Telecom API Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

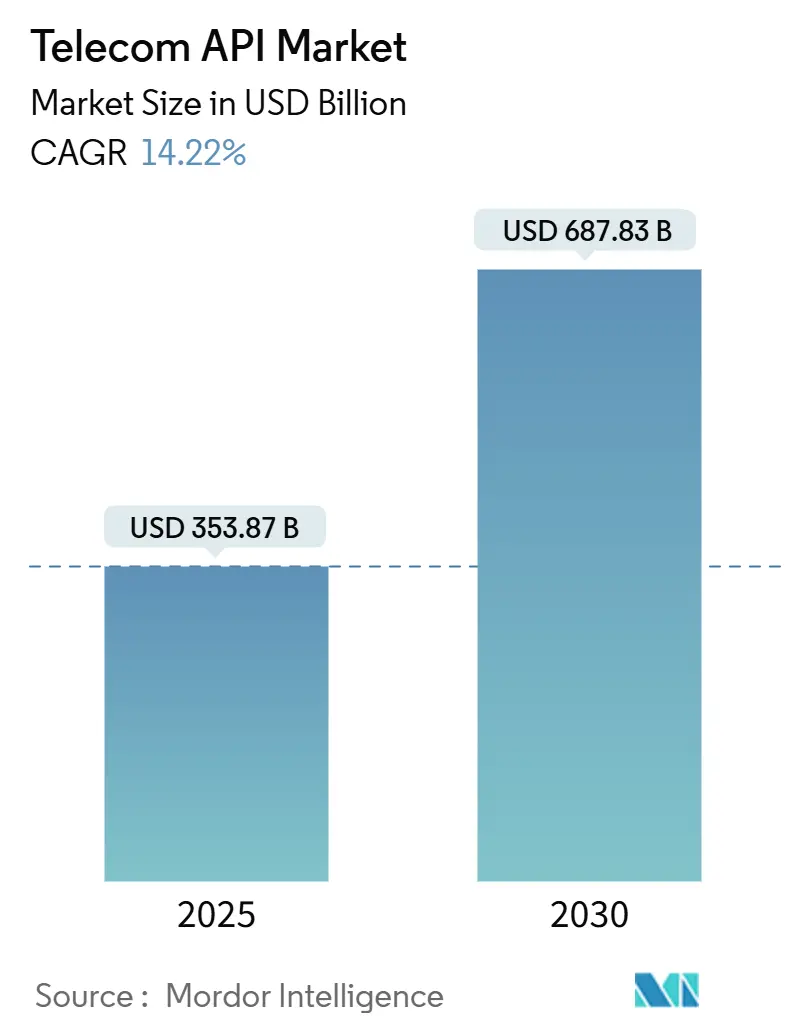

| Market Size (2025) | USD 353.87 Billion |

| Market Size (2030) | USD 687.83 Billion |

| Growth Rate (2025 - 2030) | 14.22% CAGR |

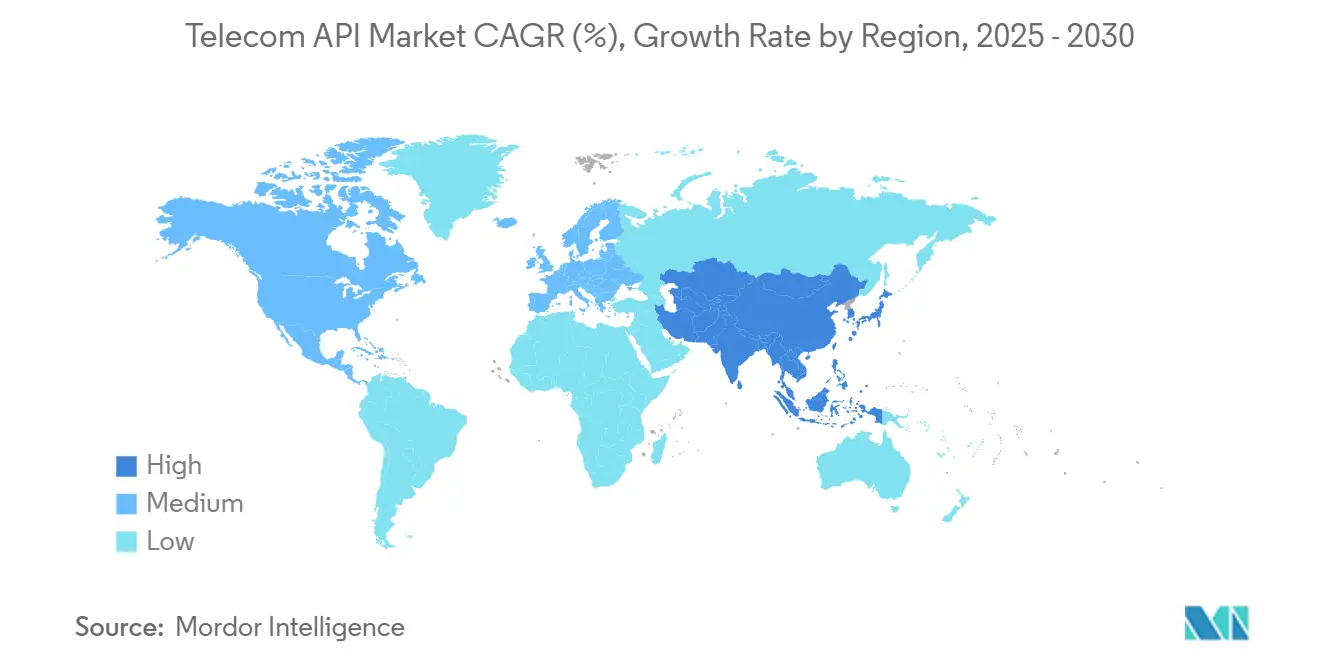

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Telecom API Market Analysis by Mordor Intelligence

The Telecom API Market size is estimated at USD 353.87 billion in 2025, and is expected to reach USD 687.83 billion by 2030, at a CAGR of 14.22% during the forecast period (2025-2030).

Uptake reflects the telecom sector’s pivot to programmable networks, monetization of 5G capabilities, and the rapid spread of Communications Platform as a Service (CPaaS). Key forces behind growth include standardization efforts such as GSMA Open Gateway, the proliferation of quality-on-demand APIs for 5G network slicing, and enterprise demand for embedded real-time communications. Competitive intensity has prompted consolidation: equipment vendors and carriers have formed joint ventures to pool network APIs, while CPaaS specialists scale through enterprise acquisition strategies. The market also benefits from hybrid cloud deployments that balance cloud agility with data-sovereignty requirements, positioning operators to quickly expose network functions to developer ecosystems.

Key Report Takeaways

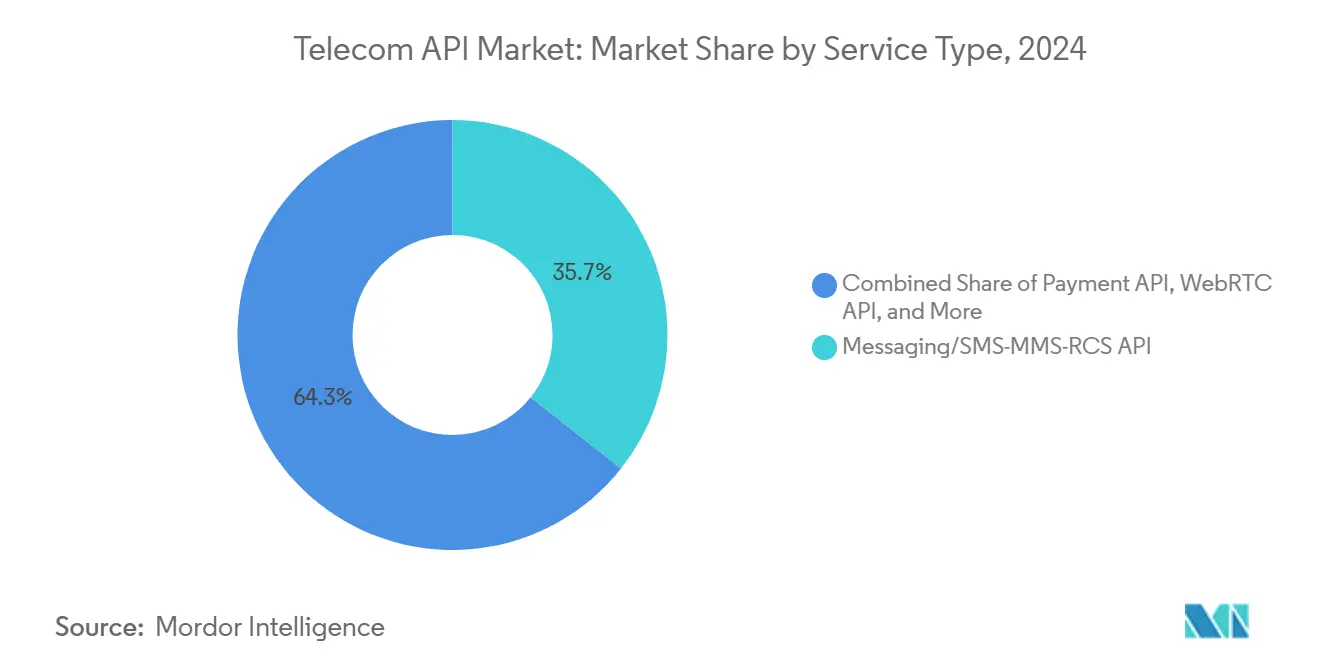

- By service type, Messaging APIs led with 35.67% revenue share in 2024; Payment APIs are projected to expand at a 17.45% CAGR through 2030.

- By deployment type, hybrid cloud captured 49.85% of the Telecom API market share in 2024 and is forecast to grow at 15.45% CAGR to 2030.

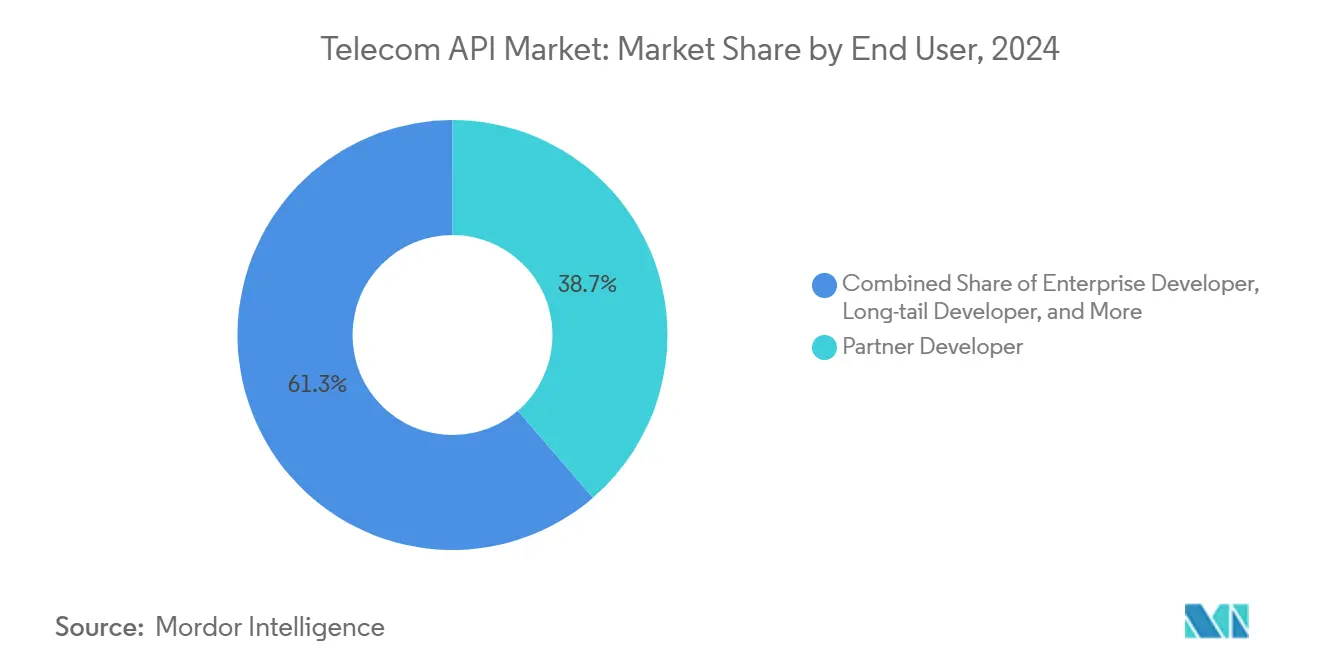

- By end user, Partner Developers commanded 38.66% share of the Telecom API market size in 2024, whereas Enterprise Developers exhibit the fastest CAGR of 15.11%.

- By business model, Aggregator-led CPaaS commanded 39.85% share of the Telecom API market size in 2024, whereas Direct Carrier Exposure is projected to grow at a 17.81% CAGR to 2030.

Global Telecom API Market Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in CPaaS adoption among enterprises | +3.20% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Open Gateway & CAMARA standardization of network APIs | +2.80% | Global, with APAC and Europe early adopters | Long term (≥ 4 years) |

| Monetization pressure on 5G driving QoS-on-demand APIs | +2.10% | Global, concentrated in 5G-mature markets | Medium term (2-4 years) |

| Edge-computing workloads need low-latency slicing APIs | +1.90% | North America, Europe, APAC core markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in CPaaS adoption among enterprises

Enterprises continue embedding omnichannel communications into customer workflows, illustrated by Twilio’s Q1 2025 revenue of USD 1.17 billion and an active customer base exceeding 335,000. Operators improve internal efficiency as well: AT&T’s MuleSoft-centered program cut onboarding cycles from one year to six weeks and saved 2 million work hours annually. The economic payoff from API reuse reinforces management's focus on developer experience and continuous integration pipelines. Generative-AI-powered coding assistants lower entry barriers for in-house teams, and personalized messaging fuels sustained traffic on SMS, RCS, and voice channels.

Open Gateway and CAMARA standardization of network APIs

Forty-nine operator groups now back GSMA Open Gateway, signaling an industry consensus on unified interfaces for capabilities such as device verification, latency control, and location services. Telefónica’s commercial launch shows developers integrating telecom features into fintech and streaming apps while retaining privacy controls[1]Telefónica, “Telefónica Demonstrates Open Gateway Commercial Use Cases,” telefonica.com. T-Mobile’s CAMARA-compliant Quality-on-Demand APIs enable low-latency deployments in healthcare, logistics, and retail. Standardization lowers integration costs for software firms and accelerates time-to-market for network-aware applications.

Monetization pressure on 5G driving QoS-on-demand APIs

Operators seek fresh revenue streams to offset USD 1 trillion of cumulative 5G capex since 2018[2]Mobile World Live, “Operators Eye New 5G APIs for Monetization,” mobileworldlive.com. Trials by Ericsson and Telefónica show on-demand slicing that lets enterprises pay for guaranteed performance during live broadcasts and mission-critical events. Analysts forecast USD 100-300 billion in potential operator revenue from network APIs within seven years, shifting the value proposition from connectivity to programmable QoS services.

Edge-computing workloads need low-latency slicing APIs

Industries deploying autonomous vehicles, AR/VR, and smart-factory controls require sub-10 millisecond response times. Demonstrations from Ericsson, Intel, and Microsoft proved slice selection on Windows laptops, pointing to a USD 300 billion enterprise network-slicing opportunity by 2025. Operators leveraging Multi-Access Edge Computing can guarantee deterministic connectivity for safety-critical IoT, reinforcing their role in Industry 4.0 supply chains.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating API-security breaches & signaling fraud | -2.40% | Global, with North America and Europe most affected | Short term (≤ 2 years) |

| Legacy OSS/BSS upgrade bottlenecks | -1.80% | Global, with mature markets facing greater challenges | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating API-security breaches and signaling fraud

API call volumes leapt 167% in 2024, exposing platforms to attack vectors that resulted in breaches at Dell, GitHub, and TracFone, the latter paying USD 16 million in penalties. Research shows 95% of organizations faced API security incidents, with 23% suffering data loss. Telecom players remain high-value targets because subscriber identity and signaling systems traverse multiple domains. Effective mitigations include zero-trust policies, continuous runtime protection, and threat-intelligence sharing between carriers and cloud providers.

Legacy OSS/BSS upgrade bottlenecks

Two-thirds of communication service providers cite technical debt in decades-old billing and operations platforms as a barrier to API monetization. Rigid on-premises stacks cannot support event-based charging or consumption-based pricing that APIs demand. Cloud-native BSS migrations deliver long-term agility but involve multi-year programs featuring process re-engineering and workforce reskilling, delaying full benefits and constraining first-mover advantage in the Telecom API market.

Segment Analysis

By Service Type: Messaging APIs power digital engagement

Messaging APIs retained 35.67% Telecom API market share in 2024, anchored by enterprise A2P traffic that reached 2.2 trillion messages. The Telecom API market size for messaging is forecast to expand steadily as businesses prioritize SMS, MMS, and Rich Communication Services for authentication and promotions. RCS growth is striking: Infobip projects A2P RCS revenue climbing to USD 4.2 billion by 2029. Meanwhile, Payment APIs are scaling fastest at 17.45% CAGR because embedded finance models blend telecom reach with fintech capabilities. Voice, IVR, and WebRTC APIs retain relevance as enterprises integrate multi-modal support into customer-experience platforms. Developers also leverage subscriber-identity and fraud-detection APIs to boost security for mobile transactions.

Demand patterns continue shifting toward value-added functionality. Generative-AI chatbots drive contextual messaging, and location-based APIs enable hyperlocal marketing in smart-city rollouts. As regulation tightens against spam, operators charge premiums for verified sender IDs, reinforcing revenue diversification. Close collaboration with cloud contact-center vendors keeps messaging APIs central to enterprise transformation agendas across healthcare, banking, and retail.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Type: Hybrid architectures dominate strategic roadmaps

Hybrid environments captured 49.85% market share in 2024 and delivered the highest growth trajectory at 15.45% CAGR, underscoring operator priorities around sovereignty and latency. Telecom API market size for hybrid deployments is projected to expand as network cores stay on-premises while microservices for billing, analytics, and exposure layers move to public cloud[3]Telecom Review, “VIVA Bahrain Launches First Hybrid Cloud Core,” telecomreview.com. Operator examples include VIVA Bahrain’s hybrid cloud core and PCCW Global’s multi-cloud strategy for wholesale APIs. Regulatory mandates for local data storage in APAC further sustain hybrid uptake.

Operators favor cloud-agnostic container orchestration to avoid vendor lock-in and to dynamically shift workloads for cost optimization. Edge nodes extend hybrid topologies, offering developers single-digit-millisecond latency for AI inference and computer-vision tasks. Pure public-cloud models remain suitable for greenfield MVNOs, but integration complexity and unpredictable egress fees limit broad adoption for tier-one operators. On-premises-only strategies persist for security-sensitive government networks yet lack the elasticity required for large-scale API economies.

By End User: Partner developers anchor ecosystem scale

Partner Developers represented 38.66% share in 2024, confirming that external innovators create much of the value in the Telecom API market. Operator developer portals, hackathons, and revenue-sharing programs foster vibrant ecosystems where start-ups test concepts such as AR tourism guides and digital-identity verifiers. Enterprise Developers contribute the fastest-growing slice with a 15.11% CAGR, driven by digital-transformation roadmaps that embed telecom functions directly in supply-chain, banking, and field-service applications. Telecom API market size for enterprise integrations will accelerate further as low-code tooling and AI code assistants democratize API use.

In parallel, Internal Developer teams modernize self-service channels and network-management tools, while Long-tail Developers capitalize on simplified onboarding processes. Successful operator programs showcase transparent pricing, sandbox environments, and usage analytics that help partners monetize at lower risk. The interplay among developer segments ensures a balanced pipeline of innovation while diversifying operator revenue beyond traditional voice and data.

Note: Segment shares of all individual segments available upon report purchase

By Business Model: Direct Carrier Exposure Drives Innovation

Direct Carrier Exposure emerges as the fastest-growing business model at 17.81% CAGR through 2030, reflecting telecommunications operators' strategic shift toward direct API monetization and reduced dependency on third-party aggregators. This acceleration demonstrates operators' increasing confidence in their ability to manage developer relationships and API ecosystems independently, driven by standardization initiatives like GSMA Open Gateway and CAMARA that simplify direct integration processes. Aggregator-led CPaaS maintains the largest market share at 39.85% in 2024, benefiting from established developer communities and comprehensive platform capabilities that reduce integration complexity for enterprises. Platform-as-a-Service models continue serving specialized use cases where organizations require greater control over their communication infrastructure, while API Marketplace and Exchange models gain traction as neutral venues for multi-operator API discovery and consumption.

Telecom operators are rethinking their business models, placing greater emphasis on building direct relationships with developers to drive long-term revenue growth. A clear example of this shift is Ericsson's Aduna initiative, which brings together 12 major operators. This partnership helps operators offer standardized APIs collectively while still maintaining their brand connections with developers. Google Cloud's marketplace syndication strategy for network APIs highlights how technology providers make it easier for carriers to connect directly with their customers. By offering the necessary platform infrastructure, they allow operators to focus on maintaining strong customer relationships. The competition between aggregator-led models and direct carrier exposure is heating up. Operators are striving to get more value from their network investments, while developers are looking for easier ways to integrate with multiple carrier networks.

Geography Analysis

North America accounted for 34.06% of 2024 revenue, reflecting high CPaaS penetration and extensive 5G coverage. Collaboration among AT&T, T-Mobile, and Verizon in the Aduna venture allows unified access to Number Verification and SIM Swap APIs that raise security for fintech and healthcare applications. Twilio’s USD 4.46 billion 2024 revenue underscores robust enterprise spending on programmable communications, while developer-first cultures spur quick uptake of new network features. Government frameworks that encourage technology sandboxes support continuous experimentation in the Telecom API market.

Asia-Pacific is forecast to register the fastest 17.51% CAGR through 2030 as mobile-first economies escalate 5G rollouts and digital-services adoption. Combined regional telco revenue hit USD 147.7 billion in Q2 2024, with 72% of operators reporting positive growth. China’s projected 88% 5G subscription rate by 2028 and initiatives in Australia, Japan, and South Korea to expose quality-on-demand APIs illustrate aggressive expansion. Government mandates for smart manufacturing and e-governance increase demand for low-latency and security features, making the Telecom API market the backbone of regional digital agendas.

Europe shows steady growth because GDPR-aligned security practices elevate customer trust in API services. Deutsche Telekom’s AI-phone roadmap demonstrates regional operator interest in converging devices, AI, and telecom capabilities. Collaborative projects among European carriers and hyperscalers accelerate edge deployments and standardized CAMARA APIs. Emerging markets in the Middle East, Africa, and Latin America ride similar trajectories, backed by network-modernization investments and cloud-partnership strategies that lower time-to-market for digital-service launches.

Competitive Landscape

Innovation and Integration Drive Market Success

The Telecom API market is moderately fragmented yet trending toward consolidation. Nokia’s purchase of Rapid APIs’ assets for less than EUR 100 million and Ericsson’s USD 6.2 billion Vonage deal (followed by a USD 3 billion impairment) illustrate equipment vendors’ shift to software-centric revenue. The Aduna joint venture unites 12 operators with roughly 50% equity stake, pooling standardized network APIs and presenting a counterweight to over-the-top CPaaS giants. Pure-play CPaaS providers such as Infobip, Sinch, and Vonage scale by embedding AI analytics and omnichannel orchestration into their platforms.

White-space opportunities have sparked entry by fintech, automotive, and cloud gaming players, all leveraging network slicing and location APIs. Start-ups equipped with low-code toolchains further democratize API creation, forcing incumbents to prioritize developer-experience enhancements and security certifications. Hyperscalers supply infrastructure and ML capabilities, yet revenue-share negotiations remain contentious as carriers protect core-service margins. Regulatory bodies push interoperability mandates to avoid ecosystem lock-in, which encourages joint ventures and alliances over outright acquisitions.

Operators now integrate AI-driven observability and threat detection across API gateways to mitigate rising security incidents. Feature differentiation increasingly rests on quality guarantees, real-time analytics, and edge-compute integration rather than simply exposing connectivity. Market leaders invest in regional data centers, sovereign-cloud options, and zero-trust frameworks to satisfy enterprise compliance requirements.

Telecom API Industry Leaders

-

AT&T Inc.

-

Telefónica SA

-

Twilio Inc.

-

Infobip Ltd

-

Sinch (CLX Communication)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Ericsson’s Aduna venture appointed Anthony Bartolo as CEO to drive global API commercialization efforts.

- February 2025: AT&T, T-Mobile, and Verizon collaborated with Aduna to launch standardized 5G Network APIs in the United States, including Number Verification and SIM Swap functionality.

- January 2025: Aduna and Bridge Alliance formed a partnership to extend CAMARA-compliant network APIs across Asia-Pacific markets, connecting Google Cloud, Infobip, Sinch, and Vonage to regional carrier networks.

- November 2024: Nokia finalized the acquisition of Rapid’s API assets, integrating them into its Network as Code platform to enhance lifecycle management.

Global Telecom API Market Report Scope

Telecom API is a set of standard software functions that an application can utilize to operate the networking architecture. The API bridges the combination between the application and the resources across the device. Telecom APIs are the medium for accessing telecom services and data for multiple communication-enabled applications. Telecom providers are leveraging APIs to create differentiated offerings. APIs enable providers to combine their services and systems with third parties, opening up more rapid partnership opportunities that produce innovative, high-quality services. The telecom API market is segmented by type of service (messaging API, IVR/voice store and voice control API, payment API, webrtc [real-time connection] API, location and map API, subscriber identity management and SSP API, and other types of services), deployment type (hybrid, multi-cloud, and other deployment types), end user (enterprise developer, internal telecom developer, partner developer, long tail developer), geography (North America, Europe, Asia-Pacific [China, South Korea, Australia, New Zealand, India, Thailand, Singapore, Malaysia, Rest of Asia-Pacific], Latin America, and Middle East and Africa). The impact of macroeconomic trends on the market is also covered under the scope of the study. Further, factors affecting the market's evolution in the near future, such as drivers and constraints, have been covered in the study. The market sizes and predictions are provided in terms of value (USD) for all the above segments.

| Messaging/SMS-MMS-RCS API |

| Voice/IVR and Voice Control API |

| Payment API |

| WebRTC API |

| Location and Mapping API |

| Subscriber ID Mgmt and SSO API |

| Other Services |

| Hybrid |

| Multi-cloud |

| Other Deployment Modes |

| Enterprise Developer |

| Internal Telecom Developer |

| Partner Developer |

| Long-tail Developer |

| Direct Carrier Exposure |

| Aggregator-led CPaaS |

| Platform-as-a-Service (PaaS) |

| API Marketplace/Exchange |

| North America |

| South America |

| Europe |

| Asia Pacific |

| Middle East and Africa |

| By Service Type | Messaging/SMS-MMS-RCS API |

| Voice/IVR and Voice Control API | |

| Payment API | |

| WebRTC API | |

| Location and Mapping API | |

| Subscriber ID Mgmt and SSO API | |

| Other Services | |

| By Deployment Type | Hybrid |

| Multi-cloud | |

| Other Deployment Modes | |

| By End-User | Enterprise Developer |

| Internal Telecom Developer | |

| Partner Developer | |

| Long-tail Developer | |

| By Business Model | Direct Carrier Exposure |

| Aggregator-led CPaaS | |

| Platform-as-a-Service (PaaS) | |

| API Marketplace/Exchange | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

What is the current size of the Telecom API market?

The Telecom API market is valued at USD 353.87 billion in 2025 and is projected to nearly double to USD 687.83 billion by 2030.

Which service segment holds the largest Telecom API market share?

Messaging APIs lead with 35.67% market share owing to the massive volume of enterprise A2P traffic.

Why are hybrid deployments favored in Telecom API platforms?

Hybrid-cloud architecture combines on-premises control of sensitive network functions with public-cloud scalability, capturing 49.85% share and the fastest growth rate.

Which region will grow fastest through 2030?

Asia-Pacific is forecast to post a 17.51% CAGR due to aggressive 5G rollouts and supportive government digital agendas.

How are operators monetizing 5G investments through APIs?

Quality-on-demand and network-slicing APIs allow enterprises to pay for guaranteed performance levels, turning network capabilities into billable services.

What are the main risks facing the Telecom API industry?

Escalating API-security breaches and legacy OSS/BSS constraints can erode margins and slow new-service launches if left unaddressed.

Page last updated on: