Purified Terephthalic Acid Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

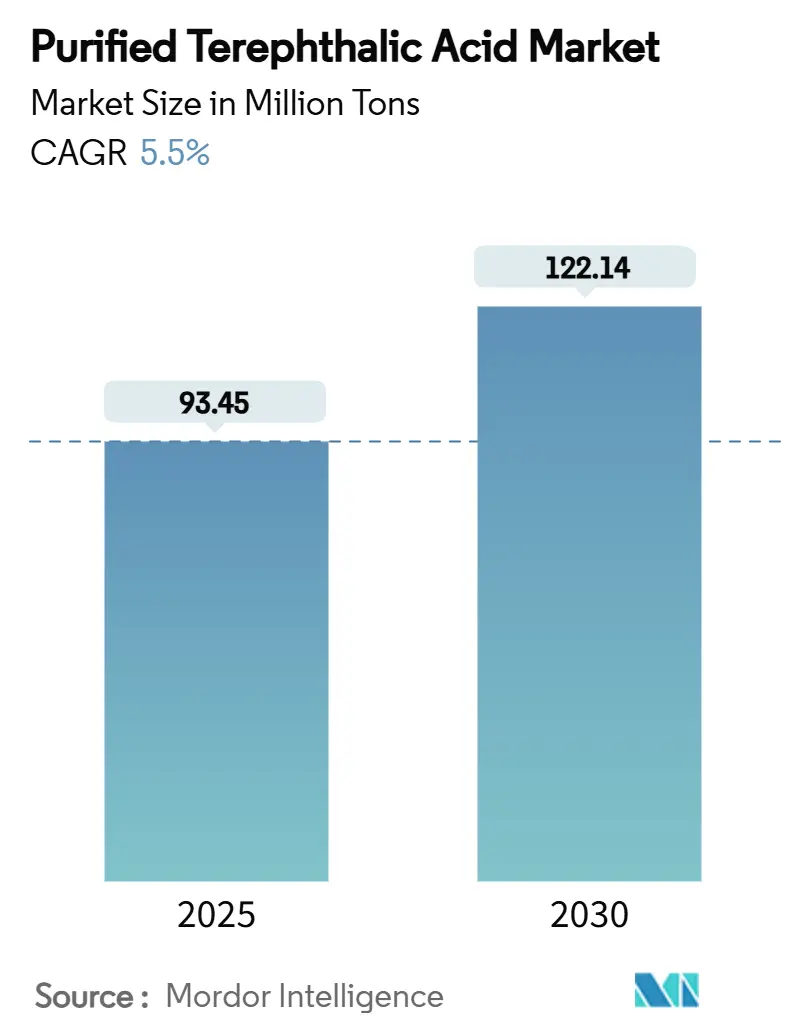

| Market Volume (2025) | 93.45 Million tons |

| Market Volume (2030) | 122.14 Million tons |

| Growth Rate (2025 - 2030) | 5.50% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Purified Terephthalic Acid Market Analysis by Mordor Intelligence

The Purified Terephthalic Acid Market size is estimated at 93.45 Million tons in 2025, and is expected to reach 122.14 Million tons by 2030, at a CAGR of 5.5% during the forecast period (2025-2030). Strong polyethylene terephthalate (PET) demand across packaging, textile and emerging automotive end-uses underpins this expansion, even as mature regions restructure capacity. Integration of petrochemical chains in China and India is reinforcing cost leadership, while chemical recycling technologies are unlocking fresh sources of feedstock and premium price pools. Feedstock volatility is narrowing margins for stand-alone producers, prompting a visible shift toward backward integration and operational efficiencies. Regulatory pushes for higher recycled content in PET packaging, especially in the European Union, are reshaping procurement strategies and spurring investment in closed-loop systems.

Key Report Takeaways

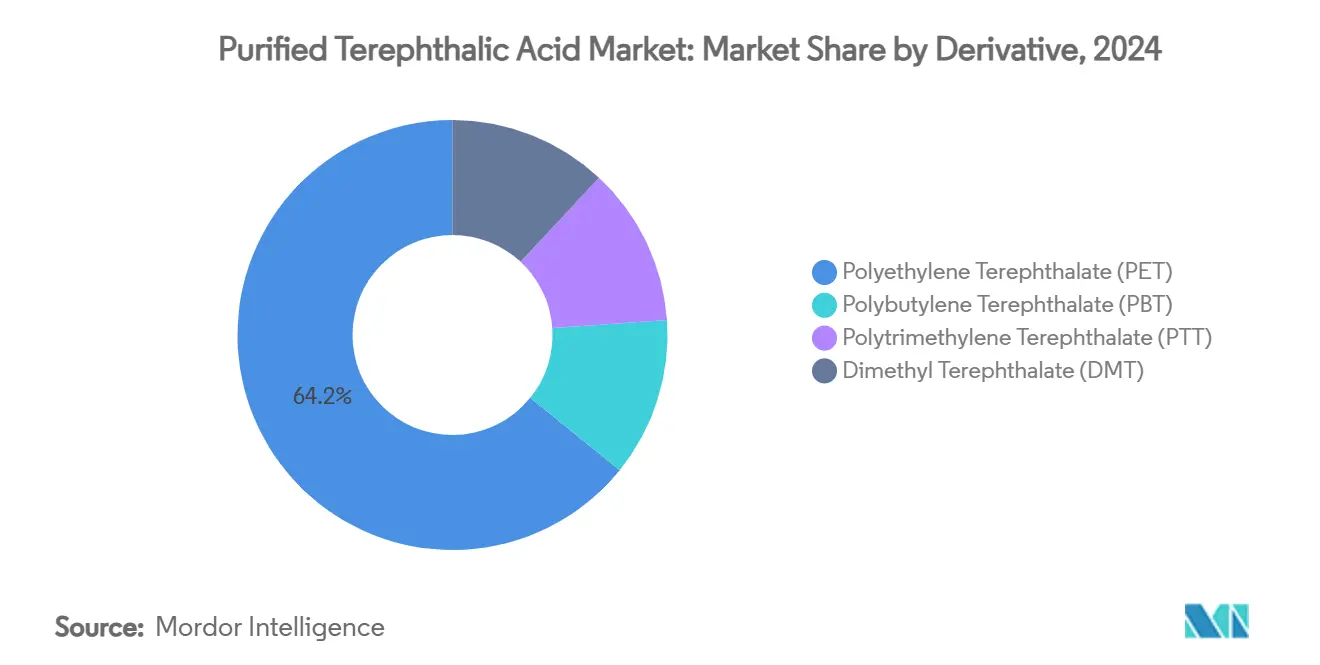

- By derivative, polyethylene terephthalate held 64.18% of purified terephthalic acid market share in 2024 and is forecast to expand at a 6.56% CAGR to 2030.

- By technology, conventional PX oxidation retained 91.15% share in 2024, yet bio-based PTA is the fastest-growing technology at 6.82% CAGR to 2030.

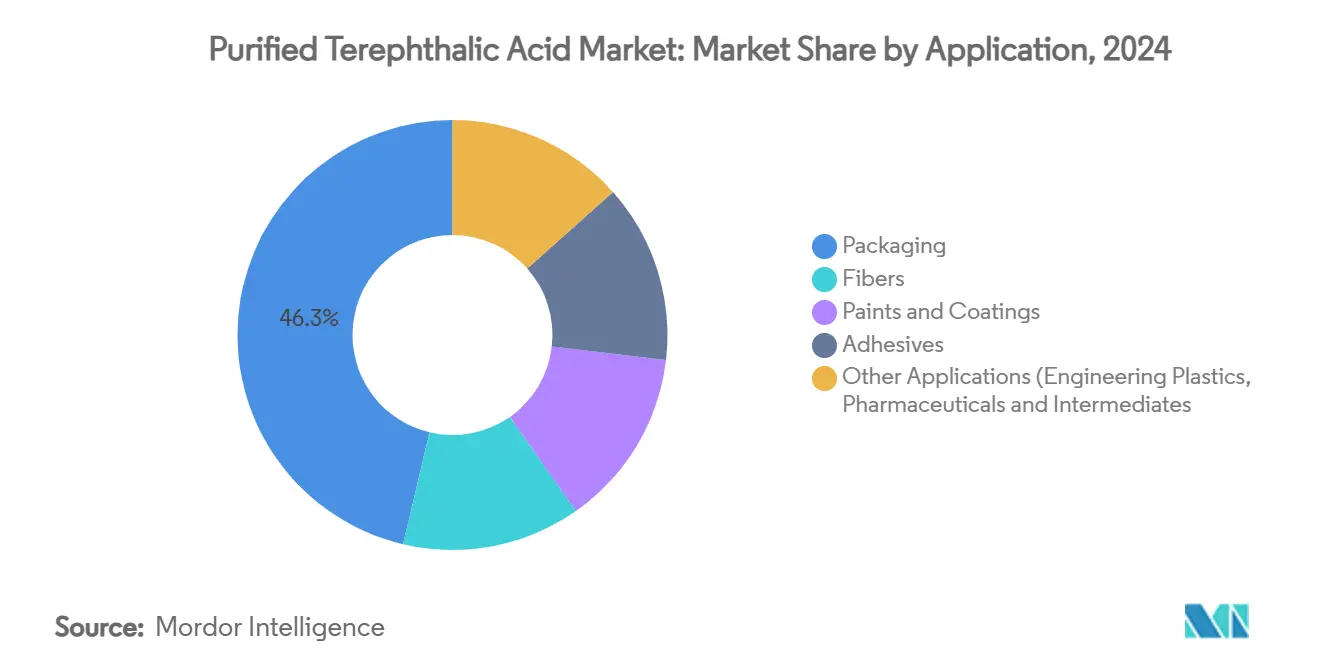

- By application, the packaging segment accounted for 46.29% share of the purified terephthalic acid market size in 2024 and is advancing at a 6.28% CAGR through 2030.

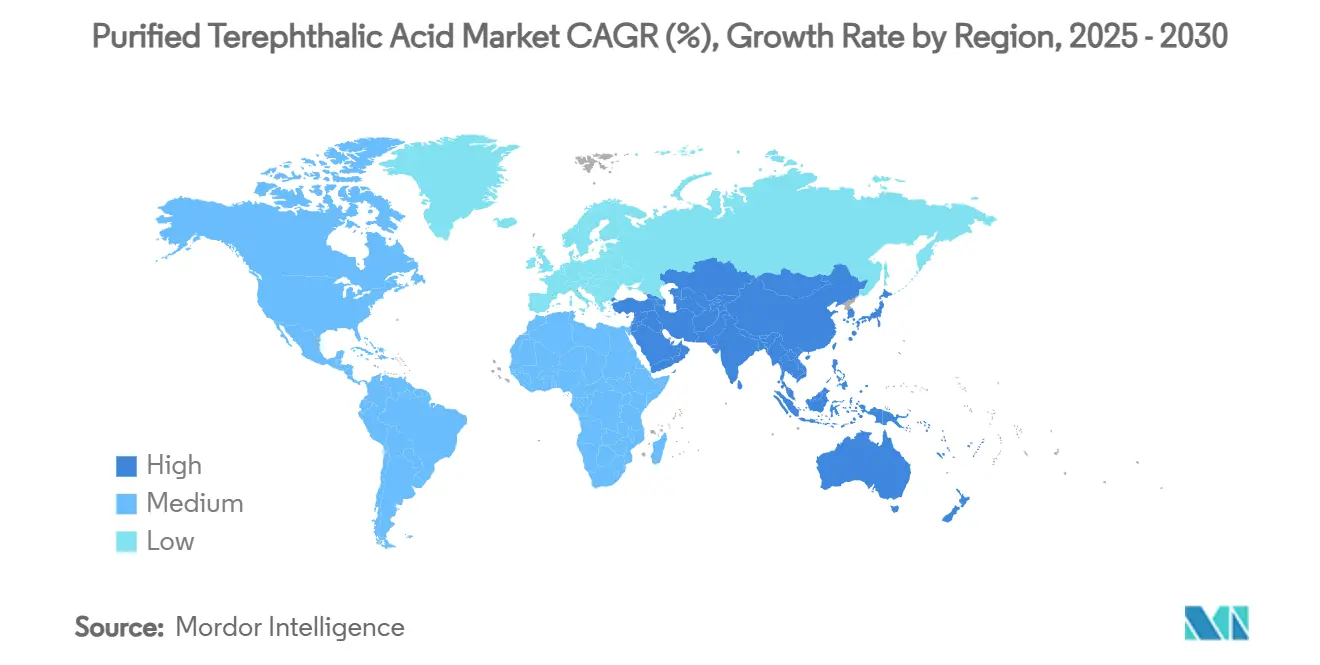

- By geography, Asia-Pacific led with 53.62% revenue share in 2024 and is growing at a 7.18% CAGR to 2030.

Global Purified Terephthalic Acid Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong PET packaging demand from e-commerce sector | +1.2% | Global, pronounced in North America & Asia-Pacific | Medium term (2-4 years) |

| Growing production of polyester fiber | +1.8% | Asia-Pacific core, spill-over to South America | Long term (≥ 4 years) |

| Growing utilization of PET from automotive industry | +0.7% | North America & EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Recycled-PET loop mandates | +0.9% | EU primary, North America secondary | Medium term (2-4 years) |

| Growing usage of battery separator grade PTA | +0.4% | Asia-Pacific core, technology transfer global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong PET Packaging Demand from E-commerce Sector

E-commerce shipping formats now favor lightweight PET containers that withstand automated sortation and long transit cycles, driving higher-grade PTA offtake. Brands in India and Southeast Asia are adopting barrier-enhanced bottles that preserve carbonation and flavor during direct-to-consumer delivery peaks. Quarterly promotions such as Singles’ Day and Diwali generate sudden PTA call-offs, keeping regional inventories tight and sustaining spot premiums. North American food and beverage suppliers are also redesigning packaging for parcel carriers, lifting PTA specifications for stress-crack resistance. These design changes convert glass and metal volumes to PET, broadening the purified terephthalic acid market in both volume and value terms. Seasonal spikes incentivize supply contracts with formula-based pricing that protect converters from PX price swings.

Growing Production of Polyester Fiber

China’s integrated PTA-to-fiber parks leverage onsite utilities and logistics synergies to deliver cost-effective fiber at scale, anchoring long-term PTA demand. Indian refiners are following suit; IndianOil is lifting PTA capacity from 553,000 tons to 700,000 tons at Panipat and adding a 1.2 million-ton line at Paradip by mid-2026, cementing India’s role as a swing supplier[1]Indian Oil Corporation, “Panipat and Paradip Expansion Investor Presentation,” iocl.com. Automotive nonwovens, geotextiles and functional apparel continue to diversify end-uses for polyester fibers, each requiring narrow PTA impurity windows that command a modest price premium. Sinopec Yizheng’s incremental 60,000 tons of polybutylene terephthalate illustrates strategic migration into engineering polymers that buffer against PET cyclicality. The durable-goods orientation of these fibers supports steadier purified terephthalic acid market volumes compared with fashion cycles.

Growing Utilization of PET from Automotive Industry

Electric-vehicle platforms are substituting metal with reinforced PET composites in battery enclosures, under-body shields and interior panels to shave vehicle weight. Trials using chemically foamed recycled PET have recorded 15-20% mass reductions while meeting crash standards. Such applications demand PTA with very low para-toluic acid impurity, promoting adoption of Invista’s T10 process upgrades at existing plants. European Union directives on End-of-Life vehicles are incentivizing OEMs to procure materials that are chemically recyclable back to PTA, embedding circularity into sourcing contracts[2]European Commission, “Directive 2023/2683 on Recycled Content in PET Bottles,” europa.eu. As these specifications tighten, PTA producers offering automotive-grade certifications gain preferential access and price lift, supporting purified terephthalic acid market growth in high-margin niches.

Recycled-PET Loop Mandates

EU legislation requires 25% recycled content in PET bottles by 2025 and 30% by 2030, prompting beverage companies to lock in chemically recycled PTA supply agreements. Parallel deposit return schemes boosted Portuguese bottle collection rates to 68.7%, elevating feedstock supply for depolymerization plants. U.S. academic studies show nationwide redemption programs could raise PET recycling from 24% to 82%, signaling a sizeable future PTA-equivalent stream for North American producers. Advanced methanolysis using gamma-valerolactone now reaches 97.8% dimethyl terephthalate yield, proving commercial readiness. These developments reinforce the purified terephthalic acid market as a cornerstone of plastic circularity and open differentiated pricing tiers for recycled-origin PTA.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicological concerns | -0.3% | EU primary, regulatory spillover to North America | Short term (≤ 2 years) |

| Volatile PX & crude prices | -1.1% | Global, acute in margin-sensitive regions | Short term (≤ 2 years) |

| Rise of PEF & other bio-polymers | -0.6% | EU & North America early adoption, Asia-Pacific following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Toxicological Concerns

ECHA registration dossiers classify terephthalic acid in the 1–10 million-ton production band within the European Economic Area, prompting heightened scrutiny over wastewater and dust exposures[3]European Chemicals Agency, “Terephthalic Acid Registration Dossier,” echa.europa.eu. Although oral LD50 values exceed 5,000 mg/kg, newer reproductive studies have led regulators to propose stricter monitoring of plant effluents. Small and mid-size producers lacking advanced treatment systems face capital outlays or possible shutdowns, trimming short-term purified terephthalic acid market capacity in Europe. Compliance costs also rise under the EU’s General Product Safety Regulation, requiring manufacturers to document the safety of PTA-derived finished goods before market entry.

Volatile PX & Crude Prices

Paraxylene exhibits strong correlation with gasoline demand, especially in U.S. spot markets, leading to unpredictable PTA-PX spreads. China’s record 14.8 million barrels per day crude runs in 2024 flooded the market with PX, yet refinery margins shrank as downstream demand lagged capacity additions. Disputes in the South China Sea further threaten maritime routes that carry a third of global trade, adding freight risk premiums. These factors compress PTA margins, compelling producers to hedge feedstock exposure or secure integration into aromatics refining, thereby safeguarding purified terephthalic acid market profitability.

Segment Analysis

By Derivative: PET Dominance Reinforced by Integration

Polyethylene terephthalate represented 64.18% of global derivative consumption in 2024, translating into the bulk of purified terephthalic acid market demand. Integrated players convert PTA to PET on-site, securing conversion margins and logistical savings that reinforce competitive barriers. The segment’s anticipated 6.56% CAGR reflects both volume growth and higher-value resins for hot-fill, refillable and barrier-enhanced packaging. Polybutylene terephthalate remains a specialty derivative with stronger heat resistance, and Sinopec Yizheng’s 80,000-ton expansion underscores the material’s automotive and electronics prospects. Polytrimethylene terephthalate is carving out a niche in functional sportswear, benefiting from its elastic recovery and softness.

Economic analyses now favor direct esterification of PTA over dimethyl terephthalate (DMT). Oxxynova’s 2022 closure of its German DMT unit underlined structural cost disadvantages. Nonetheless, catalytic processes achieving 99.9% DMT yields from PET waste demonstrate a pathway to circular DMT streams if policy incentives materialize. Overall, PET integration strategies continue to anchor the purified terephthalic acid market, while higher-margin derivatives diversify revenue against PET price cycles.

Note: Segment shares of all individual segments available upon report purchase

By Technology: Bio-based Disruption Accelerates

Conventional PX oxidation still accounted for 91.15% of production in 2024, anchoring the purified terephthalic acid market with proven economies of scale. Yet, bio-based PTA is set to record a 6.82% CAGR, driven by Idemitsu Kosan’s biomass naphtha route in Taiwan and Neste–Suntory–ENEOS collaborations that demonstrate full bio-PX integration. Chemical recycling technologies, particularly methanolysis and glycolysis, are moving from pilot to commercial scale as deposit schemes raise post-consumer PET availability. Koch Technology Solutions licenses about two-thirds of global PTA capacity and is rolling out energy-efficient single-stream reactors up to 1.6 million tons, cutting unit emissions and facilitating bolt-on recycled feed integration.

Policy signals favor lower-carbon routes. Life-cycle studies show that biomass- or waste-based PTA cuts greenhouse-gas footprints by 30–45% versus fossil PTA, an advantage increasingly monetized through carbon pricing. Producers capable of toggling between fossil, biomass and recycled feeds will gain flexibility to meet shifting customer sustainability targets within the purified terephthalic acid market.

By Application: Packaging Leadership Amid Diversification

Packaging consumed 46.29% of PTA in 2024 and is projected to grow 6.28% annually through 2030, consolidating its status as the largest purified terephthalic acid market application. Lightweight bottle programs for e-commerce, tethered caps mandated by the EU and higher recycled content thresholds all raise PTA tonnage per finished container. Fiber applications, spanning apparel, home textiles and industrial nonwovens, continue to generate steady demand tied to population growth and infrastructure projects. Paints and coatings leverage PTA’s weatherability, commanding premium pricing in architectural segments across rapidly urbanizing regions.

Adhesives and sealants use PTA-based polyols in structural bonding, while niche outlets such as pharmaceutical intermediates capture high-purity grades. Automotive adoption of foamed PET panels for battery housings and interior trim adds a new pull, albeit from a small base, supporting diversification of the purified terephthalic acid market across end-use sectors.

Geography Analysis

Asia-Pacific retained 53.62% share of global PTA consumption in 2024 and is set to grow 7.18% annually, reflecting integrated aromatics-to-polyester investments in China and India. China’s record 14.8 million barrels per day crude throughput enables ample PX feed, while Sinopec’s 3 million-ton single-train PTA plant in Jiangsu epitomizes economies of scale. India is emerging as a balancing supplier; IndianOil’s expansions at Panipat and Paradip will lift national PTA output by 1.35 million tons before mid-2026. South Korea and Japan focus on high-value resins and process licensing, whereas Southeast Asian producers exploit proximity to feedstock sources and burgeoning domestic demand. These dynamics cement Asia-Pacific’s status as the engine room of the purified terephthalic acid market.

North America’s purified terephthalic acid market benefits from competitive natural-gas liquids feed and established recycling infrastructure. Demand from carbonated soft-drink giants and rising automotive PET usage maintain utilization rates, yet new grassroots capacity remains limited as investors favor debottlenecking and integration with paraxylene units. Europe confronts structural headwinds from high energy costs and tightened emissions schemes. Facility rationalizations, such as Indorama’s review of Rotterdam operations, signal a pivot toward specialty grades and recycled feedstock rather than green-field PTA additions. Anti-dumping duties on Asian PET imports offer temporary relief but do not offset the region’s feedstock disadvantage.

South America and the Middle East & Africa present emerging growth avenues. Brazil’s polyester chain draws attention from multinational players eyeing stakes in Braskem to secure domestic market access. In the Middle East, SABIC’s USD 6.4 billion Fujian complex and TotalEnergies’ USD 11 billion Amiral project illustrate a strategy to integrate refining, PX and PTA units, then channel output into high-growth Asian markets. These long-cycle investments will gradually widen the geographic footprint of the purified terephthalic acid market, balancing demand clusters against feedstock availability.

Competitive Landscape

The purified terephthalic acid market is moderately fragmented, with the top five producers holding 45–50% of global capacity. Key players are adopting vertical integration, downstream diversification, and geographic expansion to mitigate PX volatility. Innovations like Sinopec's Jiangsu line and SABIC's Fujian complex highlight efficiency and regional investment trends. In Europe, Indorama Ventures and LyondellBasell are optimizing portfolios, while advancements in bio-based and recycled PTA, such as Idemitsu Kosan's biomass supply chain, are gaining traction. Producers focusing on value-added PTA grades and digital optimization are positioned to meet Scope 3 emission targets and capture premium market segments.

Purified Terephthalic Acid Industry Leaders

Alpek S.A.B. de C.V.

China Petroleum & Chemical Corporation.

HENGLI PETROCHEMICAL ( DALIAN ) CHEMICAL CO., LTD.

Indorama Ventures Public Company Limited.

Reliance Industries Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Indian Oil Corporation Limited (IOCL) has announced an increase in the price of Purified Terephthalic Acid (PTA) in the domestic market of India, effective February 08, 2025. This price adjustment reflects the company's response to evolving market dynamics and cost factors impacting PTA production.

- December 2023: Idemitsu Kosan Co., Ltd., Oriental Petrochemical (Taiwan) Co., Ltd. ("OPTC"), and Marubeni Corporation announced plans to establish a supply chain for biomass-derived Purified Terephthalic Acid (PTA) in Taiwan, with production set to begin in 2024. Idemitsu Kosan will produce biomass Paraxylene (PX) from biomass naphtha, which OPTC will convert into biomass PTA.

Global Purified Terephthalic Acid Market Report Scope

Terephthalic Acid, chemically known as Benzene-1,4-dicarboxylic acid, is a condensation polymer and an essential industrial aromatic precursor for polyethylene terephthalate (PET). These other petrochemical derivatives find usage in diverse industries such as packaging, textile, etc. Crude terephthalic acid obtained from the oxidation reaction of p-xylene contains impurities such as 4-carboxy benzaldehyde and several colored polyaromatics. Hence, terephthalic acid is first subjected to purification before exploiting it as an intermediate in the petrochemical industry. The terephthalic acid market is segmented by derivative, application, and geography. By derivative, the market is segmented into polyethylene terephthalate (PET), polybutylene terephthalate (PBT), polytrimethylene terephthalate (PTT), and dimethyl terephthalate. By application, the market is segmented into packaging, fibers, paints and coatings, adhesives, and other applications. The report also covers the size and forecasts for the terephthalic acid market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done based on volume (kilo tons).

| Polyethylene Terephthalate (PET) |

| Polybutylene Terephthalate (PBT) |

| Polytrimethylene Terephthalate (PTT) |

| Dimethyl Terephthalate (DMT) |

| PX Oxidation (Conventional) |

| Bio-based PTA |

| Chemical Recycling-based PTA |

| Packaging |

| Fibers |

| Paints and Coatings |

| Adhesives |

| Other Applications (Engineering Plastics, Pharmaceuticals and Intermediates, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Derivative | Polyethylene Terephthalate (PET) | |

| Polybutylene Terephthalate (PBT) | ||

| Polytrimethylene Terephthalate (PTT) | ||

| Dimethyl Terephthalate (DMT) | ||

| By Technology | PX Oxidation (Conventional) | |

| Bio-based PTA | ||

| Chemical Recycling-based PTA | ||

| By Application | Packaging | |

| Fibers | ||

| Paints and Coatings | ||

| Adhesives | ||

| Other Applications (Engineering Plastics, Pharmaceuticals and Intermediates, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Terephthalic Acid Market size?

The purified terephthalic acid market size reached 93.45 million tons in 2025 and is forecast to rise to 122.14 million tons by 2030 at a 5.5% CAGR.

Which region leads global demand?

Asia-Pacific dominates with 53.62% of global volume in 2024, supported by large integrated complexes and steady downstream consumption.

What share does packaging hold within PTA applications?

Packaging accounted for 46.29% of PTA demand in 2024 and is advancing at 6.28% annually due to e-commerce and lightweighting trends.

How will EU recycling mandates influence PTA demand?

EU rules requiring 30% recycled content in PET bottles by 2030 are accelerating investment in chemical recycling, creating premium demand for recycled-origin PTA.