| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| CAGR | 5.00 % |

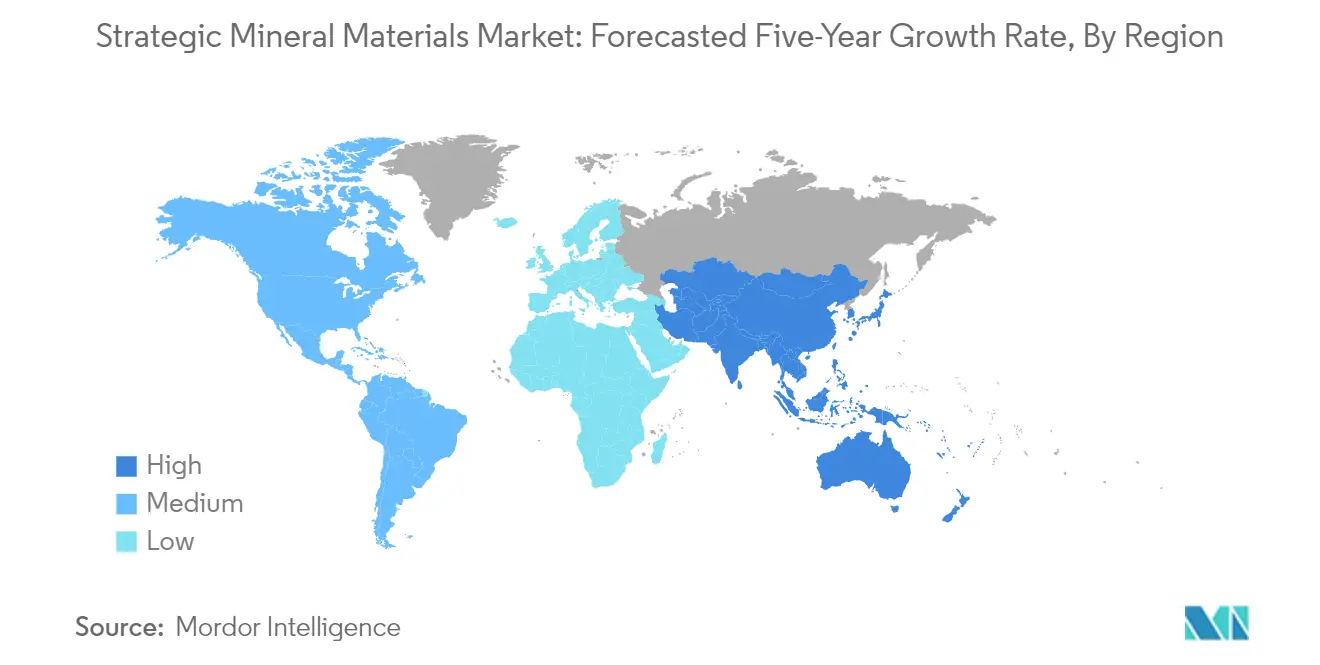

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Strategic Mineral Materials Market Analysis

The Strategic Mineral Materials Market is expected to register a CAGR of greater than 5% during the forecast period.

The strategic materials industry is experiencing significant transformation driven by geopolitical tensions and increased defense spending worldwide. The United States Department of Defense has identified more than 250 "critical raw materials" essential for military and civilian industries, highlighting their crucial role in national security. According to the Stockholm International Peace Research Institute, the United States defense budget comprised almost 40% of global military spending in 2022, with an increase of USD 71 billion from the previous year, partly due to military assistance to Ukraine. This heightened focus on defense capabilities has led to increased demand for critical minerals in military applications, from advanced electronics to aerospace components.

The electronics and semiconductor sectors continue to drive substantial demand for strategic materials, with major investments reshaping the industry landscape. Germany's electronic industry, the largest in Europe, achieved a market volume exceeding EUR 220 billion in 2022, employing more than 1.6 million workers at home and abroad. The sector's robust growth is complemented by significant developments in semiconductor manufacturing, exemplified by Intel's agreement with the German government to invest nearly EUR 32 billion over the next decade in semiconductor value chain development, ranging from R&D to manufacturing and packaging technologies.

The clean energy transition is accelerating the demand for critical raw materials across multiple applications. In the United States, solar industry installations grew by 47% in Q1 2023 compared to Q1 2022, with photovoltaic solar accounting for 54% of all new electricity-generating capacity additions. The electric vehicle sector has shown remarkable growth, with US electric car sales increasing by 55% in 2022, reaching an 8% share of new car sales. This rapid expansion in clean energy technologies has intensified the need for various rare earth elements used in solar panels, batteries, and other renewable energy applications.

The global mining and production landscape is undergoing significant restructuring as countries seek to secure reliable supply chains for strategic materials. Major mining companies are expanding their operations and developing new projects to meet growing demand. For instance, in March 2023, JX Nippon Mining & Metals Corp joined a project to produce tantalum at the Mibra mine in Brazil, marking its entry into the rare metals market. Similarly, companies like Anglo American Platinum have maintained their position as leading producers of platinum group elements, with a total production of around 3.8 million ounces, demonstrating the industry's capacity to scale production in response to market demands. The focus on securing specialty metals is crucial for maintaining competitive advantage in this evolving market.

Strategic Mineral Materials Market Trends

Growing Focus on Sustaining the National and Economic Security

The increasing global geopolitical tensions have led to a significant surge in defense spending worldwide, with the United States defense budget accounting for almost 40% of all military spending by nations worldwide in 2022. The defense spending of the United States increased by USD 71 billion in 2022 from the previous year, making it spend more on defense than the combined expenditures of the next 10 countries. The United States Department of Defense (DOD) has identified more than 250 "strategic materials" and "critical minerals" that are crucial for supporting military and essential civilian industry operations, highlighting the growing importance of securing these resources for national security.

The defense industry's technological advancement and modernization efforts are driving the demand for "defense materials." In September 2023, the United States Army approved the Sentinel A4 radar program to enter low-rate initial production, with 19 systems expected to be delivered by fiscal year 2025. This next-generation radar system, which can simultaneously identify and track multiple threat types, requires various "strategic materials" for its advanced components. Similarly, China's military modernization efforts have led to expanded production capabilities for new aircraft, including fifth-generation fighter jets like the J-20 and 4.5-generation fighters such as the J-10C and J-16, along with significant warship upgrades to strengthen its maritime capabilities.

Understand The Key Trends Shaping This Market

Download PDF

Growing Demand from Clean Energy Technologies

The clean energy transition is creating unprecedented demand for "critical minerals" across various renewable energy technologies and electric vehicle applications. In the wind energy sector, Europe installed a record number of wind farms in 2022, with an increase of nearly 4% compared to 2021. Germany's onshore wind energy sector showed impressive growth in the first half of 2023, installing 331 wind turbines with a combined capacity of 1,565 megawatts, representing 65% of the total capacity installed in the entire year of 2022. The country aims to source 80% of its electricity from renewable energy by 2030, with onshore wind power projected to reach a capacity of 115 GW.

The electric vehicle revolution is driving significant demand for "battery minerals" and associated "critical resources." The demand for automotive lithium-ion batteries increased by about 65% from 330 GWh in 2021 to 550 GWh in 2022, primarily due to the growth in electric passenger car sales. In China, the market for automotive batteries expanded by more than 70% in 2022 compared to 2021, while in the United States, the demand for batteries grew by around 80%. This growth is supported by major investments in battery manufacturing capacity, such as Ford Motor Company's USD 11.4 billion investment in Tennessee and Kentucky for advanced manufacturing of electric trucks and lithium-ion batteries, announced in partnership with SK Innovation Co. Ltd.

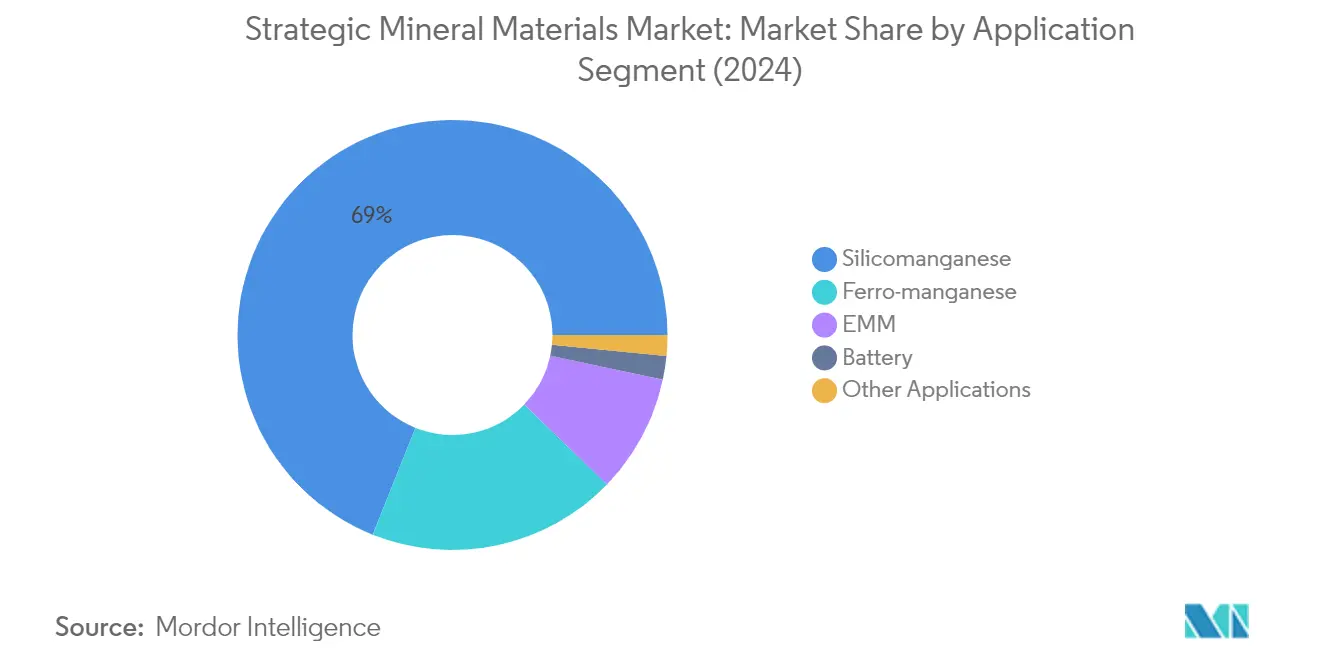

Segment Analysis: By Application

Silicomanganese Segment in Strategic Mineral Materials Market

The Silicomanganese segment continues to dominate the strategic materials market, holding approximately 69% of the total market share in 2024. This significant market position is primarily attributed to its extensive usage in the steel industry, where it serves as a crucial deoxidizer and desulfurizer in steel production. The segment's dominance is further strengthened by the growing infrastructure development and construction activities across major economies, particularly in the Asia-Pacific region. The increasing demand for high-strength steel in automotive manufacturing, construction projects, and industrial machinery has also contributed to maintaining silicomanganese's position as the leading segment in the market. Additionally, the segment benefits from established supply chains and production facilities in key mining regions, ensuring stable availability for end-users.

Battery Segment in Strategic Mineral Materials Market

The Battery segment is emerging as the fastest-growing segment in the strategic metals market, projected to grow at approximately 17% during the forecast period 2024-2029. This remarkable growth is driven by the accelerating adoption of electric vehicles globally and the expanding energy storage systems market. The segment's growth is further fueled by significant investments in battery minerals manufacturing facilities across major economies and the increasing focus on renewable energy integration. Technological advancements in battery chemistry and manufacturing processes are also contributing to the segment's expansion. The implementation of supportive government policies promoting clean energy adoption and electric vehicle infrastructure development across various regions is expected to maintain this segment's high growth trajectory throughout the forecast period.

Remaining Segments in Strategic Mineral Materials Market

The remaining segments in the technology minerals market, including Ferro-manganese, Electrolytic Manganese Metal (EMM), and other applications, continue to play vital roles in various industrial applications. The Ferro-manganese segment maintains its importance in steel production and specialized alloy manufacturing, while EMM serves critical functions in specialized electronic applications and high-purity metal production. These segments benefit from ongoing technological advancements in manufacturing processes and increasing demand from emerging applications in aerospace, electronics, and specialized industrial uses. The diversification of applications and continuous research and development activities in these segments contribute to the overall market stability and growth.

Strategic Mineral Materials Market Geography Segment Analysis

Strategic Mineral Materials Market in North America

The North American strategic materials market demonstrates robust development across the United States, Canada, and Mexico. The region benefits from extensive mining operations, advanced manufacturing capabilities, and strong demand from key end-use industries, including aerospace, automotive, electronics, and defense. The United States leads the regional market with significant production and consumption of various strategic materials, while Canada contributes through its rich mineral deposits and processing facilities. Mexico complements the regional market with its growing industrial base and increasing focus on mineral processing capabilities.

Strategic Mineral Materials Market in United States

The United States dominates the North American strategic materials market through its comprehensive industrial infrastructure and diverse application sectors. The country maintains approximately 85% share of the regional market, driven by substantial demand from its defense sector, aerospace industry, and growing electric vehicle manufacturing base. The nation's focus on securing domestic supply chains for critical minerals, coupled with investments in processing capabilities, strengthens its market position. The country's strategic initiatives to reduce dependency on imports, particularly in rare earth elements and other critical minerals, further solidify its market leadership. The robust semiconductor industry and growing renewable energy sector continue to drive demand for various strategic materials in the country.

Strategic Mineral Materials Market in Mexico

Mexico emerges as the fastest-growing market in North America with an expected growth rate of approximately 2% during 2024-2029. The country's growth is primarily driven by increasing industrialization and expanding manufacturing capabilities, particularly in the automotive and electronics sectors. Mexico's strategic geographical location and trade agreements with major economies enhance its position in the regional market. The country's developing infrastructure and increasing foreign investments in mineral processing facilities contribute to market expansion. Additionally, Mexico's rich mineral deposits and government initiatives to promote mining activities support its growth trajectory in the industrial minerals market.

Strategic Mineral Materials Market in Europe

The European strategic materials market showcases a mature and well-established infrastructure across Germany, the United Kingdom, Italy, France, and Spain. The region's market is characterized by advanced processing technologies, strict regulatory frameworks, and a strong focus on sustainable practices. The European Union's initiatives to secure critical mineral supply chains and reduce dependency on external sources shape the market dynamics. The region's robust automotive, aerospace, and electronics industries drive consistent demand for strategic materials, while increasing focus on renewable energy and electric vehicles creates new growth opportunities.

Strategic Mineral Materials Market in Germany

Germany leads the European strategic materials market with approximately 17% share of the regional market, supported by its advanced manufacturing capabilities and strong industrial base. The country's leadership position is reinforced by its robust automotive sector, growing renewable energy industry, and significant investments in electric vehicle production. Germany's advanced chemical industry and strong focus on research and development in material sciences contribute to market growth. The country's strategic initiatives in securing critical mineral supply chains and developing processing capabilities further strengthen its market position.

Strategic Mineral Materials Market Growth in Germany

Germany also emerges as the fastest-growing market in Europe with an anticipated growth rate of approximately 3% during 2024-2029. The country's growth is driven by increasing investments in electric vehicle production, expanding renewable energy sector, and advancing semiconductor industry. Germany's focus on Industry 4.0 initiatives and digitalization creates additional demand for strategic materials in various high-tech applications. The country's commitment to energy transition and sustainable technologies further accelerates market growth. Additionally, government support for research and development in advanced materials contributes to market expansion.

Strategic Mineral Materials Market in Asia-Pacific

The Asia-Pacific region represents the largest and most dynamic market for strategic materials, encompassing major economies like China, India, Japan, South Korea, and ASEAN countries. The region's market is characterized by extensive manufacturing activities, growing industrialization, and increasing investments in high-tech sectors. China dominates the regional landscape with its comprehensive mineral processing capabilities and extensive industrial base. The region benefits from robust growth in electric vehicle production, electronics manufacturing, and renewable energy installations, driving demand for various strategic materials.

Strategic Mineral Materials Market in China

China maintains its position as the largest market in the Asia-Pacific region, leveraging its extensive manufacturing capabilities and comprehensive supply chain infrastructure. The country's dominance is supported by its strong presence in rare earth elements processing, robust electronics manufacturing sector, and growing electric vehicle industry. China's strategic investments in mineral processing capabilities and focus on technological advancement strengthen its market leadership. The nation's commitment to renewable energy development and industrial modernization drives continuous demand for strategic materials.

Strategic Mineral Materials Market in ASEAN Countries

The ASEAN region emerges as the fastest-growing market in Asia-Pacific, driven by rapid industrialization and increasing investments in manufacturing capabilities. The region's growth is supported by expanding electronics manufacturing, rising automotive production, and growing infrastructure development. ASEAN countries benefit from strategic partnerships with major economies and increasing foreign direct investments in mineral processing facilities. The region's developing renewable energy sector and growing electric vehicle industry create additional demand for strategic materials.

Strategic Mineral Materials Market in Rest of World

The Rest of World market for strategic materials encompasses diverse regions including South America, the Middle East, and Africa, each contributing uniquely to the global supply chain. These regions play crucial roles in mineral extraction and processing, with significant reserves of various strategic materials. The market in these regions is characterized by growing investments in processing capabilities, increasing focus on value-added products, and expanding industrial applications. South America leads in terms of market size, while Middle Eastern countries show the fastest growth potential, driven by diversification initiatives and increasing industrial development. The regions benefit from growing investments in infrastructure development, expanding manufacturing capabilities, and increasing focus on technological advancement in mineral processing.

Get Analysis on Important Geographic Markets

Download PDF

Strategic Mineral Materials Industry Overview

Top Companies in Strategic Mineral Materials Market

The strategic materials market features prominent players like Anglo American, Glencore, Vale SA, and China Northern Rare Earth Group leading the industry through vertical integration and geographical diversification. Companies are increasingly focusing on sustainable mining practices and technological advancements in extraction processes to maintain their competitive edge. Strategic moves include expanding production capacities, particularly in rare earth elements and battery materials, while establishing long-term supply agreements with end-users in high-growth sectors like electric vehicles and renewable energy. Operational agility is demonstrated through investments in automated mining operations and digital transformation initiatives to optimize production efficiency. Product innovation efforts are centered on developing high-purity grades for specialized applications in electronics, aerospace, and clean energy sectors, with companies also emphasizing recycling and circular economy approaches to ensure resource sustainability.

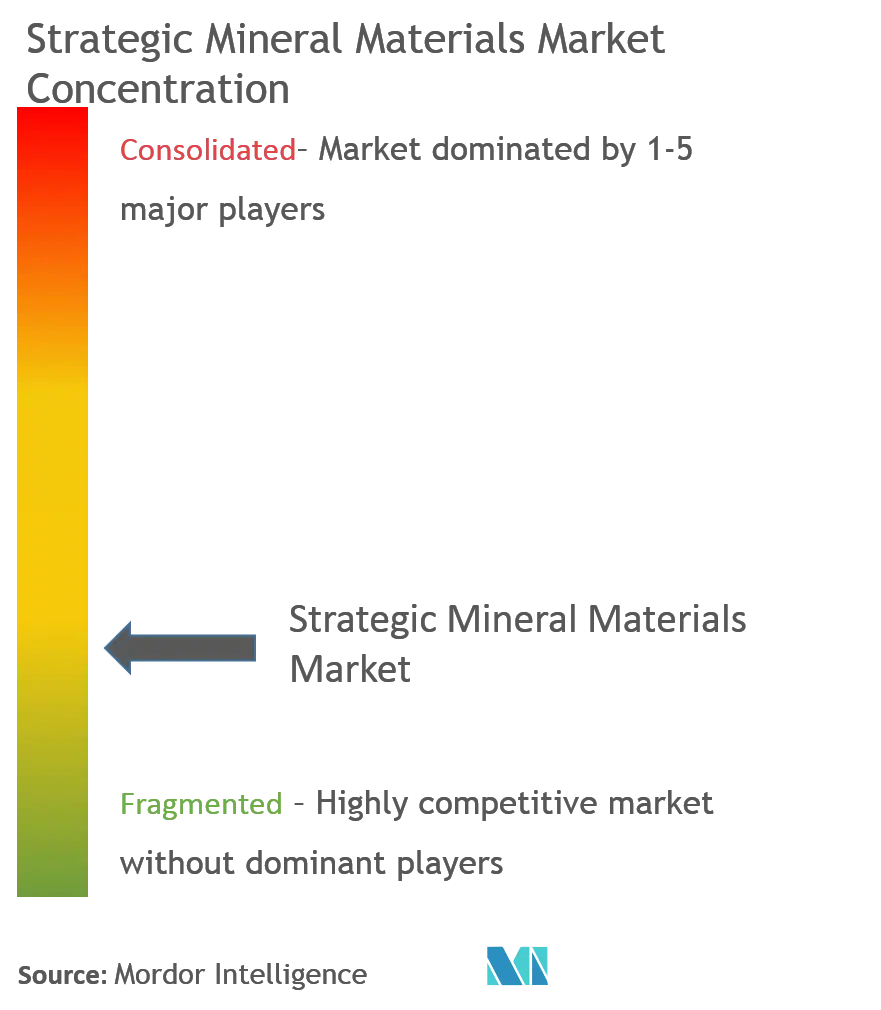

Consolidated Market with Strong Regional Players

The strategic mineral materials market exhibits a moderately consolidated structure, characterized by the presence of both global mining conglomerates and specialized regional players. Major global companies maintain their dominance through extensive mineral reserves, integrated value chains, and sophisticated processing capabilities, while regional specialists thrive by focusing on specific mineral categories or geographical markets. The market has witnessed significant merger and acquisition activity, particularly in regions with abundant reserves like Australia, Africa, and South America, as companies seek to secure critical mineral supplies and strengthen their market positions.

The competitive dynamics vary significantly across different mineral segments, with some materials like rare earth elements showing high concentration among Chinese producers, while others like platinum group metals feature more geographically diverse production bases. Market entry barriers remain high due to substantial capital requirements, complex regulatory frameworks, and the need for specialized technical expertise. Joint ventures and strategic partnerships have become increasingly common, especially in developing markets, as companies seek to share risks and leverage complementary capabilities in exploration, extraction, and processing operations.

Innovation and Sustainability Drive Future Success

Success in the critical minerals industry increasingly depends on companies' ability to balance operational efficiency with environmental stewardship and stakeholder engagement. Incumbent players are strengthening their positions by investing in advanced processing technologies, developing closed-loop recycling systems, and establishing direct relationships with end-users in high-growth sectors. The ability to provide consistent quality, ensure supply chain transparency, and maintain environmental compliance has become crucial for maintaining market share, particularly as end-users face growing pressure to demonstrate responsible sourcing practices.

For new entrants and smaller players, opportunities exist in specialized market segments where technical expertise and customer relationships can overcome scale disadvantages. Success factors include developing innovative extraction methods that reduce environmental impact, focusing on minerals critical to emerging technologies, and building strategic partnerships with technology companies and end-users. The regulatory landscape continues to evolve, with increasing emphasis on environmental protection, community relations, and supply chain security, making compliance capabilities and stakeholder management essential for long-term success. Companies must also address the challenge of end-user concentration in certain segments while maintaining flexibility to respond to shifting demand patterns and potential substitution risks.

Strategic Mineral Materials Market Leaders

-

Anglo American plc

-

Glencore

-

Intercontinental Mining

-

Materion Corporation

-

Vale

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Strategic Mineral Materials Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Drivers

- 4.1.1 Growing Demand from Various End-user Industries

- 4.1.2 Other Drivers

-

4.2 Restraints

- 4.2.1 Impact of COVID-19 Pandemic

- 4.2.2 Growing Environmental Concerns over Mining Operations

- 4.3 Industry Value-chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5. MARKET SEGMENTATION

-

5.1 Mineral

- 5.1.1 Antimony

- 5.1.1.1 Flame Retardants

- 5.1.1.2 Batteries

- 5.1.1.3 Ceramics and Glass

- 5.1.1.4 Catalyst

- 5.1.1.5 Alloys

- 5.1.2 Barite

- 5.1.2.1 Oil and Gas

- 5.1.2.2 Other Applications (paints, chemical manufacturing and others)

- 5.1.3 Beryllium

- 5.1.3.1 Electronics

- 5.1.3.2 Aerospace

- 5.1.3.3 Automotive

- 5.1.3.4 Energy

- 5.1.3.5 Other Applications

- 5.1.4 Cobalt

- 5.1.4.1 Batteries

- 5.1.4.2 Superalloys

- 5.1.4.3 Cemented Carbides and Diamond Tools

- 5.1.4.4 Catalysts

- 5.1.4.5 Other Applications

- 5.1.5 Fluorspar

- 5.1.5.1 Chemicals

- 5.1.5.2 Steel

- 5.1.5.3 Aluminum

- 5.1.5.4 Cement

- 5.1.5.5 Other Applications

- 5.1.6 Gallium

- 5.1.6.1 Integrated Circuits

- 5.1.6.2 Laser diodes

- 5.1.6.3 Photodetectors

- 5.1.6.4 Solar Cells

- 5.1.6.5 Other Applications

- 5.1.7 Germanium

- 5.1.7.1 Fiber Optics

- 5.1.7.2 Infrared Optics

- 5.1.7.3 Catalyst

- 5.1.7.4 Electrical and Solar Equipment

- 5.1.7.5 Other Applications

- 5.1.8 Indium

- 5.1.8.1 Flat-Panel Display Screens and Touchscreens

- 5.1.8.2 Low Melting Alloys and Solders

- 5.1.8.3 Semiconductors

- 5.1.8.4 Transparent Heat Reflectors

- 5.1.8.5 Other Applications

- 5.1.9 Manganese

- 5.1.9.1 Casting Alloys

- 5.1.9.2 Packaging

- 5.1.9.3 Transportation

- 5.1.9.4 Construction

- 5.1.9.5 Other Applications

- 5.1.10 Niobium

- 5.1.10.1 Steel

- 5.1.10.2 Super Alloys

- 5.1.10.3 Superconducting Magnets

- 5.1.10.4 Capacitors

- 5.1.10.5 Glass

- 5.1.10.6 Other Applications

- 5.1.11 Platinum Group Elements

- 5.1.11.1 Autocatalyst

- 5.1.11.2 Jewelry

- 5.1.11.3 Electrical & Electronics

- 5.1.11.4 Chemical

- 5.1.11.5 Other Applications

- 5.1.12 Rare Earth Elements

- 5.1.12.1 Catalyst

- 5.1.12.2 Batteries

- 5.1.12.3 Magnetic Alloys

- 5.1.12.4 Metallurgy

- 5.1.12.5 Other Applications

- 5.1.13 Tantalum

- 5.1.13.1 Electronics

- 5.1.13.2 Medical

- 5.1.13.3 Aerospace

- 5.1.13.4 Automotive

- 5.1.13.5 Other Applications

-

5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 ASEAN Countries

- 5.2.1.6 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Spain

- 5.2.3.6 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations and Agreements

- 6.2 Market Share/Ranking Analysis**

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Anglo American plc

- 6.4.2 CBMM

- 6.4.3 Glencore

- 6.4.4 Indium Corporation

- 6.4.5 Intercontinental Mining

- 6.4.6 Materion Corporation

- 6.4.7 South32

- 6.4.8 Vale

- 6.4.9 WARRIOR GOLD INC.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Application base of Various Minerals

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Strategic Mineral Materials Industry Segmentation

The strategic mineral materials market report includes:

| Mineral | Antimony | Flame Retardants | |

| Batteries | |||

| Ceramics and Glass | |||

| Catalyst | |||

| Alloys | |||

| Barite | Oil and Gas | ||

| Other Applications (paints, chemical manufacturing and others) | |||

| Beryllium | Electronics | ||

| Aerospace | |||

| Automotive | |||

| Energy | |||

| Other Applications | |||

| Cobalt | Batteries | ||

| Superalloys | |||

| Cemented Carbides and Diamond Tools | |||

| Catalysts | |||

| Other Applications | |||

| Fluorspar | Chemicals | ||

| Steel | |||

| Aluminum | |||

| Cement | |||

| Other Applications | |||

| Gallium | Integrated Circuits | ||

| Laser diodes | |||

| Photodetectors | |||

| Solar Cells | |||

| Other Applications | |||

| Germanium | Fiber Optics | ||

| Infrared Optics | |||

| Catalyst | |||

| Electrical and Solar Equipment | |||

| Other Applications | |||

| Indium | Flat-Panel Display Screens and Touchscreens | ||

| Low Melting Alloys and Solders | |||

| Semiconductors | |||

| Transparent Heat Reflectors | |||

| Other Applications | |||

| Manganese | Casting Alloys | ||

| Packaging | |||

| Transportation | |||

| Construction | |||

| Other Applications | |||

| Niobium | Steel | ||

| Super Alloys | |||

| Superconducting Magnets | |||

| Capacitors | |||

| Glass | |||

| Other Applications | |||

| Platinum Group Elements | Autocatalyst | ||

| Jewelry | |||

| Electrical & Electronics | |||

| Chemical | |||

| Other Applications | |||

| Rare Earth Elements | Catalyst | ||

| Batteries | |||

| Magnetic Alloys | |||

| Metallurgy | |||

| Other Applications | |||

| Tantalum | Electronics | ||

| Medical | |||

| Aerospace | |||

| Automotive | |||

| Other Applications | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| South Africa | |||

| Rest of Middle-East and Africa | |||

Need A Different Region or Segment?

Customize Now

Strategic Mineral Materials Market Research FAQs

What is the current Strategic Mineral Materials Market size?

The Strategic Mineral Materials Market is projected to register a CAGR of greater than 5% during the forecast period (2025-2030)

Who are the key players in Strategic Mineral Materials Market?

Anglo American plc, Glencore, Intercontinental Mining, Materion Corporation and Vale are the major companies operating in the Strategic Mineral Materials Market.

Which is the fastest growing region in Strategic Mineral Materials Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Strategic Mineral Materials Market?

In 2025, the Asia Pacific accounts for the largest market share in Strategic Mineral Materials Market.

What years does this Strategic Mineral Materials Market cover?

The report covers the Strategic Mineral Materials Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Strategic Mineral Materials Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Strategic Mineral Materials Market Research

Mordor Intelligence provides a comprehensive analysis of the strategic materials and critical minerals industry. We leverage decades of expertise in industrial raw materials research. Our extensive report covers the entire spectrum of critical raw materials, including rare earth elements, specialty metals, and industrial minerals. The analysis encompasses crucial aspects of mineral security, strategic elements, and technology minerals. It provides detailed insights into supply chains, production capabilities, and market dynamics. Our research methodology incorporates both primary and secondary data sources. This ensures a thorough examination of critical resource availability and strategic metals distribution patterns.

This detailed market analysis benefits stakeholders across the battery minerals and defense materials sectors. It offers crucial insights into critical mineral supply trends and future market trajectories. The report provides valuable information about essential minerals procurement strategies and emerging opportunities in the industrial minerals market. For a comprehensive understanding, our critical minerals market review is available as an easy-to-download report PDF. It features detailed analysis of critical minerals companies and their role in maintaining robust supply chains. The research particularly emphasizes the growing importance of strategic minerals in global trade and their impact on mineral security, making it an indispensable tool for industry decision-makers.