Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

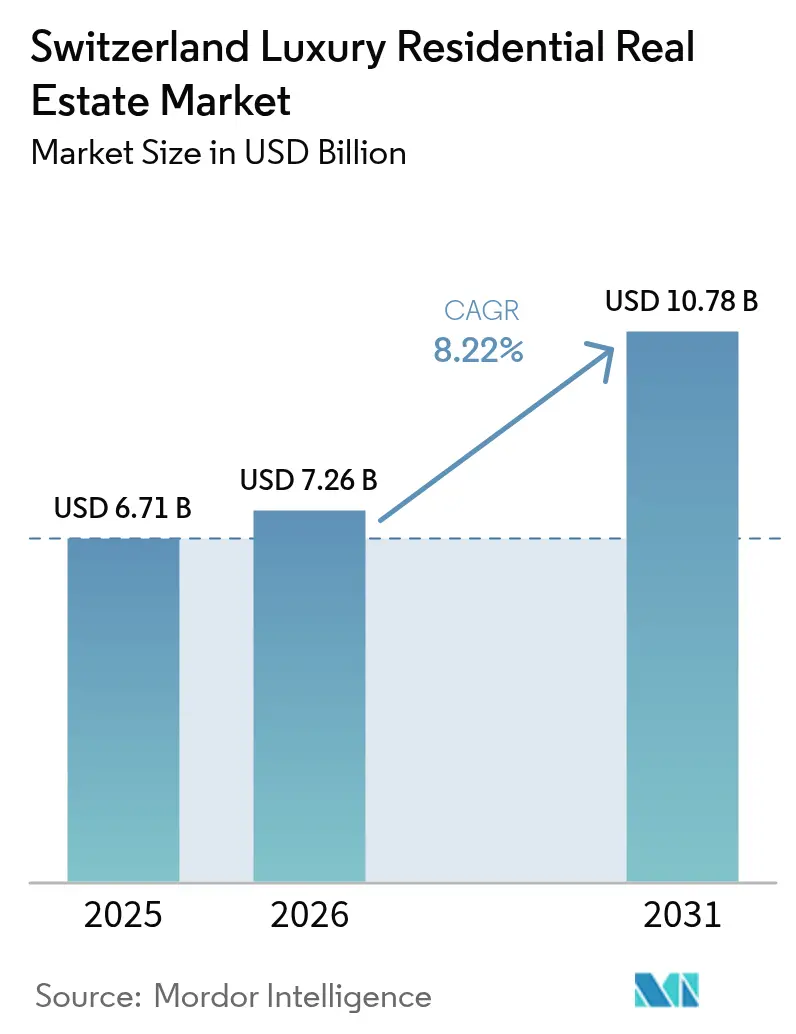

| Base Year Market Size (2025) | USD 6.71 Billion |

| Market Size (2026) | USD 7.26 Billion |

| Market Size (2031) | USD 10.78 Billion |

| Growth Rate (2026 - 2031) | 8.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Luxury Residential Real Estate Market Analysis by Mordor Intelligence

The Switzerland luxury residential real estate market size is expected to grow from USD 6.71 billion in 2025 to USD 7.26 billion in 2026 and is forecast to reach USD 10.78 billion by 2031 at 8.22% CAGR over 2026-2031. A sustained inflow of ultra-high-net-worth (UHNW) migrants, an enduring safe-haven reputation, and a deepening appetite for hard-asset protection continue to underpin demand. While traditional sales still dominate transactions, premium rentals are accelerating as wealthy newcomers test the environment before purchasing. Limited land availability in prime cantons locks in scarcity, supporting price appreciation and pushing developers toward vertical, amenity-rich projects. At the same time, tokenization platforms, ESG-driven design, and branded residences have begun reshaping competitive tactics as brokers race to differentiate their offer sets.

Key Report Takeaways

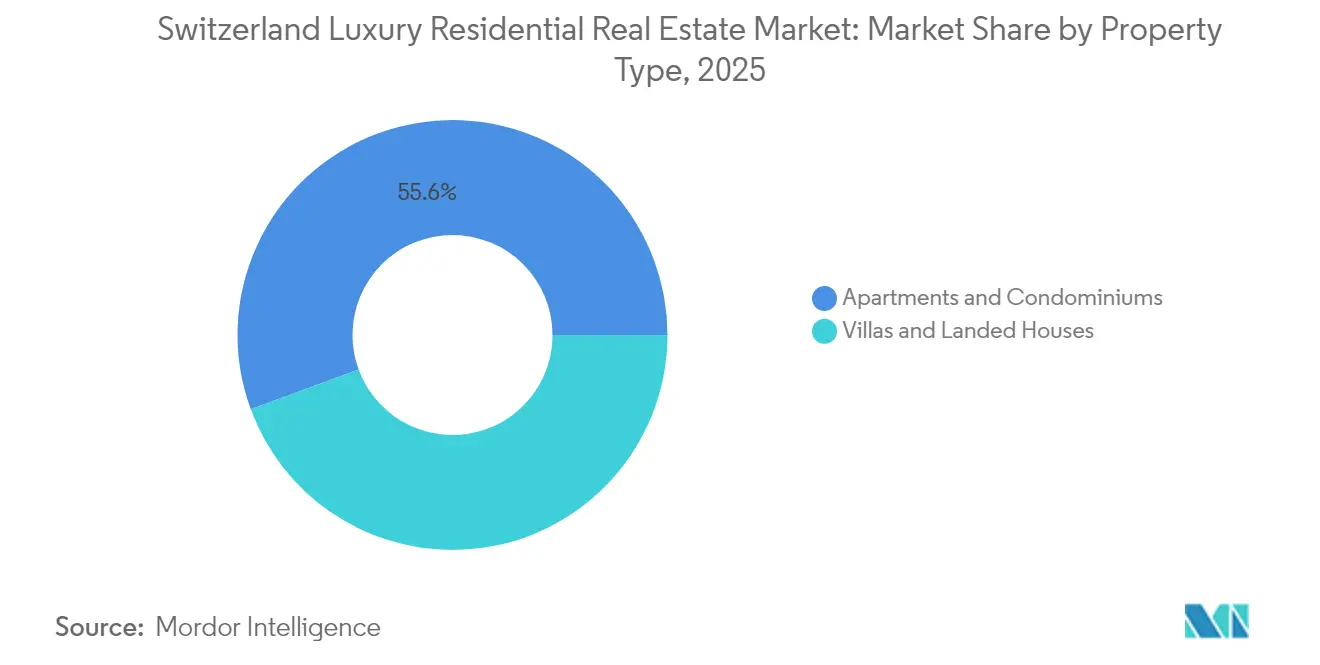

- By property type, apartments and condominiums controlled 55.62% of the Switzerland luxury residential real estate market share in 2025. The Switzerland luxury residential real estate market for the same segment is projected to post the fastest 8.61% CAGR through 2031.

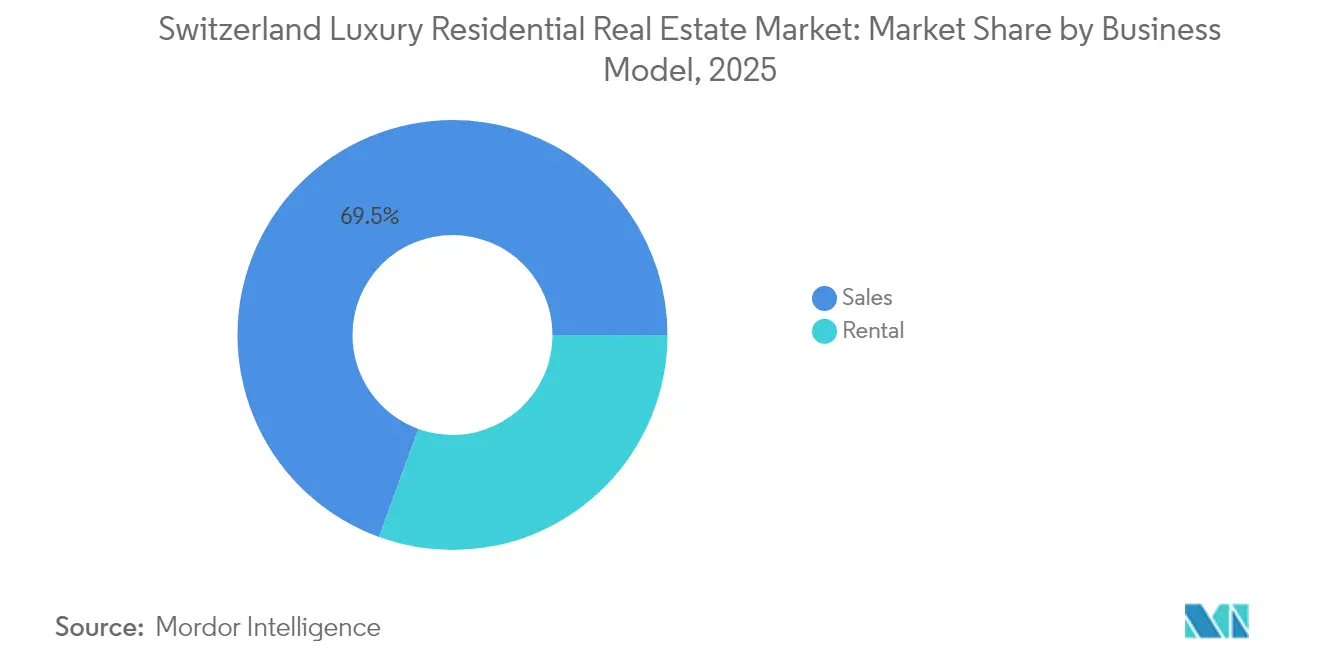

- By business model, the sales segment retained a 69.45% share of the Switzerland luxury residential real estate market size in 2025. The Switzerland luxury residential real estate market for the rental segment is advancing at a 9.28% CAGR to 2031.

- By mode of sale, secondary resale captured 54.60% of the Switzerland luxury residential real estate market size in 2025. The Switzerland luxury residential real estate market for primary new-build properties is growing at 8.75% CAGR through 2031.

- By city, Zurich led with 27.82% of the Switzerland luxury residential real estate market revenue share in 2025. The Switzerland luxury residential real estate market for Zug is forecast to expand at a 9.52% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Negative/low interest-rate environment | +2.1% | Nationwide, spillover from EU | Short term (≤ 2 years) |

| Second-home demand from EU & UK buyers | +1.8% | Alpine resorts, Lake Geneva, Ticino | Long term (≥ 4 years) |

| Strong UHNW wealth inflows & safe-haven appeal | +1.5% | Zurich, Geneva, Zug | Medium term (2-4 years) |

| Crypto-wealth deployment via tokenization | +1.2% | Zug, Zurich, nationwide | Medium term (2-4 years) |

| Expansion of single-family offices | +0.9% | Zurich, Geneva, Basel | Medium term (2-4 years) |

| Health-tech-enabled wellness homes | +0.8% | Alpine resorts, urban luxury | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong UHNW Wealth Inflows & Safe-Haven Appeal

Switzerland attracted a record 1,500 new millionaires in 2024, reinforcing the nation’s safe-haven pull for internationally mobile capital. Zurich, Geneva, and Zug sit at the epicenter of this migration, yet seasonal destinations such as Gstaad and St. Moritz also register rising villa demand. Beyond banking secrecy, Switzerland’s innovation ranking and stable governance amplify its magnetism. The outcome is consistent upward pressure on trophy-asset prices and a structurally high demand floor that shields the Switzerland luxury residential real estate market from short-term volatility.

Negative/Low Interest-Rate Environment Fueling Real-Asset Allocation

Persistently accommodative monetary settings across developed economies continue to suppress fixed-income yields, nudging wealthy investors toward tangible assets. Swiss luxury homes offer an appealing hedge against inflation and currency swings, prompting a noticeable tilt to all-cash deals and faster closings. The trend simultaneously reduces financing friction for developers and supports premium valuations as cash buyers display minimal price sensitivity[1]Sotheby’s International Realty, “2024 Global Luxury Outlook,” sothebysrealty.

Second-Home Demand from Neighboring EU & UK Buyers

Affluent households from the EU and the UK are broadening their real-estate footprint to include Swiss addresses, diversifying risk and lifestyle options. Interest now extends beyond ski-only chalets toward year-round residences near Basel and Geneva. Dual-season properties that mix winter sports with summer recreation capture a growing slice of cross-border capital, reinforcing geographic demand resilience[2]Financial Times, “Swiss Alpine Homes Surge as EU Buyers Diversify,” ft.com.

Expansion of Single-Family Offices Driving Off-Market Transactions

Roughly 320 single-family offices worldwide, averaging USD 2.6 billion in net wealth, operate with an increasing focus on private Swiss real-estate allocations. These players favor discreet, off-market trades, rewarding brokers with deep relationship networks. Confidential deal-making lifts average ticket values and filters supply into invitation-only channels, strengthening the pricing power of the Switzerland luxury residential real estate market[3]UBS Switzerland AG, “Global Family Office Report 2024,” ubs.com .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lex Koller restrictions on foreign ownership | –1.2% | Nationwide, varying by canton | Long term (≥ 4 years) |

| ESG retrofit capex for heritage properties | –1.0% | Alpine resorts, historic cores | Medium term (2-4 years) |

| Scarce developable land & stringent zoning | –0.8% | Urban centers, Alpine resorts | Long term (≥ 4 years) |

| Climate-risk-driven insurance spikes | –0.6% | Alpine resort areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lex Koller Restrictions on Foreign Ownership

Lex Koller limits non-resident acquisitions outside designated resort zones, adding legal complexity and dampening some overseas demand. Specialized counsel becomes mandatory, lengthening deal timelines and raising transaction costs. Ongoing political debate around tighter thresholds injects additional uncertainty, leading some buyers to accelerate purchases while others pause.

Scarce Developable Land & Stringent Zoning Limits

Mountainous terrain and rigid zoning shrink the pool of buildable plots, particularly in Zurich and Geneva. Developers pivot toward vertical luxury towers, but pro-environment approvals slow pipeline velocity. The bottleneck reinforces price stability yet caps volume growth, nudging investors to compete fiercely for limited inventory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Apartments Drive Urban Consolidation

Apartments and condominiums dominated with a 55.62% share in 2025, and this slice is set to widen on an 8.61% CAGR. The Switzerland luxury residential real estate market size for high-rise dwellings already exceeds that of villas and will outpace landed homes through 2031. Scarcity of downtown land incentivizes vertical builds, while turnkey smart-building features attract globally mobile buyers. Branded residences backed by hospitality groups introduce concierge services and rental pools that broaden appeal. At the same time, villa demand persists in lakeside and resort niches, but permitting caps restrain fresh supply and shift the focus toward lavish renovations rather than ground-up projects.Urban apartments are also prime candidates for fractional tokenization, opening ownership to a wider investor base without disturbing title integrity. This innovation could lift liquidity and compress hold periods, improving exit prospects for developers. Moreover, wellness-centric floor-plans and energy-positive façades align with Switzerland’s long-term carbon goals, reinforcing premium price resilience even as economic cycles fluctuate.

By Business Model: Rental Segment Accelerates

Although outright sales held 69.45% of revenues in 2025, luxury rentals are racing ahead at a 9.28% CAGR, reflecting lifestyle fluidity among top-tier tenants. Executives relocating for post-merger assignments prefer the flexibility of six-to-thirty-six-month leases, often negotiated with hotel-grade services bundled in. This trend benefits institutional landlords chasing stable yields in a low-rate landscape.The Switzerland luxury residential real estate market size for leased stock is forecast to double between 2026 and 2031 as developers allocate floors within new towers to serviced rental units. Tax considerations also play a role: leasing can facilitate domicile planning and ease cross-border mobility, especially for EU citizens who maintain primary homes abroad. Landlords capitalize by offering tailored concierge, wellness, and digital-nomad packages that differentiate premium rental offerings.

By Mode of Sale: Primary Market Innovation

Secondary resales comprised 54.60% of 2025 turnover, yet new construction is sprinting ahead at 8.75% CAGR. Buyers crave ESG-certified materials, geothermal heating, and AI-enabled building management that older stock rarely offers. Developers respond with boutique blocks—often fewer than twenty units—featuring private spas, art storage, and security suites.Higher building costs are partly offset by price premiums inherent in modern amenities. Furthermore, alignment with forthcoming Swiss energy codes shields owners from forced retrofits. As sustainability scorecards increasingly influence financing terms, primary assets gain an intrinsic advantage. The Switzerland luxury residential real estate market share of new builds will therefore expand steadily, crowding traditional chalets that lack retrofit feasibility.

