| Study Period | 2019 - 2030 |

| Market Volume (2025) | 328.20 kilotons |

| Market Volume (2030) | 420.87 kilotons |

| CAGR | 5.10 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players_-_Key_Players.webp "Styrene Ethylene Butylene Styrene (SEBS) Market Major Players")

*Disclaimer: Major Players sorted in no particular order |

Market Size")

Styrene Ethylene Butylene Styrene (SEBS) Market Analysis

The Styrene Ethylene Butylene Styrene Market size is estimated at 328.20 kilotons in 2025, and is expected to reach 420.87 kilotons by 2030, at a CAGR of 5.1% during the forecast period (2025-2030).

The global manufacturing landscape for styrene-ethylene-butylene-styrene (SEBS) continues to evolve, driven by shifting production patterns and technological advancements across multiple industries. The footwear sector, a significant consumer of SEBS, has demonstrated robust growth with global production reaching 23.9 billion pairs in 2022, indicating strong demand for SEBS in footwear applications. The material's versatility as a thermoplastic elastomer in providing flexibility, durability, and enhanced performance characteristics has led to its increased adoption in various manufacturing processes. The integration of SEBS in modern manufacturing has been particularly notable in regions with strong manufacturing bases, where its superior properties are leveraged for multiple applications.

The electronics industry has emerged as a crucial growth sector for SEBS applications, with significant developments in manufacturing capabilities and technological integration. This is evidenced by the remarkable 15% increase in electronics production in Russia during 2022, highlighting the growing importance of SEBS in electronic components and applications. The material's excellent electrical insulation properties and resistance to environmental factors have made it increasingly valuable in the production of electronic components, cables, and housing materials. The industry's focus on miniaturization and improved performance characteristics has further accelerated the adoption of SEBS as an elastic polymer in electronic applications.

Sustainability initiatives and environmental regulations have become increasingly influential in shaping the SEBS market landscape. Manufacturers are focusing on developing eco-friendly formulations and production processes to align with global sustainability goals. The material's recyclability and potential as a replacement for PVC in various applications has positioned it favorably in the context of circular economy initiatives. Industry players are investing in research and development to enhance the environmental profile of SEBS while maintaining its performance characteristics.

Regional manufacturing capabilities continue to evolve, with significant developments in key manufacturing hubs. According to the German Association of the Automotive Industry (VDA), Germany's production of 4.12 million units of passenger vehicles in 2023, representing a 21.2% increase, demonstrates the robust demand for SEBS in automotive applications. The material's use in automotive components, particularly in weather seals, window encapsulation, and interior trim applications, has grown significantly. This growth is supported by the material's ability to meet stringent performance requirements while offering design flexibility and durability as a polymer modifier and impact modifier.

Styrene Ethylene Butylene Styrene (SEBS) Market Trends

Increasing Investments in the Adhesives Industry

The adhesives industry has witnessed significant capital investments through new manufacturing facilities and capacity expansions, driving the demand for SEBS as a key raw material. Various expansion projects are being carried out globally by major manufacturers to meet the growing demand from end-user industries. For instance, in January 2024, adhesives manufacturer Greif announced the inauguration of a new adhesives manufacturing facility in Cincinnati, Ohio, to serve the growing demand from applications including tube and core construction, corrugated, boxboard, gypsum, and furniture manufacturing. Similarly, in September 2023, DuPont opened a new adhesives production facility in Zhangjiagang (ZJG), East China, focusing on serving customers in the transportation industry, primarily in lightweight and fast-growing vehicle electrification applications.

The investment momentum continued throughout 2023 with several other major developments in the adhesives sector. In June 2023, Henkel AG & Co. KGaA announced the opening of a new manufacturing facility for adhesives in Yantai Chemical Industry Park in Shandong Province, China, through which the company aims to manufacture high-impact adhesive products. Additionally, in August 2023, Henkel Korea completed the construction of high-impact electronics solutions for the Adhesive Technologies business unit in Songdo High-tech Industrial Cluster in Incheon, South Korea. These investments are complemented by strategic partnerships, such as Pidilite Industries Ltd's agreement to manufacture Germany-based Jowat's range of hot melts in India at their Vapi, Gujarat facility under the brand name Fevicol Jowat. The use of adhesive polymer and polymer compound technologies in these facilities highlights the industry's focus on innovation and quality.

Understand The Key Trends Shaping This Market

Download PDF

Growing Demand from the Automotive Industry

The automotive industry's robust growth and transformation towards electric vehicles have emerged as significant drivers for the SEBS market. According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), in 2023, around 93.55 million vehicles were produced worldwide, registering a substantial growth rate of 10% compared to 85.02 million vehicles in 2022. The passenger car segment showed particularly strong performance, with approximately 68 million units manufactured worldwide in 2023, marking an 11% increase compared to the previous year. This growth directly impacts SEBS demand, as it is extensively used in automotive applications such as weather seals, window encapsulation, glass run channels, static seals, interior trim, and instrument panel preparation.

The electric vehicle (EV) segment represents a particularly dynamic growth driver for SEBS consumption. Industry projections indicate that global EV sales are expected to reach 31 million units by 2027 and surge to 74.5 million units by 2035, representing a transformative shift in the automotive landscape. This transition is particularly evident in China, where the passenger EV market demonstrated remarkable growth with sales increasing by 87% year-over-year in 2022. Chinese brands like BYD, Wuling, Chery, Changan, and GAC have established strong market positions, with local brands commanding 81% of the market share. The Chinese government's target of achieving a 20% electric vehicle production penetration rate by 2025 further underscores the growth potential for SEBS in automotive applications, particularly in components specific to electric vehicles. The use of rubber compound and synthetic rubber materials in these applications is crucial for enhancing vehicle performance and sustainability.

Segment Analysis: Form

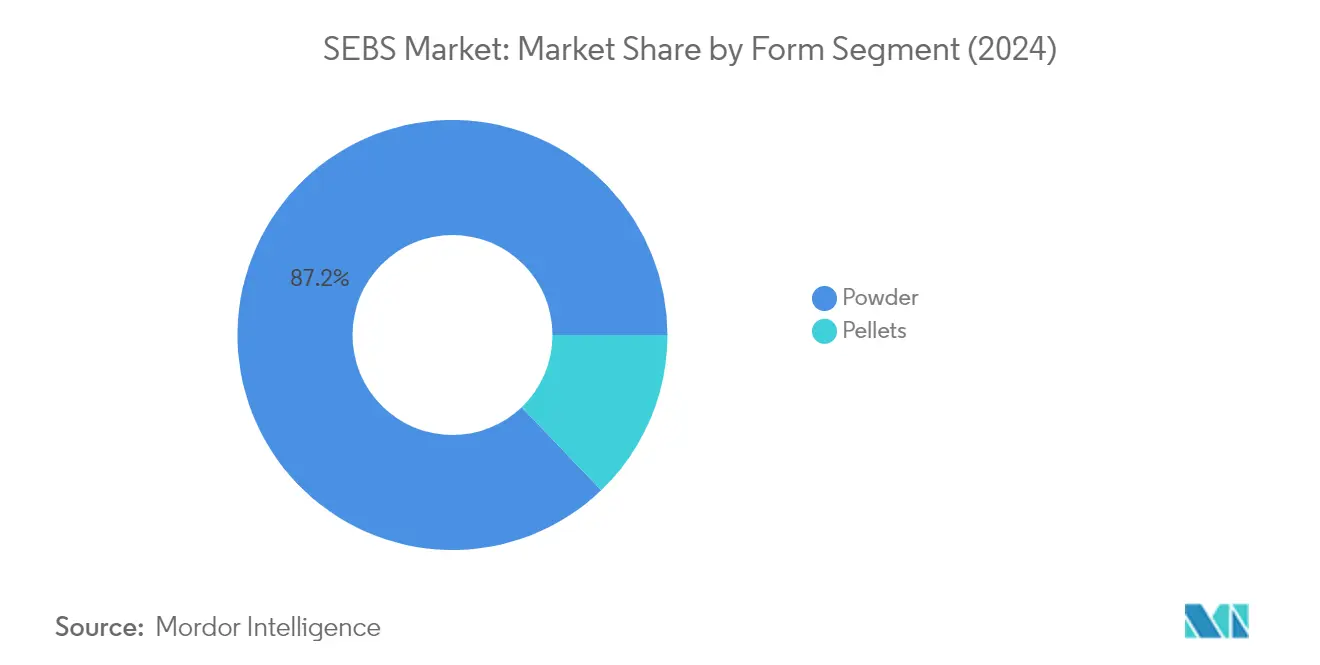

Powder Segment in Styrene Ethylene Butylene Styrene (SEBS) Market

The powder form dominates the global SEBS market, accounting for approximately 87% of the total market volume in 2024. This significant market share can be attributed to powder SEBS's superior properties, including high-temperature tolerance, excellent aging properties, good solubility, superior compounding performance, and exceptional oil absorption capabilities. The powder form is extensively used in various applications, particularly in adhesives and sealants manufacturing, where it plays a crucial role in pressure-sensitive adhesives for tapes, labels, and construction adhesives. Furthermore, the segment is projected to maintain its dominance with the fastest growth rate of around 5% during 2024-2029, driven by its increasing adoption in polymer modifier applications and rising demand from the automotive and electronics industries.

Pellets Segment in Styrene Ethylene Butylene Styrene (SEBS) Market

The pellet form of SEBS represents a smaller but significant segment of the market, offering unique advantages in specific applications. Manufactured using polyolefin plastics such as polyethylene (PE) and polypropylene (PP), SEBS pellets are particularly valued for their high strength, flexibility, and excellent temperature resistance properties. The segment finds extensive applications in various industries, including consumer goods, automotive parts, and building materials. Pellet-form SEBS is especially preferred in applications requiring direct processing and where consistent material flow is crucial. The segment's growth is supported by its increasing adoption in high-end applications where precise material properties and processing characteristics are essential, often serving as a plastic modifier.

Segment Analysis: End-User Industry

Adhesives and Sealants Segment in SEBS Market

The Adhesives and Sealants segment dominates the global Styrene Ethylene Butylene Styrene (SEBS) market, commanding approximately 19% of the total market share in 2024. This significant market position is driven by the extensive use of SEBS in various adhesive applications, including tapes, labels, and construction-based adhesives. The segment's dominance is further strengthened by SEBS's excellent properties, such as high shear strength, weathering resistance, and superior aging properties. Major companies like H.B. Fuller, Henkel AG, and DuPont have been expanding their adhesive manufacturing facilities globally, particularly in regions like China and Vietnam, indicating strong market growth potential. The powder form of SEBS is particularly popular in this segment due to its superior oil absorption and good solubility characteristics, making it ideal for pressure-sensitive and other adhesive applications.

Plastics Segment in SEBS Market

The Plastics segment is projected to be the fastest-growing segment in the SEBS market, with an expected growth rate of approximately 6% during the forecast period 2024-2029. This remarkable growth is attributed to the increasing adoption of SEBS in various thermoplastic applications, particularly in polystyrene, polyethylene, and polypropylene modifications. The segment's growth is driven by SEBS's ability to enhance impact strength, elastic properties, and low-temperature flexibility in plastic products. The expansion is further supported by growing investments in plastic manufacturing facilities globally, particularly in regions like China and India. The versatility of SEBS in plastic applications, ranging from food packaging to consumer electronics housings and automotive interiors, continues to drive its adoption in this segment, often serving as an impact modifier and thermoplastic elastomer.

Remaining Segments in End-User Industry

The other significant segments in the SEBS market include Automotive, Electrical & Electronics, Footwear, Sporting and Toys, and Roads and Railways. The Automotive segment benefits from SEBS's use in gaskets, seals, and weatherstripping applications. The Electrical & Electronics segment utilizes SEBS for wire insulation and electronic component protection. The Footwear segment leverages SEBS's flexibility and durability properties in shoe soles and platforms. The Sporting and Toys segment capitalizes on SEBS's safety features and durability for various applications. The Roads and Railways segment employs SEBS for bitumen modification and infrastructure applications. Each of these segments contributes uniquely to the market's overall growth, driven by specific industry requirements and technological advancements, often utilizing SEBS as a rubber compound and polymer compound.

Styrene Ethylene Butylene Styrene (SEBS) Market Geography Segment Analysis

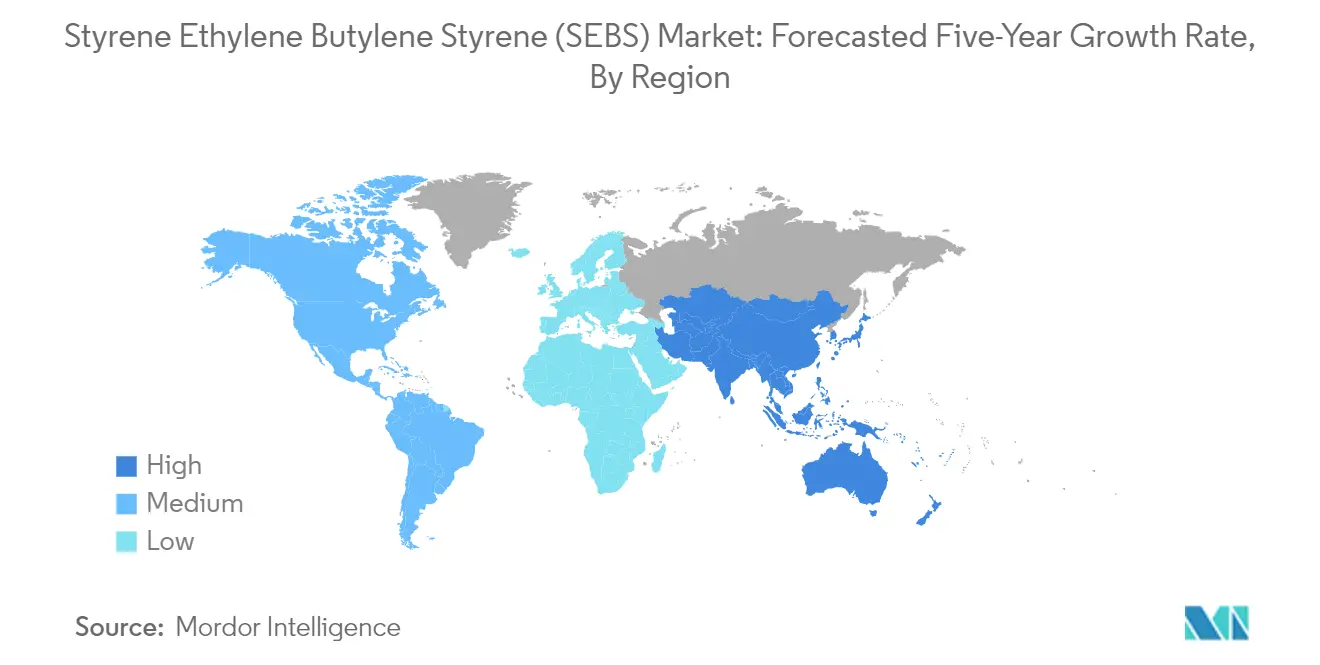

Styrene Ethylene Butylene Styrene (SEBS) Market in Asia-Pacific

The Asia-Pacific region represents the largest market for Styrene Ethylene Butylene Styrene (SEBS) globally, with significant production and consumption across major economies, including China, India, Japan, and South Korea. The region's dominance is driven by extensive manufacturing activities, a growing automotive sector, and increasing investments in the adhesives industry. The presence of major electronics manufacturing hubs, particularly in countries like China, Japan, and South Korea, further strengthens the market. The region also benefits from robust footwear production, with several countries serving as global manufacturing centers.

Styrene Ethylene Butylene Styrene (SEBS) Market in China

China dominates the Asia-Pacific SEBS market, holding approximately 58% share of the regional market in 2024. The country's market leadership is supported by its position as the world's largest automobile market in terms of both production and sales. China's electronics sector has shown remarkable growth, with the country being a strong and favorable market for electronics producers due to low labor costs and flexible policies. The country has also embarked on strategic initiatives like the "Made in China 2025" plan, demonstrating its commitment to industrial development. Additionally, China's position as the world's largest manufacturer and exporter of footwear further strengthens its market dominance in the thermoplastic elastomer market.

Styrene Ethylene Butylene Styrene (SEBS) Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, with a projected growth rate of approximately 8% during 2024-2029. The country's growth is driven by rapid industrialization and increasing investments in manufacturing sectors. India's automotive industry shows promising growth potential, supported by government initiatives like "Make in India" and "Aatma Nirbhar Bharat." The country's electronics manufacturing industry is experiencing significant expansion, backed by policies promoting domestic manufacturing and reducing import dependence. Furthermore, India's position as the second-largest footwear manufacturer globally, contributing around 9% to global production, creates substantial opportunities for SEBS market growth.

Styrene Ethylene Butylene Styrene (SEBS) Market in North America

The North American SEBS market is characterized by advanced manufacturing capabilities, a strong presence of key market players, and significant technological innovations. The region's market is primarily driven by the United States, Canada, and Mexico, with substantial demand from various end-user industries, including automotive, electronics, and adhesives sectors. The region benefits from robust research and development activities and increasing adoption of advanced materials across industries, including thermoplastic elastomer and synthetic rubber solutions.

Styrene Ethylene Butylene Styrene (SEBS) Market in United States

The United States leads the North American market, accounting for approximately 73% of the regional market in 2024. The country's market leadership is supported by its strong automotive industry, being one of the world's largest automotive markets. The US also demonstrates significant demand from the adhesives and sealants sector, driven by growing e-commerce and packaging industries. The country's robust electronics manufacturing sector and increasing investments in infrastructure development further contribute to market growth, particularly in the SBC market.

Styrene Ethylene Butylene Styrene (SEBS) Market in United States Growth

The United States also emerges as the fastest-growing market in North America, with an expected growth rate of approximately 5% during 2024-2029. This growth is driven by increasing investments in infrastructure development, rising demand for electric vehicles, and an expanding electronics manufacturing sector. The country's focus on sustainable materials and growing emphasis on research and development activities in polymer science contribute to market expansion. Additionally, the strong presence of major market players and continuous technological advancements support market growth in the thermoplastic elastomer and polymer compound sectors.

Styrene Ethylene Butylene Styrene (SEBS) Market in Europe

The European SEBS market demonstrates a mature and well-established industry landscape, encompassing major economies such as Germany, the United Kingdom, France, and Italy. The region's market is characterized by a strong focus on research and development, stringent quality standards, and increasing emphasis on sustainable materials. The presence of major automotive manufacturers, a robust electronics industry, and a growing construction sector drive market growth across the region, particularly in the SBC market.

Styrene Ethylene Butylene Styrene (SEBS) Market in Germany

Germany maintains its position as the largest SEBS market in Europe, driven by its dominant automotive industry and strong manufacturing base. The country hosts major car-making brands and leads the European automotive market with numerous assembly and engine production plants. Germany's electronics sector, being the largest in Europe, further strengthens its market position. The country's focus on technological innovation and sustainable development creates continued opportunities for market growth in the rubber compound sector.

Styrene Ethylene Butylene Styrene (SEBS) Market in France

France emerges as the fastest-growing market in Europe, supported by its expanding automotive sector and growing electronics industry. The country's focus on sustainable development and increasing investments in infrastructure projects drive market growth. France's strong presence in adhesives and sealants manufacturing, coupled with growing construction activities, creates favorable conditions for market expansion. The country's emphasis on research and development in polymer science further supports market development in the TPE market.

Styrene Ethylene Butylene Styrene (SEBS) Market in South America

The South American SEBS market is primarily driven by Brazil and Argentina, with Brazil emerging as both the largest and fastest-growing market in the region. The market benefits from growing automotive production, expanding electronics manufacturing, and increasing infrastructure development activities across the region. Brazil's position as a major automotive hub and Argentina's developing industrial sector contribute significantly to regional market growth. The region's focus on improving infrastructure and growing manufacturing capabilities creates opportunities for market expansion.

Styrene Ethylene Butylene Styrene (SEBS) Market in Middle East and Africa

The Middle East and Africa SEBS market shows promising growth potential, with Saudi Arabia and South Africa as key markets. Saudi Arabia emerges as both the largest and fastest-growing market in the region, driven by significant investments in infrastructure development and growing industrial activities. The region benefits from increasing construction activities, an expanding automotive sector, and a growing focus on industrial diversification. South Africa's developing automotive industry and infrastructure projects contribute to regional market growth.

Get Analysis on Important Geographic Markets

Download PDF

Styrene Ethylene Butylene Styrene Industry Overview

Top Companies in Styrene Ethylene Butylene Styrene (SEBS) Market

The global SEBS market is characterized by continuous product innovation focused on developing sustainable and high-performance materials, particularly for automotive, medical, and consumer applications. Companies are investing heavily in research and development to enhance their innovation portfolios, with an emphasis on polyvinyl chloride alternatives and high melt flow polymers for specialized applications. Operational excellence is being pursued through integrated manufacturing capabilities and robust distribution networks spanning multiple continents. Strategic moves in the industry are centered around vertical integration across the value chain, from raw material sourcing to end-product manufacturing. Market leaders are expanding their presence through capacity additions, particularly in the Asia-Pacific region, while simultaneously strengthening their foothold in established markets through strategic partnerships and collaborations. The focus on technological advancement and process optimization remains paramount, with companies investing in state-of-the-art production facilities and innovation centers across North America, Europe, and Asia.

Consolidated Market with Strong Regional Players

The SEBS market exhibits a partially consolidated structure, with the top five manufacturers commanding a substantial share of global production capacity. These leading players are predominantly large chemical conglomerates with diverse product portfolios and significant financial resources, enabling them to invest in advanced manufacturing facilities and extensive distribution networks. The market is characterized by a mix of global chemical giants and specialized elastomer manufacturers, with companies like Kraton Corporation and Sinopec maintaining dominant positions through their integrated operations and technological expertise. Recent years have witnessed significant merger and acquisition activity, exemplified by DL Chemical's acquisition of Kraton Corporation and ENEOS Corporation's acquisition of JSR's elastomers business.

The competitive dynamics vary significantly across regions, with Asian manufacturers, particularly Chinese companies, rapidly expanding their production capabilities and market presence. The industry structure is evolving through strategic partnerships and joint ventures, especially in emerging markets, as companies seek to strengthen their regional presence and access new customer bases. Market leaders are increasingly focusing on developing specialized grades and applications while maintaining cost competitiveness through economies of scale and operational efficiency. The barrier to entry remains high due to substantial capital requirements, technical expertise needs, and the importance of established customer relationships in key end-use industries.

Innovation and Sustainability Drive Future Success

Success in the SEBS market increasingly depends on companies' ability to develop innovative products that meet evolving customer requirements while adhering to stringent environmental regulations. Incumbent players are focusing on expanding their product portfolios with bio-based alternatives and enhanced performance characteristics, particularly for high-value applications in medical devices and automotive components. The ability to maintain strong relationships with key customers in concentrated end-use industries, while simultaneously developing new application areas, has become crucial for maintaining market position. Companies are also investing in digital capabilities and technical support services to differentiate their offerings and create additional value for customers.

For contenders looking to gain market share, the focus needs to be on developing specialized products for niche applications while building a strong regional presence in high-growth markets. The threat of substitution from alternative elastomers necessitates continuous innovation and cost optimization efforts. Regulatory compliance, particularly regarding environmental standards and chemical safety, is becoming increasingly important for maintaining market access. Success in the market also requires robust supply chain management capabilities and the ability to navigate raw material price volatility. Companies that can effectively combine technological innovation with operational excellence while maintaining strong customer relationships are likely to emerge as market leaders in the future.

Styrene Ethylene Butylene Styrene (SEBS) Market Leaders

-

Kraton Corporation

-

China Petrochemical Corporation (Sinopec Corp.)

-

Celanese Corporation

-

TSRC

-

Asahi Kasei Corporation

- *Disclaimer: Major Players sorted in no particular order

_Market-_Market_Concentration.webp)

Need More Details on Market Players and Competiters?

Download PDF

Styrene Ethylene Butylene Styrene (SEBS) Market News

- April 2023: The China Petroleum and Chemical Corporation subsidiary Hainan Baling Chemical New Material Co. Ltd invested RMB 1.92 billion (USD 279.74 million) in the Hainan Baling project and initiated the production of its styrene-butadiene copolymer (SBC) project in Hainan, China. The project's SBC plant produces 170,000 tons of SBS and SEBS products annually, including 120,000 tons of SBS products and 50,000 SEBS products.

- August 2022: Kraton announced the expansion of the production capacity of styrene block copolymers at a manufacturing facility in Mailiao, Taiwan. This strategic move was expected to increase the capacity of the facility by 30% for the styrene-ethylene-butylene-styrene product range.

Styrene Ethylene Butylene Styrene (SEBS) Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Increasing Investments in the Adhesives Industry

- 4.1.2 Growing Demand From the Automotive Industry

- 4.1.3 Other Drivers

-

4.2 Restraints

- 4.2.1 Hazardous Nature and Regulations of Styrene

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION (Market Size in Volume)

-

5.1 Form

- 5.1.1 Pellets

- 5.1.2 Powder

-

5.2 End-User Industry

- 5.2.1 Footwear

- 5.2.2 Adhesives and Sealants

- 5.2.3 Plastics

- 5.2.4 Roads and Railways

- 5.2.5 Automotive

- 5.2.6 Sporting and Toys

- 5.2.7 Electrical and Electronics

- 5.2.8 Other-end User Industries (Medical, 3D Printing, Lubricant Tackifiers, etc.)

-

5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Asahi Kasei Corporation

- 6.4.2 Celanese Corporation

- 6.4.3 China Petrochemical & Chemical Corporation (Sinopec Corp.)

- 6.4.4 Dynasol Group

- 6.4.5 General Industrial Polymers

- 6.4.6 ENEOS Corporation

- 6.4.7 Kraton Corporation

- 6.4.8 Kuraray Co. Ltd

- 6.4.9 LCY GROUP

- 6.4.10 Ningbo Changhong Polymer Scientific and Technical Inc.

- 6.4.11 Ravago

- 6.4.12 RTP Company

- 6.4.13 Trinseo

- 6.4.14 TSRC

- 6.4.15 Versalis SpA

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emergence as a Replacement For PVC Across Various Applications

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Styrene Ethylene Butylene Styrene Industry Segmentation

Styrene ethylene butylene styrene, also known as SEBS, is an important thermoplastic soft elastomer (TPE) that behaves like rubber without undergoing vulcanization. SEBS is a high-temperature, high-resistance hydrogenated product. It has high mechanical strength and high safety. It is stable in color, odorless, and free of impurities. SEBS is often mixed with other oils, such as paraffin, to increase processing efficiency.

The SEBS market is segmented by form, end-user industry, and geography. By form, the market is segmented into pellets and powder. By end-user industry, the market is segmented into footwear, adhesives, and sealants, plastic, roads and railways, automotive, sporting and toys, electrical and electronics, and other end-user industries (medical, 3D printing, lubricant tackifiers, etc). The report also covers the market sizes and forecasts in 27 countries across major regions. For each segment, the market sizes and forecasts are provided based on volume (kilotons).

| Form | Pellets | ||

| Powder | |||

| End-User Industry | Footwear | ||

| Adhesives and Sealants | |||

| Plastics | |||

| Roads and Railways | |||

| Automotive | |||

| Sporting and Toys | |||

| Electrical and Electronics | |||

| Other-end User Industries (Medical, 3D Printing, Lubricant Tackifiers, etc.) | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Thailand | |||

| Indonesia | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| NORDIC countries | |||

| Turkey | |||

| Russia | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| Qatar | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Styrene Ethylene Butylene Styrene (SEBS) Market Research FAQs

How big is the Styrene Ethylene Butylene Styrene Market?

The Styrene Ethylene Butylene Styrene Market size is expected to reach 328.20 kilotons in 2025 and grow at a CAGR of 5.10% to reach 420.87 kilotons by 2030.

What is the current Styrene Ethylene Butylene Styrene Market size?

In 2025, the Styrene Ethylene Butylene Styrene Market size is expected to reach 328.20 kilotons.

Who are the key players in Styrene Ethylene Butylene Styrene Market?

Kraton Corporation, China Petrochemical Corporation (Sinopec Corp.), Celanese Corporation, TSRC and Asahi Kasei Corporation are the major companies operating in the Styrene Ethylene Butylene Styrene Market.

Which is the fastest growing region in Styrene Ethylene Butylene Styrene Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Styrene Ethylene Butylene Styrene Market?

In 2025, the Asia Pacific accounts for the largest market share in Styrene Ethylene Butylene Styrene Market.

What years does this Styrene Ethylene Butylene Styrene Market cover, and what was the market size in 2024?

In 2024, the Styrene Ethylene Butylene Styrene Market size was estimated at 311.46 kilotons. The report covers the Styrene Ethylene Butylene Styrene Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Styrene Ethylene Butylene Styrene Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Styrene Ethylene Butylene Styrene (SEBS) Market Research

Mordor Intelligence provides a comprehensive analysis of the SEBS and styrenic block copolymer industries. We leverage extensive expertise in thermoplastic elastomer research. Our detailed report examines the evolving landscape of styrene ethylene butylene styrene applications. This includes its role as an impact modifier and polymer additive. The analysis covers crucial developments in SBC (Styrenic Block Copolymer) technology and TPR (Thermoplastic Rubber) innovations. It also explores emerging trends in synthetic rubber applications, all available in an easy-to-download report PDF format.

Stakeholders across the thermoplastic elastomer market gain valuable insights into polymer compound developments and rubber compound applications. The report extensively covers modified polymer technologies and their impact on the TPE industry. It also analyzes trends in elastic polymer and flexible polymer applications. Our research encompasses the complete value chain, from SEBS polymer manufacturing to end-use applications in the styrenic thermoplastic elastomer sector. This provides actionable intelligence for industry participants in the synthetic rubber industry and SBC market.