Sterilization Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.31 Billion |

| Market Size (2031) | USD 14.72 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

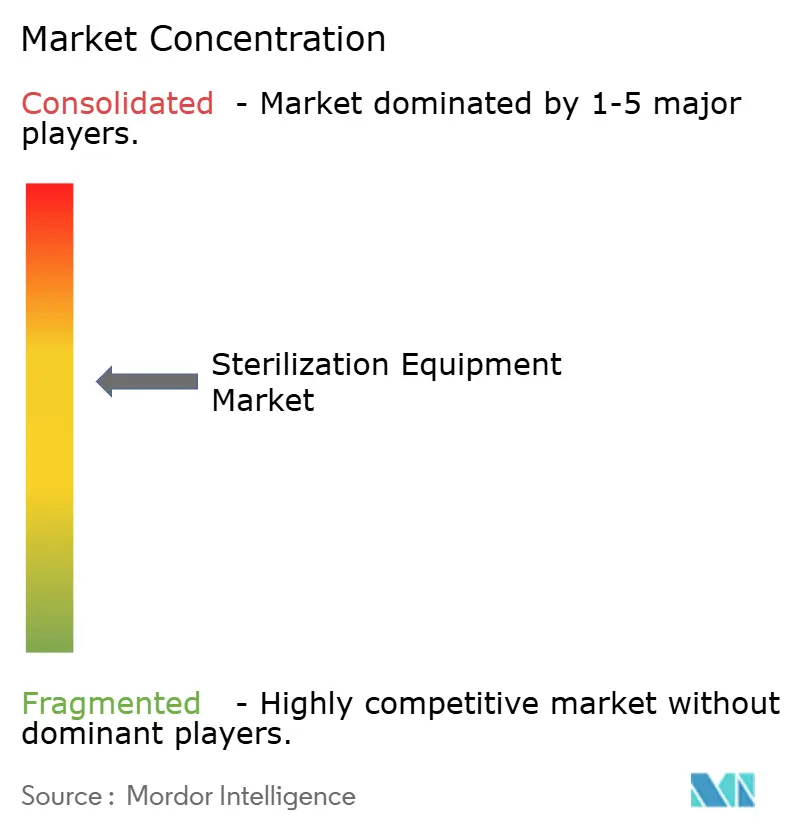

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sterilization Equipment Market Analysis by Mordor Intelligence

The Sterilization Equipment Market size is estimated at USD 10.31 billion in 2026, and is expected to reach USD 14.72 billion by 2031, at a CAGR of 7.39% during the forecast period (2026-2031).

Demand is rising as hospitals, ambulatory centers, and pharmaceutical plants modernize infection-control infrastructure and scale up throughput. Growth is most visible in low-temperature systems that handle heat-sensitive robotic and flexible endoscopes, while steam autoclaves continue to anchor baseline capacity. Contract service providers are expanding gamma, electron-beam, and ethylene-oxide offerings for device and drug makers that prefer outsourcing over in-house chambers. At the same time, cobalt-60 isotope shortages and environmental scrutiny of chemical sterilants are prompting shifts toward alternative radiation or hydrogen-peroxide plasma cycles. Competitive differentiation centers on validation know-how, digital traceability, and service breadth, creating room for both global manufacturers and niche specialists to capture share.

Key Report Takeaways

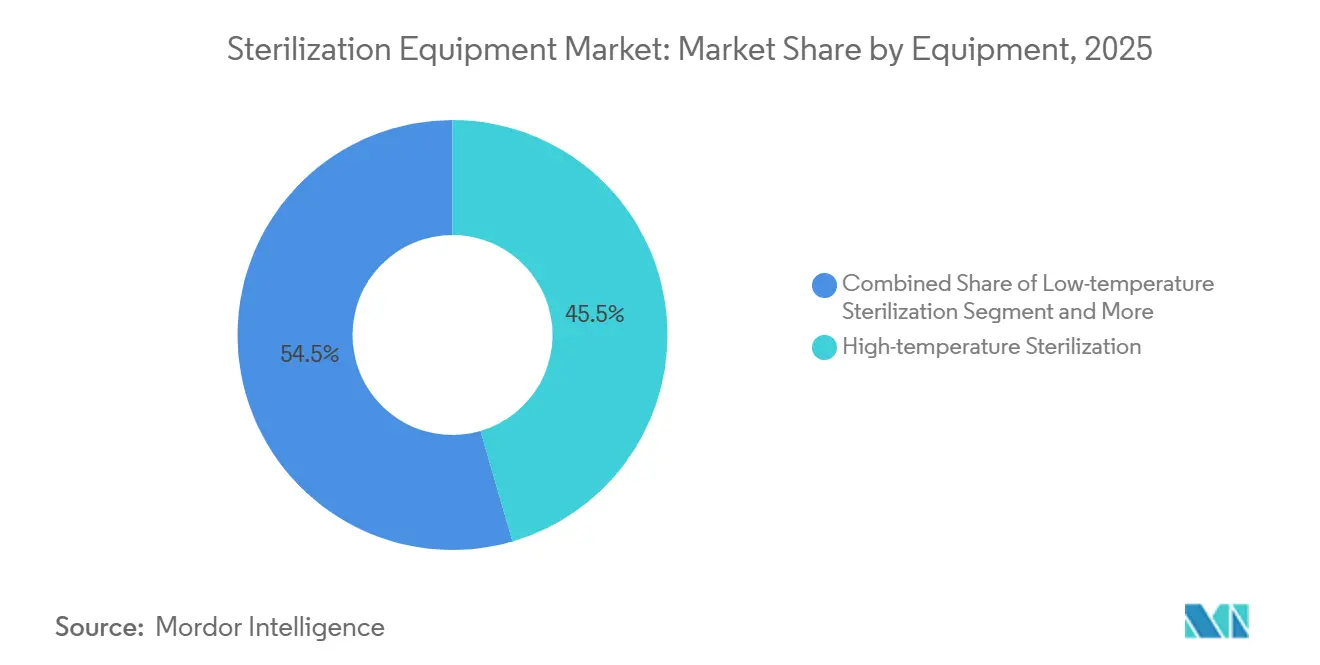

- By equipment, high-temperature sterilization led with 45.55% of sterilization equipment market share in 2025, whereas low-temperature systems are projected to expand at an 11.25% CAGR through 2031.

- By end user, hospitals and clinics held 55.53% of the sterilization equipment market size in 2025, but ambulatory surgery centers are growing at a 9.85% CAGR to 2031.

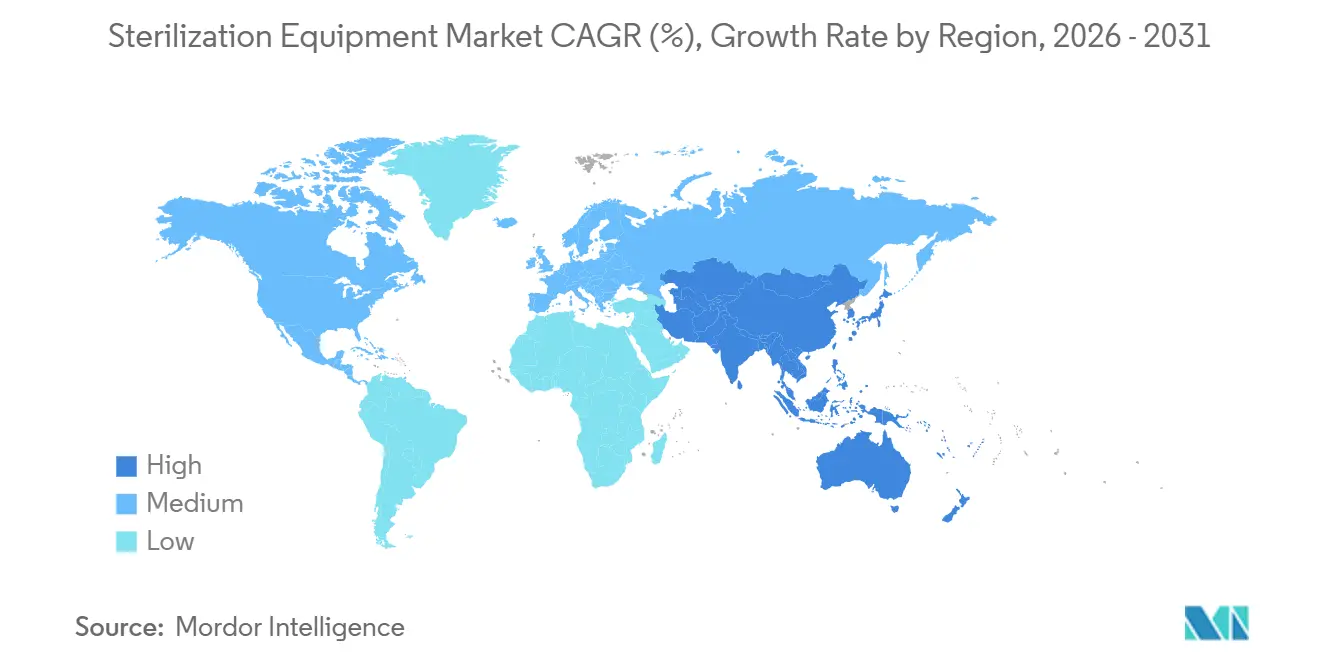

- By geography, North America contributed 39.13% revenue in 2025, while Asia-Pacific is forecast to outpace all regions at an 8.81% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sterilization Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HAIs and cross-contamination risk | +1.8% | North America and Europe | Short term (≤ 2 years) |

| Increase in surgical procedures | +1.5% | Global, led by Asia-Pacific | Medium term (2-4 years) |

| Expansion of pharma & biotech manufacturing | +1.3% | North America and Europe | Medium term (2-4 years) |

| Regulatory tightening on sterilization compliance | +0.9% | North America and EU | Long term (≥ 4 years) |

| Robotics-driven need for low-temperature H₂O₂ plasma | +1.2% | North America and Europe | Medium term (2-4 years) |

| Growth of mobile on-demand sterilization services | +0.7% | Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising HAIs And Cross-Contamination Risk

Healthcare-associated infections affect 1 in 31 U.S. inpatients on any given day, a statistic that keeps infection prevention high on executive agendas[1]Centers for Disease Control and Prevention, “HAI Data Portal,” cdc.gov. European surveillance shows 3.2 million cases every year, with device-associated episodes accounting for roughly one-third of events. Regulators now require supplemental high-level disinfection for duodenoscopes and similar devices, elevating the urgency of upgrading older autoclaves and ethylene-oxide chambers. Institutions unable to validate consistent cycles risk accreditation penalties, so many are fast-tracking versatile platforms that combine faster turnaround with lower chemical residuals. Spending is greatest in large North American and European systems, yet similar patterns are emerging in tertiary hospitals across Asia-Pacific.

Increase In Surgical Procedures

Robotic and minimally invasive surgeries are expanding procedure counts worldwide. Hip and knee replacements among OECD members increased 4.2% per year between 2019 and 2024, while cataract procedures advanced 3.8% annually[2]Organisation for Economic Co-operation and Development, “Health Statistics 2024,” oecd.org. U.S. hospitals report robotic techniques in more than 15% of general-surgery cases, which introduces delicate polymer tools that cannot withstand 132 °C steam cycles. This shift helps explain why low-temperature modalities are outpacing the broader sterilization equipment market. Facilities are layering hydrogen-peroxide plasma or low-temperature steam-formaldehyde units on top of legacy steam capacity to maintain throughput without compromising instrument integrity. Asia-Pacific volumes are accelerating fastest, reflecting rising disposable incomes and hospital construction.

Expansion Of Pharma & Biotech Manufacturing

Sixteen cell and gene therapies won U.S. approval in 2024, each requiring highly controlled aseptic fill-finish operations. Pharmaceutical plants are therefore increasing demand for tunnel sterilizers, hydrogen-peroxide generators, and outside contract services. STERIS disclosed 9% contract-sterilization revenue growth in fiscal 2024, citing biologics customers as a prime driver. European CDMOs echo similar trends as EMA mandates robust sterility assurance for advanced therapies. Growth is strongest in North America and Western Europe, yet spill-over investment is reaching Singapore, South Korea, and India as multinational firms widen biologics footprints.

Regulatory Tightening On Sterilization Compliance

The FDA harmonized its Quality Management System Regulation with ISO 13485:2016 in February 2024, compelling manufacturers to prove validated cycles and retain detailed batch records. Europe’s Medical Device Regulation enforces similar oversight, including audits of sterilization subcontractors during conformity assessments. China’s NMPA adopted guidelines mirroring ISO 11135 and ISO 14937, narrowing domestic-international compliance gaps. Such convergence raises entry barriers yet provides clear protocols that favor vendors with mature validation toolkits. Facilities now bundle data-logging sensors and digital traceability modules into purchase specifications, further boosting equipment refresh cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and maintenance costs | -1.1% | Global | Short term (≤ 2 years) |

| Toxicity concerns over chemical sterilants | -0.6% | North America and Europe | Medium term (2-4 years) |

| Co-60 isotope supply constraints | -0.5% | North America and Europe | Short term (≤ 2 years) |

| Shift toward single-use disposable instruments | -0.9% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital And Maintenance Costs

Hospital-grade steam units range from USD 50,000 to USD 150,000, and hydrogen-peroxide plasma systems often exceed USD 200,000 before validation. Annual service contracts add another 10%–15%, pressuring budgets in smaller ambulatory centers that already face tightening reimbursements. The American Hospital Association ranked sterilizers only fifth in 2024 capital-spending priorities, after electronic records, imaging, robotics, and infrastructure[3]American Hospital Association, “2024 Capital Spending Survey,” aha.org. Many facilities run autoclaves beyond a 15-year service life, accepting higher breakdown risk to defer investment. Emerging-market buyers confront even steeper hurdles because imported equipment is priced in foreign currency and tied to fluctuating exchange rates.

Shift Toward Single-Use Disposable Instruments

Orthopedic and endoscopy suppliers increasingly promote disposable tools that eliminate reprocessing steps. A 2024 JAMA study found single-use duodenoscopes cut infection risk by 78% compared with reusable models. Hospitals tempted by infection-control gains must weigh environmental impacts: a Lancet Planetary Health lifecycle review reported 3.2 kg CO₂-equivalent emissions for a single-use laparoscopic instrument versus 0.4 kg for a reusable item amortized over 50 uses. Sustainability mandates in the United Kingdom, the EU, and some U.S. states are therefore slowing universal conversion, but the trend nonetheless removes part of the addressable sterilization equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment: Low-Temperature Modalities Gain Ground

Low-temperature systems are projected to grow at an 11.25% CAGR from 2026 to 2031, substantially above the 7.39% pace of the overall sterilization equipment market. Hospitals are layering hydrogen-peroxide plasma, ethylene oxide, and ozone platforms onto existing steam capacity instead of wholesale replacement. The U.S. Environmental Protection Agency tightened ethylene-oxide emission limits in 2024, raising operating costs for commercial chambers and nudging facilities toward hydrogen-peroxide cycles that leave no carcinogenic residuals. Meanwhile, cobalt-60 shortages are accelerating the pivot to electron-beam lines that rely on high-energy electricity rather than isotopes, trimming both turnaround time and disposal liabilities. These dynamics underscore why capital is shifting toward versatile, low-toxicity systems capable of validating mixed instrument loads.

High-temperature steam remains indispensable for wrapped surgical trays, linens, and heat-stable metal tools. Cycle costs hover near USD 0.10, and standard loads finish in under 45 minutes, keeping steam dominant where utility infrastructure is reliable. Dry-heat sterilizers, operating at 160 °C–180 °C for 60–120 minutes, are increasingly confined to glassware and petroleum products as disposable alternatives proliferate. Filtration sterilization supports biologics processing but captures only a narrow slice of sterilization equipment market share. Gamma radiation still handles the bulk of single-use medical device volumes, yet isotope supply gaps have opened doors for 10-MeV electron-beam accelerators. Although a complete accelerator line can cost more than USD 5 million, high-throughput hubs justify the spend through faster cycles and elimination of isotope logistics.

By End User: Ambulatory Centers Accelerate

Hospitals and clinics captured 55.53% revenue in 2025 owing to diverse procedural portfolios and validated central sterile supply departments. Ambulatory surgery centers, however, are forecast to advance at a 9.85% CAGR, widening the sterilization equipment market as more orthopedic, ophthalmic, and gastrointestinal cases migrate outpatient. Medicare certified 6,150 U.S. centers by late 2024, a 3.8% annual increase, and ASC procedure volumes climbed 6.2% in the same period. These facilities favor compact tabletop steam units paired with hydrogen-peroxide plasma chambers, achieving high turnover without the spatial demands of hospital-grade autoclaves. The cost-conscious model aligns with private payer incentives that reward same-day discharge.

Pharma and biotech producers form a smaller but rapidly expanding customer base. Each newly approved cell or gene therapy adds dedicated fill-finish lines that depend on validated sterilization tunnels or outsourced gamma, ethylene-oxide, or electron-beam cycles. Academic research institutes, dental offices, and veterinary hospitals round out demand with lower-capacity steam or dry-heat units, adding geographic breadth even if dollar contribution is modest.

Geography Analysis

North America accounted for 39.13% of 2025 revenue, anchored by the United States’ dense hospital network and high procedural rates. Replacement sales now dominate, as many facilities defer upgrades amid wider capital pressures, ranking sterilizers behind imaging and robotics in planned spending. Canada is centralizing capacity into regional hubs to spread maintenance overhead, whereas Mexico attracts medical-tourism cases that drive fresh installation of compact multi-modal systems.

Asia-Pacific is forecast to record the fastest 8.81% CAGR through 2031, fueled by hospital construction in China and India, rising insurance coverage, and growing adoption of robotic surgery. China added 1,200 hospitals over 2022-2024, most with central sterile departments large enough to justify mixed low-temperature and high-capacity steam installations. India’s mobile pilot improved instrument availability by 22% in district hospitals, signaling a pragmatic route to scale infection control where fixed infrastructure lags. Japan’s 28.9% 65-plus population share sustains cataract and joint replacement volumes that underpin steady autoclave demand.

Europe remains technology-focused. The 2024 Medical Device Regulation rollout increased audits of sterilization subcontractors, favoring firms with ISO-aligned documentation. Germany, France, and the United Kingdom represent most spending, while EU cohesion funds spur modernization across Southern and Eastern members. The Middle East is building academic hospitals that meet Joint Commission standards to support medical tourism. Sub-Saharan Africa is adopting solar-powered tabletop steam units and mobile trucks as stop-gaps against chronic power outages. South America’s private networks, especially in Brazil, purchase mid-tier steam and hydrogen-peroxide units to serve metropolitan surgical centers.

Competitive Landscape

The sterilization equipment market shows moderate concentration. STERIS, Getinge, and Fortive’s Advanced Sterilization Products division collectively supply a majority of installed capital, leveraging multiyear service contracts, sizable R&D budgets, and broad validation toolkits. STERIS’ Applied Sterilization Technologies segment posted 8% year-over-year growth in Q3 2024, driven by outsourced gamma and ethylene-oxide demand. Getinge’s Life Science division recorded 6% organic order growth, largely from biotech clients scaling aseptic lines. Stryker’s acquisition of TSO3 extends its hydrogen-peroxide plasma presence into ambulatory care.

White-space competition comes from mobile service operators and digital tracking specialists. E-BEAM Services invested in additional 10-MeV accelerators to hedge cobalt-60 shortages, highlighting a strategic pivot toward electron-beam capacity. Noxilizer promotes nitrogen-dioxide cycles that run at ambient temperature and leave no carcinogenic residues, targeting combination-product manufacturers. Smaller European vendors such as Belimed, MMM Group, and Steelco refine modular steam and low-temperature cabinets for space-constrained facilities. Regulatory recognition of vaporized hydrogen peroxide under Category A reduces market entry barriers, amplifying competitive churn around cycle chemistry, chamber size, and user-interface simplicity.

Sterilization Equipment Industry Leaders

Getinge AB

STERIS PLC

Fortive Corp. (Advanced Sterilization Products)

Solventum Corporation

Metall Zug (Belimed)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Getinge released the updated Solsus 66 Steam Sterilizer to address evolving central sterile supply department requirements.

- June 2025: Azenta Life Sciences expanded its FluidX line with electron-beam-treated externally threaded tubes, delivering a chemical-free sterile solution for laboratory sample storage.

Global Sterilization Equipment Market Report Scope

As per the scope of the report, sterilization equipment is an essential step in the reprocessing of reusable medical instruments and surgical instruments that have been contaminated, or potentially contaminated, by the patient's biological fluids. The aim of the sterilization is the prevention of potential cross-infection between patients by killing micro-organisms, such as bacteria, viruses, and many others. Therefore, effective cleaning of the instrument is particularly important to remove contamination physically.

The sterilization equipment market is segmented by equipment, end user, and geography. By equipment, the sterilization equipment market is segmented into high-temperature sterilization, wet/steam sterilization, dry heat sterilization, low-temperature sterilization including ethylene oxide (ETO), hydrogen peroxide plasma, ozone, and other low-temperature methods, filtration sterilization, and ionizing radiation sterilization comprising e-beam, gamma, and other ionizing technologies. By end user, the market is categorized into hospitals and clinics, pharma and biotech manufacturers, research and academic institutes, ambulatory surgery centers, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.

| High-temperature Sterilization | Wet/Steam Sterilization |

| Dry Heat Sterilization | |

| Low-temperature Sterilization | Ethylene Oxide (ETO) |

| Hydrogen Peroxide Plasma | |

| Ozone | |

| Other Low-temperature Methods | |

| Filtration Sterilization | |

| Ionizing Radiation Sterilization | E-beam |

| Gamma | |

| Other Ionizing Technologies |

| Hospitals & Clinics |

| Pharma & Biotech Manufacturers |

| Research & Academic Institutes |

| Ambulatory Surgery Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Equipment | High-temperature Sterilization | Wet/Steam Sterilization |

| Dry Heat Sterilization | ||

| Low-temperature Sterilization | Ethylene Oxide (ETO) | |

| Hydrogen Peroxide Plasma | ||

| Ozone | ||

| Other Low-temperature Methods | ||

| Filtration Sterilization | ||

| Ionizing Radiation Sterilization | E-beam | |

| Gamma | ||

| Other Ionizing Technologies | ||

| By End User | Hospitals & Clinics | |

| Pharma & Biotech Manufacturers | ||

| Research & Academic Institutes | ||

| Ambulatory Surgery Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the sterilization equipment market in 2031?

The sterilization equipment market size is expected to reach USD 14.72 billion by 2031.

Which equipment segment is growing fastest?

Low-temperature systems, especially hydrogen-peroxide plasma units, are forecast to expand at an 11.25% CAGR through 2031.

Why are ambulatory surgery centers investing heavily in sterilization capacity?

Outpatient migration of orthopedic, ophthalmic, and gastrointestinal procedures requires compact, quick-cycle sterilizers to maintain throughput without inpatient infrastructure.

How are cobalt-60 shortages affecting contract sterilization services?

Supply constraints are encouraging service providers to install electron-beam accelerators that deliver radiation without isotopes and reduce processing times.

Which regions will lead growth between 2026 and 2031?

Asia-Pacific is projected to register the highest 8.81% CAGR, driven by hospital construction in China and India and rising robotic-surgery adoption.

Page last updated on: