Textile Chemicals Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

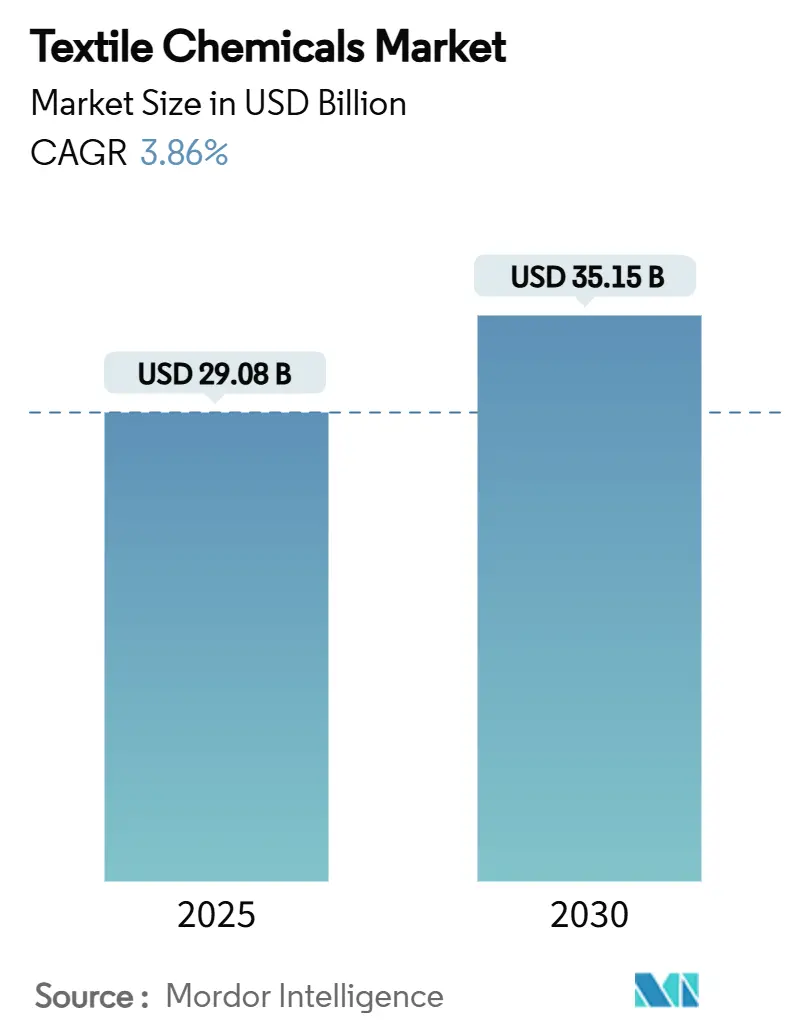

| Market Size (2025) | USD 29.08 Billion |

| Market Size (2030) | USD 35.15 Billion |

| Growth Rate (2025 - 2030) | 3.86% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Textile Chemicals Market Analysis by Mordor Intelligence

The Textile Chemicals Market size is estimated at USD 29.08 billion in 2025, and is expected to reach USD 35.15 billion by 2030, at a CAGR of 3.86% during the forecast period (2025-2030). This moderate growth reflects a maturing sector that is adapting to stricter environmental regulations and rising demand for sustainable manufacturing. Robust expansion in Asia Pacific, escalating adoption of digital printing, and heightened focus on functional finishes are together reshaping competitive priorities across the textile chemicals market. Ongoing PFAS phase-outs and petrochemical price swings are tempering near-term momentum, yet sustained investment in bio-enzymatic and water-based technologies is expected to preserve long-run growth visibility within the textile chemicals market.

Key Report Takeaways

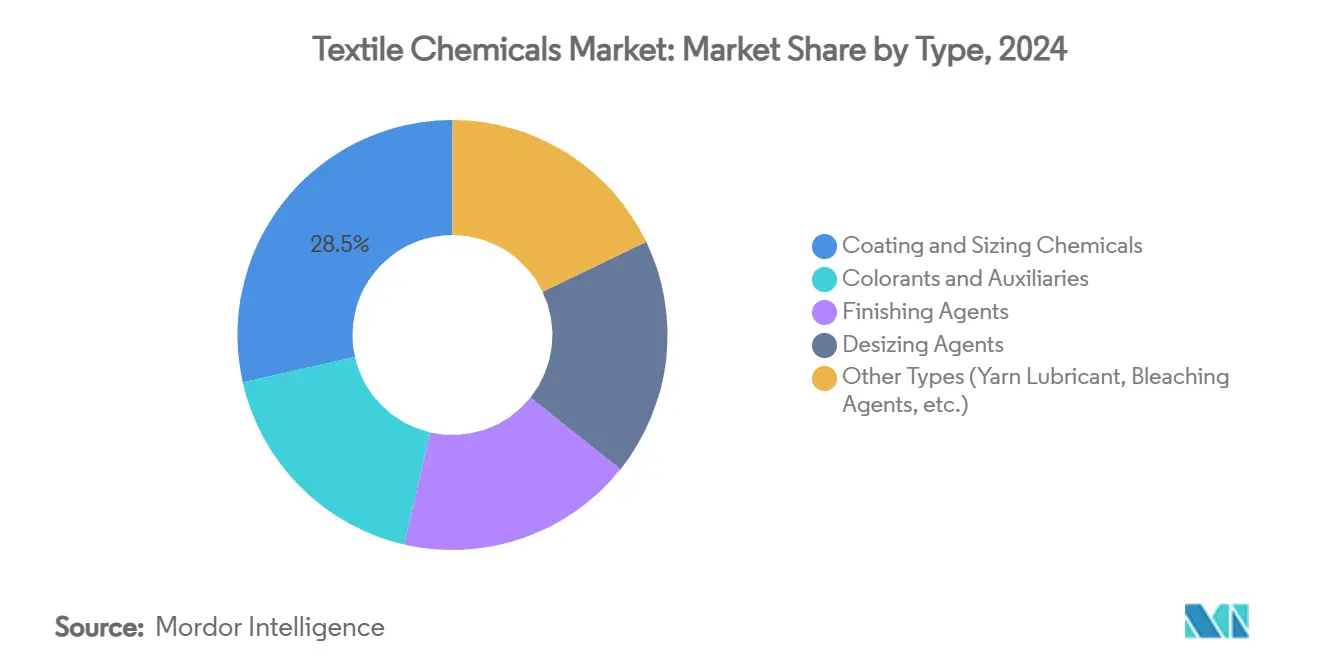

- By type, coating and sizing chemicals led with 28.54% of textile chemicals market share in 2024, while finishing agents are projected to accelerate at a 4.35% CAGR through 2030.

- By raw material, synthetic fibres accounted for 70.14% of the textile chemicals market size in 2024; natural fibres are set to expand at a 4.22% CAGR over 2025-2030.

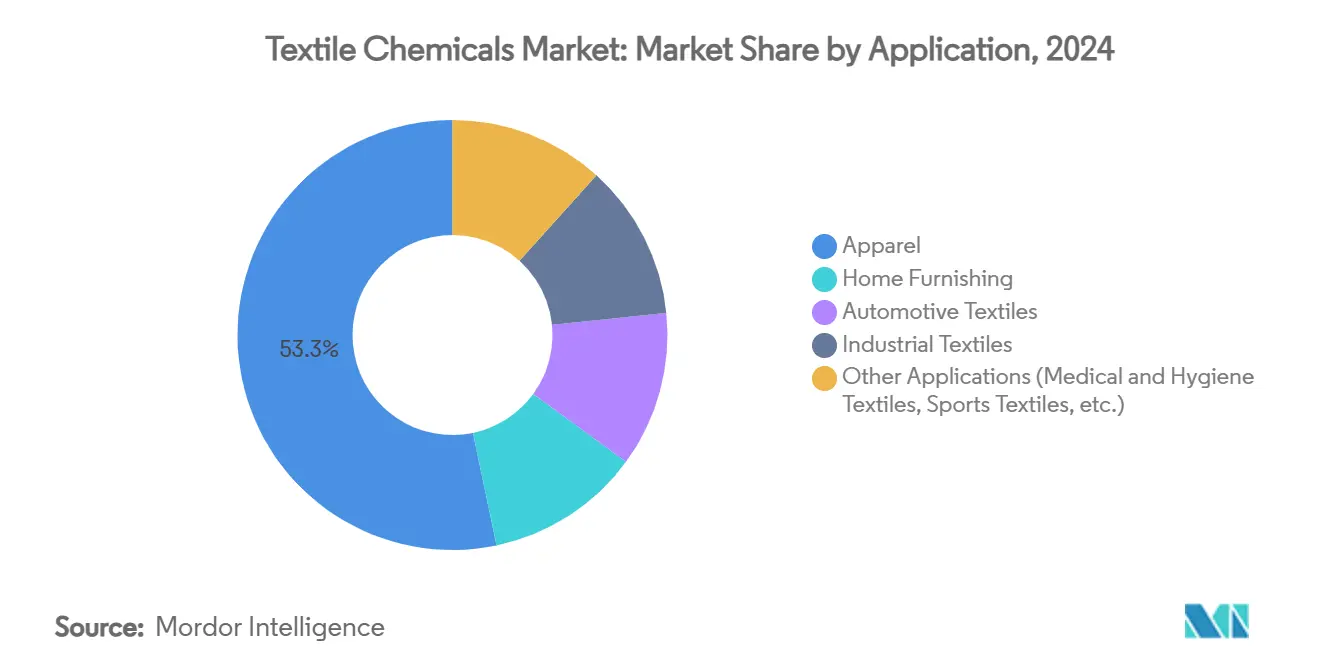

- By application, apparel dominated with 53.27% revenue share in 2024, whereas industrial textiles represent the fastest-growing segment at 4.11% CAGR to 2030.

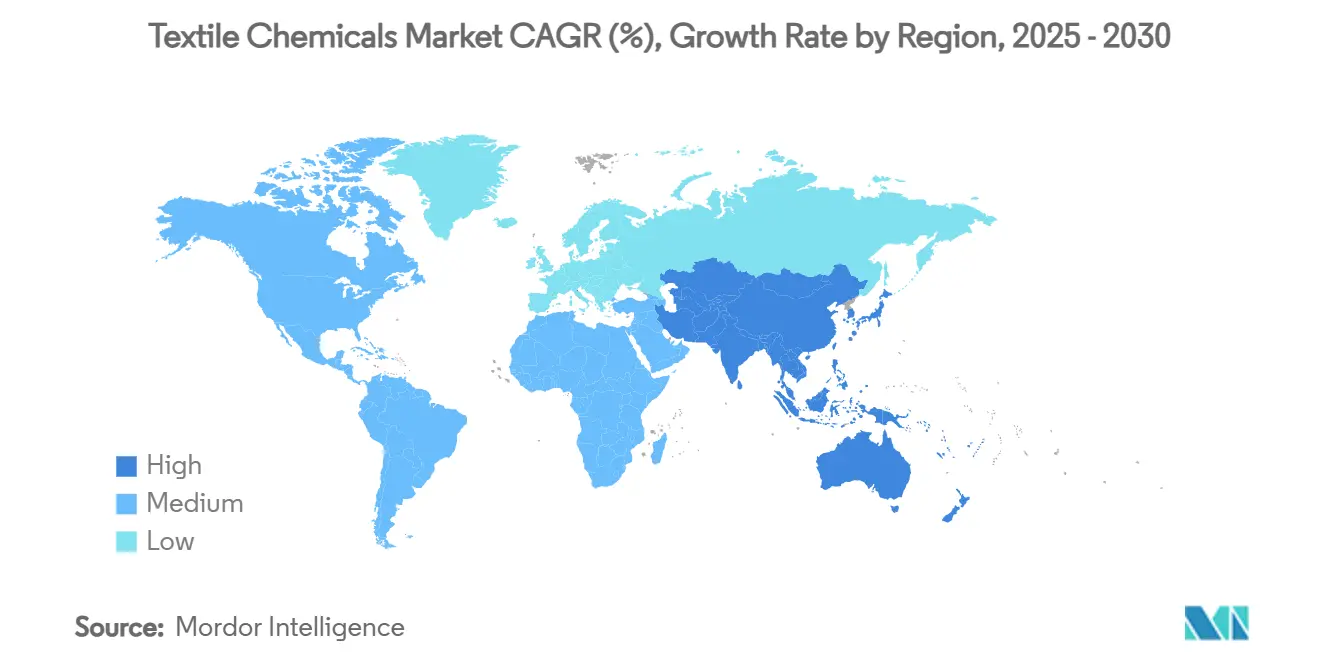

- By geography, Asia Pacific controlled 71.25% revenue in 2024 and is advancing at a 4.01% CAGR, buoyed by China’s USD 301.1 billion export performance and India’s targeted USD 350 billion industry value by 2030.

Global Textile Chemicals Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust growth in Asia Pacific textile production | +1.2% | Asia Pacific core, spill-over to global supply chains | Medium term (2-4 years) |

| Rising demand for technical/industrial textiles | +0.8% | Global, with concentration in North America and Europe | Long term (≥ 4 years) |

| Stricter global regulations favouring low-VOC chemistries | +0.6% | Global, with early adoption in EU and North America | Short term (≤ 2 years) |

| Boom in digital-textile printing inks and auxiliaries | +0.4% | Global, with leadership in Asia Pacific and Europe | Medium term (2-4 years) |

| Rapid adoption of bio-enzymatic processing solutions | +0.3% | Global, with faster uptake in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Growth in Asia Pacific Textile Production

Rapid capacity additions and supportive government incentives are lifting the textile chemicals market across Asia Pacific. China’s 2024 textile exports grew 5.7% to USD 141.96 billion, sustaining large-scale chemical consumption in coating, sizing, and colorant operations. India’s Production Linked Incentive program earmarking INR 10,683 crore for man-made fibres is steering long-run demand for high-performance finishes. Concentrated regional supply chains enable swift adoption of bio-based and low-VOC chemistries, reinforcing Asia Pacific’s centrality within the global textile chemicals market.

Rising Demand for Technical/Industrial Textiles

Automotive lightweighting and medical hygiene requirements are setting new specification baselines for flame-retardant, antimicrobial, and thermally resilient chemistries. The industrial textiles segment’s 4.11% CAGR highlights how the textile chemicals market is transitioning from commodity volumes toward application-specific formulations that command premium pricing. Nanotechnology-enabled finishes are further elevating performance thresholds, intensifying R&D competition among specialty suppliers.

Stricter Global Regulations Favouring Low-VOC Chemistries

California’s statutory PFAS limit of 100 ppm effective January 2025, stepping down to 50 ppm by 2027, is catalyzing a global pivot toward water-based alternatives. Parallel moves in the EU’s Integrated Pollution Prevention and Control framework mandate best-available techniques across dyeing and finishing, creating mandatory pull-through for compliant chemistries. Suppliers with PFAS-free water-repellent portfolios are experiencing accelerated customer onboarding, reinforcing sustainability as a decisive buying criterion in the textile chemicals market[1]European Commission JRC, “Reference Document on Best Available Techniques for the Textiles Industry,” europa.eu.

Boom in Digital-Textile Printing Inks and Auxiliaries

Digital pigment printing requires tailored ink vehicles and pre-treatment auxiliaries that slash water use and eliminate steaming. Brands seeking bespoke, short-run production are driving volume away from conventional batch dyeing toward digital workflows, broadening specialty chemical revenue streams. RUDOLF’s 2024 launch of a formaldehyde-free digital toolbox underscores how process redesign is altering the revenue mix within the textile chemicals market[2]RUDOLF Group, “Digital Pigment Printing Toolbox Launch Press Release,” rudolf.de .

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pollution control costs in dyeing and finishing | -0.9% | Global, with higher impact in developing markets | Short term (≤ 2 years) |

| Volatile petrochemical feedstock prices | -0.7% | Global, with particular impact on synthetic fiber processing | Medium term (2-4 years) |

| PFAS and other substance phase-outs raising reformulation costs | -0.5% | North America and EU initially, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pollution Control Costs in Dyeing and Finishing

Wastewater treatment upgrades now absorb significant capital outlays as operators strive to meet lower COD and BOD discharge limits. Smaller processors that cannot finance biological and membrane technologies are exiting or merging, consolidating chemical demand among larger, compliance-ready buyers. This restructuring raises entry barriers and raises switching costs within the textile chemicals market.

Volatile Petrochemical Feedstock Prices

Crude-linked intermediates such as paraxylene faced double-digit quarterly swings during 2024-2025, translating directly into margin pressure for polyester-oriented surfactants and finishes. Limited pass-through ability forces chemical producers to hedge via long-term contracts or backward integration, encouraging scale and reinforcing the strategic value of bio-based feedstocks that buffer the textile chemicals market from oil shocks.

Segment Analysis

By Type: Coating and Sizing Leadership Amid Finishing Innovation

Coating and sizing chemicals commanded 28.54% of 2024 revenue, underpinning throughput across weaving and knitting lines. Their ubiquity secures steady baseline demand, stabilising the textile chemicals market even during fashion-cycle downturns. Innovation, however, is most visible in finishing agents, expected to grow at 4.35% CAGR through 2030 as customers request water-repellent, stretch-retentive, and antimicrobial functionalities in a single bath.

Environmental performance is differentiating product pipelines, with multifunctional silicone-polymer hybrids displacing fluorinated repellents. Desizing agents have shifted toward bio-enzymatic alternatives that reduce effluent load. Collectively these advances preserve the revenue core while elevating margins, reinforcing the wealth of opportunity in the textile chemicals market.

Note: Segment shares of all individual segments available upon report purchase

By Raw Material: Synthetic Fibre Dominance Alongside Natural Fibre Upswing

Synthetic substrates retained 70.14% revenue share in 2024 due to polyester’s entrenched position in apparel and home textiles. Consistent handle and process behaviour let mills standardise chemical recipes, anchoring the textile chemicals market. Natural fibres, however, are expanding at a 4.22% CAGR on regulatory and consumer pressure for renewables. Enzyme-based scouring and plant-derived mordants now match performance benchmarks once achievable only with petrochemical inputs, opening new growth pockets.

Bio-based specialties are capturing share in coloration and finishing, aided by drop-in compatibility with conventional machinery. As mills invest in blended yarns, chemical suppliers must balance formulation sets for dual fibre lines, adding complexity yet broadening the addressable textile chemicals market.

By Application: Apparel Strength Faces Industrial Textile Momentum

Apparel represented 53.27% of 2024 turnover, leveraging continuous fast-fashion runs and diverse seasonal palettes. Rising social compliance costs, though, are compressing margins, compelling mills to adopt higher-efficiency auxiliaries and low-risks dyes. Industrial textiles, expanding at 4.11% CAGR, apply stringent technical specifications demanding flame-retardant, low-smoke, and antibacterial systems, thereby boosting average selling prices.

Home furnishings and hygiene textiles further diversify demand, as consumers pay a premium for easy-clean, odour-control, and hypoallergenic features. Integration of smart yarn sensors is spawning next-generation coating chemistries, sustaining innovation pipelines essential for the long-term vitality of the textile chemicals market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia Pacific captured 71.25% revenue in 2024, supported by China’s USD 301.1 billion export base and India’s projected USD 350 billion industry by 2030. Regional governments continue to subsidise capacity expansion and technical-textile clusters, maintaining a 4.01% CAGR that anchors the global textile chemicals market. Supply-chain depth, from fibre spinning to garment assembly, allows rapid qualification of new green chemistries, ensuring Asia Pacific’s sustained leadership.

North America holds a smaller yet strategically important share, specialising in protective, aerospace, and medical fabrics where specification compliance trumps unit cost. Mexico’s near-shoring momentum to US brands is reigniting regional yarn dyehouse investments, opening fresh routes for high-value auxiliaries. California and New York PFAS rules accelerate adoption of water-based repellents, positioning North America as a testbed for next-wave sustainable options within the textile chemicals market.

Europe’s mature sector benefits from advanced machinery and a robust regulatory framework that favours circularity. Investment in textile-to-textile recycling chemicals is climbing, with Germany and Italy pioneering polyester depolymerisation plants. Strong luxury and technical segments fund R&D in low-impact finishes, upholding Europe’s influence on global standards. Emerging regions in South America and the Middle East are scaling output but remain constrained by infrastructure gaps, delaying their fuller integration into the textile chemicals market.

Competitive Landscape

The textile chemicals market exhibits moderate fragmentation. Archroma finalised its purchase of Huntsman Textile Effects in March 2025, amalgamating pigment, auxiliary, and finishing portfolios under one roof and signalling a new era of scale-driven innovation. Clariant pre-empted regulatory crackdowns by announcing a 100% PFAS-free range in December 2023, boosting customer conversions from brands that face imminent state-level bans.

Intense R&D rivalry centres on multifunctional, bio-derived chemistries able to withstand repeated laundering without performance loss. Digital print auxiliaries and enzyme toolkits are headline growth areas, with specialty suppliers partnering directly with printer OEMs and mill integrators. Venture investment is also fuelling start-ups developing biosurfactants and fermentation-based dye precursors, introducing disruptive possibilities to the textile chemicals market.

In response, incumbents are adopting open-innovation models, co-creating bespoke formulations with key accounts to lock in multi-year supply frameworks. Data-enabled dosing and inline monitoring tools extend competitive differentiation beyond the drum to the process floor, embedding chemical suppliers deeper into mill operations and solidifying customer retention.

Textile Chemicals Industry Leaders

-

Archroma

-

Dow

-

DyStar Group

-

Huntsman International LLC

-

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Archroma declared a USD 750,000 operational expansion in Allendale County, South Carolina. This move will generate 6 new jobs at its facility, focusing on dyes, chemicals, and optical brightening agents tailored to the textile market.

- February 2024: Archroma unveiled its latest innovation, Super Systems+. These advanced systems integrate fiber-specific processing solutions with intelligent effects, empowering textile and apparel brands, retailers, and mills to enhance both their economic and environmental sustainability, as well as influence the textile chemicals market.

Global Textile Chemicals Market Report Scope

Textile chemicals are specialty chemicals used during the dyeing and processing textiles to impart desired properties to an array of end products used in clothing, bedding, carpets, car interiors, industries, etc. Processing natural or artificial fabrics with textile chemicals improves textile wearability, functionality (such as imparting antibacterial features, flame retardancy, etc.), and appearance. The textile chemicals market is segmented by type, application, and geography. By type, the market is segmented into coating and sizing chemicals, colorants and auxiliaries, finishing agents, de-sizing agents, and other types. By application, the market is segmented into apparel, home furnishing, automotive textile, industrial textile, and other applications. The report also covers the size and forecasts for the textile chemicals market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD Million).

| Coating and Sizing Chemicals |

| Colorants and Auxiliaries |

| Finishing Agents |

| Desizing Agents |

| Other Types (Yarn Lubricant, Bleaching Agents, etc.) |

| Natural Fibres |

| Synthetic Fibres |

| Bio-Based |

| Speciality Chemicals |

| Apparel |

| Home Furnishing |

| Automotive Textiles |

| Industrial Textiles |

| Other Applications (Medical and Hygiene Textiles, Sports Textiles, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Coating and Sizing Chemicals | |

| Colorants and Auxiliaries | ||

| Finishing Agents | ||

| Desizing Agents | ||

| Other Types (Yarn Lubricant, Bleaching Agents, etc.) | ||

| By Raw Material | Natural Fibres | |

| Synthetic Fibres | ||

| Bio-Based | ||

| Speciality Chemicals | ||

| By Application | Apparel | |

| Home Furnishing | ||

| Automotive Textiles | ||

| Industrial Textiles | ||

| Other Applications (Medical and Hygiene Textiles, Sports Textiles, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Textile Chemicals Market size?

The textile chemicals market is valued at USD 29.082 billion in 2025.

What compound annual growth rate is the market projected to record through 2030?

The market is forecast to expand at a 3.86% CAGR, reaching USD 35.145 billion by 2030.

Which region holds the largest share of global textile chemicals demand?

Asia Pacific leads with 71.25% market share, supported by China’s large export base and India’s industry expansion plans.

Which product segment is expected to grow the fastest between 2025 and 2030?

Finishing agents are projected to rise at a 4.35% CAGR as brands seek multifunctional, sustainable textile finishes.

Page last updated on: