Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 37.94 Billion |

| Market Size (2031) | USD 113.22 Billion |

| Growth Rate (2026 - 2031) | 24.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Telehealth Services Market Analysis by Mordor Intelligence

The Europe Telehealth Services Market size is estimated at USD 37.94 billion in 2026, and is expected to reach USD 113.22 billion by 2031, at a CAGR of 24.44% during the forecast period (2026-2031).

This growth reflects the continent’s shift from episodic, facility-based encounters to data-rich remote monitoring, which keeps patients connected to clinicians between visits. Germany leads current revenue because statutory insurers integrated teleconsultation into standard benefits, while Italy’s hospital-at-home pilots foreshadow the next wave of demand. Cloud infrastructure, smartphone saturation, and impending interoperability mandates lower technical barriers, and demographic pressure from an aging population further cements telehealth’s role in chronic-care management. Competitive dynamics now favor platforms that integrate into existing clinical workflows and can finance compliance with the European Union’s AI Act, which takes full effect in 2027.

Key Report Takeaways

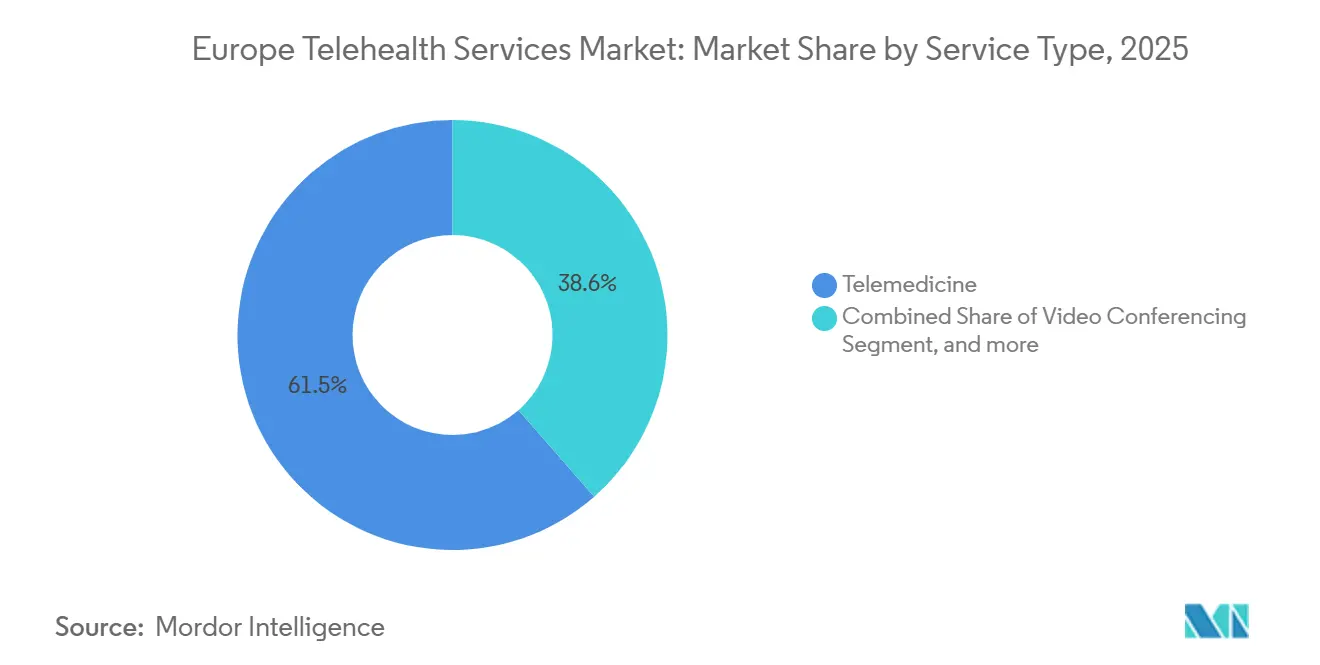

- By service type, telemedicine led with a 61.45% revenue share of the European telehealth service market in 2025, while remote patient monitoring is forecast to expand at a 26.75% CAGR through 2031.

- By application, tele-consultation accounted for 21.43% of the Europe telehealth service market size in 2025; tele-psychiatry is advancing at a 27.45% CAGR to 2031.

- By end user, providers held a 55.34% share of the European telehealth service market in 2025, whereas the patient segment is growing at a 27.32% CAGR.

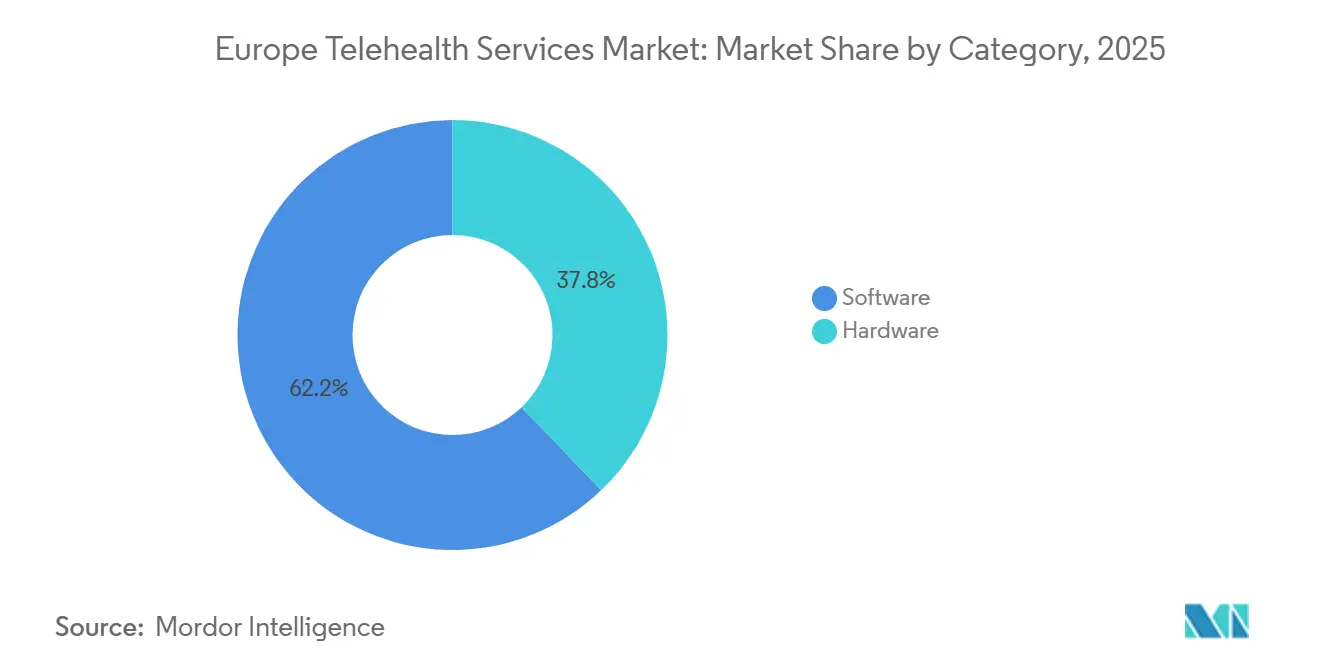

- By category, software captured 62.16% of the European telehealth service market share in 2025 and continues to post the highest 26.54% CAGR.

- By delivery mode, cloud-based platforms commanded 51.45% of revenue in 2025 and are forecast to rise at 26.87% CAGR.

- By geography, Germany contributed 28.54% of regional revenue in 2025; Italy shows the fastest growth rate of 25.65% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Telehealth Services Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Chronic Disease Burden | +6.2% | Pan-European, acute in Germany, Italy, Spain | Long term (≥ 4 years) |

| Post-COVID Reimbursement Reforms | +5.8% | France, Germany, UK; uneven in Southern & Eastern Europe | Medium term (2-4 years) |

| High Smartphone & Broadband Penetration | +3.1% | Northern & Western Europe; lagging in rural Southern Europe | Short term (≤ 2 years) |

| PSTN Switch-Off and IP Migration | +2.4% | UK-centric, spillover to Ireland, Netherlands | Medium term (2-4 years) |

| EU Digital Health Data Space | +3.9% | Pan-European, early gains in Benelux, Nordics | Long term (≥ 4 years) |

| AI-Driven Clinical Decision Support | +4.1% | Germany, France, UK; pilot stage in Southern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Chronic Disease Burden Escalating Demand for Remote Care

Citizens aged 65 and above represented 21% of Europe’s population in 2023, and projections indicate that the cohort will reach 30% by 2050, with concentrations in Germany, Italy, and Spain. Chronic illnesses already account for 70%–80% of health budgets, and telehealth reduces the need for frequent travel by shifting routine monitoring to patients’ homes. A 2024 WHO tool listed 15 European countries that have embedded telemedicine into their national strategies, underlining policy alignment with demographic realities. Hospital-at-home models, which cut inpatient costs by up to 30%, rely on continuous vital-sign feeds that the Europe telehealth service market now readily supplies. These factors combine to fuel remote monitoring’s status as the fastest-growing service type.

Post-COVID Regulatory Reimbursement Reforms Enabling Teleconsultations

Temporary pandemic measures have become permanent: France now reimburses video visits for established patients, Germany removed prior authorization for remote encounters in 2024, and the UK scaled virtual wards within the National Health Service[1]NHS England, “Virtual wards: Delivering hospital care at home,” england.nhs.uk. Southern Europe remains patchy, but the formal inclusion of teleconsultation codes into fee schedules anchors revenue visibility, inviting platform investment. Divergent fee levels still temper uptake among specialists who rely on procedure-based income. Nonetheless, standardized billing in core markets establishes a foundation for the broader Europe telehealth service market to mature.

High Smartphone & Broadband Penetration Supporting Video Visits

Smartphone penetration is expected to exceed 80% in Germany, France, and the UK by 2024, and 5G will blanket most urban areas, enabling clinician-grade video quality. The 2025 Gigabit Infrastructure Act now obliges member states to extend gigabit coverage to every household by 2030, prioritizing rural zones where specialist scarcity is acute[2]European Commission, “Gigabit Infrastructure Act,” digital-strategy.ec.europa.eu. Familiarity with consumer video apps lowers onboarding friction, accelerating adoption. However, bandwidth gaps in rural Spain, Italy, and Eastern Europe still favor store-and-forward workflows until backhaul upgrades are complete.

PSTN Switch-Off Catalyzing Migration To IP-Based Remote Monitoring Platforms

Ofcom delayed the UK copper network sunset to January 2027 after finding 1.7 million vulnerable residents still depend on analog alarms[3]Ofcom, “Protecting vulnerable consumers during the PSTN switch-off,” ofcom.org.uk. Vendors must now retrofit devices with cellular modules, triggering a replacement wave that benefits IP-native monitoring suppliers capable of streaming real-time vitals instead of simple alarms. Similar transitions loom in Ireland and the Netherlands, enlarging the addressable equipment pool for the Europe telehealth service industry.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented National Reimbursement Frameworks | -4.3% | Pan-European, acute in Southern & Eastern Europe | Medium term (2-4 years) |

| Data Privacy & GDPR Compliance Costs | -2.1% | Pan-European, enforcement concentrated in Germany, France | Short term (≤ 2 years) |

| Looming EU AI Act Certification Complexity | -3.2% | Germany, France, Benelux; pilot stage elsewhere | Medium term (2-4 years) |

| Telehealth Workforce Shortages | -2.8% | UK, Germany, France; spillover to Southern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented National Reimbursement Frameworks Limiting Cross-Border Scaling

Even with shared data rails, payment rules remain local. France underpays video visits relative to in-person care, Germany links reimbursement to diagnosis codes, and Spain’s 17 regions apply separate criteria. Remote monitoring, which requires continuous billing, suffers most. The absence of mutual recognition forces platforms to tailor products market by market, hampering economies of scale and slowing the wider Europe telehealth service market.

Data Privacy & GDPR Compliance Costs Burdening Small Providers

Platforms must secure explicit patient consent, maintain data-processing registers, and appoint data-protection officers. Fines can reach 4% of global revenue, discouraging smaller entrants that cannot amortize compliance overhead. Germany and France levy the highest penalties, prompting some startups to confine launches to less stringent jurisdictions, narrowing competitive diversity inside the Europe telehealth service market.

Segment Analysis

By Service Type: Remote Monitoring Outpaces Episodic Consultations

Remote patient monitoring is projected to expand at a 26.75% CAGR, eclipsing all other modalities, while telemedicine still generated 61.45% of 2025 revenue for the Europe telehealth service market. The combination of continuous vital sign capture and algorithmic alerts enables clinicians to intervene early, reducing hospitalization costs by up to 30%. Hospital-at-home programs anchor payer willingness to reimburse long-term monitoring, thus crystallizing a durable revenue stream.

Telemedicine’s video and phone visits remain indispensable for initial assessment and follow-up. Consumer familiarity with mainstream video apps eases adoption, but reimbursement ceilings temper growth in specialist care. Store-and-forward services, such as tele-dermatology, thrive where broadband is weak, while asynchronous chat attracts younger users who value convenience. The PSTN sunset compels legacy alarm vendors to re-engineer their devices, unlocking a new installed base for platforms that integrate both monitoring and consulting functionality.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Mental Health Drives Fastest Expansion

Tele-psychiatry is advancing at a 27.45% CAGR, propelled by a lingering post-pandemic mental-health backlog and a limited psychiatric workforce. Chat-based sessions skirt AI Act high-risk rules, easing compliance hurdles and catering to patients who prefer text-based interactions over video. Tele-consultation, by contrast, retained 21.43% of the Europe telehealth service market size in 2025 because it spans broad primary-care use cases.

Cardiology follows as remote ECG and rehabilitation protocols achieve insurer acceptance, buttressed by professional guidelines that codify monitoring thresholds. Pathology and radiology utilize asynchronous uploads, but concerns about malpractice and uneven reimbursement slow growth. The WHO’s 2024 support tool endorses mental health and chronic disease management as top telehealth value areas, reinforcing the focus on investment.

By End User: Patients Gain Ground on Providers

Providers generated 55.34% of 2025 revenue; however, the patient segment is forecast to increase by 27.32% annually as direct-to-consumer models proliferate. Mobile apps that sell on-demand care bypass gatekeeper referrals, satisfying users who prize speed and privacy. Payers grow more slowly, leveraging telehealth to trim claims rather than generate revenue.

Integration into electronic health record systems solidifies provider loyalty, whereas patients primarily judge brands based on their interface and price. The European Health Data Space provides patients with formal control over their records, making platform switching easier once the technical rollout is complete. Nonetheless, specialist access still often requires general-practitioner referral, capping the direct-to-consumer ceiling until policy liberalizes.

By Category: Software Dominates Hardware

Software secured 62.16% of revenue and posted the highest 26.54% CAGR, confirming a shift toward subscription billing and rapid cloud updates. Hardware, including wearables and diagnostic peripherals, remains essential but is increasingly commoditized. IP migration in the UK sparks a one-time hardware replacement wave, yet long-term value accrues to platforms that interpret data rather than merely collect it.

Analytics modules predict exacerbations, allowing case managers to triage resources. Conversely, the Medical Device Regulation elevates documentation burdens on hardware firms, consolidating supply among larger manufacturers. Open Bluetooth standards further erode brand lock-in, favoring ecosystem-agnostic devices.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Delivery Mode: Cloud Infrastructure Enables Scalability

Cloud deployment captured 51.45% of 2025 revenue and is rising at 26.87% CAGR as providers trade capital expenditure for subscription fees. Mobile-first design appeals to younger clinicians and patients, while web-only offerings are losing favor due to their limited offline capabilities. On-premise systems persist in research hospitals that demand direct data access but represent a shrinking niche.

Cloud providers now meet ISO 27001 and GDPR requirements via EU-based data centers, placating sovereignty concerns. The European Health Data Space relies on API interoperability that cloud vendors can deliver through routine updates, whereas on-premise installations need manual patches, slowing compliance. Germany’s cybersecurity agency published 2025 guidance affirming the feasibility of cloud services, further tipping the balance.

Geography Analysis

Germany generated 28.54% of regional revenue in 2025 as statutory insurers adopted direct billing for teleconsultation and agreed on flat-rate hospital-at-home payments. The United Kingdom scaled virtual wards after 2024 pilots cut inpatient costs by up to 30%. France reimburses video visits at rates below those for in-person visits, making telehealth attractive primarily for general practitioners rather than procedure-driven specialists.

Italy is the fastest-growing geography, with a 25.65% CAGR, thanks to regional hospital-at-home deployments that alleviate rural physician shortages. Spain’s 17 autonomous communities create reimbursement heterogeneity, fragmenting the potential user base. Nordic and Benelux states leverage mature digital identities and prior cross-border agreements to test pan-European consultations, while Poland and Romania lag behind due to weaker broadband infrastructure.

The Gigabit Infrastructure Act mandates gigabit connectivity for every household by 2030, aiming to erase rural bandwidth disparities that currently limit the European telehealth service market. Meanwhile, the UK-EU data adequacy decision preserves lawful data flows post-Brexit, sustaining bilateral telehealth activity.

Competitive Landscape

Competition is moderate, with no single model dominant. Large multispecialty platforms rely on physician density and integrated booking systems to secure providers. Hospital-at-home players monetize continuous vitals that generate billable events, while direct-to-consumer brands compete through marketing and user experience. AI tooling differentiates leaders by boosting clinician throughput, but the EU AI Act’s certification costs favor capitalized incumbents.

The PSTN switch-off accelerates consolidation as smaller telecare operators struggle to finance device retrofits, opening acquisition opportunities for digital-native firms. Network effects intensify: more clinicians attract more patients, which in turn draws still more clinicians, creating regional winner-take-all outcomes. Nonetheless, workforce shortages and fragmented payment rules prevent outright monopoly, keeping the Europe telehealth service market competitively balanced.

Europe Telehealth Services Industry Leaders

AMD Global Telemedicines Inc

Kry

Doctolib

Immedicare

Babylon Health

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: The NHS plans to launch NHS Online, an ‘online hospital’ without a physical site, starting in 2027. The digital service will connect patients with expert clinicians across England, enabling faster care. Patients will be triaged via the NHS App and can book scans at local Community Diagnostic Centres.

- February 2025: a new telemedicine pilot project was launched in the district of Traunstein. The initiative, led by the Technical University of Munich (TUM), focuses on delivering quicker and more efficient medical care to nursing home residents through their primary care providers. The project aims to decrease unnecessary hospital admissions and enhance patient care in the region.

- August 2024: The European Union adopted the AI Act, classifying diagnostic algorithms as high-risk and introducing mandatory conformity assessments, audits, and public registration.

Europe Telehealth Services Market Report Scope

As per scope of the report, telehealth services refer to the delivery of healthcare remotely through digital communication technologies like video calls, phone consultations, and online platforms. They enable patients to receive medical advice, diagnosis, and follow-up care without needing to visit healthcare facilities. Telehealth improves access to healthcare, especially in remote or underserved areas.

The Europe Telehealth Service Market is Segmented by Service Type (Telemedicine, Video Conferencing, Remote Patient Monitoring, App-Based Consultation, and Other Service Types), Application (Tele-Consultation, Tele-Pathology, Patient Care, Tele-Psychiatry, Tele-Cardiology, and Other Applications), End User (Providers, Patients, Payers), Category (Hardware and Software), Delivery Mode (Cloud-Based, Web-Based, and On-Premise), and Geography (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe). The report offers the value (in USD million) for the above segments.

By Service Type

| Telemedicine |

| Video Conferencing |

| Remote Patient Monitoring |

| App-Based Consultation |

| Other Service Types |

By Application

| Tele-Consultation |

| Tele-Pathology |

| Patient Care |

| Tele-Psychiatry |

| Tele-Cardiology |

| Other Applications |

By End User

| Providers |

| Patients |

| Payers |

By Category

| Hardware |

| Software |

By Delivery Mode

| Cloud-Based |

| Web-Based |

| On-Premise |

Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Service Type | Telemedicine |

| Video Conferencing | |

| Remote Patient Monitoring | |

| App-Based Consultation | |

| Other Service Types | |

| By Application | Tele-Consultation |

| Tele-Pathology | |

| Patient Care | |

| Tele-Psychiatry | |

| Tele-Cardiology | |

| Other Applications | |

| By End User | Providers |

| Patients | |

| Payers | |

| By Category | Hardware |

| Software | |

| By Delivery Mode | Cloud-Based |

| Web-Based | |

| On-Premise | |

| Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the forecast value of the Europe telehealth service market in 2031?

The Europe telehealth service market is projected to reach USD 113.22 billion by 2031.

Which service type is expanding fastest across the region?

Remote patient monitoring shows the highest trajectory, rising at a 26.75% CAGR through 2031.

Why is tele-psychiatry growing so quickly?

A sustained post-pandemic mental-health backlog and limited psychiatric workforce push demand, leading tele-psychiatry to grow at 27.45% CAGR.

Which country currently holds the largest revenue share?

Germany leads with 28.54% of regional revenue thanks to insurer reimbursement that embeds teleconsultation into routine care.

How will the EU AI Act affect telehealth vendors?

Diagnostic AI tools must undergo costly audits and certification by 2027, favoring well-capitalized platforms and likely accelerating market consolidation.

What infrastructure development will most influence rural telehealth adoption?

The Gigabit Infrastructure Act mandates gigabit-speed coverage for every household by 2030, reducing bandwidth constraints that currently limit rural uptake.