Geography Analysis

Zurich anchored 27.82% of transaction values in 2025 and sustains a pipeline constrained by zoning curbs around its lakefront districts. Financial services consolidation has ushered in senior executives and fintech founders who view proximity to the city’s CBD and innovation hubs as non-negotiable. Limited developable plots compress supply, keeping the Switzerland luxury residential real estate market price points in Zurich among Europe’s highest.Geneva retains its stature as the second-largest cluster, fueled by diplomatic presence and a robust private-banking ecosystem. Cross-border French residents have grown their participation, drawn by lifestyle perks and the city’s international school network. Developers are embedding wellness squares and green roofs to satisfy buyers’ ESG and health expectations. Zug shines as the fastest riser at a 9.52% CAGR on the back of corporate tax incentives and its burgeoning Crypto Valley brand. Blockchain entrepreneurs require rapid, versatile housing solutions, triggering demand for smart apartments that integrate digital-wallet door access and cold-storage vaults. The canton’s efficient rail links to Zurich bolster its allure.Bern and Basel round out the major urban contenders, with Basel benefiting from life-science cluster growth and Bern from federal administrative stability. Resort territories—Gstaad, Verbier, St. Moritz—specialize in chalet and penthouse offerings that capture seasonal affluence. Climate-risk adaptation, such as avalanche shielding and low-carbon heating systems, is now standard, propping up property values despite rising insurance costs. Overall, the geographic spread cushions the Switzerland luxury residential real estate market against localized shocks, distributing demand drivers across finance, diplomacy, technology, and tourism corridors.

Regulatory Landscape

Foreign participation in Swiss luxury residential property is governed by the Federal Act on the Acquisition of Immovable Property in Switzerland by Foreign Non-Residents (Lex Koller/ANRA), which in practice is administered by competent cantonal authorities that determine when transactions require authorization. A key 2026 policy event is the Federal Council opening a public consultation on 15 April 2026 to tighten Lex Koller, with the consultation period running until 15 July 2026. The proposed package targets both direct purchases and indirect exposure via listed real estate vehicles.

The proposed Lex Koller revision introduces tighter permit requirements, including for purchases of primary residences by certain non-EU/EFTA nationals. It also includes restrictions aimed at passive rental investment by non-residents in commercial property, alongside constraints on acquisitions of shares in residential property companies by persons abroad. In parallel, the Federal Assembly authorized a CHF 1.92 billion commitment credit on 2 June 2026 to support affordable housing contingent liabilities (effective for 1 July 2027 to 31 December 2033), reinforcing the political focus on housing affordability that shapes scrutiny of luxury-market capital flows.

Value Chain Analysis

The value chain in Swiss luxury residential real estate runs from land sourcing and entitlement (highly canton- and municipality-driven zoning and permitting) through design and construction (general contractors such as Implenia, specialist trades, and premium materials), then commercialization (brokerage networks including Sotheby’s International Realty Switzerland, Engel & Völkers, BARNES, SPG Finest Properties, and Naef Prestige - Knight Frank), and finally ownership operations (property management, concierge and service partners, insurers, and lenders and wealth managers). Institutional owners such as Swiss pension funds and insurers are influential on the hold-and-operate side, while family offices and UHNW buyers drive demand for off-market sourcing and privacy-led advisory.

Bottlenecks are concentrated upstream, where scarce buildable plots in prime cantons and lengthy planning approvals limit new luxury supply and shift activity toward redevelopments and vertical projects. Transaction-stage friction is also material for foreign demand, with Lex Koller compliance and cantonal authorization processes shaping buyer eligibility, deal timelines, and structuring (including via funds or corporate vehicles). This increases the role of specialized legal and tax advisors in closing high-ticket transactions.

Competitive Landscape

The competitive field remains moderately consolidated. Sotheby’s International Realty Switzerland and Engel & Völkers together handle a significant slice of marquee listings, while SPG Finest Properties and BARNES Switzerland excel in boutique off-market brokering. Global franchise brands harness cross-border referral pipelines, appealing to buyers relocating from Asia and the Middle East. Local agencies leverage granular canton knowledge and regulatory fluency to maintain relevance.

Technology adoption divides incumbents. Early movers pilot tokenized sales portals and AI-led valuation tools, whereas heritage-driven firms lean on interpersonal trust. The Switzerland luxury residential real estate market demonstrates an appetite for hybrid offerings: traditional concierge service fused with data-enabled transparency. M&A chatter has intensified following the UBS-Credit Suisse consolidation, with wealth-management divisions exploring in-house brokerage capabilities that could compress fees and pressure stand-alone agencies.

Strategic pivots include branded wellness residences in Verbier, senior-living luxury towers in Lugano, and co-ownership platforms targeted at expatriate professionals. Firms competent in structuring these novel formats are positioned to capture the next wave of demand.

Switzerland Luxury Residential Real Estate Industry Leaders

Sotheby’s International Realty Switzerland

Engel & Völkers Switzerland

BARNES Switzerland

SPG Finest Properties

Naef Prestige – Knight Frank

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is forming around product formats that monetize scarcity while lowering friction for globally mobile buyers, especially premium rentals and serviced, amenity-rich urban apartments. Within the study scope, apartments and condominiums already hold 55.62% share in 2025, while rentals are the fastest-growing business model. Demand is concentrated in Zurich, Geneva, and Zug, and supply is constrained by zoning and limited land, creating differentiation room for turnkey, wellness-oriented layouts, building-level services, and smart-building features that fit six-to-thirty-six-month lease use cases alongside eventual purchase decisions.

Capital-markets and distribution innovation is another opportunity area, but it is closely linked to policy direction. The Federal Council launched a consultation on 15 April 2026 to tighten Lex Koller, including proposed curbs on indirect investment via listed real estate vehicles, which increases the value of compliant structuring and domestically anchored capital partners. In parallel, UBS published Luxury Property Focus 2026 and noted luxury price gains of over 3% on average in 2025 across 31 prime Swiss locations, with Alpine regions cited at 6% growth in 2025. That pricing track record supports investment in ESG-forward new-builds and high-quality repositioning in top nodes and select resort markets where scarcity and lifestyle demand converge.

Recent Industry Developments

- July 2026: Engel & Voelkers Nordwestschweiz began construction on the Vier Hoehen project in Oberwil, comprising 26 condominiums and four houses. The start of works adds fresh high-end supply in a market where new-build availability is constrained by permitting and land scarcity, and it supports the shift toward apartment-led luxury formats.

- May 2026: UBS Switzerland AG published Luxury Property Focus 2026, reporting that luxury residential prices rose by an average of over 3% in 2025 across 31 prime Swiss locations, with Alpine regions cited at 6% growth in 2025. The report provides an institutional benchmark used by wealth managers and buyers for pricing discipline and location selection, influencing liquidity and negotiation dynamics for trophy assets.

- May 2025: Citi partnered with SIX Digital Exchange (SDX) to open tokenized private-market access for institutional investors. The initiative strengthened the infrastructure and investor familiarity needed for tokenized real-asset exposure, which aligns with growing interest in fractional or digital distribution models for high-value property-linked investments.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the total value of luxury residential property transactions in Switzerland, where the homes are priced and positioned as premium residences (apartments, condominiums, villas, and landed houses) across key cities and resort-linked locations.

Scope exclusions: We exclude commercial real estate, standard residential units below luxury price thresholds, and pure land-only sales that are not tied to a completed or marketed luxury home transaction.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Business Model

- Sales

- Rental

- By Mode of Sale

- Primary (New-build)

- Secondary (Resale)

- By City

- Zurich

- Geneva

- Basel

- Bern

- Zug

- Other Cities

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a fact base on Switzerland housing activity, pricing signals, and foreign demand constraints, and then mapping these to what is realistic for the luxury end of the market. We mainly relied on public statistical releases and policy notes to avoid assumptions that cannot be checked later.

Common inputs included sources such as the Swiss Federal Statistical Office (housing and construction indicators), the Swiss National Bank (macro and mortgage series), land registry and canton level publications where available, OECD housing indicators, and BIS property price statistics for cross checks. We also used company annual reports, investor presentations, reputable press coverage, and an import and export shipment-level database selectively to sanity check high value materials flows linked to premium construction. This list is not exhaustive and many other public and subscription sources were also referred to for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually selling in the luxury bracket, how much is new-build versus resale, and how buyer appetite changes across major cities and resort-led markets. We spoke with a mix of developers, brokers, property advisors, lenders, and legal or tax practitioners to confirm price thresholds, deal velocity, and the role of non-resident demand, which then helped us tighten assumptions used in the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | APAC: 41% |

| Mid tier: 51% | Functional/Unit leaders: 26% | EMEA: 37% |

| Smaller Players: 14% | Managers: 60% | Americas: 22% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic together, so the totals remain anchored to observable housing activity while still reflecting luxury specific deal structure. The top-down build starts from Switzerland residential transaction and price signals, which are then filtered using luxury price thresholds, prime location concentration, and the share of activity that fits high end stock.

To corroborate the totals, we used selective bottom-up approximations like sampled listings to infer absorption, cross checks on average selling prices by city cluster, and developer pipeline checks for new-build units. Key inputs (illustrative) included luxury home price indices and spreads versus mainstream housing, transaction counts and turnover rates in high demand municipalities, new-build versus resale mix, mortgage rate expectations and affordability sensitivity in the premium segment, and policy constraints affecting non-resident purchases.

For forecasting, scenario analysis was applied around interest rates, safe haven demand, and supply tightness, and then a light multivariate regression was used to keep price and volume paths consistent with macro variables that interviewees expect to matter most. Where bottom-up signals were thin for smaller cities, gaps were handled by applying validated ratios from comparable markets and then re-checking results against observed inventory and time-on-market trends.

Data Validation & Update Cycle

Outputs were checked in steps so any unrealistic jumps could be caught early, including year to year variance scans by city cluster and by sales versus rental contribution. We compared the model against independent signals like published price growth for luxury homes, construction completions, mortgage rate moves, and observed listing stock, and then reviewed mismatches before sign-off.

Reports refresh annually, and interim updates are triggered when material events occur such as sharp rate changes, major regulatory shifts, or visible demand breaks in prime areas. Before delivery, a final analyst pass is completed to ensure the latest public releases and fresh interview feedback are reflected in the charts and market totals.

Mordor Intelligence's Switzerland Luxury Residential Real Estate Market Sizing Compared With Other Published Estimates

Published values for Switzerland luxury residential real estate do not always line up because the term luxury is not defined the same way across sources, and because some studies mix price tracking with transaction value sizing. Differences also come from how resale activity is treated, whether rentals are counted as part of the market value, and how often the underlying price thresholds are refreshed.

The table shows a clear spread that mostly traces back to scope boundaries and the conversion of price trends into total market value. In Mordor Intelligence's model, the market value is tied to luxury residential transaction value in Switzerland (including premium rentals), and city level sizing is built from activity and pricing checks rather than only extrapolating a luxury price index.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.26 B (2026) | |

| Global Consultancy A | USD 6.20 B (2026) | Uses a narrower luxury threshold and tends to count only primary market sales, which can understate resale heavy cities and omit high value rental activity. |

| Trade Journal B | USD 8.90 B (2026) | Back-solves market value from premium price change headlines and a broad housing value pool, which can over-include high priced but not truly luxury stock and double count turnover assumptions. |

Overall, the comparison suggests that the main sensitivity is not the math, it is what gets counted as luxury and how price signals are translated into value. By keeping the inputs traceable to transaction activity, price thresholds, and city level checks, we keep the market total easier to replicate and less dependent on one single pricing series.

Key Questions Answered in the Report

What is the current size of the Switzerland luxury residential real estate market?

The market is valued at USD 7.26 billion in 2026 and is projected to reach USD 10.78 billion by 2031.

Which property type leads the market?

Apartments and condominiums command 55.62% share and are growing at an 8.61% CAGR through 2031.

Why are luxury rentals expanding so quickly?

Wealthy tenants increasingly prefer flexibility, prompting the rental segment to advance at a 9.28% CAGR.

Which Swiss city shows the fastest luxury-property growth?

Zug leads with a 9.52% CAGR due to its low-tax regime and crypto-friendly ecosystem.

How do Lex Koller rules influence foreign buyers?

They restrict non-resident purchases outside resort zones, adding legal complexity and trimming potential demand growth.

What technology trends are reshaping the market?

Tokenized property platforms, wellness-tech integration, and ESG-driven design are creating new investment and product formats.

Page last updated on: