Market Overview

| Study Period | 2017 - 2029 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2029 |

| Market Size (2025) | USD 486.3 Million |

| Market Size (2029) | USD 621.4 Million |

| Growth Rate (2025 - 2029) | 6.32% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland E-bike Market Analysis by Mordor Intelligence

The Switzerland E-bike Market size is estimated at 486.3 million USD in 2025, and is expected to reach 621.4 million USD by 2029, growing at a CAGR of 6.32% during the forecast period (2025-2029).

Switzerland's e-bike industry is undergoing significant transformation driven by technological advancements and strategic corporate movements. The market landscape saw a major shift when TVS Motor acquired a 75% stake in the Swiss E-Mobility Group (SEMG) in 2022, demonstrating the growing international interest in Switzerland's e-bike sector. This consolidation has been accompanied by expansion initiatives, as evidenced by M-way, Switzerland's largest e-bike specialist, opening a new branch in Sihlcity, Zurich-Wiedikon, focusing on urban mobility solutions. These developments highlight the industry's maturation and the increasing importance of establishing a strong retail presence in key urban centers.

Infrastructure development plays a crucial role in supporting the e-bike Switzerland market's growth, with Switzerland boasting an extensive network of dedicated bike lanes reaching 2,920 kilometers in 2022. The country's commitment to sustainable transportation is further reinforced by comprehensive government support through subsidies and incentives. For instance, in Geneva, the government offers subsidies of up to CHF 250 for electric bikes and CHF 500 for cargo bikes, making these vehicles more accessible to the general population. This systematic approach to infrastructure development and financial support has created a robust foundation for market expansion.

Technological innovation continues to drive market evolution, particularly in battery technology and vehicle design. The industry has witnessed a remarkable decline in lithium-ion battery prices, dropping by over 75% over the past decade, making electric bikes increasingly cost-competitive. Leading manufacturers are leveraging these advances to introduce sophisticated new models, as demonstrated by BMC's launch of the Roadmachine 01 AMP X e-bike in 2022, featuring high-quality carbon fiber construction and internal cable routing. These innovations are setting new standards for performance and design in the industry.

The market is experiencing a notable shift in consumer adoption patterns, with projections indicating that e-bike penetration rates will reach 69.52% by 2029. This trend is supported by the expansion of electric bicycle sharing services and rental programs across major Swiss cities, making e-bikes more accessible to both residents and tourists. The industry is also witnessing increased collaboration between traditional bicycle manufacturers and technology companies, leading to enhanced product offerings with advanced features such as integrated navigation systems and smart connectivity options. These developments are creating new opportunities for market growth while reshaping the competitive landscape.

Switzerland E-bike Market Trends and Insights

Switzerland exhibits a high and steadily increasing E-Bike adoption rate, reflecting a mature market and strong consumer demand.

- While the country witnessed significant growth in the sales of bicycles over the past few years, in recent years, people have started shifting toward e-bikes, with consumers over the age of 40 highly contributing to the growth in the demand for e-bikes. Effortless riding in a given range, exercise benefits, and the ability to save time during traffic congestion have increased the adoption of e-bicycles in the country. These factors, along with reduced fuel costs and eco-friendly rides, accelerated the e-bicycle adoption rate in Switzerland in 2019.

- The COVID-19 pandemic positively affected the bicycle industry in Switzerland. Consumers not wishing to use public or rented transportation to maintain social distancing changed their commuting methods and invested in e-bikes, which are among the most convenient and affordable options among daily modes of commuting to offices and nearby places. Such factors further accelerated the adoption rate of e-bikes in 2020 across Switzerland.

- The drop in COVID-19 cases and the easing of government regulations saw the resumption of business operations and the removal of trade barriers, which resulted in good growth in the sales of e-bicycles in the country in 2021. The unveiling of new products and models with advanced features such as long battery life, good warranty offers, cashback, and discount schemes are projected to increase the adoption rate of e-bikes during the forecast period in Switzerland.

Understand The Key Trends Shaping This Market

Download PDF

Switzerland maintains a stable percentage of commuters traveling 5-15 km daily, indicating consistent commuting distances.

- Switzerland is highly popular for bicyclers and the country has witnessed a significant number of bicycle users over the past few years. However, most of people traveling to various places such as offices, businesses, or market areas opted for other means of transport as approximately 50% of the population opted for cars in 2020, and close to 10% of people opted for the bicycle (including e-bikes) to travel from 5 to 15 kilometers.

- The Swiss bicycle market was dramatically impacted by worries about COVID-19 and the pandemic wave. People chose to walk or bike instead of taking public transportation to work. After the pandemic's effects, fewer people used public transportation, which led to an increase in daily bicycle commuters of by 0.2% in 2021 over 2020. Additionally, the developments in e-bikes with advanced features such as longer battery lives encouraged more people to choose bicycles, which led to an increase in commuters who made trips of 5 to 15 kilometres in 2021 over 2020 throughout Switzerland.

- Since the limitations were lifted and the pandemic wave was relaxed, people have started commuting by bicycle as a habit. Within a radius of 5 to 15 kilometres, a significant number of people now go to work each day by bicycle between offices, businesses, and local markets. The number of people riding bicycles to work is increasing due to health benefits, producing no emissions, and saves you time by avoiding traffic. In Switzerland, these factors are expected to reach 63.6% in commuter travel between 5 and 15 kilometres during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Switzerland's bicycle sales peak in 2020, followed by a gradual decline, suggesting a market readjusting after a period of high demand.

- Switzerland maintains low and stable inflation rates, reflecting its strong and stable economic environment.

- Switzerland's e-bike battery prices are on a steady decline, reflecting technological advancements and a competitive market.

- Switzerland's steady increase in dedicated bicycle lanes reflects its ongoing commitment to enhancing cycling infrastructure for promoting sustainable mobility.

- Switzerland's E-bike charging time is steadily decreasing, showcasing the country's innovation in battery technology and electric vehicle infrastructure.

- Switzerland's consistently high GDP per capita demonstrates its global economic leadership and prosperity.

- Switzerland's bicycle rental market experienced a significant rise in 2020 and has been growing steadily since, indicating a robust market.

- Switzerland's hyper-local delivery sector is growing steadily, reflecting an increasing consumer adaptation to localized digital services.

- Switzerland's trekker numbers are steadily growing, signaling the enduring appeal of its alpine landscapes and the country's outdoor lifestyle.

- Switzerland's Traffic Congestion Index shows slight fluctuations, indicating variable traffic conditions and efforts to manage congestion.

Segment Analysis: Propulsion Type

Pedal Assisted Segment in Switzerland E-bike Market

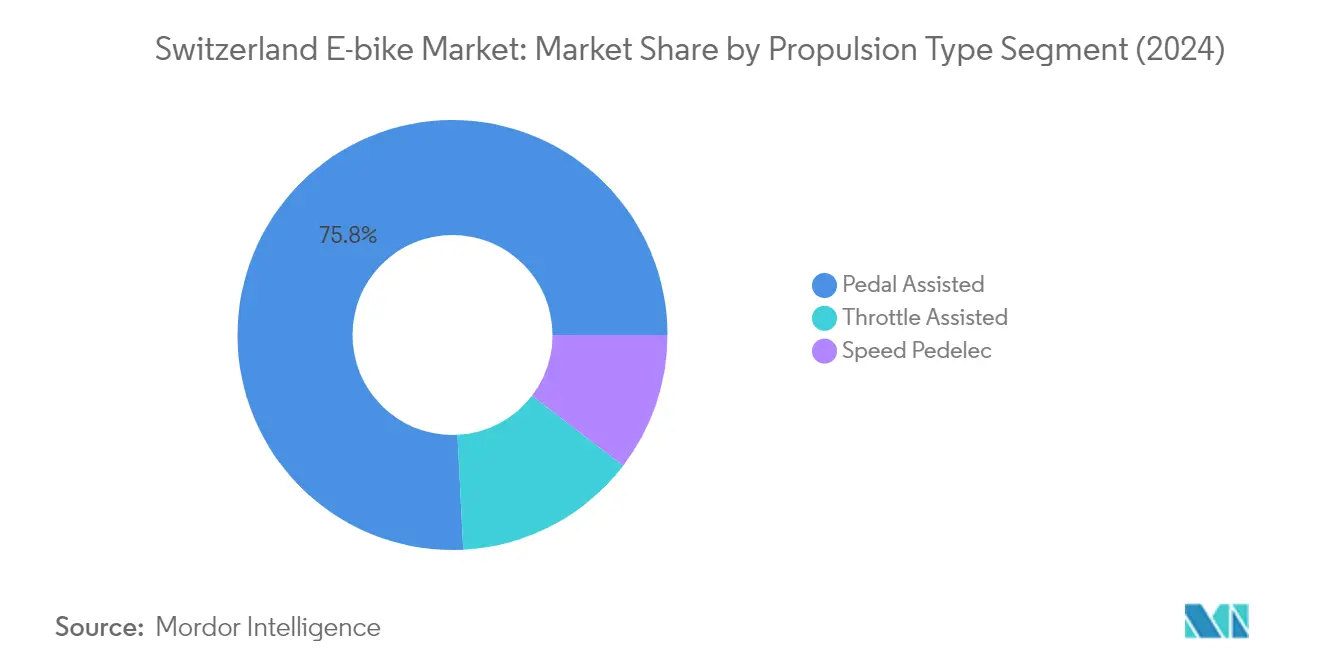

The pedal-assisted e-bike segment dominates the Switzerland e-bike market, commanding approximately 76% market share in 2024. This significant market position is attributed to several key advantages that pedal-assisted e-bikes offer over other variants. These e-bikes feature greater motor power, enabling riders to pedal more easily and quickly while maintaining better control over their riding experience. The segment's popularity is particularly driven by its ability to provide smoother rides on hills, slope changes, and uneven terrain while reducing joint tension. The decreasing battery prices have helped make these bikes more accessible to a broader consumer base, while technological advancements have improved the overall user interface, allowing integration with smartphones for real-time information on speed and battery status.

Speed Pedelec Segment in Switzerland E-bike Market

The speed pedelec segment is projected to exhibit the fastest growth in the Switzerland e-bike market, with an expected growth rate of approximately 8% during the forecast period 2024-2029. This accelerated growth is primarily driven by the increasing demand for recreational activities like off-road riding and long-distance travel, coupled with a growing preference for bikes over cars for daily commutes. The segment's expansion is further supported by Switzerland's unique regulations that facilitate obtaining licenses for e-bikes with maximum assisted speeds of over 45 km/h, differentiating it from other European markets. The rising interest in performance-based cycling and the segment's appeal to enthusiasts seeking faster commuting options in Switzerland's diverse terrain are expected to sustain this growth momentum.

Remaining Segments in Propulsion Type

The throttle-assisted segment represents a significant portion of the Swiss e-bike market, offering unique advantages for specific user groups and applications. These e-bikes are particularly valuable for navigating congested traffic or riding more quickly on country roads with switchbacks, making them ideal for users who prefer minimal pedaling effort. The segment particularly appeals to users with medical conditions that may limit their ability to pedal continuously, as well as those seeking a more motorcycle-like riding experience. However, regulatory requirements such as insurance, helmet usage, and licensing requirements influence this segment's adoption patterns in the Swiss market.

Segment Analysis: Application Type

City/Urban Segment in Switzerland E-bike Market

The electric city bike segment dominates the Switzerland e-bike market, commanding approximately 77% market share in 2024, driven by increasing environmental and health consciousness in urban areas. The segment's strong performance is supported by extensive development of dedicated bike lanes and infrastructure across major Swiss cities, including popular routes like Herzschlaufe Seetal, Herzroute, and Appenzeller Route. The growth is further bolstered by expanding e-bike sharing programs in major cities like Zurich, aimed at reducing traffic congestion and lowering CO2 emissions. Additionally, the segment benefits from strong adoption among students and working professionals who use e-bikes for daily commuting to educational institutions and workplaces, particularly in city centers and suburban areas where these bikes offer convenient navigation through congested streets.

Cargo/Utility Segment in Switzerland E-bike Market

The electric cargo bike segment is emerging as the fastest-growing category in the Swiss e-bike market, projected to expand at approximately 7.2% during 2024-2029. This remarkable growth is primarily driven by the increasing adoption of e-cargo bikes for last-mile deliveries and urban logistics solutions. The segment's expansion is supported by the fact that research indicates up to 25% of all goods and 50% of light deliveries in urban areas could be fulfilled by cargo bikes. The growth is further accelerated by the significantly lower operational costs compared to conventional fuel vehicles and small electric vans, making them an attractive option for businesses. Major companies like Amazon, Walmart, and IKEA are increasingly incorporating cargo e-bikes into their delivery fleets, setting a trend for sustainable urban logistics solutions.

Remaining Segments in Application Type

The Trekking segment represents a significant portion of the Swiss e-bike market, catering to adventure enthusiasts and recreational cyclists. This segment particularly benefits from Switzerland's mountainous terrain and extensive network of cycling trails, making it popular among both locals and tourists. The electric mountain bike segment is specifically designed to handle challenging terrains while providing assistance for longer rides, making them ideal for exploring Switzerland's diverse landscape. The segment's growth is supported by increasing interest in outdoor activities and adventure tourism, with manufacturers continuously introducing advanced features to enhance the riding experience in mountainous conditions.

Segment Analysis: Battery Type

Lithium-ion Battery Segment in Switzerland E-bike Market

The Lithium-ion electric bicycle battery segment dominates the Switzerland e-bike market, commanding approximately 100% market share in 2024, establishing itself as both the largest and fastest-growing segment. This overwhelming dominance can be attributed to several key advantages that lithium-ion batteries offer over other battery types, including their superior capacity-to-weight ratio, longer lifespan, and minimal maintenance requirements. The segment's growth is further bolstered by continuous technological advancements and declining battery prices, making them increasingly cost-effective for manufacturers and consumers alike. Key market players are heavily investing in research and development to improve battery performance, focusing on aspects such as faster charging capabilities, extended range, and enhanced durability. The integration of smart features and battery management systems has also contributed to the segment's dominance, allowing for better monitoring and optimization of battery performance. Additionally, the growing emphasis on environmental sustainability and the push towards cleaner transportation solutions has reinforced the preference for lithium-ion batteries in e-bikes, as they offer a more eco-friendly alternative compared to traditional battery technologies.

Competitive Landscape

Top Companies in Switzerland E-bike Market

The Swiss e-bike market is characterized by intense competition and continuous innovation among key players like Swiss E-Mobility Group (SEMG), CUBE Bikes, Canyon Bicycle, and Maxon Motor AG. Companies are actively pursuing product development initiatives, launching new models with advanced features such as improved battery life, enhanced motor efficiency, and smart connectivity options. Operational agility is demonstrated through flexible manufacturing processes and robust supply chain management, allowing companies to adapt quickly to changing market demands. Strategic partnerships, particularly in technology development and distribution networks, have become increasingly important for maintaining a competitive advantage. Market expansion strategies focus on strengthening dealer networks, establishing experience centers, and developing direct-to-consumer channels, while also emphasizing after-sales service excellence and customer support infrastructure.

Mix of Global and Local Specialists

The Swiss e-bike market presents a diverse competitive landscape featuring both established global manufacturers and specialized local players. International conglomerates like Pon.Bike and Trek Fahrrad bring extensive resources and global manufacturing capabilities, while local specialists such as myStromer AG and BMC Switzerland leverage their deep understanding of Swiss consumer preferences and terrain requirements. The market structure shows moderate consolidation, with larger players acquiring smaller innovative companies to expand their technological capabilities and market reach, as exemplified by TVS Motor Company's acquisition of Swiss E-Mobility Group.

Market dynamics are shaped by a combination of traditional bicycle manufacturers transitioning into electric bike production and pure-play e-bike specialists emerging with innovative offerings. Companies are increasingly focusing on vertical integration, from research and development to distribution, to maintain quality control and optimize costs. The competitive environment is further characterized by strategic alliances between manufacturers and technology providers, particularly in developing advanced battery systems and motor technologies, creating barriers to entry for new market entrants.

Innovation and Localization Drive Future Success

Success in the Swiss e-bike market increasingly depends on companies' ability to balance technological innovation with local market adaptation. Incumbent players must focus on continuous product development, particularly in areas such as battery efficiency, motor performance, and smart features, while maintaining strong relationships with dealers and service networks. Building brand loyalty through superior customer experience, comprehensive warranty programs, and efficient after-sales service will be crucial for maintaining market position. Companies must also invest in sustainable manufacturing practices and circular economy initiatives to align with Swiss environmental standards and consumer preferences.

For contenders looking to gain market share, differentiation through specialized product offerings and innovative business models will be essential. This includes developing niche-specific e-bikes for urban commuting, cargo delivery, or mountain biking, and implementing flexible ownership models such as subscription services. Success will also depend on navigating the regulatory landscape, particularly regarding speed limitations, battery disposal, and safety standards. Companies must consider the growing influence of e-bike sharing platforms and potential shifts in urban mobility policies while building resilient supply chains to mitigate future disruptions.

Switzerland E-bike Industry Leaders

Canyon Bicycle

CUBE Bikes

Maxon Motor AG

Pon.Bike (Schweiz) GmbH

Swiss E-Mobility Group (SEMG)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2022: BMC Switzerland and Uniqo, a company that creates custom aero equipment, partnered to cater to the current trends in custom aero bars and extensions in professional cycling.

- November 2022: BMC unveiled the new Roadmachine 01 AMP X road e-bike, which features a fork and frame made of high-quality carbon fiber with internal cable routing.

- September 2022: BMC introduced the Kaius 01 carbon gravel bike to achieve the ideal blend of stiffness, lightweight, and front-end stability. This bike is constructed with a carbon layup and gravel-specific geometry.

Switzerland E-bike Market Report Scope

Pedal Assisted, Speed Pedelec, Throttle Assisted are covered as segments by Propulsion Type. Cargo/Utility, City/Urban, Trekking are covered as segments by Application Type. Lead Acid Battery, Lithium-ion Battery, Others are covered as segments by Battery Type.Propulsion Type

| Pedal Assisted |

| Speed Pedelec |

| Throttle Assisted |

Application Type

| Cargo/Utility |

| City/Urban |

| Trekking |

Battery Type

| Lead Acid Battery |

| Lithium-ion Battery |

| Others |

| Propulsion Type | Pedal Assisted |

| Speed Pedelec | |

| Throttle Assisted | |

| Application Type | Cargo/Utility |

| City/Urban | |

| Trekking | |

| Battery Type | Lead Acid Battery |

| Lithium-ion Battery | |

| Others |

Need A Different Region or Segment?

Customize Now

Market Definition

- By Application Type - E-bikes considered under this segment include city/urban, trekking, and cargo/utility e-bikes. The common types of e-bikes under these three categories include off-road/hybrid, kids, ladies/gents, cross, MTB, folding, fat tire, and sports e-bike.

- By Battery Type - This segment includes lithium-ion batteries, lead-acid batteries, and other battery types. The other battery type category includes nickel-metal hydroxide (NiMH), silicon, and lithium-polymer batteries.

- By Propulsion Type - E-bikes considered under this segment include pedal-assisted e-bikes, throttle-assisted e-bikes, and speed pedelec. While the speed limit of pedal and throttle-assisted e-bikes is usually 25 km/h, the speed limit of speed pedelec is generally 45 km/h (28 mph).

| Keyword | Definition |

|---|---|

| Pedal Assisted | Pedal-assist or pedelec category refers to the electric bikes that provide limited power assistance through torque-assist system and do not have throttle for varying the speed. The power from the motor gets activated upon pedaling in these bikes and reduces human efforts. |

| Throttle Assisted | Throttle-based e-bikes are equipped with the throttle assistance grip, installed on the handlebar, similarly to motorbikes. The speed can be controlled by twisting the throttle directly without the need to pedal. The throttle response directly provides power to the motor installed in the bicycles and speeds up the vehicle without paddling. |

| Speed Pedelec | Speed pedelec is e-bikes similar to pedal-assist e-bikes as they do not have throttle functionality. However, these e-bikes are integrated with an electric motor which delivers power of approximately 500 W and more. The speed limit of such e-bikes is generally 45 km/h (28 mph) in most of the countries. |

| City/Urban | The city or urban e-bikes are designed with daily commuting standards and functions to be operated within the city and urban areas. The bicycles include various features and specifications such as comfortable seats, sit upright riding posture, tires for easy grip and comfortable ride, etc. |

| Trekking | Trekking and mountain bikes are special types of e-bikes that are designed for special purposes considering the robust and rough usage of the vehicles. These bicycles include a strong frame, and wide tires for better and advanced grip and are also equipped with various gear mechanisms which can be used while riding in different terrains, rough grounded, and tough mountainous roads. |

| Cargo/Utility | The e-cargo or utility e-bikes are designed to carry various types of cargo and packages for shorter distances such as within urban areas. These bikes are usually owned by local businesses and delivery partners to deliver packages and parcels at very low operational costs. |

| Lithium-ion Battery | A Li-ion battery is a rechargeable battery, which uses lithium and carbon as its constituent materials. The Li-Ion batteries have a higher density and lesser weight than sealed lead acid batteries and provide the rider with more range per charge than other types of batteries. |

| Lead Acid Battery | A lead acid battery refers to sealed lead acid battery having a very low energy-to-weight and energy-to-volume ratio. The battery can produce high surge currents, owing to its relatively high power-to-weight ratio as compared to other rechargeable batteries. |

| Other Batteries | This includes electric bikes using nickel–metal hydroxide (NiMH), silicon, and lithium-polymer batteries. |

| Business-to-Business (B2B) | The sales of e-bikes to business customers such as urban fleet and logistics company, rental/sharing operators, last-mile fleet operators, and corporate fleet operators are considered under this category. |

| Business-to-Customers (B2C) | The sales of electric scooters and motorcycles to direct consumers is considered under this category. The consumers acquire these vehicles either directly from manufacturers or from other distributers and dealers through online and offline channel. |

| Unorganized Local OEMs | These players are small local manufacturers and assemblers of e-bikes. Most of these manufacturers import the components from China and Taiwan and assemble them locally. They offer the product at low cost in this price sensitive market which give them advantage over organized manufacturers. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Dockless e-Bikes | Electric bikes that have self-locking mechanisms and a GPS tracking facility with an average top speed of around 15mph. These are mainly used by bike-sharing companies such as Bird, Lime, and Spin. |

| Electric Vehicle | A vehicle which uses one or more electric motors for propulsion. Includes cars, scooters, buses, trucks, motorcycles, and boats. This term includes all-electric vehicles and hybrid electric vehicles |

| Plug-in EV | An electric vehicle that can be externally charged and generally includes all-electric vehicles as well as plug-in hybrids. In this report we use the term for all-electric vehicles to differentiate them from plug-in hybrid electric vehicles. |

| Lithium-Sulphur Battery | A rechargeable battery that replaces the liquid or polymer electrolyte found in current lithium-ion batteries with sulfur. They have more capacity than Li-ion batteries. |

| Micromobility | Micromobility is one of the many modes of transport involving very-light-duty vehicles to travel short distances. These means of transportation include bikes, e-scooters, e-bikes, mopeds, and scooters. Such vehicles are used on a sharing basis for covering short distances, usually five miles or less. |

| Low Speed Electric Vehicls (LSEVs) | They are low speed (usually less than 25 kmph) light vehicles that do not have an internal combustion engine, and solely use electric energy for propulsion. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF