| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 8.45 Billion |

| Market Size (2030) | USD 12.08 Billion |

| CAGR (2025 - 2030) | 7.41 % |

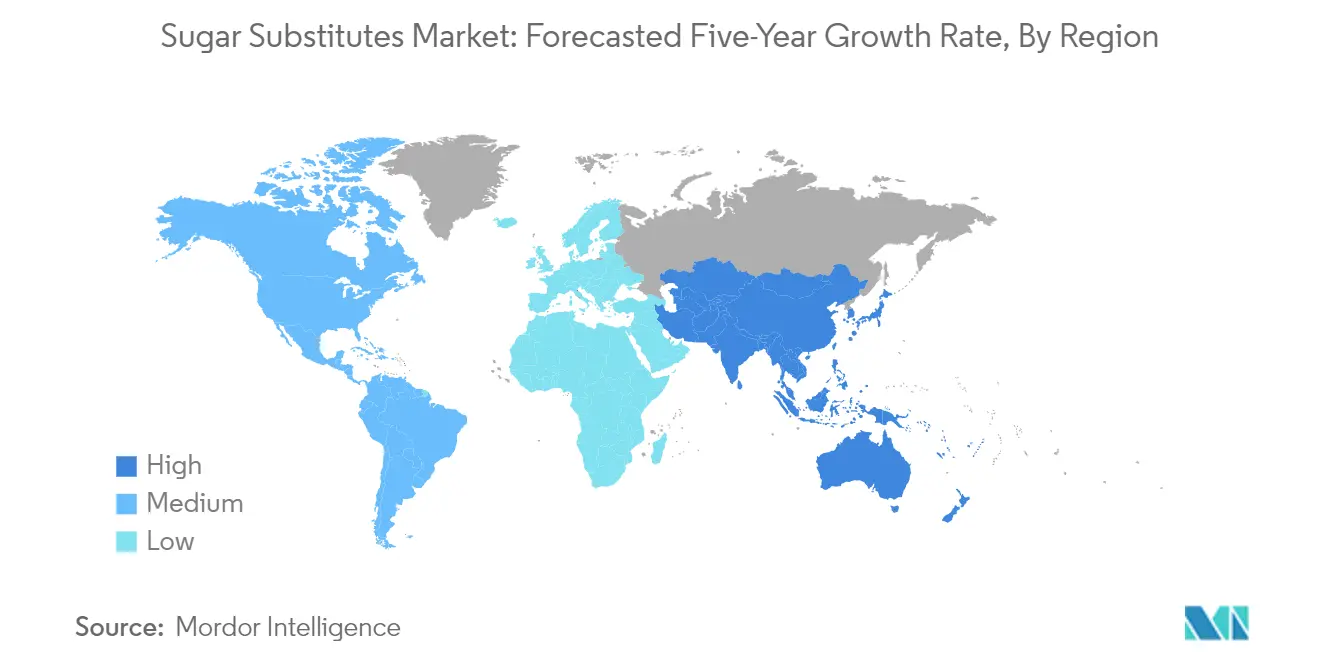

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

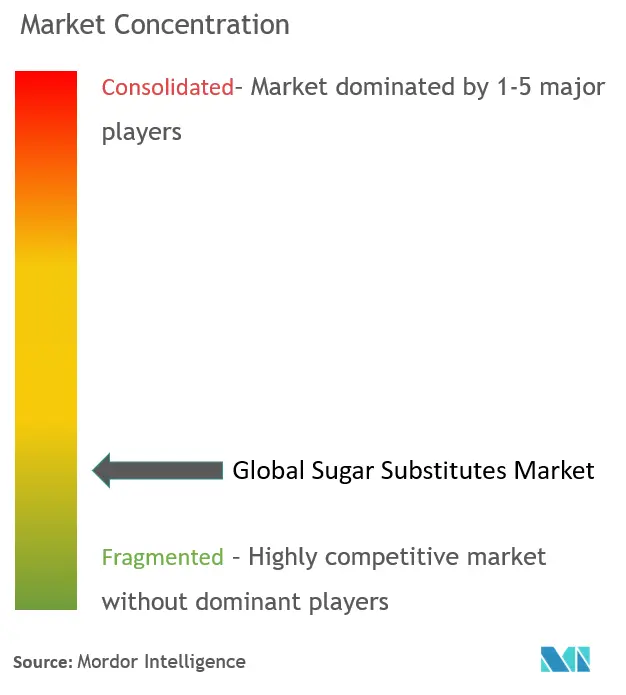

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Sugar Substitutes Market Analysis

The Sugar Substitutes Market size is estimated at USD 8.45 billion in 2025, and is expected to reach USD 12.08 billion by 2030, at a CAGR of 7.41% during the forecast period (2025-2030).

The sugar substitute industry is experiencing significant transformation driven by evolving consumer preferences and regulatory developments. Major health organizations and governments worldwide are implementing stricter guidelines regarding sweetener consumption, exemplified by the World Health Organization's landmark decision in August 2023 to caution against the use of artificial sweeteners for weight control. This regulatory scrutiny has accelerated innovation in natural sweetener alternatives, with manufacturers increasingly focusing on clean-label solutions. The industry has also witnessed substantial investments in sustainable production methods, with companies like Splenda establishing domestic stevia farming operations in March 2023 to ensure supply chain transparency and meet growing demand.

The market landscape is being reshaped by generational shifts in consumer preferences and heightened health awareness. According to the International Food Information Council's 2022 report, there are distinct generational differences in sweetener preferences, with 31% of Gen Z and 30% of Millennials showing a strong inclination towards low or no-calorie sweeteners, compared to 23% of Gen X consumers. This demographic variation has prompted manufacturers to diversify their product portfolios and develop targeted marketing strategies. The industry has responded with innovative formulations that address both taste and health concerns, leading to increased research and development investments in natural sweetener technologies.

Technological advancements in sweetener production and formulation have become a crucial differentiator in the market. Companies are investing in proprietary extraction and purification technologies to improve the taste profile of natural sweeteners while maintaining their health benefits. For instance, Tate & Lyle's launch of TASTEVIA SOL Stevia Sweetener in July 2023 represents a breakthrough in stevia technology, addressing previous limitations in solubility and taste. These innovations are enabling manufacturers to achieve higher sugar reduction levels while maintaining consumer acceptance.

According to Kerry Group's 2023 report, 86% of consumers express concern about sugar overconsumption leading to diabetes, driving demand for alternative sweetening solutions. This heightened health consciousness has led to increased collaboration between ingredient manufacturers and food companies to develop application-specific sweetener solutions. The industry is witnessing a shift towards integrated approaches that combine different sweetener technologies to achieve optimal taste profiles while meeting clean-label requirements. Manufacturers are also investing in consumer education initiatives to build trust and understanding of various sweetener options, particularly focusing on natural sugar alternatives.

Sugar Substitutes Market Trends

Surging Consumer Inclination Toward Clean-Label Sugar Substitutes

The growing demand for clean labels and natural food products is gaining significant momentum, driven by increasing consumer awareness about the negative health effects of artificial ingredients. According to the 2022 Food and Health Survey, nearly three in four Americans (73%) are trying to limit (59%) or avoid (14%) sugars, with two-thirds (67%) specifically targeting added sugars. This heightened awareness has prompted manufacturers to replace polyols with sugar substitutes, particularly in the Asia-Pacific region, where over two-thirds (69%) of consumers have expressed interest in switching from artificial sweeteners to natural alternatives, according to a 2021 Tate & Lyle Ingredients Tracker survey.

The popularity of natural sweeteners has been rising steadily, with stevia gaining particular prominence due to its clean label appeal. Sugar alcohols like sorbitol and maltitol are being rapidly replaced by natural sweeteners like stevia due to their association with digestive problems. Leading players in the natural substitute for sugar market are expanding their presence in emerging markets through innovation and strategic launches. For instance, in June 2023, Tate & Lyle PLC launched TASTEVIA SOL Stevia Sweetener, an internationally patent-protected breakthrough in stevia technology, aimed at helping customers solve stevia solubility issues while delivering on consumer demand for healthier and tastier sugar and calorie-reduced products.

Understand The Key Trends Shaping This Market

Download PDF

Shift Toward Convenience and Processed Food and Beverage Consumption

The increasing demand for convenience and processed foods, such as ready-to-eat foods, ready-to-drink beverages, snacks, and frozen meals, is driving significant growth in the food additives market, including sugar alternatives. Sugar substitutes have become ubiquitous ingredients in products like ketchup, whole-wheat bread, salad dressing, yogurt, breakfast cereals, and beverages, with high-intensity sweeteners playing a particularly crucial role as they are 200 to 20,000 times sweeter than regular sugar. This allows manufacturers to incorporate sugar alternatives into numerous processed foods and beverages without altering the taste.

The consumption of high-intensity sweeteners in developed regions is experiencing substantial growth, particularly in the diet beverages market. Manufacturers are increasingly adopting strategies to meet this growing demand through innovative product launches. For instance, in February 2022, Sweegen launched its novel, high-intensity brazzein sweetener, which offers a sweetening effect of 500-2,000 times that of regular sugar, making it an ideal choice for processed food applications. Energy drinks containing high-intensity sweeteners have also gained significant traction, with brands like Red Bull using aspartame and acesulfame potassium, Celsius incorporating stevia leaf extracts, and Zevia utilizing organic stevia leaf extract.

Soaring Demand for Sugar Substitutes from Diabetic and Obese Populations

The escalating prevalence of diabetes and obesity worldwide has become a primary driver for the sugar substitutes market. According to a survey conducted in 2022, approximately 41% of respondents indicated they limit sugar intake to avoid weight gain, while 38% aim to improve their diet, and 35% seek to prevent future health conditions. This growing health consciousness has led consumers to actively seek natural sweeteners with zero calories to maintain their blood glucose levels, particularly driving the demand for products like stevia that align with these health-conscious requirements.

The food and beverage industry has responded to these health concerns by introducing products containing natural low-calorie sweeteners, particularly focusing on stevia-based ingredients. Leading players are working on offering unique next-generation zero-calorie sweeteners that allow individuals with obesity or diabetes to indulge in sweetness while maintaining lifestyle goals. For instance, in April 2021, Manus Bio introduced the next generation of "Natural zero-calorie sweeteners" under its brand NutraSweet Naturals in the United States. The company emphasizes that its plant-based, zero-calorie, 100-percent pure-tasting sweetener can be incorporated into everyday lifestyles, particularly targeting health-conscious consumers and those managing diabetes and obesity.

Segment Analysis: By Product Type

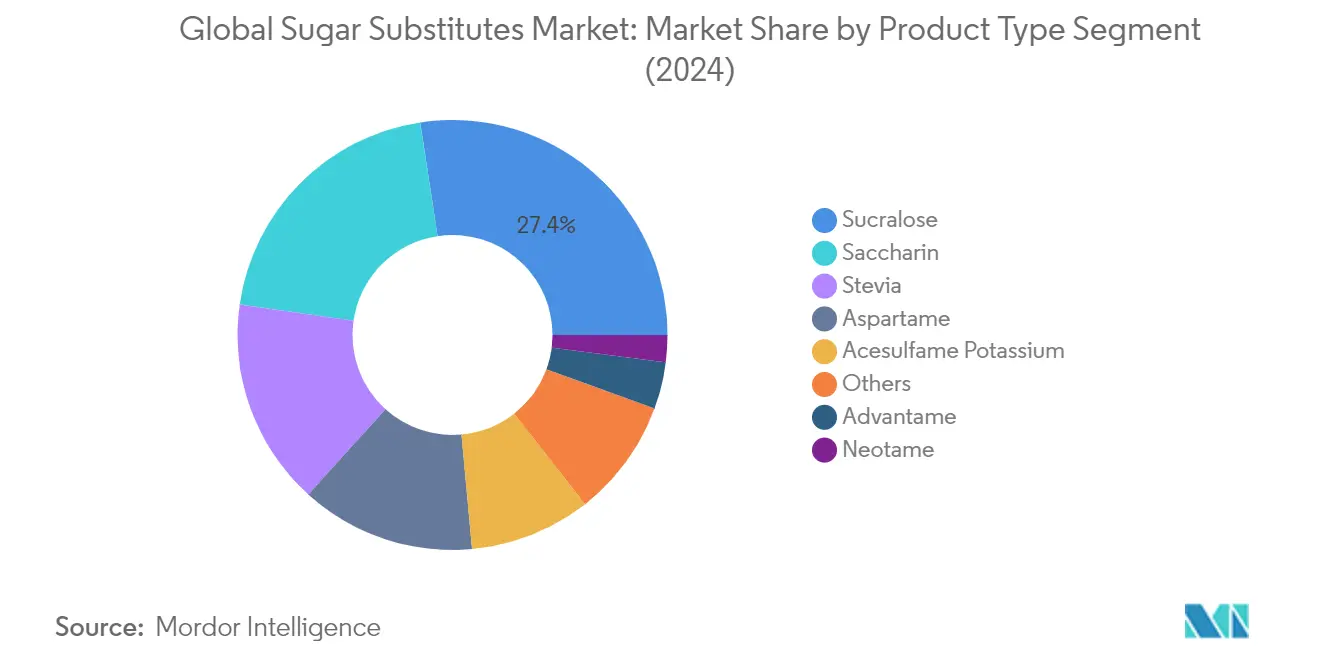

Sucralose Segment in Global Sugar Substitutes Market

The sucralose market segment continues to dominate the global sugar substitutes market, holding approximately 27% market share in 2024. This significant market position is primarily driven by sucralose's extensive adoption in various end-use applications, including pharmaceuticals, food, and beverages, and its growing demand as a food-retaining agent and nutritional supplement in pharmaceutical syrups and injections. The segment's leadership is further strengthened by strong research and development activities combined with technical capabilities that have put manufacturers at the forefront of innovation. The versatility of sucralose in different applications, its heat stability, and long shelf life have made it particularly attractive to food and beverage manufacturers. Additionally, the constant demand from the food and beverage industry to use sucralose sweetener in various products, including bakery items, health drinks, juice, and confectionery, has significantly contributed to its market dominance.

Stevia Segment in Global Sugar Substitutes Market

The stevia segment is emerging as the fastest-growing segment in the global sugar substitutes market, with an expected growth rate of approximately 8% during 2024-2029. This remarkable growth trajectory is driven by increasing consumer preference for natural and plant-derived sweeteners, particularly among health-conscious consumers looking to lower calorie intake or manage blood sugar levels. Stevia's appeal as a natural substitute for artificial sweeteners has been further enhanced by its versatility in various applications, from beverages to baked goods. The segment's growth is also supported by ongoing innovations in stevia formulations that improve taste profiles and reduce bitter aftertaste. Major food and beverage manufacturers are increasingly incorporating stevia into their product portfolios, responding to the growing consumer demand for natural, zero-calorie sweetening solutions. The segment's expansion is further bolstered by its sustainability credentials and the increasing focus on clean-label ingredients in the food and beverage industry.

Remaining Segments in Sugar Substitutes Market by Product Type

The sugar substitutes market encompasses several other significant segments, including saccharin, aspartame, acesulfame potassium, advantame, and neotame, each serving specific market needs and applications. Saccharin maintains a strong presence in the market due to its cost-effectiveness and widespread use in pharmaceuticals and oral care products. Aspartame continues to be a crucial player, particularly in the beverage industry, owing to its sugar-like taste profile. Acesulfame potassium has gained traction due to its stability in various food processing conditions and synergistic effects when combined with other sweeteners. Advantame, despite its smaller market share, is valued for its intense sweetening power and clean taste profile. Neotame, while having a smaller market presence, offers unique advantages in specific applications due to its high sweetness intensity and heat stability. These segments collectively contribute to the market's diversity and cater to various industry-specific requirements and consumer preferences.

Segment Analysis: Application

Beverage Segment in Global Sugar Substitutes Market

The beverage segment continues to dominate the global sugar substitutes market, holding approximately 41% market share in 2024. This significant market position is primarily driven by the increasing consumer demand for low-calorie and sugar-free beverages across both carbonated and non-carbonated categories. Sugar substitutes like acesulfame potassium, advantame, aspartame, neotame, saccharin, sucralose, and stevia are commonly used in beverages such as soft drinks, energy drinks, and flavored water. The segment's growth is further bolstered by regulatory pressure in the form of sugar taxes driving global F&B brands to adopt sweeteners in their beverage value chain. For instance, in France, soft drinks are up to 3.5% more expensive as taxes are applied to drinks with added sugars. The increasing concerns about excessive sugar consumption and the corresponding rise of sugar-related diseases have prompted beverage manufacturers to turn to sweeteners as sugar alternatives, as they are many times sweeter than sugar but contribute minimal to no calories when added to beverages.

Food Segment in Global Sugar Substitutes Market

The food segment is projected to witness the fastest growth in the sugar substitutes market, with an expected growth rate of approximately 5% during 2024-2029. This accelerated growth is attributed to the expanding applications across various food categories, including baked foods, cereals, confectionery, dairy alternatives, and sauces. Manufacturers are increasingly incorporating sugar additives in food products to meet the growing consumer demand for healthier alternatives while maintaining taste profiles. The segment's growth is particularly notable in categories like dairy products, where sugar substitutes help enhance scoopability and sweetness while improving softness and re-crystallization rates in creamy or delicate fruit flavors. The confectionery sector is also witnessing significant adoption, with sugar substitutes being used in products like sugar-free gums, caramels, and chocolates, catering to the growing health-conscious consumer base seeking reduced-sugar options.

Remaining Segments in Application Segmentation

The pharmaceuticals segment plays a crucial role in the sugar substitutes market, where sweeteners are extensively used as excipients to improve taste perception and mask the bitter taste of medications. In the pharmaceutical industry, sugar substitutes are utilized in various applications, including liquid medications, chewable tablets, and orally disintegrating tablets. The segment's importance is particularly evident in the preparation of liquid oral preparations, syrup bases, and coating of pills and tablets. The low-calorie value of these substitutes makes them especially suitable for pharmaceutical applications targeting overweight individuals and those with dietary restrictions. Natural sweeteners in this segment are gaining increased attention due to their lower toxicity compared to artificial sweeteners, contributing to the segment's steady growth in the overall market.

Sugar Substitutes Market Geography Segment Analysis

Sugar Substitutes Market in North America

The North American sugar substitutes market demonstrates robust growth driven by increasing health consciousness and the rising prevalence of diabetes and obesity. The region's market is characterized by strong research and development activities, particularly in natural sweeteners like stevia and monk fruit. The United States, Canada, and Mexico form the key markets, with manufacturers focusing on product innovations and clean-label solutions. The regulatory environment, particularly the FDA's approval processes for new sweeteners, plays a crucial role in shaping market dynamics. Consumer preference for natural and organic alternatives to artificial sweeteners continues to influence product development and marketing strategies across these countries.

Sugar Substitutes Market in the United States

The United States dominates the North American sugar substitutes market, holding approximately 74% of the regional market share. The market is driven by stringent regulations on sugar consumption and increasing consumer awareness about health issues. The country's food and beverage industry actively incorporates sugar substitutes in various products, from soft drinks to baked goods. Major manufacturers are focusing on developing innovative natural sweeteners to meet the growing demand for clean-label products. The presence of key market players and their extensive distribution networks further strengthens the market position. The rising diabetic population and increasing obesity rates continue to drive the demand for sugar alternatives across various applications.

Sugar Substitutes Market in Mexico

Mexico emerges as the fastest-growing market in North America, with a projected growth rate of approximately 4% during 2024-2029. The country's market growth is primarily driven by increasing health consciousness and government initiatives to combat obesity and diabetes. Mexican consumers are increasingly adopting sugar-free and reduced-sugar products, particularly in beverages and processed foods. The market benefits from the presence of both international and local manufacturers who are expanding their product portfolios to meet the growing demand. Recent regulatory changes and increasing awareness about health issues related to sugar consumption continue to drive market expansion. The country's food and beverage industry is actively incorporating various sugar substitutes in new product developments.

Sugar Substitutes Market in Europe

The European sugar substitutes market showcases significant growth potential, driven by stringent regulations on sugar content in food and beverages. The region's market is characterized by strong consumer awareness about health issues and a preference for natural sweeteners. Key markets including Germany, the United Kingdom, France, Spain, Italy, and Russia demonstrate varying adoption rates of sugar substitutes. The European Food Safety Authority's regulations and approvals significantly influence market dynamics. Manufacturers across these countries focus on developing innovative solutions that align with the clean-label trend and meet specific consumer preferences in different markets.

Sugar Substitutes Market in Germany

Germany leads the European sugar substitutes market, commanding approximately 21% of the regional market share. The country's market is characterized by strong research and development activities in natural sweeteners and innovative sugar reduction solutions. German consumers show a strong preference for natural and organic alternatives, driving manufacturers to develop clean-label products. The presence of major food and beverage manufacturers and their focus on sugar reduction strategies strengthens the market. The country's robust food processing industry and increasing health consciousness among consumers continue to drive market growth.

Sugar Substitutes Market in Germany - Growth Perspective

Germany also emerges as the fastest-growing market in Europe, with a projected growth rate of approximately 4% during 2024-2029. The growth is driven by increasing consumer awareness about sugar-related health issues and strong government support for sugar reduction initiatives. German manufacturers are actively investing in research and development of innovative sugar substitutes, particularly focusing on natural alternatives. The country's strong focus on sustainability and clean-label products continues to drive market expansion. The growing preference for healthier alternatives in the food and beverage industry further supports market growth.

Sugar Substitutes Market in Asia-Pacific

The Asia-Pacific sugar substitutes market demonstrates significant growth potential, driven by increasing health consciousness and rising disposable incomes. The region encompasses diverse markets including China, Japan, India, and Australia, each with unique consumer preferences and regulatory frameworks. The market benefits from the growing food and beverage industry and increasing adoption of Western dietary habits. Manufacturers are focusing on developing cost-effective solutions while maintaining quality standards. The region's large population base and increasing awareness about health issues provide substantial growth opportunities.

Sugar Substitutes Market in China

China dominates the Asia-Pacific sugar substitutes market, leading both in market size and production capacity. The country's market benefits from extensive manufacturing capabilities and strong research and development infrastructure. Chinese manufacturers are increasingly focusing on developing high-quality stevia and other natural sweeteners. The growing food and beverage industry and increasing health consciousness among consumers drive market growth. The country's robust supply chain and distribution networks further strengthen its market position.

Sugar Substitutes Market in China - Growth Perspective

China maintains its position as the fastest-growing market in Asia-Pacific, demonstrating remarkable growth potential. The market benefits from increasing health awareness and government initiatives to reduce sugar consumption. Chinese manufacturers are actively investing in research and development of innovative sugar substitutes. The country's large consumer base and growing demand for healthier alternatives in food and beverages drive market expansion. The strong focus on natural and clean-label products continues to shape market development.

Sugar Substitutes Market in South America

The South American sugar substitutes market shows promising growth potential, with Brazil and Argentina emerging as key markets. The region's market is driven by increasing health consciousness and government initiatives to reduce sugar consumption. Brazil leads the market in terms of size, while also demonstrating strong growth potential. The market benefits from the presence of both international and local manufacturers who are expanding their product portfolios. Consumer awareness about health issues and the growing food and beverage industry continue to drive market growth. The region's regulatory environment and increasing adoption of sugar-free products shape market dynamics.

Sugar Substitutes Market in Middle East and Africa

The Middle East and Africa sugar substitutes market demonstrates significant growth potential, with South Africa and the United Arab Emirates as key markets. The region's market is characterized by increasing health consciousness and the growing prevalence of lifestyle-related diseases. The United Arab Emirates leads the market in terms of size, while also showing strong growth potential. The market benefits from increasing urbanization and Western dietary influences. Consumer awareness about health issues and the growing food and beverage industry continue to drive market growth. The region's regulatory environment and increasing adoption of sugar-free products shape market dynamics.

Get Analysis on Important Geographic Markets

Download PDF

Sugar Substitutes Industry Overview

Top Companies in Sugar Substitutes Market

The global sugar substitutes market is characterized by intense innovation and strategic developments among key players like Ajinomoto, Tate & Lyle, Ingredion, and Cargill. Companies are heavily investing in research and development to create novel sweetening solutions, particularly focusing on natural alternatives like stevia and monk fruit extracts. The industry witnesses frequent product launches targeting specific application areas such as beverages, bakery, and confectionery, with emphasis on clean-label and organic offerings. Operational excellence is being achieved through vertical integration of supply chains, particularly in stevia production, while strategic partnerships with agricultural producers ensure consistent raw material supply. Market leaders are expanding their geographical presence through distribution partnerships and facility expansions, particularly in emerging markets across Asia-Pacific and Latin America, while simultaneously strengthening their position in established markets through acquisitions and joint ventures.

Consolidated Market with Strong Regional Players

The sugar substitutes market exhibits a unique competitive structure where global conglomerates coexist with specialized regional manufacturers. Major multinational companies leverage their extensive research capabilities, established distribution networks, and diverse product portfolios to maintain market leadership, while regional players capitalize on their local market knowledge and specialized product offerings. The market demonstrates moderate consolidation, with the top players holding significant market share, though numerous smaller players maintain strong positions in specific regional markets or niche product segments. The industry's competitive dynamics are further shaped by the presence of ingredient specialists focusing exclusively on natural sweeteners.

The market has witnessed significant merger and acquisition activity, primarily driven by large companies seeking to expand their natural sweetener portfolios and strengthen their regional presence. Companies are increasingly pursuing strategic acquisitions to gain access to proprietary technologies, particularly in stevia processing and taste modification. Vertical integration has emerged as a key trend, with major players acquiring or partnering with raw material suppliers to ensure supply chain control and maintain quality standards. These consolidation activities are reshaping the competitive landscape, leading to increased market concentration while simultaneously fostering innovation through the integration of complementary capabilities.

Innovation and Sustainability Drive Future Success

Success in the sugar substitute industry increasingly depends on companies' ability to align with evolving consumer preferences and regulatory requirements. Market leaders are strengthening their positions through continuous investment in research and development, focusing on improving taste profiles and developing novel extraction technologies. Companies are also establishing strong sustainability credentials through responsible sourcing practices and environmental stewardship programs. The ability to provide comprehensive sweetening solutions, rather than individual ingredients, has become crucial for maintaining market share, while developing application-specific formulations helps in penetrating new market segments.

For emerging players and market contenders, success lies in identifying and exploiting niche market opportunities while building strong intellectual property portfolios. Companies must navigate complex regulatory environments across different regions while maintaining cost competitiveness through operational efficiency. The market's future will be shaped by players' ability to address growing end-user demands for natural, clean-label products while managing substitution risks from emerging sweetener technologies. Building strong relationships with food and beverage manufacturers through technical support and customized solutions will be crucial for long-term success, as will the ability to adapt to potential regulatory changes regarding sweetener safety and labeling requirements. The role of artificial sweetener companies in this evolving landscape cannot be understated, as they continue to innovate and adapt to market demands.

Sugar Substitutes Market Leaders

-

Cargill Incorporated

-

Tate & Lyle PLC

-

Ajinomoto Co., Inc

-

Ingredion Incorporated

-

ADM

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Sugar Substitutes Market News

- July 2023: Tate & Lyle unveiled an exciting addition to its sweetener lineup, known as TASTEVA SOL Stevia Sweetener. This groundbreaking innovation, protected by international patents, significantly enhances the company's capacity to assist customers in addressing solubility challenges associated with stevia in the realm of food and beverages. Moreover, it contributes to meeting the growing consumer demand for healthier, more delectable, and lower-calorie sugar-reduced products.

- April 2022: Tate & Lyle responded to the soaring demand for allulose. This rare sugar has gained widespread popularity since the Food and Drug Administration's (FDA) decision to exclude it from the total and added sugars declarations on nutrition facts labels. In a bid to meet this increased demand, the company expanded its allulose production capabilities.

- March 2022: Cargill introduced its innovative line of stevia products, harnessing the power of EverSweet + ClearFlo technology. This cutting-edge sweetener system seamlessly integrates Cargill's stevia sweetener with natural flavors, offering an array of advantages, including the ability to modify flavor profiles, accelerate dispersion, and enhance solubility and stability within various formulations.

Sugar Substitutes Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Consumer Inclination Toward Clean-label Sugar Substitute

- 4.1.2 Demand For Sugar Substitutes From Diabetic and Obese Population

-

4.2 Market Restraints

- 4.2.1 Availability of Low-cost Sweeteners

-

4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Type

- 5.1.1 Acesulfame Potassium

- 5.1.2 Advantame

- 5.1.3 Aspartame

- 5.1.4 Neotame

- 5.1.5 Saccharin

- 5.1.6 Sucralose

- 5.1.7 Stevia

- 5.1.8 Other Types

-

5.2 Application

- 5.2.1 Food

- 5.2.1.1 Baked Foods and Cereals

- 5.2.1.2 Confectionery

- 5.2.1.3 Dairy and Dairy Alternatives

- 5.2.1.4 Sauces, Condiments, and Dressings

- 5.2.1.5 Othe r Food Applications

- 5.2.2 Beverage

- 5.2.3 Pharmaceuticals

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 Germany

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Most Active Companies

- 6.2 Most Adopted Strategies

- 6.3 Market Share Analysis

-

6.4 Company Profiles

- 6.4.1 Tate & Lyle PLC

- 6.4.2 Ingredion Inc.

- 6.4.3 Ajinomoto Co., Inc

- 6.4.4 Cargill Inc

- 6.4.5 Morita Kagaku Kogyo Co. Ltd

- 6.4.6 JK Sucralose Inc.

- 6.4.7 Manus Bio Inc.

- 6.4.8 Archer Daniels Midland Company

- 6.4.9 Xianghua GL Stevia Co

- 6.4.10 GLG Life Tech Corp.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Sugar Substitutes Industry Segmentation

Sugar substitutes are chemical or plant-based substances used to sweeten or enhance the flavor of food products and beverages.

The sugar substitute market is segmented by type, application, and geography. By type, the market is segmented into acesulfame potassium, advantame, aspartame, neotame, saccharin, sucralose, stevia, and others. By application, the market is segmented into food, beverage, and pharmaceuticals. The food segment is further segmented into baked foods and cereals, confectionery, dairy and dairy alternatives, sauces, condiments, and dressings, and other food applications. The report further analyses the market's global scenario, including a detailed analysis of North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Type | Acesulfame Potassium | ||

| Advantame | |||

| Aspartame | |||

| Neotame | |||

| Saccharin | |||

| Sucralose | |||

| Stevia | |||

| Other Types | |||

| Application | Food | Baked Foods and Cereals | |

| Confectionery | |||

| Dairy and Dairy Alternatives | |||

| Sauces, Condiments, and Dressings | |||

| Othe r Food Applications | |||

| Beverage | |||

| Pharmaceuticals | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Spain | ||

| United Kingdom | |||

| Germany | |||

| France | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | South Africa | ||

| United Arab Emirates | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Sugar Substitutes Market Research FAQs

How big is the Sugar Substitutes Market?

The Sugar Substitutes Market size is expected to reach USD 8.45 billion in 2025 and grow at a CAGR of 7.41% to reach USD 12.08 billion by 2030.

What is the current Sugar Substitutes Market size?

In 2025, the Sugar Substitutes Market size is expected to reach USD 8.45 billion.

Who are the key players in Sugar Substitutes Market?

Cargill Incorporated, Tate & Lyle PLC, Ajinomoto Co., Inc, Ingredion Incorporated and ADM are the major companies operating in the Sugar Substitutes Market.

Which is the fastest growing region in Sugar Substitutes Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Sugar Substitutes Market?

In 2025, the Asia Pacific accounts for the largest market share in Sugar Substitutes Market.

What years does this Sugar Substitutes Market cover, and what was the market size in 2024?

In 2024, the Sugar Substitutes Market size was estimated at USD 7.82 billion. The report covers the Sugar Substitutes Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Sugar Substitutes Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Sugar Substitutes Market Research

Mordor Intelligence offers a comprehensive analysis of the global sugar substitute industry. We leverage extensive expertise in tracking artificial sweetener trends and market dynamics. Our research covers the complete spectrum of sugar alternative products, including natural and synthetic sugar substitutes, sucralose, advantame, and allulose additives. The report provides detailed insights into the sugar substitute market. It analyzes both natural substitute for sugar products and artificial sweetener companies across various applications, such as beverages and food processing sectors.

Stakeholders benefit from our thorough examination of sugar replacement trends, competitive landscape analysis, and future market projections. The report, available as an easy-to-download PDF, covers crucial aspects such as trends in sweeteners, plant based sugar alternative developments, and emerging next generation sugar substitute innovations. Our analysis includes comprehensive coverage of sugar reducing ingredients across different regions. This provides valuable insights for manufacturers, investors, and industry participants. The report examines sugar substitutes examples and their applications, offering strategic recommendations for business growth and market expansion.