| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 186.48 Billion |

| Market Size (2030) | USD 274.13 Billion |

| CAGR (2025 - 2030) | 8.01 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Market Size")

System On Chip Market Analysis

The System On Chip Market size is estimated at USD 186.48 billion in 2025, and is expected to reach USD 274.13 billion by 2030, at a CAGR of 8.01% during the forecast period (2025-2030).

The semiconductor industry is experiencing unprecedented transformation driven by substantial government investments and policy initiatives aimed at strengthening domestic manufacturing capabilities. In the United States, the CHIPS and Science Act has catalyzed over USD 166 billion in manufacturing investments for semiconductors and electronics since its implementation. Similarly, the European Union has attracted over EUR 90 billion in semiconductor industry investments through the European Chips Act, demonstrating a global push toward establishing robust semiconductor manufacturing ecosystems. These initiatives reflect a broader trend of nations working to secure their semiconductor supply chains and reduce dependence on specific geographic regions for critical components.

The automotive sector's rapid evolution toward electrification is fundamentally reshaping semiconductor demand patterns, particularly in the System-on-Chip segment. While traditional gasoline-powered vehicles typically utilize between 50 to 150 semiconductor chips, electric vehicles can require up to 3,000 chips per vehicle, representing a massive increase in semiconductor content per vehicle. This transformation is driving unprecedented demand for sophisticated SoC solutions capable of managing complex power systems, advanced driver assistance features, and enhanced connectivity requirements in modern vehicles.

Industrial automation and robotics continue to drive significant demand for sophisticated SoC solutions across manufacturing sectors. In 2022, global industrial robot installations reached 553,052 units, with particularly strong adoption across Asia, Europe, and the Americas. This automation trend is creating new requirements for System-on-Chip technologies that can handle real-time processing, advanced sensing capabilities, and complex control systems while maintaining high reliability and performance standards in industrial environments.

The evolution of SoC architecture is witnessing a paradigm shift with the emergence of heterogeneous integration and 3D-IC technologies. Chip designers are moving beyond traditional Moore's Law scaling to explore innovative approaches for increasing transistor density and improving performance. This includes the vertical stacking of ICs and the integration of diverse components within a single package, enabling higher chip density and terabytes of bandwidth to meet the demands of next-generation intelligent devices. These architectural innovations are particularly crucial for applications requiring high-performance computing capabilities while maintaining power efficiency. The semiconductor system-on-chips industry is at the forefront of these advancements, driving the future of technology.

System On Chip Market Trends

Rising Adoption of Emerging Technologies like IoT and AI

The proliferation of Internet of Things (IoT) and artificial intelligence (AI) technologies is creating unprecedented demand for sophisticated SoC chip solutions. According to Ericsson's projections, IoT connections are expected to reach approximately 35 billion by 2028, with short-range IoT devices anticipated to grow from 10.3 billion in 2022 to 25 billion by 2027. This massive expansion of connected devices requires highly integrated, power-efficient computing solutions that can handle complex AI algorithms while maintaining minimal power consumption. The integration of AI capabilities into system-on-chip technologies enables devices to process data locally at the edge, reducing latency and improving real-time decision-making capabilities for applications ranging from smart home devices to industrial automation systems.

The convergence of IoT and AI is driving innovation in SoC chip design, with manufacturers developing specialized chips that combine multiple functionalities, including sensor interfaces, wireless connectivity, and AI accelerators. These advanced SoCs are essential for enabling features like predictive maintenance in industrial equipment, intelligent power management in smart buildings, and enhanced security in IoT devices. The demand for edge AI processing capabilities has led to the development of more sophisticated SoC architectures, as evidenced by recent innovations such as Silicon Labs' introduction of new integrated circuit families specifically designed for tiny IoT devices, featuring exceptional energy efficiency and wireless connectivity optimized for compact, battery-operated devices such as medical devices, wearables, and smart sensors.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Investments in 5G and Growing Demand for 5G Smartphones

The rapid deployment of 5G infrastructure and growing demand for 5G-enabled devices is driving significant innovation and investment in SoC chip development. According to Ericsson's latest mobility report, 5G mobile subscriptions are expected to surpass 1.5 billion globally by the end of 2023, creating substantial demand for advanced SoC solutions that can support high-speed data processing and efficient power management. This trend is catalyzing major industry collaborations, as evidenced by the July 2023 partnership between Intel and Ericsson to manufacture custom 5G SoCs using Intel's 18A process technology, aimed at creating highly differentiated products for future 5G infrastructure.

The increasing sophistication of 5G smartphones is driving the development of more advanced system-on-chip technologies that can handle complex processing requirements while maintaining power efficiency. This is reflected in recent industry developments, such as MediaTek's September 2023 announcement of its first system-on-chip using TSMC's 3nm technology, with volume production planned for 2024. Additionally, the April 2023 collaboration between Intel Foundry Services and Arm to enable mobile SoC designers to build their products on the Intel 18A process demonstrates the industry's commitment to advancing 5G smartphone capabilities. These developments are particularly significant as smartphone subscriptions are projected to grow from 6.4 billion in 2022 to exceed 7.7 billion by 2028, indicating sustained demand for advanced SoC solutions in mobile devices. The smartphone SoC market share is expected to grow as these technologies evolve, further influencing the mobile SoC market.

Segment Analysis: By Type

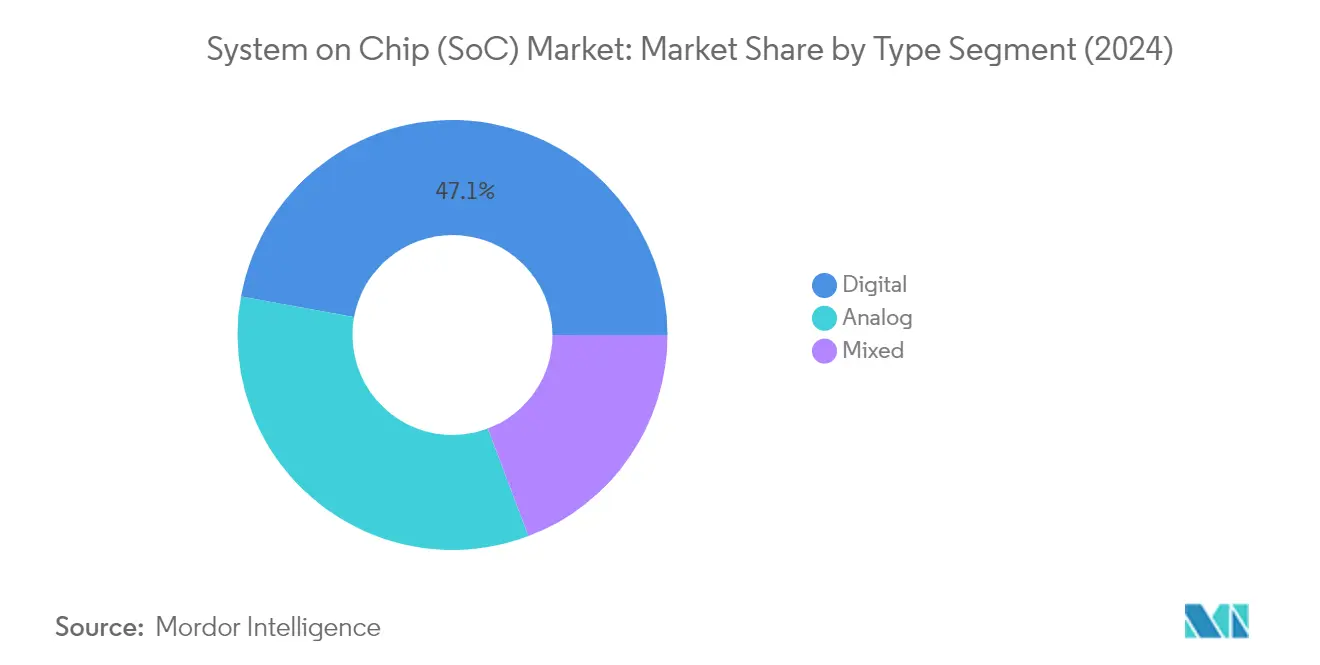

Digital Segment in System on Chip (SoC) Market

The digital segment continues to dominate the global System on Chip (SoC) market, holding approximately 47% market share in 2024. This significant market position is driven by the increasing adoption of digital SoCs in various applications, including Internet of Things devices, smartphones, and reconfigurable devices like Field Programmable Gate Arrays (FPGA). Digital SoCs are particularly valued for their high processing speed, immunity to noise, and enhanced efficiency in data processing applications. The segment's growth is further bolstered by developments in mobile chipsets, with companies like Intel and MediaTek introducing advanced digital SoC solutions optimized for 5G technology and artificial intelligence applications. The rising demand for computing power driven by digitalization across industries has led to increased investments in digital SoC development, particularly for applications requiring high-performance processing capabilities.

Mixed Signal Segment in System on Chip (SoC) Market

The mixed signal segment is projected to experience the highest growth rate of approximately 9% during the forecast period 2024-2029. This accelerated growth is attributed to the increasing demand for SoCs that can efficiently handle both analog and digital signals in a single chip. Mixed signal SoCs are gaining prominence in applications such as sensors, healthcare devices, and RF SoC implementations, where the ability to process both types of signals is crucial. The segment's growth is being driven by advancements in wireless applications and the rising adoption of IoT devices that require sophisticated signal processing capabilities. Major manufacturers are investing in developing advanced mixed signal SoC solutions with improved power efficiency and reduced system complexity, particularly for applications in 5G technology, automotive electronics, and consumer devices.

Remaining Segments in System on Chip (SoC) Market by Type

The analog segment represents a crucial component of the SoC market, playing a vital role in applications requiring high-precision programmable analog capabilities. Analog SoCs are essential in various applications, including sensor interfaces, wireless communication, power management, and data acquisition systems. These components are particularly important in IoT devices, smartphones, and mobile devices, where they handle functions like audio processing, camera interfaces, and touchscreen controllers. The segment continues to evolve with innovations in areas such as motor drivers for automotive applications and developments in analog machine learning chips, contributing significantly to the overall market dynamics.

Segment Analysis: By End User Industry

Consumer Electronics Segment in System on Chip (SoC) Market

The consumer electronics segment maintains its dominance in the System on Chip (SoC) market, commanding approximately 46% market share in 2024. This significant market position is primarily driven by the increasing adoption of smartphones, intelligent speakers, tablets, wearables, and other smart devices that extensively employ edge AI chips. The integration of SoCs in consumer electronics facilitates improved efficiency, decreased energy usage, and compactness, making them essential for numerous applications. The rising demand for AI chip technology, coupled with the escalating adoption of AI technology and the proliferation of IoT-connected consumer devices, has further strengthened this segment's market position. Major manufacturers are continuously introducing customized SoC chips for various consumer electronic applications, enhancing their performance and capabilities while focusing on power efficiency and compact design.

Communications Segment in System on Chip (SoC) Market

The communications segment is experiencing remarkable growth in the SoC market, projected to expand at approximately 10% CAGR from 2024 to 2029. This accelerated growth is primarily attributed to the rapid advancement of 5G technology and the increasing demand for high-speed data connectivity. The segment's expansion is further supported by the rising number of mobile subscribers and the growing need for value-added managed services. The integration of various components, including Wi-Fi and cellular network modems, into SoCs specifically designed for communication devices has become increasingly crucial. The trend toward remote working and digital transformation has intensified the demand for network connectivity and infrastructure, driving innovation in communication-focused SoC solutions. Manufacturers are developing more sophisticated and efficient SoC designs to meet the evolving requirements of modern communication systems.

Remaining Segments in End User Industry

The automotive, computing and data storage, industrial, and other segments collectively represent significant opportunities in the SoC market. The automotive segment is witnessing substantial growth due to the increasing integration of advanced driver assistance systems (ADAS) and electric vehicle technologies. The computing and data storage segment focuses on developing high-performance SoCs for data centers and cloud computing applications. The industrial segment is driven by the growing adoption of automation and Industry 4.0 technologies, while the remaining segments cater to specialized applications in healthcare, aerospace, and defense sectors. These segments are experiencing varying levels of growth based on their specific technological requirements and market dynamics, contributing to the overall diversification and expansion of the SoC market.

System On Chip (SoC) Market Geography Segment Analysis

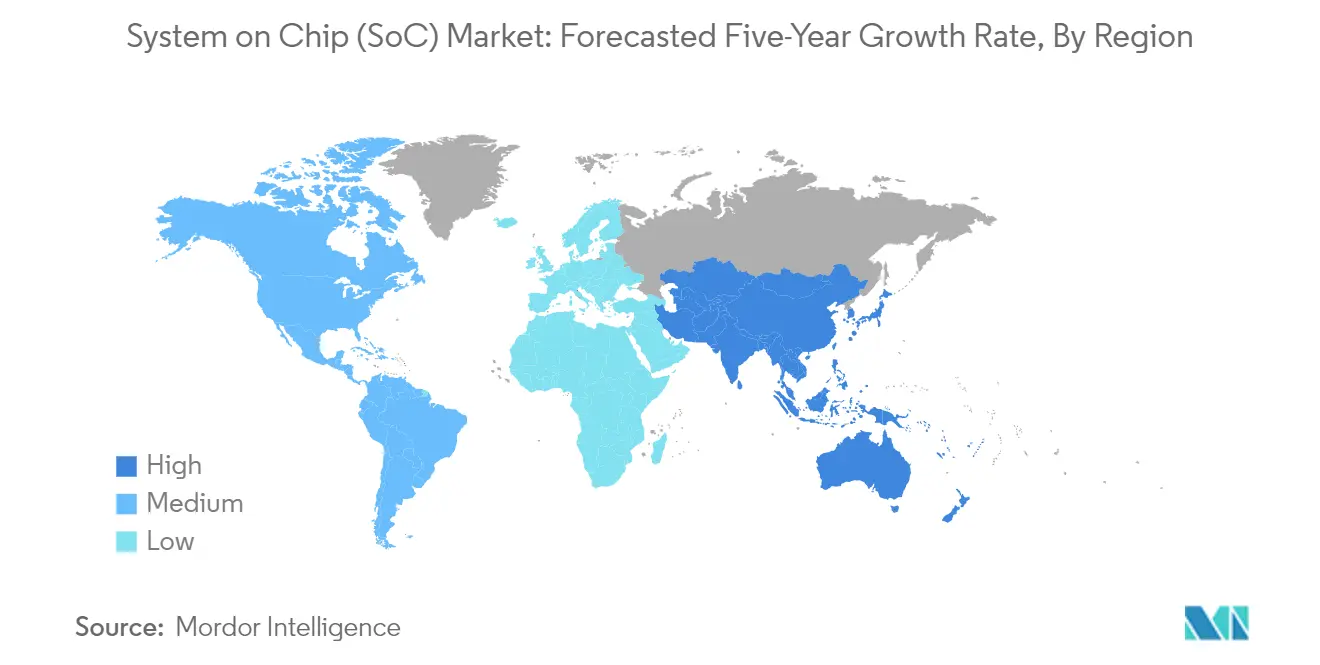

System on Chip (SoC) Market in North America

The North American SoC market continues to demonstrate robust growth, commanding approximately 22% of the global SoC market share in 2024. The region's market dynamics are primarily driven by the rapid adoption of emerging technologies like the Internet of Things (IoT) and the increasing integration of artificial intelligence capabilities. The strong presence of major semiconductor manufacturers and continuous technological innovations in the region contribute significantly to market expansion. The region's focus on advanced driver assistance systems (ADAS) and autonomous vehicles has created substantial opportunities for automotive SoC market manufacturers, particularly in the automotive sector. Furthermore, the growing demand for 5G-enabled devices and the ongoing development of 5G infrastructure are catalyzing market growth. The presence of a mature semiconductor ecosystem, coupled with substantial research and development investments, positions North America as a key player in the global SoC industry. The region's emphasis on edge computing and AI applications continues to drive innovation in SoC design and implementation.

System on Chip (SoC) Market in Europe

The European System on Chip (SoC) market has exhibited steady growth, with an annual growth rate of approximately 6% between 2019 and 2024. The region's market is characterized by a strong emphasis on automotive electronics and industrial automation applications. Europe's strategic focus on developing domestic semiconductor capabilities has led to increased investments in SoC research and development. The region's automotive sector, particularly the electric vehicle segment, continues to be a major driver for SoC adoption. The European market benefits from robust government support and initiatives aimed at strengthening the semiconductor industry's competitiveness. The presence of established automotive manufacturers and their increasing focus on connected and autonomous vehicles creates sustained demand for advanced SoC solutions. Additionally, the region's strong industrial base and growing adoption of Industry 4.0 technologies contribute significantly to market growth. The emphasis on sustainable and energy-efficient solutions has also influenced SoC development in the region.

System on Chip (SoC) Market in Asia-Pacific

The Asia-Pacific SoC market is poised for exceptional growth, with a projected annual growth rate of approximately 9% from 2024 to 2029. The region represents the largest and most dynamic market for SoC solutions, driven by the presence of major semiconductor manufacturing facilities and a robust electronics manufacturing ecosystem. China, Japan, Taiwan, and South Korea collectively form the backbone of the region's SoC industry, with significant contributions from emerging economies like India and Southeast Asian nations. The region's dominance in smartphone manufacturing and consumer electronics production continues to drive substantial demand for SoC solutions. The rapid adoption of 5G technology and increasing investments in telecommunications infrastructure further accelerate market growth. The presence of major foundries and semiconductor manufacturing facilities provides a competitive advantage to the regional market. Additionally, the growing automotive electronics sector and increasing adoption of IoT devices contribute to the region's market expansion.

System on Chip (SoC) Market in Rest of the World

The Rest of the World region, encompassing Latin America, the Middle East, and Africa, represents an emerging market for SoC solutions with significant growth potential. The market in these regions is primarily driven by increasing digitalization efforts and growing adoption of smartphones and consumer electronics. The automotive sector's transformation, particularly in Latin American countries, is creating new opportunities for SoC applications. Government initiatives to promote digital inclusion and enhance telecommunications infrastructure are contributing to market growth. The region is witnessing increased investments in 5G infrastructure development, which is expected to drive demand for SoC solutions. The growing focus on electric vehicle adoption in several African nations and the Middle East is creating new opportunities for automotive SoC applications. Additionally, the increasing penetration of IoT devices and smart technologies across various sectors is fostering market growth in these regions.

Get Analysis on Important Geographic Markets

Download PDF

System On Chip Industry Overview

Top Companies in System on Chip (SoC) Market

The global SoC market is dominated by established players, including Broadcom, Intel, MediaTek, Microchip Technology, NXP Semiconductors, Qualcomm, Samsung Electronics, STMicroelectronics, Apple, and TSMC. These SoC manufacturers are heavily investing in research and development to advance their foundry and semiconductor capabilities, with a particular focus on emerging technologies like AI, 5G, and autonomous systems. The industry witnesses continuous product innovation through the development of more powerful and efficient chips, with companies increasingly focusing on customizable solutions to meet specific application requirements. Strategic partnerships and collaborations have become crucial, especially in areas like automotive SoCs and mobile computing platforms. Companies are expanding their manufacturing capabilities globally, with significant investments in new fabrication facilities across Asia, Europe, and North America, while also focusing on sustainable and energy-efficient production methods.

Market Structure Shows High Entry Barriers

The SoC market exhibits a highly consolidated structure dominated by large multinational corporations with extensive manufacturing capabilities and robust intellectual property portfolios. These established SoC companies benefit from significant economies of scale, strong customer relationships, and comprehensive distribution networks spanning multiple regions. The market has high entry barriers due to the substantial capital requirements for manufacturing facilities, extensive research and development needs, and the complexity of chip design processes. The industry is characterized by strategic alliances and partnerships, particularly between design houses and foundries, creating an intricate ecosystem of interdependent relationships.

The market has witnessed strategic mergers and acquisitions aimed at expanding technological capabilities and market reach, particularly in emerging application areas like automotive and IoT devices. Companies are increasingly focusing on vertical integration strategies to maintain control over their supply chains and reduce dependencies on external partners. Regional players, especially in Asia, are gradually expanding their presence through government support and strategic investments in manufacturing capabilities. The industry also sees collaboration between traditional semiconductor companies and technology giants, particularly in developing specialized SoCs for specific applications.

Innovation and Adaptability Drive Future Success

Success in the SoC market increasingly depends on companies' ability to innovate and adapt to rapidly evolving technological demands. Incumbent SoC vendors must maintain their competitive edge through continuous investment in advanced manufacturing processes, development of specialized solutions for emerging applications, and strategic partnerships with key customers. Companies need to focus on developing energy-efficient designs, implementing advanced packaging technologies, and expanding their intellectual property portfolios. The ability to offer customized solutions while maintaining cost competitiveness will be crucial for market success, as will the capacity to navigate complex supply chain dynamics and geopolitical challenges.

For new entrants and smaller players, success lies in identifying and focusing on niche market segments where they can develop specialized expertise. Companies must build strong relationships with foundries and technology partners while investing in research and development to create differentiated products. The increasing importance of specialized applications in areas like artificial intelligence, autonomous vehicles, and IoT presents opportunities for focused innovation. Regulatory compliance, particularly in areas like data security and environmental sustainability, will become increasingly important for all market participants. Companies must also maintain flexibility in their manufacturing strategies to address potential supply chain disruptions and changing market demands.

System On Chip Market Leaders

-

Broadcom Inc.

-

Intel Corporation

-

MediaTek Inc.

-

Microchip Technology Inc.

-

NXP Semiconductors NV

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

System On Chip Market News

- September 2023: MediaTek and TSMC announced the successful development of its first chip using TSMC’s leading-edge 3nm technology, taping out MediaTek’s flagship Dimensity system-on-chip (SoC) with volume production expected in 2024. This marks a significant milestone in the long-standing strategic partnership between MediaTek and TSMC, with both companies taking full advantage of their chip design and manufacturing strengths to create flagship SoCs with high-performance and low-power features jointly, empowering global end devices.

- April 2023: Broadcom Inc. announced the production of Jericho3-AI, enabling the industry’s highest-performance fabric for artificial intelligence (AI) networks. Jericho3-AI revolutionizes AI networking with best-in-class capabilities such as perfect load balancing, congestion-free operation, ultra-high radix, and Zero-Impact Failover, culminating in significantly shorter job completion times for any AI workload.

System On Chip Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain/Supply Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Rising Adoption of Emerging Technologies Like IoT and AI

- 5.1.2 Increasing Investments in 5G and Growing Demand for 5G Smartphones

-

5.2 Market Restraints

- 5.2.1 High Initial Costs of R&D

6. MARKET SEGMENTATION

-

6.1 By Type

- 6.1.1 Analog

- 6.1.2 Digital

- 6.1.3 Mixed

-

6.2 By End-user Industry

- 6.2.1 Consumer Electronics

- 6.2.2 Communications

- 6.2.3 Automotive

- 6.2.4 Computing and Data Storage

- 6.2.5 Industrial

- 6.2.6 Other End-user Industries

-

6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Rest of the World

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 Broadcom Inc.

- 7.1.2 Intel Corporation

- 7.1.3 Mediatek Inc.

- 7.1.4 Microchip Technology Inc.

- 7.1.5 NXP Semiconductors NV

- 7.1.6 Qualcomm Incorporated

- 7.1.7 Samsung Electronics Co. Ltd

- 7.1.8 STMicroelectronics NV

- 7.1.9 Toshiba Corporation

- 7.1.10 Apple Inc.

- 7.1.11 Taiwan Semiconductor Manufacturing Company Limited (TSMC)

- 7.1.12 Texas Instruments Incorporated

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

System On Chip Industry Segmentation

System-on-a-chip refers to a type of integrated circuit (IC) design that combines many or all high-level function elements of an electronic device onto a single chip instead of using separate components mounted to a motherboard, as is done in traditional electronics design. The components that an SoC generally looks to incorporate within itself include a central processing unit, input and output ports, internal memory, and analog input and output blocks, among other things.

The system-on-chip (SoC) market is segmented by type (analog, digital, and mixed), end-user industry (consumer electronics, communications, automotive, computing and data storage, industrial, and other end-user industries), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Type | Analog |

| Digital | |

| Mixed | |

| By End-user Industry | Consumer Electronics |

| Communications | |

| Automotive | |

| Computing and Data Storage | |

| Industrial | |

| Other End-user Industries | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| Rest of the World |

Need A Different Region or Segment?

Customize Now

System On Chip Market Research FAQs

How big is the System On Chip Market?

The System On Chip Market size is expected to reach USD 186.48 billion in 2025 and grow at a CAGR of 8.01% to reach USD 274.13 billion by 2030.

What is the current System On Chip Market size?

In 2025, the System On Chip Market size is expected to reach USD 186.48 billion.

Who are the key players in System On Chip Market?

Broadcom Inc., Intel Corporation, MediaTek Inc., Microchip Technology Inc. and NXP Semiconductors NV are the major companies operating in the System On Chip Market.

Which is the fastest growing region in System On Chip Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in System On Chip Market?

In 2025, the Asia Pacific accounts for the largest market share in System On Chip Market.

What years does this System On Chip Market cover, and what was the market size in 2024?

In 2024, the System On Chip Market size was estimated at USD 171.54 billion. The report covers the System On Chip Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the System On Chip Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

System On Chip (SoC) Market Research

Mordor Intelligence provides a comprehensive analysis of the system on chip industry. We leverage extensive expertise in SOC semiconductor research and consulting. Our team of analysts thoroughly examines SOC manufacturers and system on chip vendors. This provides detailed insights into chip customization service trends and technological developments. The report covers crucial aspects of SOC technologies and their implementation across various sectors. We pay particular attention to system on chip companies and their strategic initiatives. Available as an easy-to-read report PDF, our analysis encompasses both established SOC manufacturers and emerging players in the industry.

The report offers actionable insights into system on chip market size trends and growth projections. This enables stakeholders to make informed decisions. Our analysis covers various aspects, including SOC as a service offerings, emerging chip sizes, and advanced system-on-chip technologies. The comprehensive coverage extends to SOC system developments, chip customization trends, and evolving industry standards. Stakeholders benefit from our detailed examination of SOC industry dynamics, technological innovations, and future growth opportunities. This is supported by robust data analysis and expert insights from leading system on chip manufacturers.