Static Application Security Testing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 0.68 Billion |

| Market Size (2031) | USD 1.89 Billion |

| Growth Rate (2026 - 2031) | 22.82% CAGR |

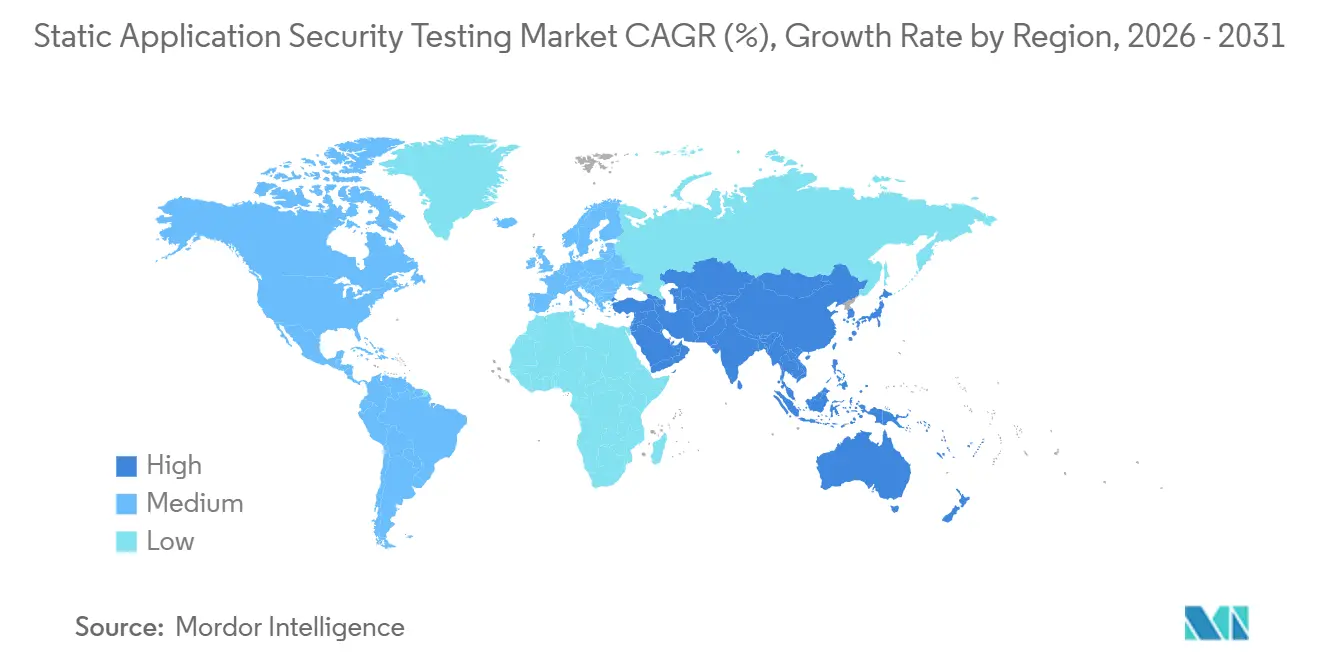

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

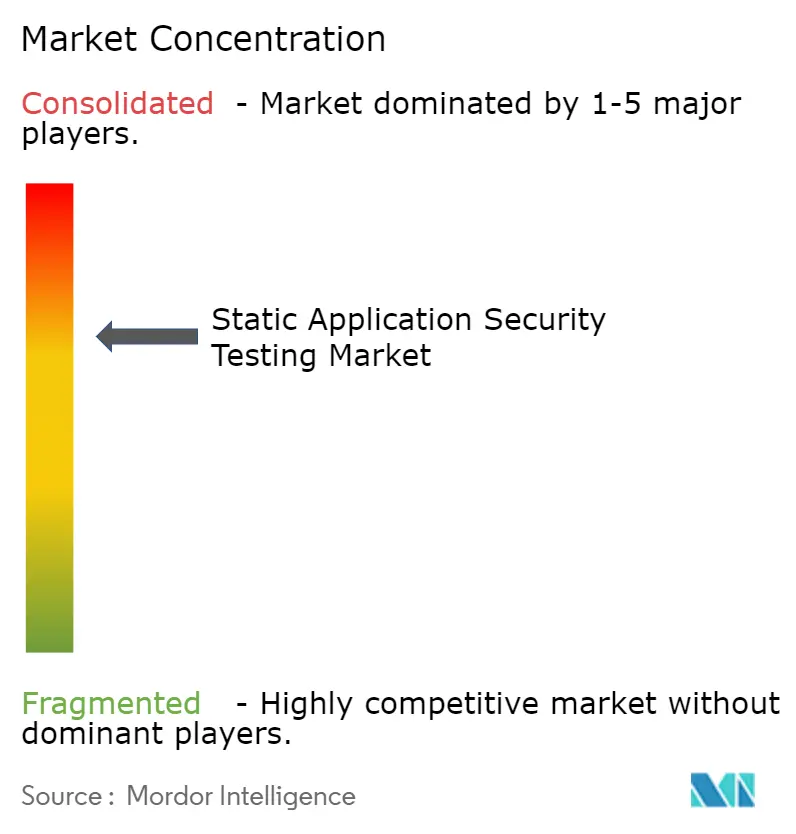

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Static Application Security Testing Market Analysis by Mordor Intelligence

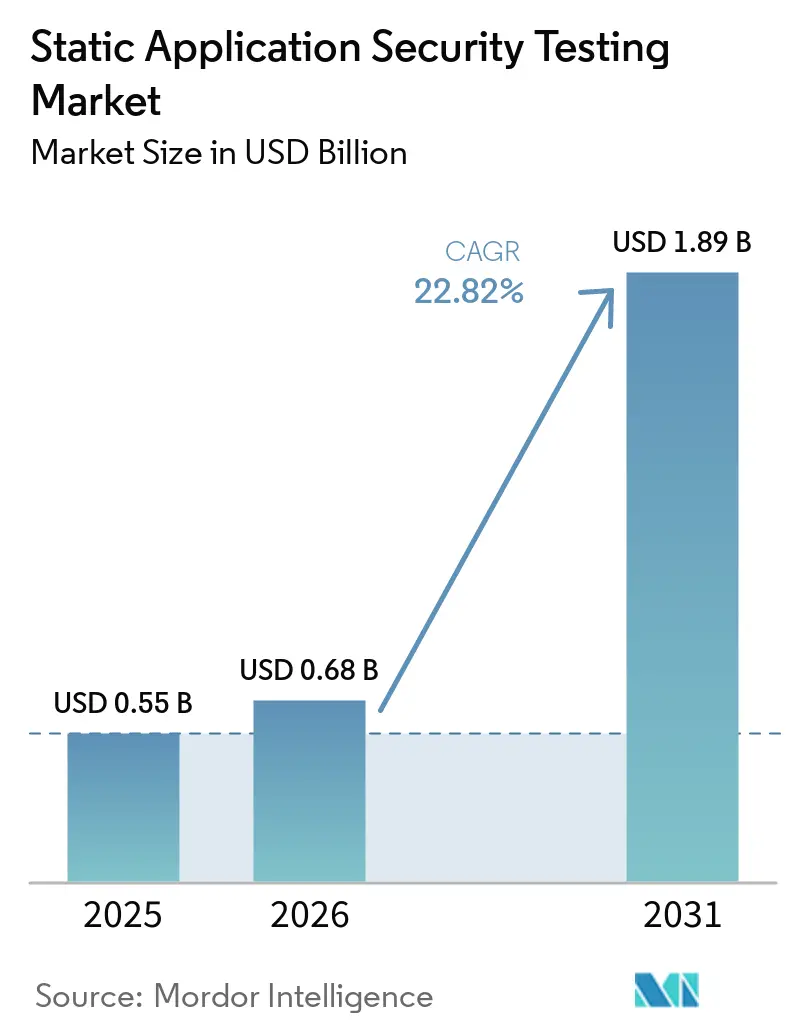

The static application security testing market size was valued at USD 0.55 billion in 2025 and is expected to grow from USD 0.68 billion in 2026 to reach USD 1.89 billion by 2031, at a 22.82% CAGR over 2026-2031. Heightened regulatory deadlines across the United States, Europe, and Asia are accelerating early-stage code scanning, while AI-generated code inflates vulnerability volumes, elevating demand for continuous in-IDE analysis. Enterprises are redirecting budgets from periodic penetration tests toward always-on static application security testing (SAST), and secure-by-design clauses inside federal and critical-infrastructure contracts have converted the tool from an optional control to a purchase-order requirement. Platform consolidation is squeezing point-solution vendors, favoring suites that combine SAST, software composition analysis, and secrets detection under a single policy engine. Hybrid deployment models that keep sensitive artifacts on-premises but burst compute to the cloud are emerging as the preferred architecture for regulated industries navigating data-sovereignty rules.

Key Report Takeaways

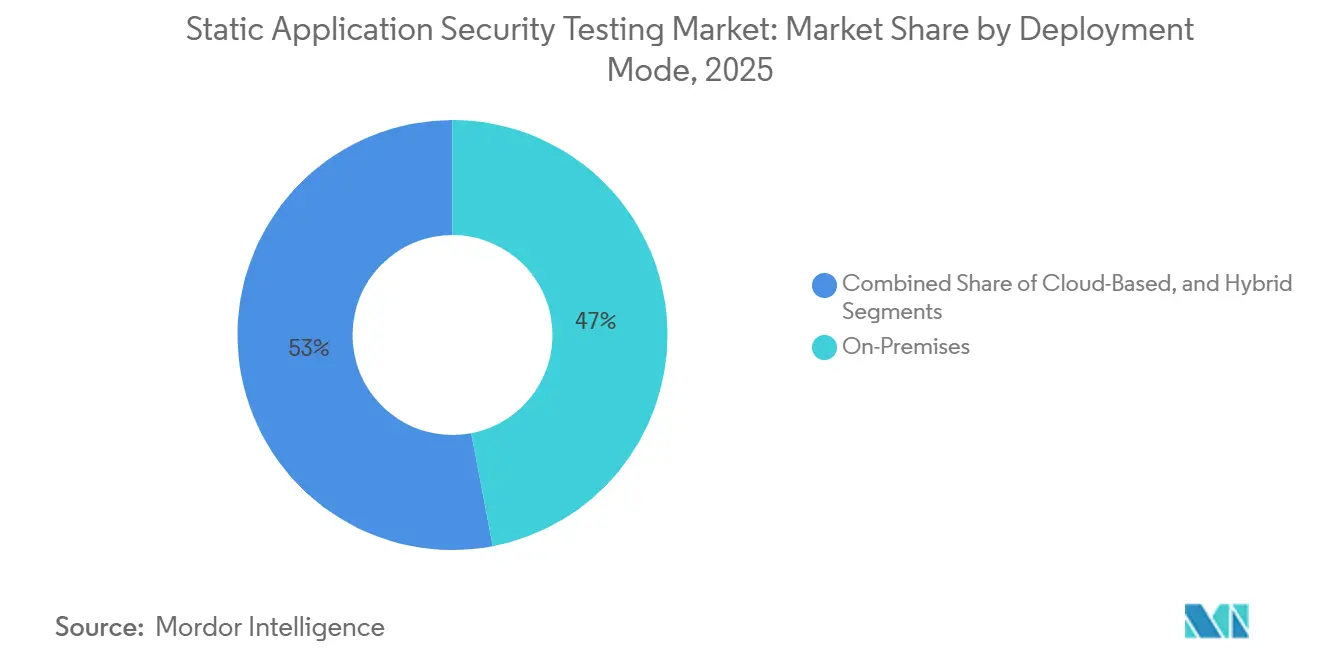

- By deployment mode, on-premises installations led with 47.02% of the static application security testing market share in 2025, while cloud-based deployments are projected to expand at a 24.4% CAGR through 2031.

- By organization size, large enterprises accounted for 70.30% of the static application security testing (SAST) market share in 2025, whereas small and medium enterprises are forecast to register a 23.3% CAGR during the same period.

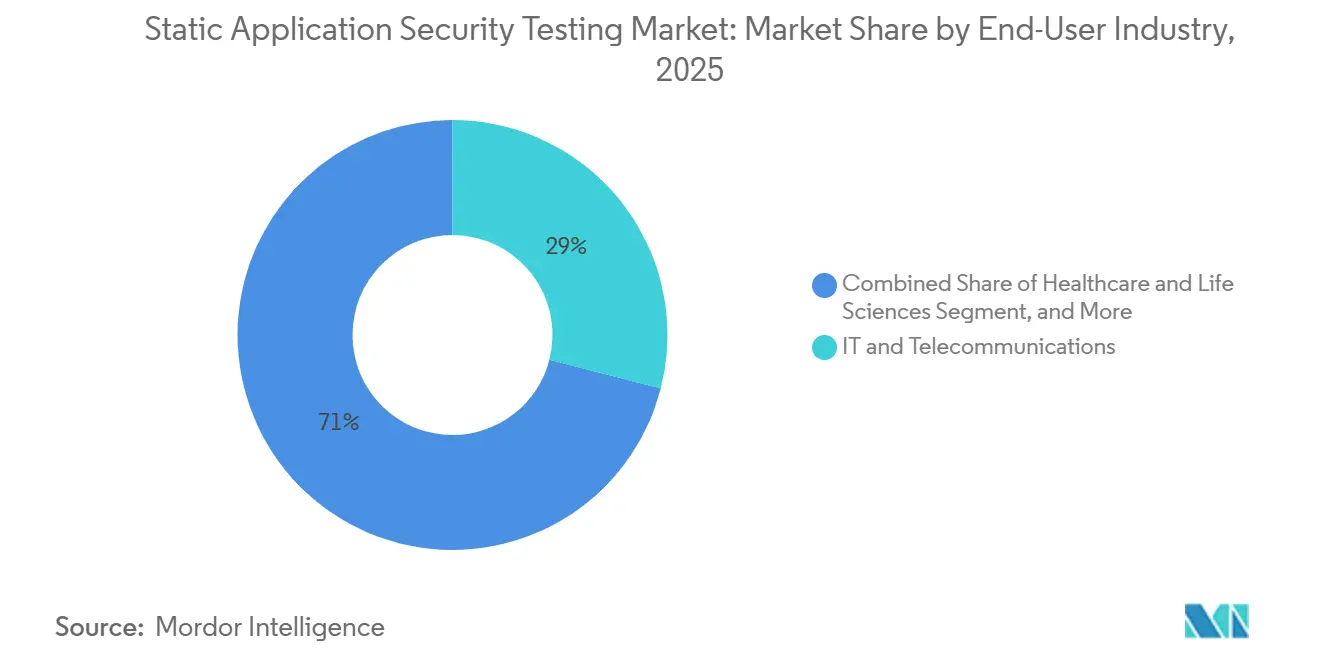

- By end-user industry, IT and telecommunications accounted for 29.00% of the SAST market share of 2025 spending, but healthcare and life sciences are anticipated to grow at a 24.88% CAGR through 2031.

- By the integration phase, CI/CD pipeline scanning captured 42.50% of the SAST market share of 2025 revenue, and IDE plugins are expected to grow at a 25.08% CAGR through 2031.

- By geography, North America accounted for 38.20% of global revenue in 2025, yet Asia-Pacific is set to grow at a 25.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Static Application Security Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise Of AI-Generated Code | +5.2% | Global with focus in North America and Europe | Short term (≤ 2 years) |

| Mandates On Software SBOMs | +4.8% | North America and EU, spill-over to APAC | Medium term (2-4 years) |

| API-First SDLC Shift | +3.6% | Global, led by North America and APAC | Medium term (2-4 years) |

| DevSecOps Tool-Chain Consolidation | +3.1% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Secure-By-Design Procurement Clauses | +3.7% | North America, EU, and APAC public sectors | Short term (≤ 2 years) |

| Quantum-Resistant Cryptography Audit Need | +2.4% | North America and Europe, early APAC uptake | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

API-first SDLC shift

Modern software relies on microservices that communicate through well-defined API endpoints. Static scanners built for monolithic code often miss authentication weaknesses or excessive data exposure across these endpoints. Retailer Sally Beauty gained full API inventory visibility within 30 days by adding API-aware scanners, underscoring measurable benefits.[1]APIsec, “Sally Beauty Automates API Security with APIsec,” apisec.ai Organisations shifting to API-centric architectures report 40% higher vulnerability detection when using scanners that parse Swagger or OpenAPI files alongside source code. This premium capability raises average selling prices, lifting revenue across the static application security testing market. The driver remains strongest in North America and Western Europe where microservices adoption is most mature.

Mandates on software SBOMs

Government orders now require suppliers to ship a software bill of materials that lists every open-source component. The OWASP 2025 advisory links 60% of critical Java bugs to third-party libraries, so buyers view SBOM functions as proof of secure code. Federal agencies such as the US Centers for Medicare & Medicaid Services have rolled out secret-scanning policies that reward vendors capable of real-time dependency monitoring.[2]US Centers for Medicare and Medicaid Services, “GitHub Secret Scanning,” security.cms.gov Vendors that automate SBOM generation and correlate findings with known CVEs widen their addressable base, fuelling growth for the static application security testing market.

Rise of AI-generated code

Veracode’s 2025 study showed AI-generated code carries a 45% higher vulnerability density than human-written baselines, with spikes in injection flaws and hard-coded secrets.[3]Chris Wysopal, “AI-Generated Code Vulnerability Analysis,” Veracode, VERACODE.COM Developers using assistants such as GitHub Copilot can create functional code blocks within seconds, yet manual review spends 15-30 minutes per issue, widening remediation backlogs. Inline SAST plugins that surface flaws during authoring reduce this gap and are now table stakes for enterprise tooling. The Cloud Security Alliance found that organizations without real-time AI code scanning logged 2.3 times more post-deployment vulnerabilities.[4]Cloud Security Alliance Research Team, “AI Code Security Research,” Cloud Security Alliance, CLOUDSECURITYALLIANCE.ORG FDA guidance published in February 2026 requires vendors to document SDLC controls for AI-assisted development, turning sub-second feedback loops from convenience into compliance.[5]Cybersecurity and Infrastructure Security Agency, “SBOM Minimum Elements Framework,” CISA, CISA.GOV

DevSecOps tool-chain consolidation

Security teams complain that 70% of triage time is lost to duplicate alerts across isolated tools. Buyers now demand unified dashboards that merge SAST, SCA and secrets detection. GitLab’s 27% revenue jump after bundling Advanced SAST into its Ultimate tier illustrates purchasing preference for a single pane of glass. Consolidation reduces total cost of ownership and speeds policy rollout, sustaining above-average price realisation in the static application security testing market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High False-Positive Fatigue | -3.8% | Global, acute in large enterprises with legacy SAST | Short term (≤ 2 years) |

| Shortage of AppSec Engineers | -2.9% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Legacy Monolith Refactoring Cost | -1.6% | North America and Europe, financial and manufacturing sectors | Long term (≥ 4 years) |

| Data-Residency Compliance Hurdles | -1.4% | EU and APAC, regulated industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High false-positive fatigue

Security analysts dedicate 70% of investigation time to alerts that turn out to be non-issues. This burden erodes trust and slows rollout of new policies. Smaller teams often mute scanner output, raising the risk of missed exploits. Vendors respond with machine-learning classifiers that push false-positive rates below 0.1%, but premium modules add cost that many mid-market buyers hesitate to absorb. Until accuracy improves across entry-level tiers, purchase cycles in the SAST market may elongate.

Shortage of AppSec engineers

Demand for specialists outstrips supply across major economies. Senior application security roles command six-figure salaries, yet universities graduate too few candidates. Large enterprises can pay, but SMEs struggle, leaving developers to run scans without deep security knowledge. Automated prioritisation and in-IDE fix suggestions help, yet complexity remains a barrier that tempers growth for the static application security testing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Sovereignty Concerns Anchor On-Premises Revenue

On-premises deployments held 47.02% of 2025 revenue as European banks, defense contractors, and healthcare providers retain code repositories behind their firewalls to meet DORA and GDPR oversight. Static application security testing market size gains here come from perpetual licenses bundled with professional services for high-assurance environments. Cloud-based scanning will nonetheless climb at a 24.4% CAGR to 2031, propelled by elastic compute that accelerates parallel scans across microservices. Hybrid models, which keep artifacts local yet offload compute to managed cloud nodes, balance sovereignty with scale and are emerging as preferred architectures for regulated entities.

Control versus velocity defines purchasing decisions. Cloud platforms integrate natively with GitHub, GitLab, and Azure DevOps, shrinking time-to-value, while on-premises installations incur infrastructure maintenance costs. Sovereign cloud regions offered by hyperscalers could erode the compliance advantage of on-premises tools. Vendors delivering identical feature sets across deployment options without price penalties position best to capture organizations navigating evolving residency mandates in the SAST market.

By Organization Size: SME Growth Hinges On Consumption-Based Pricing

Large enterprises generated 70.3% of 2025 revenue by embedding SAST into sprawling codebases and demanding deep customization. They negotiate enterprise-wide contracts that fold in training, premium support, and SLAs, producing predictable renewal streams. Small and medium enterprises, however, are forecast to add double-digit revenue at a 23.3% CAGR through 2031 as vendors introduce per-developer seat models and metered scanning that drop upfront costs.

Free community tiers from GitHub and SonarSource seed adoption, while AI-guided remediation lowers the expertise needed to interpret scan results. Once SMEs mature, upselling advanced capabilities such as SBOM generation and cross-file taint analysis increases contract value. Vendors excelling at land-and-expand motions convert grassroots developer adoption into organization-wide rollouts, expanding static application security testing market penetration across the mid-market.

By End-User Industry: Healthcare Leads Growth On FDA Compliance Pressure

IT and telecommunications held 29.00% of 2025 outlays because software vendors view code security as a customer trust differentiator. Yet healthcare and life sciences will surge at 24.88% CAGR through 2031 as FDA Computer Software Assurance guidance compels inclusion of SBOMs and documented AI controls in premarket dossiers. Hospitals also face HIPAA amendments that shorten breach notification windows, driving earlier adoption of code scanning. Banking and insurance institutions confront DORA’s annual resilience testing and tri-annual threat-led penetration regimes, embedding SAST as a prerequisite for board-level risk attestations.

Government and defense procurement frameworks now mandate SAST within continuous integration pipelines, while manufacturing and automotive firms implement the practice to support connected-product security and NIS2 supply-chain obligations. Retail adoption lags due to thin margins but climbs as API-driven payments raise fraud exposure. Sector-specific penalty regimes ultimately dictate adoption velocity.

By Integration Phase: IDE Plugins Gain Share On Developer-Experience Focus

CI/CD pipeline scanning owned 42.50% of 2025 billings as nightly jobs enforce security gates before production. IDE plugins, though, are set to outpace at a 25.08% CAGR, surfacing flaws during code creation and eliminating up to 90% of rework according to Checkmarx’s February 2026 Kiro integration. Developers demand sub-second feedback, so vendors deploy lightweight heuristics in editors and reserve deep dataflow passes for CI jobs.

Centralized batch scans remain for legacy monoliths and compliance audits, but are declining in relative influence. Leading platforms now blend the three scan tiers and correlate alerts, giving engineers a single risk narrative rather than disjointed reports. Context-rich integration wins mindshare and reduces alert fatigue, thereby increasing fix rates and demonstrable risk reduction in the SAST market.

Geography Analysis

North America captured 38.2% of 2025 revenue, propelled by CISA’s USD 331 million Continuous Diagnostics and Mitigation budget and embedded SBOM pilots that turn SAST into a contract deliverable. OMB’s shift to risk-based attestations rewards platforms that correlate static findings with runtime exposure, driving refreshed procurement among federal suppliers. Canada is aligning procurement language, and Mexican regulators are applying DORA-style operational testing to cross-border banks, extending regional headroom.

Asia-Pacific is the fastest mover with a 25.27% CAGR forecast to 2031. Taiwan’s 2025 National Cybersecurity Strategy requires secure-by-design attestations across semiconductor and infrastructure supply chains. New Zealand’s 2026-2030 cybersecurity roadmap targets quantum readiness and critical-infrastructure resilience, prompting utilities to adopt code scanning. Fragmented regulations in China, Japan, India, and South Korea create localization complexity that favors vendors with multilingual rule sets and regional support teams.

Europe sits at a compliance crossroads. DORA took effect in January 2025, imposing four-hour incident reporting and threat-led penetration cycles that include source-code assessments, while NIS2 and the Cyber Resilience Act layer additional obligations. Only 14 of 27 member states fully transposed NIS2 by mid-2025, yet enforcement fines reach EUR 10 million (USD 11.8 million), pushing enterprises to fast-track SAST rollouts. Sovereign-cloud incentives and on-premises favoritism persist among banks and insurers, but hybrid models broaden appeal by balancing oversight with elasticity.

Competitive Landscape

Autonomous Supply-Chain Control-Towers

The static application security testing market remains moderately competitive. Synopsys, Veracode, and Checkmarx headline the enterprise tier, differentiating through high-precision engines and AI-generated remediation. GitHub, GitLab, and SonarSource leverage community adoption, embedding SAST inside developer workflows at near-zero switching costs. Synopsys’ USD 2.1 billion divestiture in 2024 and Checkmarx’s private-equity courtship underline consolidation pressure.

Partnerships rival acquisitions; Veracode’s integration with Palo Alto Networks correlates code flaws with cloud posture data, showcasing code-to-cloud risk narratives. Disruptors such as DeepSource and OX-Security target self-service SME buyers with consumption pricing. False-positive reduction, hybrid scanning, and agentic AI triage are now battleground features. Vendors harnessing LLMs for contextual correlation and ready-made compliance reports generation stand to expand their share of the static application security testing industry as SAST commoditizes as a standalone tool.

Static Application Security Testing Industry Leaders

Synopsys, Inc. (Software Integrity Group)

Veracode, Inc.

Checkmarx Ltd.

Snyk Limited (SAST module only)

Sonatype, Inc. (Code Quality & SAST)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Checkmarx introduced AI SAST with LLM-powered analysis, Triage Assist, and Remediation Assist to cut manual effort.

- March 2026: Veracode rolled out Veracode Fix for SCA, bundling multi-file pull-request remediation.

- February 2026: Checkmarx enhanced Kiro IDE support with real-time scanning inside developer workflows.

- January 2026: Palo Alto Networks integrated Veracode scanning into Cortex Cloud for code-to-cloud visibility.

Global Static Application Security Testing Market Report Scope

The Static Application Security Testing Market Report is Segmented by Deployment Mode (On-Premises, Cloud-Based, Hybrid), Organization Size (Large Enterprises and Small and Medium Enterprises), End-User Industry (IT and Telecommunications, Banking, Financial Services, and Insurance, Healthcare and Life Sciences, Government and Defense, Retail and E-Commerce, Manufacturing and Automotive, Other End-User Industry (Energy, Education)), Integration Phase (IDE Plugins, CI/CD Pipeline, and Centralized Scanning), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premises |

| Cloud-Based |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| IT and Telecommunications |

| Banking, Financial Services and Insurance |

| Healthcare and Life Sciences |

| Government and Defense |

| Retail and E-Commerce |

| Manufacturing and Automotive |

| Other End-User Industry (Energy, Education) |

| IDE Plugins |

| CI/CD Pipeline |

| Centralized Scanning |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment Mode | On-Premises | ||

| Cloud-Based | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-User Industry | IT and Telecommunications | ||

| Banking, Financial Services and Insurance | |||

| Healthcare and Life Sciences | |||

| Government and Defense | |||

| Retail and E-Commerce | |||

| Manufacturing and Automotive | |||

| Other End-User Industry (Energy, Education) | |||

| By Integration Phase | IDE Plugins | ||

| CI/CD Pipeline | |||

| Centralized Scanning | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the static application security testing market in 2026?

Mordor Intelligence estimates static application security testing market size at USD 0.68 billion in 2026 and projects it to reach USD 1.89 billion by 2031.

Which deployment mode is growing fastest?

Cloud-based SAST is forecast to expand at a 20.4% CAGR through 2031 as organizations seek elastic compute and simplified integration.

Why is healthcare adoption accelerating?

FDA Computer Software Assurance rules effective 2026 mandate SBOMs and documented SDLC controls, pushing healthcare and life-sciences firms toward continuous code scanning.

What is the main barrier to SAST adoption?

High false-positive rates consume developer time and erode trust, although vendors cutting inaccuracies below 5% are reversing this trend.

Which region will contribute most new revenue by 2031?

Asia-Pacific, led by Taiwan, Singapore, and New Zealand policies, is set to grow at a 22% CAGR and add the largest incremental spend.

Page last updated on: