Stainless Steel Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

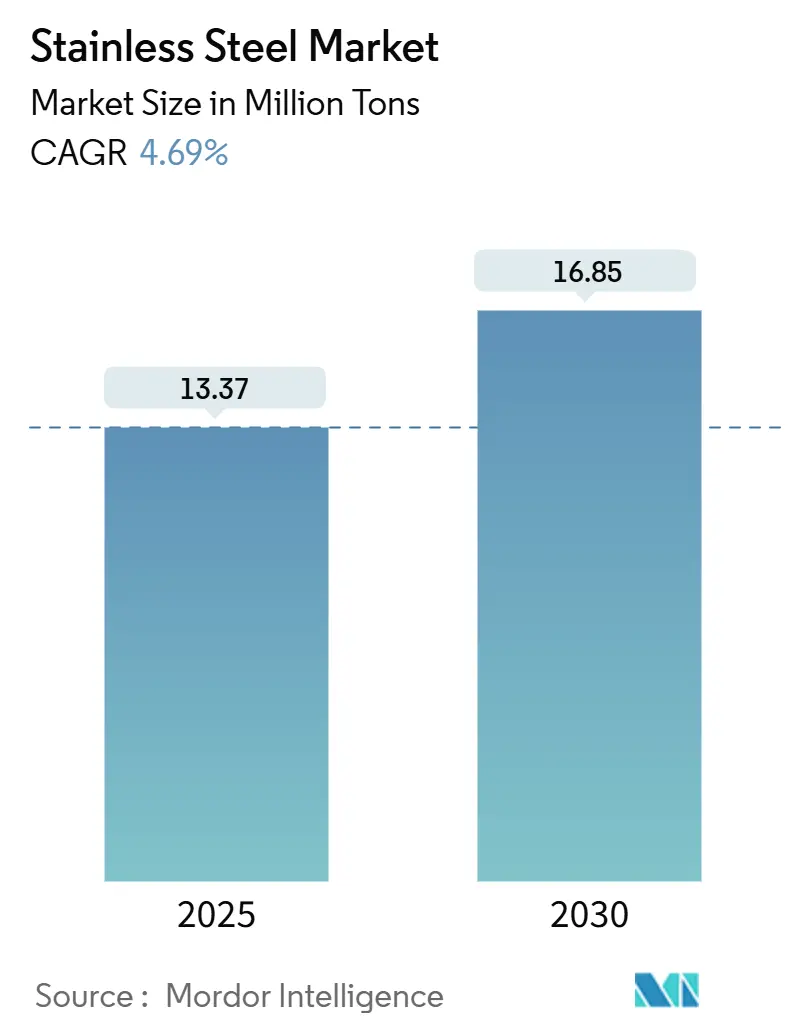

| Market Volume (2025) | 13.37 Million tons |

| Market Volume (2030) | 16.85 Million tons |

| Growth Rate (2025 - 2030) | 4.69% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Stainless Steel Market Analysis by Mordor Intelligence

The stainless-steel market stands at 13.37 million tons in 2025 and is forecast to reach 16.85 million tons by 2030, advancing at a 4.69% CAGR. Robust construction activity, rising adoption of cryogenic grades for LNG logistics, and government-backed green-hydrogen investments are expanding demand even as raw-material cost swings reshape purchasing decisions. Producers are accelerating process electrification and recycled-content strategies to comply with emerging “green steel” norms, while downstream users in food processing and coastal infrastructure are locking in premium grades to lower lifetime costs. Trade remedies in the European Union and India’s procurement rules redraw supply chains, giving regional mills better pricing power. At the same time, appliance makers are pivoting toward low-nickel ferritic grades in response to volatile nickel prices, creating fresh competitive angles in alloy development.

Key Report Takeaways

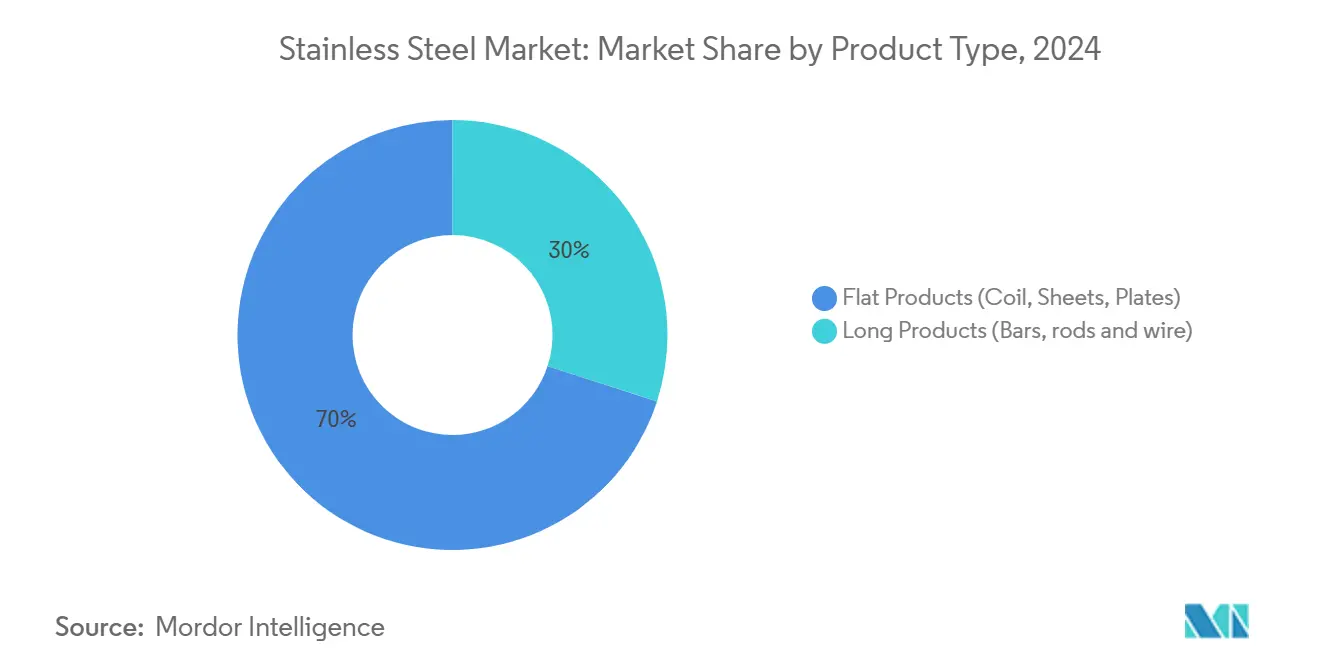

- By product type, flat products led with 70% of stainless-steel market share in 2024 and are projected to rise at a 4.9% CAGR to 2030.

- By form, cold-rolled materials accounted for 60% of the stainless-steel market size in 2024 and are expanding at a 5.1% CAGR through 2030.

- By grade, the 300 Series commanded 65% of the stainless-steel market size in 2024, while duplex grades recorded the fastest 5.2% CAGR to 2030.

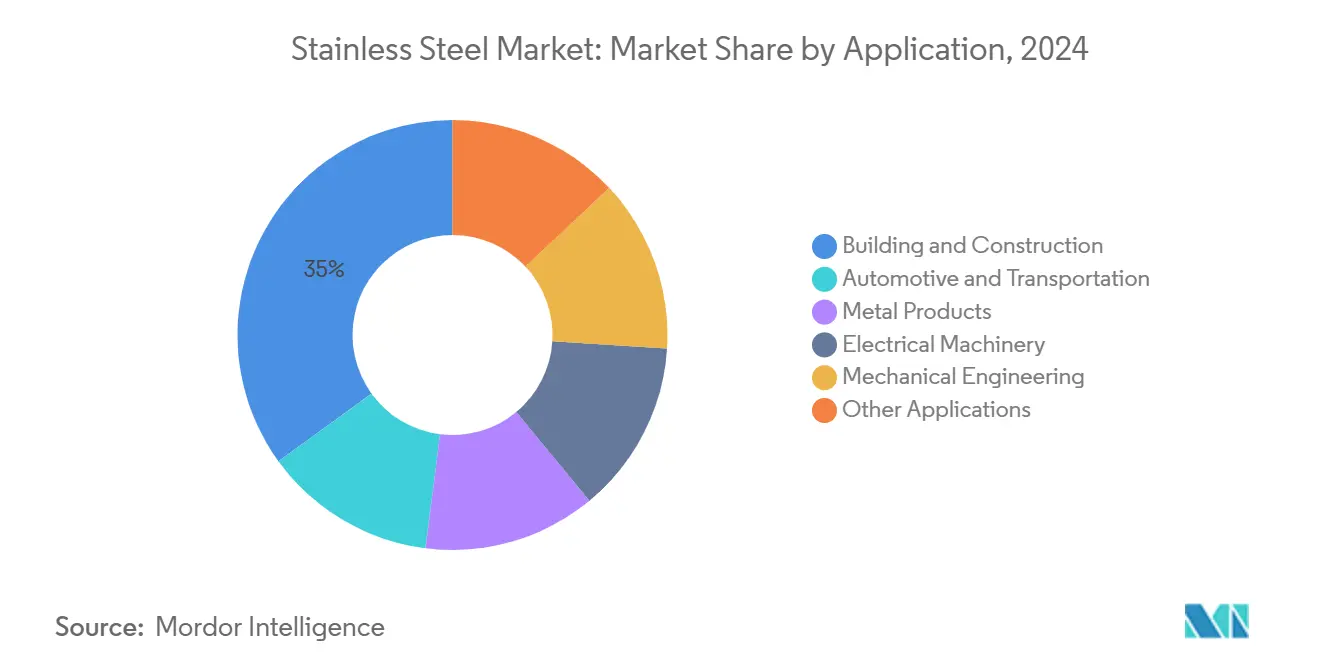

- By application, building and construction held 35% of the stainless-steel market share in 2024; automotive and transportation is the fastest-growing use at a 5.1% CAGR through 2030.

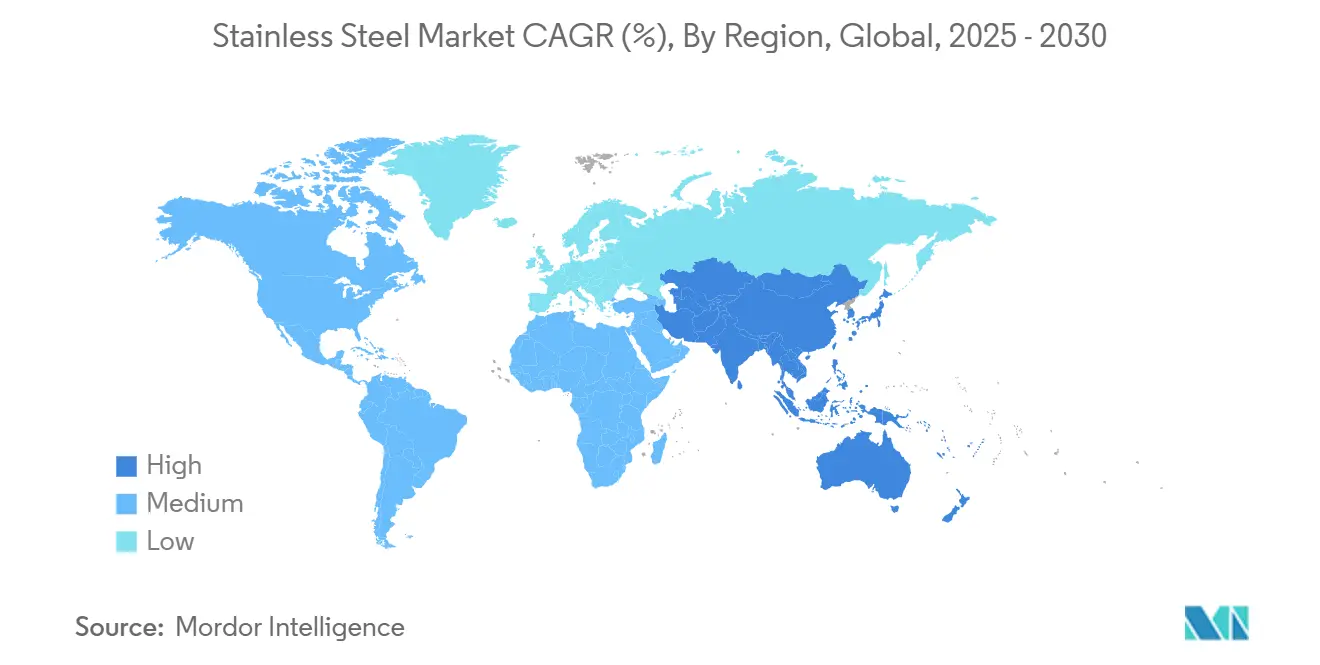

- By geography, Asia-Pacific contributed 65% to the stainless-steel market in 2024, growing at 5.3% annually to 2030.

Global Stainless Steel Market Trends and Insights

Driver Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory stainless-steel rebar in Indian coastal bridges | +0.8% | India, spillover to the Asia coastal markets | Medium term (2-4 years) |

| LNG and cryogenic storage expansion across Asia | +0.7% | China, Japan, South Korea | Medium term (2-4 years) |

| FSMA-driven food-equipment replacement in the United States | +0.5% | North America, gradual EU uptake | Short term (≤2 years) |

| EU green-hydrogen electrolyzer build-out | +0.6% | European Union; spillover North America | Long term (≥4 years) |

| Growing Demand from Construction | +0.4% | Global, with the strongest impact in Asia-Pacific | Medium term (≈3-4 yrs) |

| Source: Mordor Intelligence | |||

Mandatory Use of Stainless-Steel Rebar in India’s Coastal Infrastructure Codes

India’s highway authority now requires stainless-steel reinforcement in bridges exposed to marine conditions, guaranteeing multi-decade demand for duplex and 300-series grades[1]Ministry of Road Transport and Highways, “Technical Circulars on National Highways,” morth.nic.in. The rule lifts baseline consumption because stainless rebar delivers 100-year service life and cuts maintenance outlays over carbon steel alternatives[2]Stainless Steel Rebar Association, “Why stainless?” stainlesssteelrebar.org. Domestic mills gain further advantage under new procurement policies favoring locally melted steel.

LNG and Cryogenic Storage Boom Across Asia Stimulating 304L/316L Demand

China’s latest order for 1,000 LNG vehicle cylinders confirms accelerating uptake of cryogenic stainless grades across transport and storage assets. Research on liquid-hydrogen tanks shows 316L retains strength at –253 °C, cementing its role in next-generation energy logistics. The surge favors mills with deep metallurgical expertise and high purity refining capacity.

Replacement of Food-Processing Equipment Under U.S. FSMA Sanitary Rules

FSMA compliance is forcing processors to replace legacy machinery with smooth, self-draining stainless designs that reduce cleaning labor. Equipment buyers now weigh total cost of ownership, rewarding suppliers that engineer hygienic layouts aligned with the “10 Commandments of Sanitary Design”.

Green-Hydrogen Electrolyzer Build-out in the EU Requiring Duplex Grades

The European Commission approved EUR 6.9 billion in state aid for hydrogen infrastructure that specifies corrosion-resistant duplex plates for electrolyzer stacks[3]European Commission, “State aid for the hydrogen value chain,” ec.europa.eu . Additional funding via the European Hydrogen Bank targets 1.58 million tonnes of renewable hydrogen over ten years, anchoring long-run demand for specialty stainless.

Restraint Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nickel-price volatility driving ferritic substitution | –0.6% | Global appliance hubs | Short term (≤2 years) |

| EU anti-dumping tariffs on Chinese imports | –0.4% | European Union; global trade flows | Short term (≤2 years) |

| Availablility of subsitutes | -0.2% | Global, particularly in non-critical applications | Medium term (≈3-4 yrs) |

| Source: Mordor Intelligence | |||

Nickel-Price Volatility Prompting Appliance OEM Substitution

Appliance manufacturers are strategically pivoting to alternative stainless steel grades with reduced nickel content, spurred by the ongoing volatility in nickel prices. This shift is noteworthy, given that in common grades such as Core 304 and Supra 316L, nickel can constitute more than 65% of the cost. Appliance makers are therefore adopting low-nickel ferritic grades such as Core 4509, tempering growth in austenitic demand.

EU Anti-Dumping Tariffs on Chinese Imports Raising Input Costs

Provisional duties on tin-coated flat products from China raise delivered prices by 20-30%. Importers rushed to stock ahead of the levy, but long-term sourcing is shifting toward local mills and alternative Asian suppliers.

Segment Analysis

By Product Type: Flat Products Lead Through Versatility

Flat products held 70% of stainless-steel market share in 2024 and are on track for a 4.9% CAGR through 2030. This dominance secures the largest stainless steel market size contribution because coils, sheets, and strips meet structural, cladding, and automotive panel needs. Construction firms value their corrosion resistance and aesthetic uniformity, while automakers use thin gauges to lighten vehicles and meet emission rules. Growth also stems from the increased use of duplex flat plates in LNG tanks and electrolyzers.

Heightened performance requirements keep flat products attractive even when nickel prices fluctuate, yet long product producers counter with low-nickel duplex bars to defend margins. Procurement managers weigh life-cycle savings against upfront costs, and the outcome tends to favor flat product producers with in-house service centers that offer cut-to-length, polishing, and plasma-welded plate solutions.

Note: Segment shares of all individual segments available upon report purchase

By Form: Cold Rolled Dominates Through Superior Finish

Cold-rolled stainless accounted for 60% of the 2024 stainless steel market size and is progressing at a 5.1% CAGR. Its smooth surface supports downstream painting, polishing, and deep drawing, which drives usage in elevator cabins, appliances, and medical devices. Cold rolling also raises yield strength, allowing thinner gauges that reduce material cost without performance loss. Hot-rolled plate retains relevance in heavy-vehicle frames and pressure vessels but faces limited finish options. Cold-drawn wire, though niche, attracts precision spring makers requiring tight tolerances.

Automotive OEMs increasingly adopt cold-rolled grades to shed weight and improve crash energy absorption. Food equipment builders specify 2B-finish 304 sheets that clean easily and resist pitting. Mills with integrated pickling and bright-annealing lines secure higher conversion margins because they can deliver ready-to-fabricate material, shorten customer lead times and enhance loyalty.

By Grade: 300 Series Maintains Premium Position

The 300 Series kept a 65% volume share in 2024, or 8.3 million tons, reaffirming its place at the top of the stainless-steel market. Its combination of chromium and nickel delivers unmatched formability and corrosion performance for dairy, beverage, and architectural segments. Duplex grades expand fastest at 5.2% per year, thanks to their strength-to-weight edge and lower nickel reliance. This momentum is prominent in desalination plants, LNG pipelines, and hydrogen systems, where chloride-stress cracking resistance is critical.

By Application: Construction Builds Foundation for Growth

The construction sector absorbed 35% of stainless-steel market consumption in 2024, underpinned by urban rail, airports, and façade refurbishments. Stainless cladding resists grime in polluted megacities and meets green-building rating needs thanks to 90% recycled content. Life-cycle costing convinces project owners to choose duplex plate for footbridges and roof trusses, driving steady procurement even when commodity prices spike.

Automotive and transportation show the fastest 5.1% CAGR as electric-vehicle makers adopt martensitic safety components and battery enclosures. Metal products, electrical machinery, and mechanical engineering hold diverse but stable demand for valves, pumps, and fasteners that operate in corrosive or hygienic settings. Growing consumer awareness of durability sees stainless cookware and personal-care items gaining share in household goods.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific dominated the stainless-steel market with a 65% share. Regional demand grows at 5.3% annually to 2030, supported by China’s continuing output leadership and India’s capacity expansion plan.

In North America, the United States is upgrading food-processing plants to meet FSMA standards, spurring sanitary-finish sheet orders. EU electrolyzer subsidies of EUR 6.9 billion encourage local duplex plate purchases. Anti-dumping duties on Chinese coated steel amplify domestic order books. However, higher energy costs versus Asia weigh on hot-rolled profitability.

South America and the Middle-East, and Africa regions, while currently holding smaller market shares, are experiencing growth driven by infrastructure development and industrialization. Countries like Saudi Arabia and the UAE are increasing stainless steel consumption in construction and desalination projects in the Middle East, leveraging the material's corrosion resistance in harsh environments.

Competitive Landscape

The global stainless-steel market exhibits high fragmentation. The competitive dynamics are shifting as companies pursue strategic consolidation to enhance scale economies and geographic reach. Sustainability has emerged as a key competitive differentiator, with companies like Outokumpu introducing Circle Green stainless steel, which achieves a carbon footprint as low as 7% of the global average by utilizing 100% recycled content and renewable energy sources. The competitive landscape is further complicated by trade tensions and anti-dumping measures, creating regional market distortions that favor local producers in protected markets while challenging exporters facing tariff barriers.

Stainless Steel Industry Leaders

-

China BaoWu Steel Group Corporation Limited

-

Acerinox

-

Jindal Stainless Limited

-

POSCO

-

TSINGSHAN HOLDING GROUP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: United States Steel Corporation, a stainless steel manufacturer, and Nippon Steel Corporation finalized their merger. United States Steel will continue U.S. operations, while Nippon plans to build a new facility by 2028.

- May 2024: Jindal Stainless Limited unveiled a substantial investment plan of USD 650 million, aiming to boost its production capacity by 40% to reach 4.2 million tonnes per annum in Indonesia, focusing on a stainless steel melt shop.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the stainless-steel market as the aggregate melt-shop production and first-sale shipments of corrosion-resistant iron-based alloys that contain at least 10.5% chromium and, when required, nickel, molybdenum, or other elements to achieve specified mechanical and aesthetic properties. Markets for downstream fabricated products, scrap trading, and specialty alloys such as super-duplex grades are outside the scope.

Scope exclusion: powder metallurgy stainless, clad plate, and castings remain beyond the present study.

Segmentation Overview

- By Product Type

- Flat Products (Coil, Sheets, Plates)

- Long Products (Bars, rods and wire)

- By Form

- Hot Rolled

- Cold Rolled

- Cold Drawn

- By Grade

- 200 Series

- 300 Series

- 400 Series

- Duplex

- Precipitation-Hardening and Others

- By Application

- Building and Construction

- Automotive and Transportation

- Metal Products

- Electrical Machinery

- Mechanical Engineering

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Vietnam

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Turkey

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- Qatar

- United Arab Emirates

- Turkey

- South Africa

- Nigeria

- Egypt

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with melt-shop planners in Asia, European service center buyers, construction contractors, and automotive materials engineers across key producing and consuming nations. These discussions confirmed utilization rates, alloy surcharge pass-through, and regional demand pivots, allowing us to tighten assumptions harvested from secondary material.

Desk Research

Our analysts begin with public datasets that track stainless steel flows, such as annual melt-shop output from the International Stainless Steel Forum, UN Comtrade customs codes for 72xx HTS categories, and capacity filings posted by regional associations like Eurofer and the Specialty Steel Industry of North America. Company 10-Ks, investor decks, and export refund registers further refine grade mixes and average selling prices. Subscription resources, D&B Hoovers for plant-level revenues and Dow Jones Factiva for transaction news, anchor corporate splits. Patent libraries on Questel and shipment tallies from Volza help spot emerging uses and trade corridors. The sources listed illustrate, not exhaust, the evidence base that underpins desk research.

Market-Sizing & Forecasting

A blended top-down build starts with ISSF production, net imports, and verified inventory swings to recreate apparent consumption by region. We then cross-check totals with selective bottom-up tests, supplier roll-ups of slab capacity and sampled average selling price times volume, for credibility. Variables such as residential floor space completions, light vehicle output, nickel price premia, recycling intensity, and grade mix shifts feed a multivariate regression and scenario analysis to forecast demand through 2030. Gaps in bottom-up coverage are bridged with channel checks and median ASP ladders derived from primary interviews.

Data Validation & Update Cycle

Outputs run through variance filters against historical elasticity bands; anomalies trigger a second analyst review before sign-off. Models refresh annually, with mid-cycle updates when visible events, trade rulings, smelter outages, or policy shocks, move the baseline.

Why Our Stainless Steel Baseline Earns Uncommon Trust

Published estimates differ because firms choose distinct units, pricing assumptions, and refresh cadences.

Understanding these levers is crucial for users comparing numbers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 13.37 million tons (2025) | Mordor Intelligence | - |

| USD 216.16 billion (2024) | Global Consultancy A | Reports revenue only and excludes long product tonnage, leading to larger value yet unaligned volume base. |

| USD 126.36 billion (2024) | Trade Journal B | Uses spot alloy surcharges without regional weighting and omits 200-series volumes, trimming overall size. |

The comparison shows that when scope, unit of account, and update rhythm diverge, headline numbers shift markedly.

By starting with melt-shop tonnage, layering price discovery from tier-1 interviews, and revisiting the model each year, Mordor delivers a balanced, transparent baseline that decision-makers can retrace and audit with confidence.

Key Questions Answered in the Report

What is the current size of the stainless-steel market?

The stainless-steel market stands at 13.37 million tons in 2025 and is on a 4.69% CAGR path to 16.85 million tons by 2030.

Which region dominates stainless steel demand?

Asia-Pacific leads with 65% of 2024 volume and maintains the fastest 5.3% annual growth through 2030, led by China and India.

Why are duplex grades gaining popularity?

Duplex stainless offers double the strength of standard austenitic grades, lower nickel content for cost stability, and superior corrosion resistance required in desalination, LNG, and hydrogen projects.

How is nickel-price volatility affecting alloy selection?

Volatile nickel prices push appliance manufacturers to substitute toward low-nickel ferritic grades, trimming demand for traditional 300-series stainless.

What drives stainless steel demand in food processing?

U.S. FSMA sanitary rules necessitate stainless equipment with smooth, easily cleaned surfaces, triggering equipment upgrades that boost sheet and tube consumption.

Page last updated on: