phased roll-out of stringent VOC and food-contact regulations that challenge solvent-borne lines. Nonetheless, rising furniture exports, smart-city investments, and continuing governmental S-curve incentives keep the Thailand adhesives market on a multi-year growth path.

Key Report Takeaways

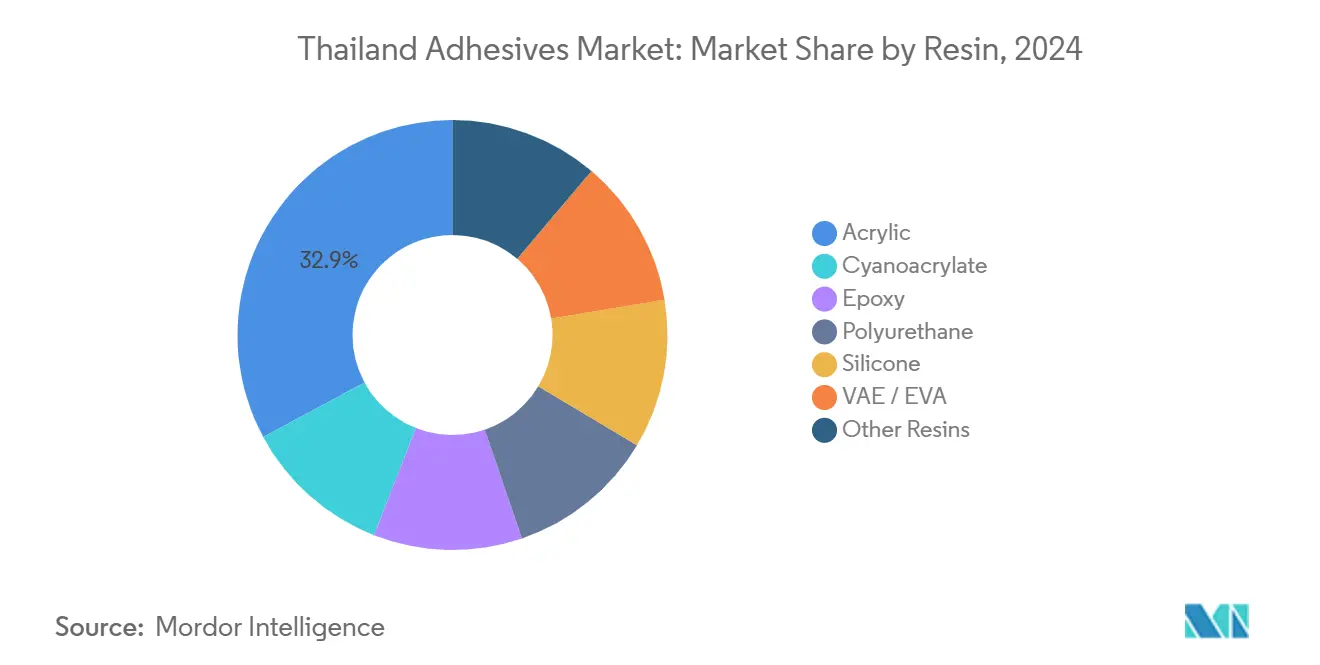

- By resin, acrylics commanded 32.86% of the Thailand adhesives market size in 2024. Polyurethane shows the strongest momentum with a 7.28% CAGR through 2030.

- By technology, water-borne products captured 44.30% of the Thailand adhesives market share in 2024. UV-cured systems are projected to grow 6.71% CAGR between 2025-2030.

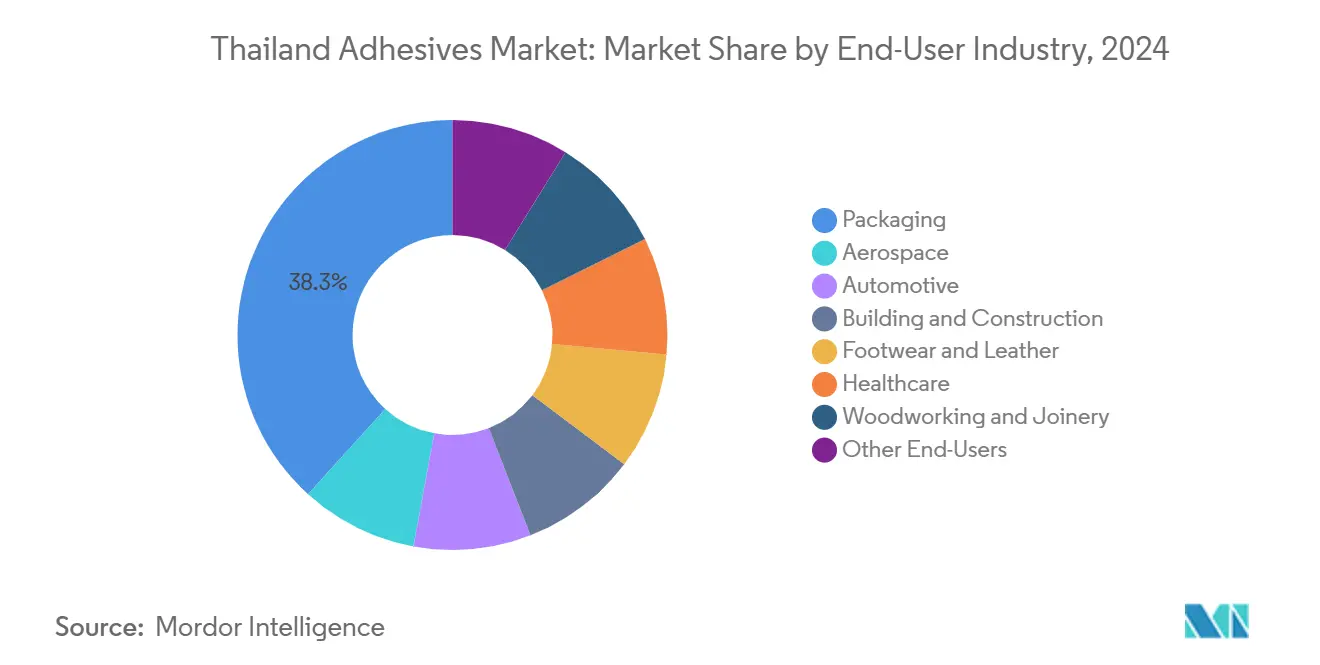

- By end-user industry, packaging led with a 38.29% share of the Thailand adhesives market size in 2024. The automotive sector is expanding at a 7.44% CAGR through 2030, the fastest among all sectors.

Thailand Adhesives Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming e-commerce packaging demand | +1.2% | Nationwide, concentrated in Bangkok and EEC | Short term (≤ 2 years) |

| EV/E-mobility supply-chain localization | +0.8% | EEC provinces: Rayong, Chonburi, Chachoengsao | Medium term (2-4 years) |

| Government EEC infrastructure spending | +0.6% | Eastern provinces, spillover to central Thailand | Long term (≥ 4 years) |

| Shift to water-borne and hot-melt technologies | +0.4% | Industrial zones countrywide | Medium term (2-4 years) |

| Rapid rise of furniture exports | +0.3% | Northern and central export clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Booming e-commerce packaging demand

Thailand’s digital-commerce surge turns fulfillment hubs into the single-largest customer pool for hot-melt and water-based case-sealing grades. Major platforms finance automated sorting centers near Bangkok, demanding consistent bond strength over longer delivery distances and variable temperatures. Sustainability mandates from cross-border retailers intensify the switch from solvent-borne to low-VOC alternatives. As a result, packaging accounted for 38.29% of 2024 revenue, firmly anchoring the Thailand adhesives market.

EV/E-mobility supply-chain localization

Local content targets under the EV3.5 incentive scheme push OEMs and tier-1s to purchase battery encapsulants, structural acrylic tapes, and EMI shielding adhesives inside Thailand. Hyundai’s THB 1 billion EV assembly plant, starting up in 2026, typifies this inflow, while Chinese component suppliers have already tripled their footprint across the EEC[1]K. Akama, “China auto parts makers triple in Thailand on EV battery rush,” Nikkei Asia, asia.nikkei.com . Demand concentrations in Rayong and Chonburi raise volumes for heat-resistant polyurethane and silicone chemistries.

Government EEC infrastructure spending

The EEC budget of THB 652 billion funds 95 projects launched in 2024 and 57 slated for 2025, spanning high-speed rail, port deepening, and the U-Tapao airport expansion. Structural adhesives and sealants resistant to tropical humidity gain steady pull through 2028, with spillover into upstream industrial estates that need flooring, panel, and façade bonding solutions.

Shift to water-borne and hot-melt technologies

PTT Global Chemical, through its allnex SEA Hub, commits to large-scale water-borne resin capacity, reinforcing the national pivot away from solvent emissions. Automotive and electronics exporters factor Scope 3 carbon calculations into sourcing, prompting converters to re-formulate toward high-solid or reactive hot-melt lines.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile petro-feedstock prices | −0.7% | Nationwide, intensified in petrochemical clusters | Short term (≤ 2 years) |

| Stricter VOC and food-contact rules | −0.5% | National with phased compliance | Medium term (2-4 years) |

| Labor shortages in construction sector | −0.4% | Urban megaproject sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile petro-feedstock prices

Despite Thailand’s growing petrochemical capacity, naphtha price swings compress margins for styrene-based, solvent-borne, and synthetic rubber adhesives. Trade-war-related tariff escalations in 2025 deepen the exposure of export-oriented converters to cost spikes, shaving 0.7% off forecast CAGR.

Stricter VOC and food-contact rules

The Ministry of Industry will classify food-contact paper as controlled goods by late 2025, forcing adhesive formulators to certify heavy-metal and migratory chemical levels. In parallel, the 2025 plastic-waste ban limits easy access to recycled PE feedstocks, raising compliance costs.

Segment Analysis

By Resin: Acrylic Strength Versus Polyurethane Innovation

Acrylics retained 32.86% of 2024 revenue thanks to their broad utility across tapes, labels, and construction sealants. Polyurethanes, however, outpace all other chemistries at a 7.28% CAGR, lining up with EV battery encapsulation, truck-body assembly, and high-rise panel bonding. Local PU monomer availability improves after PTTGC’s upstream integration moves, reducing lead times and currency exposure.

Epoxies are disproportionately used in electronics, wind-blade, and aerospace spares, appreciated for their high-temperature resistance. Silicones remain indispensable for automotive gasketing, while EVA and VAE copolymers underpin woodworking lamination lines in Chiang Mai and Ayutthaya. This resin diversity supports Thailand’s ambition to graduate into higher-value manufacturing without sacrificing supply-chain resilience.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Technology: Water-Borne Leadership Drives Environmental Compliance

Water-borne systems held 44.30% of Thailand adhesives market share in 2024, borne out of both regulatory tightening and exporter eco-labels. Multinationals retool lines to raise solid content above 55% while maintaining viscosity profiles suited to Asia’s humid conditions. These shifts allow converters to pre-empt VOC caps expected in 2027. UV-cured chemistries, though only single-digit share today, enjoy a 6.71% CAGR as electronics and luxury-packaging clients specify instant-cure, solvent-free options.

Solvent-borne usage declines in mainstream applications but persists in select industrial niches such as flexible-hose manufacturing, where chemical resistance outweighs emission penalties. Hot-melt, especially metallocene grades, sees renewed interest for high-speed case sealing, aided by lower application temperatures that cut energy bills.

By End-User Industry: Packaging Dominance Meets Automotive Acceleration

Packaging generated 38.29% of the Thailand adhesives market size in 2024, reflecting the country’s leadership in regional e-commerce fulfillment. Automated cartoning lines specify clean-running hot-melt pellets, while export-grade corrugated cases rely on water-based starch-modified dispersions. Automotive demand, although smaller in absolute terms, is projected to expand at a 7.44% CAGR, powered by EV battery manufacturing and lightweight composite bonding. This twin-engine effect sustains a diversified order book, shielding suppliers from sector-specific volatility.

The Thailand adhesives market continues to benefit from healthcare disposables, electronics assembly, and woodworking, albeit at steadier single-digit growth. Noteworthy is the USD 17 million PCB laminate plant, due for completion in 2026, which is expected to increase local consumption of epoxies formulated for high-TG substrates. In the furniture industry, steady shipments to the U.S. and Japan sustain demand for low-formaldehyde dispersion grades, while Thailand’s emerging aerospace MRO cluster provides a niche for high-performance phenolics.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Thailand adhesives market first benefits from the EEC, whose tri-province cluster (Rayong, Chonburi, Chachoengsao) concentrates automotive, smart-electronics, and robotics investments. Over 60% of new specialty-adhesive projects announced in 2024-2025 cite proximity to Laem Chabang port and the expanding double-track rail for feeder logistics[2]Royal Thai Embassy, “Eastern Economic Corridor (EEC),” washingtondc.thaiembassy.org. Central Thailand, anchored by Bangkok, remains the country’s consumption and distribution hub, leveraging its rank as the world’s ninth-most-efficient logistics center for nationwide deliveries.

Northern provinces such as Chiang Mai increasingly supply wooden furniture and processed food, sustaining EVA and water-based dispersion orders. In the south, agriprocessing and emerging aerospace MRO facilities in Phuket and Songkhla spur demand for high-performance elastomeric systems. The comprehensive FTA network, including RCEP and CPTPP accession discussions, further enables adhesive suppliers to ship within ASEAN at preferential tariffs, magnifying export competitiveness.

Digital-infrastructure upgrades, including 5G corridors and data-center builds, broaden electronics-grade adhesive pull in both metropolitan and peri-urban districts. Simultaneously, the cross-country land-bridge project that links the Gulf of Thailand and the Andaman Sea earmarks future opportunities for marine-grade bonding and corrosion-resistant sealants. Environmental legislation, however, applies nationwide, compelling formulators in every region to invest in capture systems or transition to greener chemistries ahead of the 2027 VOC cap.

Competitive Landscape

Thailand’s adhesives market exhibits moderate fragmented. Domestic conglomerates leverage technology-transfer deals to move up the value curve. PTT Global Chemical’s planned allnex SEA Hub extension positions the group as a high-solids resin leader, potentially challenging imports in the next two years. Meanwhile, smaller family-owned converters carve niches in furniture and footwear, yet face capital hurdles in meeting upcoming food-safety and VOC standards. Strategic moves are converging on sustainability and supply-chain localization. Multinationals retrofit Thai factories into regional export bases, hedging against geopolitical tensions elsewhere. Start-ups focus on bio-based raw materials derived from cassava and palm waste, banking on circular-economy incentives. The competitive tempo thus hinges on agility in formulation innovation, compliance, and last-mile technical service—capabilities that differentiate winners in the Thailand adhesives market.

Thailand Adhesives Industry Leaders

-

Henkel AG and Co. KGaA

-

Sika AG

-

H.B. Fuller

-

Selic Corp PCL

-

3M

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2024: Meridian Adhesives Group, a manufacturer of adhesive solutions, announced the acquisition of PAS Bangkok Co., Ltd., an adhesive specialist and one-stop service provider in Thailand. This strategic move strengthens Meridian's footprint in Thailand and complements its existing PAS operations.

- December 2024: Arkema finalized the acquisition of Dow’s flexible packaging laminating adhesives business, one of the leading global producers of adhesives for the flexible packaging market. This acquisition will enable Bostik to ideally complement its existing commercial presence, product offering and technological breadth for flexible packaging.

Thailand Adhesives Market Report Scope

Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, Woodworking and Joinery are covered as segments by End User Industry. Hot Melt, Reactive, Solvent-borne, UV Cured Adhesives, Water-borne are covered as segments by Technology. Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA are covered as segments by Resin.

By Resin

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Polyurethane |

| Silicone |

| VAE/EVA |

| Other Resins |

By Technology

| Water-Borne |

| Solvent-Borne |

| UV-Cured |

| Others |

By End-User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking and Joinery |

| Other End-Users |

| By Resin | Acrylic |

| Cyanoacrylate | |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| VAE/EVA | |

| Other Resins | |

| By Technology | Water-Borne |

| Solvent-Borne | |

| UV-Cured | |

| Others | |

| By End-User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking and Joinery | |

| Other End-Users |

Need A Different Region or Segment?

Customize Now

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF