Spain Pharmaceutical Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

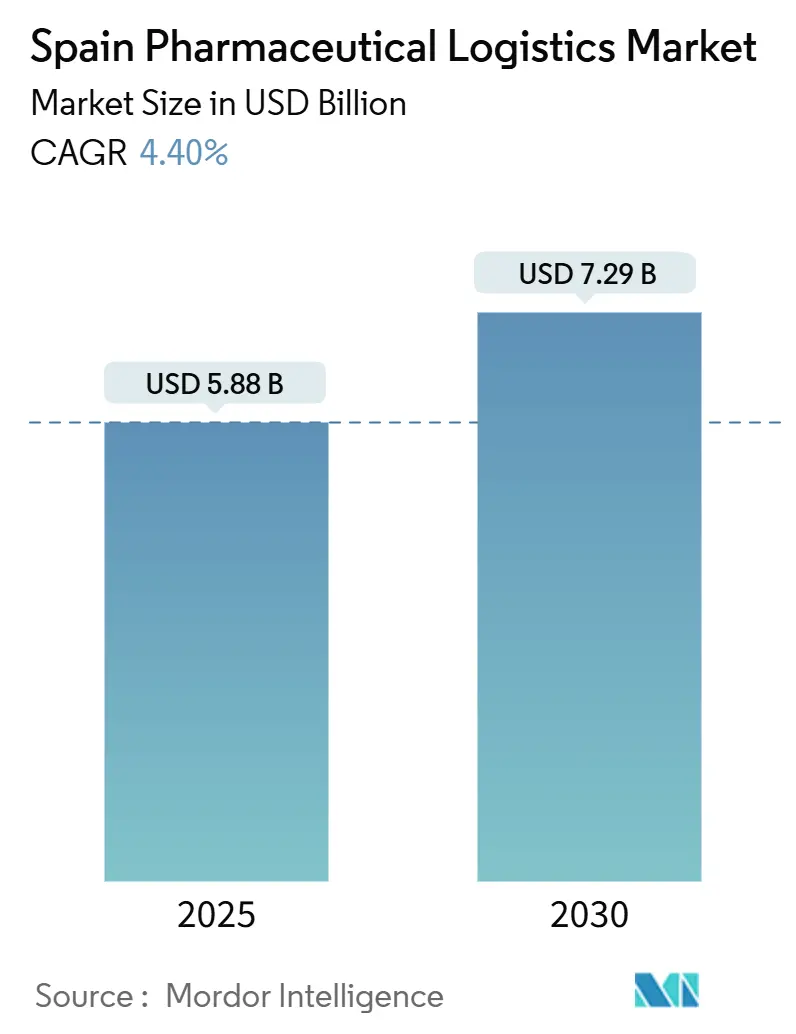

| Market Size (2025) | USD 5.88 Billion |

| Market Size (2030) | USD 7.29 Billion |

| Growth Rate (2025 - 2030) | 4.40% CAGR |

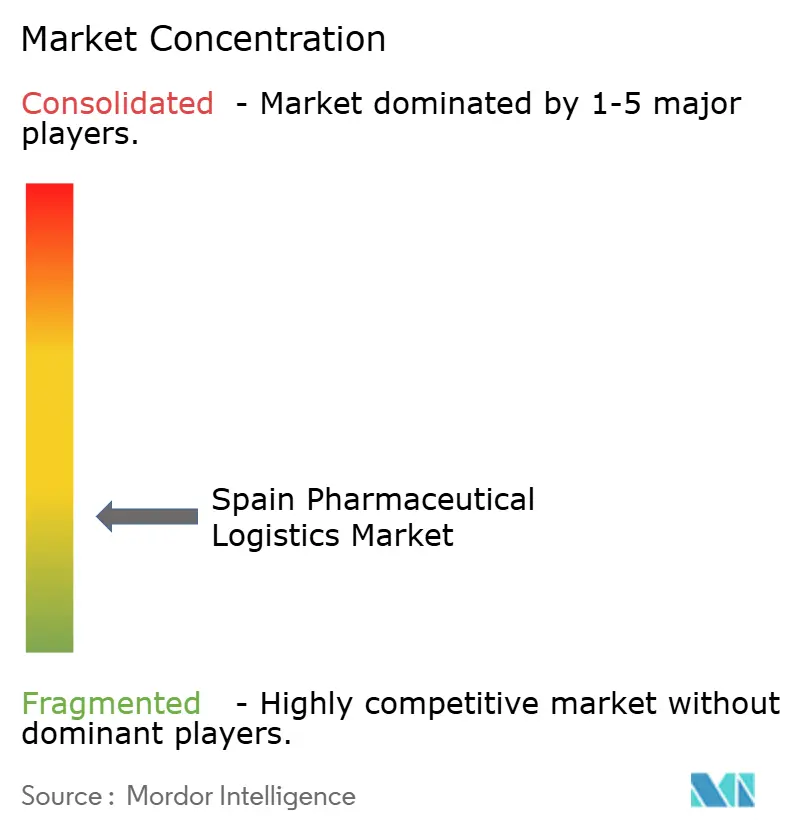

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spain Pharmaceutical Logistics Market Analysis by Mordor Intelligence

The Spain Pharmaceutical Logistics Market size is estimated at USD 5.88 billion in 2025, and is expected to reach USD 7.29 billion by 2030, at a CAGR of 4.40% during the forecast period (2025-2030).

Robust motorway, port, and airport capacity positions Spain as a Southern European gateway that reduces lead times for temperature-sensitive medicines and heightens demand for end-to-end visibility tools[1]Invest in Spain, “Transport and Logistics Industry in Spain,” investinspain.org. Logistic parks clustered along the Mediterranean and Atlantic corridors speed cross-border flows into France and Italy, which is critical as 80% of European medicines now require temperature control. Regulatory reforms around GDP certification tighten quality thresholds and reward operators with automated monitoring systems. Competitive intensity is rising because global leaders are injecting billions into Spanish capacity, accelerating technology adoption, and sparking consolidation.

Key Report Takeaways

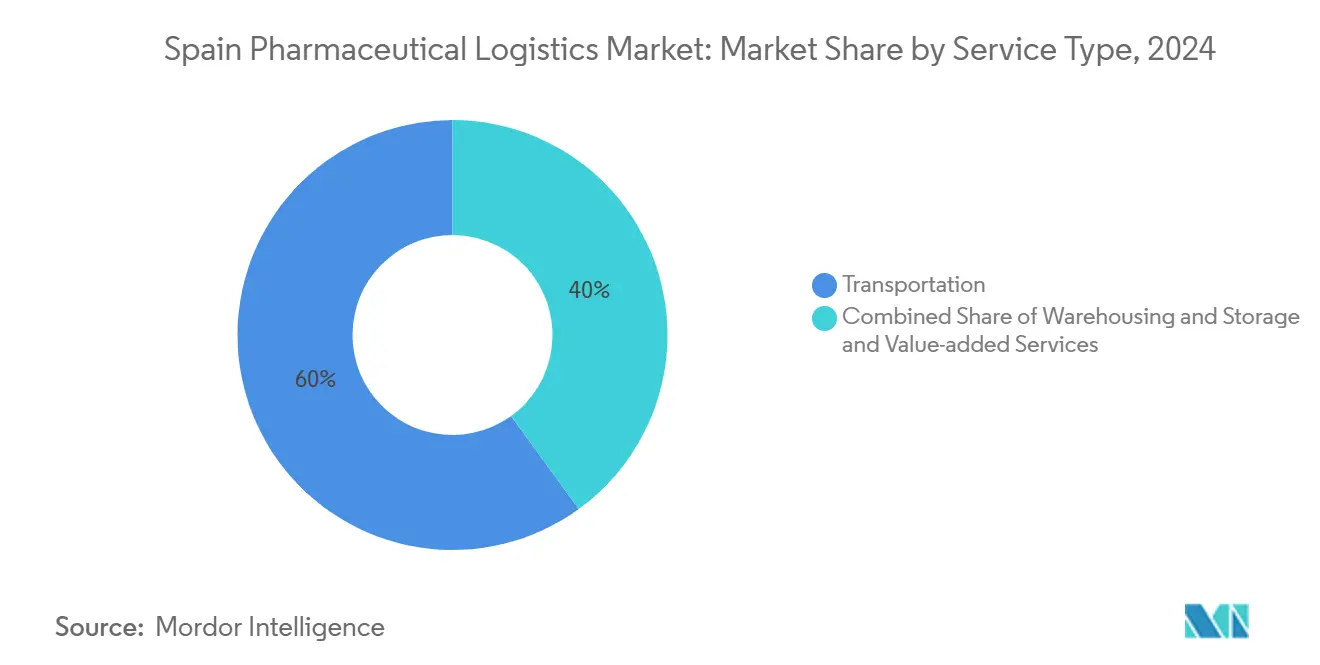

- By service type, transportation commanded 60% of the Spain pharmaceutical logistics market share in 2024, whereas value-added services & others are forecast to expand at a 4.80% CAGR through 2030.

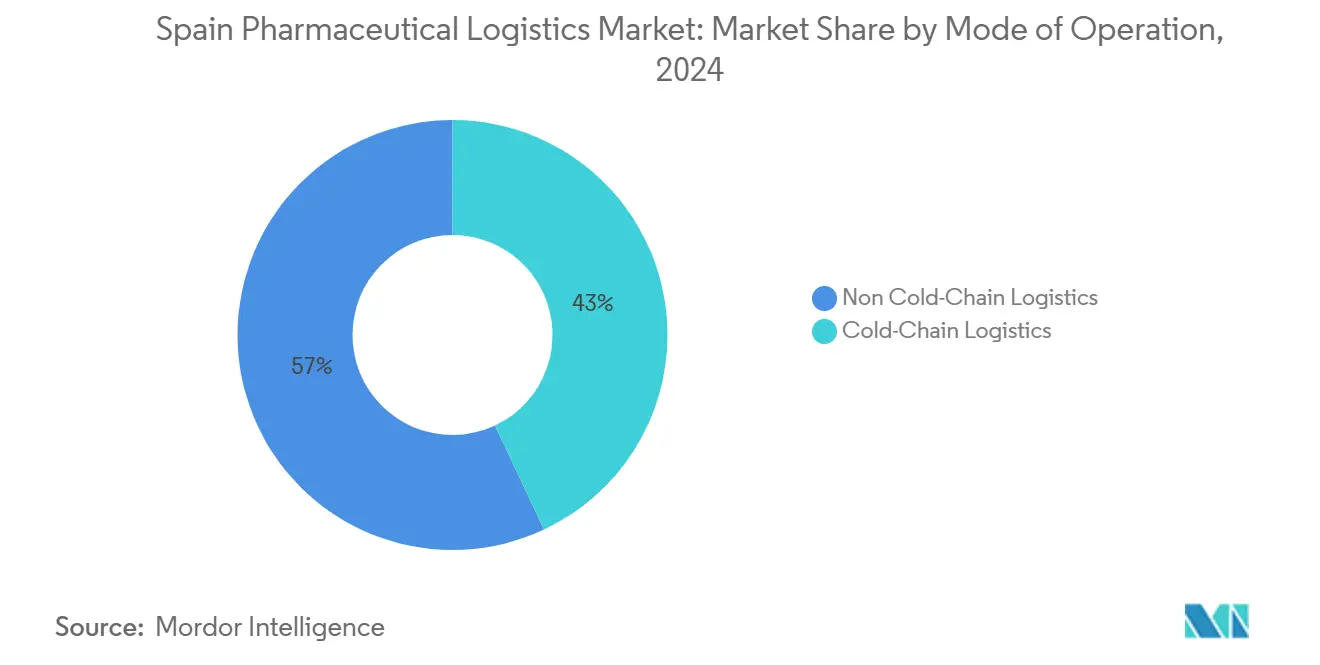

- By mode of operation, non-cold-chain logistics held 57% of the Spain pharmaceutical logistics market size in 2024, while cold-chain logistics is set to advance at a 5.1% CAGR through 2030.

- By product type, prescription drugs captured 23% of the Spain pharmaceutical logistics market share in 2024; cell & gene therapies is expected to post a 5.9% CAGR to 2030, outpacing all other categories.

Spain Pharmaceutical Logistics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising domestic pharmaceutical sales volume | +0.8% | Madrid, Barcelona, Valencia | Medium term (2-4 years) |

| Ageing population & chronic disease burden | +1.2% | Rural regions nationwide | Long term (≥ 4 years) |

| Expansion of biologics & temperature-sensitive therapies | +0.9% | Barcelona, Madrid | Medium term (2-4 years) |

| EU Falsified Medicines Directive enforcement | +0.6% | Nationwide | Short term (≤ 2 years) |

| RRF-backed cold-chain infrastructure | +0.7% | Industrial corridors | Medium term (2-4 years) |

| Hospital outsourcing of supply models | +0.5% | Public healthcare systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Domestic Pharmaceutical Sales Volume

Annual domestic drug revenue exceeds EUR 23 billion (USD 25 billion) and supports more than 260,000 jobs, which strengthens the baseline for logistics growth. Public health spending at EUR 134 billion (USD 143 billion) creates dependable demand across the Spanish pharmaceutical logistics market. Per-capita medicine outlays at EUR 477 (USD 510) surpass European averages, reinforcing volume stability. Yet drug shortages jumped 41% in 2024, with 4,983 items affected, exposing vulnerabilities in replenishment cycles. January 2024 recorded 947 unavailable products, underscoring the need for predictive inventory tools that reduce cascading care disruptions.

Ageing Population & Chronic Disease Burden Intensifying Last-Mile Demand

Long-term demographic projections show a sharply rising proportion of citizens older than 65 by 2074[2]Instituto Nacional de Estadística, “Population Projections 2024-2074,” ine.es. Chronic illnesses shift dispensing patterns toward repeat prescriptions delivered to patients’ homes, which magnifies last-mile complexity within Spain pharmaceutical logistics market. Digital health platforms integrate telemedicine with pharmacy networks and require timed deliveries of cardiovascular and diabetes drugs. Generic penetration led by Kern Pharma and Teva supports affordability but raises shipment frequency. Personalized oncology regimens from PharmaMar demand traceable, patient-specific cold-chain movements that extend beyond hospital pharmacies into home-care settings.

Expansion of Biologics & Temperature-Sensitive Therapies

Cell & gene therapies are the fastest-growing category at a 5.9% CAGR to 2030. ROVI recorded 141% sales growth for Okedi in 2024 and will begin global syringe manufacturing by 2026, cementing Spain as a high-value export base. Reusable thermal packaging is forecast to jump from 30% to 70% adoption in Europe, reflecting both sustainability targets and cost control. UPS Healthcare has earmarked USD 20 billion in revenue by 2026, much of it linked to expanded Spanish cold-chain capacity. Continuous temperature logging and lane-risk mapping tools are now standard procurement requirements for biologics shippers.

EU Falsified Medicines Directive Serialization Deadline Enforcement

Spain enforces fines up to EUR 1 million (USD 1.04 million) for non-compliance with serialization mandates, driving investments in tamper-evident packaging and barcode scanning[3]European Commission, “Criminal Involvement in Falsification of Medicines,” ec.europa.eu. The national regulator AEMPS launched the AI-powered MeQA engine in 2025 to streamline data queries, accelerating batch release processes[4]AEMPS, “La AEMPS lanza MeQA,” aemps.gob.es. EMA confirmed GDP certificates will no longer receive blanket extensions, so operators must pass full on-site audits in 2025. Enhanced oversight raises operating costs but also elevates service quality, strengthening market resilience.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver shortage & escalating labour costs | -0.9% | Industrial corridors | Short term (≤ 2 years) |

| Ensuring temperature integrity amid climate extremes | -0.5% | Southern regions | Medium term (2-4 years) |

| Fragmented cold-storage real-estate ownership | -0.4% | Major metropolitan areas | Long term (≥ 4 years) |

| Rising energy costs for refrigerated warehouses | -0.6% | Energy-intensive facilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Driver Shortage & Escalating Labour Costs

Cold-chain operators represent 2.5% of Iberian food GDP and face acute driver shortages that inflate wage bills. DHL answered with a EUR 2 billion (USD 2.08 billion) health-logistics program that prioritizes automation to counter labor gaps. UPS seeks to double healthcare revenue to USD 20 billion by 2026, banking on robotics and routing software to lift productivity. Despite capital injections, immediate driver scarcity restricts capacity during influenza vaccine peaks, restraining Spain pharmaceutical logistics market expansion.

Rising Energy Costs Impacting Refrigerated-Warehouse Margins

Energy inflation threatens refrigerated real estate margins as compressors and backup generators run longer during summer heatwaves. Cold-chain failures already cost the global drug industry USD 35 billion each year. Spanish operators deploy solar panels and phase-change materials to buffer surges, but capital payback extends beyond three years. Extreme weather delays shipments and forces higher safety inventories, eroding efficiency gains. Real-time energy dashboards and automated set-point controls are rapidly becoming competitive necessities.

Segment Analysis

By Service Type: Transportation Dominates Despite Value-Added Growth

Transportation captured 60% of Spain pharmaceutical logistics market share in 2024, propelled by 15,825 km of motorways connecting ports at Barcelona, Valencia, and Algeciras. This backbone delivers medicines to 200,000 European points of sale through networks managed by Logista and DHL. Road haulage remains the preferred mode for its overnight reach, but airfreight is scaling via Girona and Zaragoza airports to meet urgent biologic demand. Sea and rail corridors increasingly attract shippers pursuing carbon-reduction targets, with CEVA citing 70% lower emissions for refrigerated sea lanes. Value-added services & others are expected to post a 4.8% CAGR to 2030 as GDP documentation, kitting, and late-stage customization become standard contract inclusions. FedEx secured a CEIV Pharma Corporate Certificate in 2025 and won USD 400 million in healthcare contracts, illustrating the commercial payoff from compliance excellence.

Spain pharmaceutical logistics market size for value-added services & others is forecast to rise, aligned with expanding outsourcing by Spanish hospitals. The modal mix will tilt toward temperature-controlled containers that embed IoT sensors, creating data streams monetized through predictive lane validation services. UPS’s integration of Frigo-Trans and BPL widens its European 2-8 °C footprint and offers Spanish pharma exporters a single invoice solution spanning road, sea and air. Sustainability is another driver, with electric trucks now servicing inner-city clinics in Madrid under CEVA’s FORPLANET label, reducing emissions by 26,000 tons in 2024.

Note: Segment shares of all individual segments available upon report purchase

By Mode of Operation: Cold-Chain Acceleration Outpaces Traditional Logistics

Non-cold-chain flows still hold 57% of 2024 volumes, moving stable tablets and capsules that dominate primary-care prescriptions. However, cold-chain lanes expand at 5.1% CAGR because biologics launches require 2-8 °C or -80 °C transit windows, thus enlarging Spain pharmaceutical logistics market size in temperature-controlled subsegments. Spain’s three-phase vaccine cold-chain modernization elevated packaging standards and upgraded pharmacy refrigerators nationwide. Schmitz Cargobull’s purchase of Atlantis Global System embeds telematics into trailers, delivering continuous lane performance data to shippers.

Spain pharmaceutical logistics market share for cold-chain services is expected to climb by 2030 as therapy mixes shift. AI models such as SARIMA and Facebook Prophet improve capacity planning by 15% and reduce stockouts during flu seasons. Sensors integrated into reusable boxes feed blockchain ledgers to confirm temperature integrity on arrival. Integrators are piloting phase-change lockers for home delivery of insulin and oncology injectables, reflecting chronic-care decentralization trends.

By Product Type: Cell Therapies Drive Specialized Logistics Evolution

Prescription drugs remain the largest category with 23% of 2024 revenue. Yet cell & gene therapies hold the highest growth potential and will command a disproportionate share of logistics spending by 2030 because shipments must travel under dry-ice or liquid-nitrogen conditions. Clinical trial materials flow through Alliance Healthcare’s Barcelona hub, which manages more than 500 trials annually and offers just-in-time lab-kit assembly. Spain pharmaceutical logistics market size for clinical trial consignments is projected to grow 5% yearly, driven by rising oncology studies at Hospital Vall d’Hebron that use AI to cut medication errors, saving up to EUR 1.8 billion (USD 1.87 billion) in systemic costs.

Biologics and biosimilars gain momentum as patents expire. Vaccine and blood-product lanes already comply with GDP, but now add real-time CO₂ and vibration sensors to mitigate potency loss. The “others” bucket encompasses advanced therapeutics that need ultra-low temperature shippers and authenticated chain-of-custody portals. AEMPS audits force periodic recalibration of dataloggers and validate last-mile protocols, ensuring safe delivery to Spanish hospitals.

Geography Analysis

The Spain pharmaceutical logistics market is anchored by Madrid, Barcelona, and Valencia, cities that combine manufacturing clusters with multi-modal hubs. Madrid’s inland port consolidates cross-dock operations that reach 90% of the domestic population within 24 hours, boosting the city’s share of national pharma throughput. Barcelona supplies France and Italy through AP-7 and port container sailings, giving it a strategic export advantage. Valencia’s Sagunto terminal will gain EUR 28 million (USD 29.1 million) in EU funding to extend rail links, increasing refrigerated container capacity.

Northern regions like the Basque Country specialize in biosimilar production, which calls for expedited shipping to German buyers. Andalusia’s hotter climate necessitates redundant cooling layers during summer peak, raising operating costs but also stimulating innovation in passive packaging gels. The Canary and Balearic islands depend on airfreight replenishment cycles every 48 hours to avoid stockouts of chronic disease medicines, motivating carriers to invest in narrow-body aircraft with containerized holds. Overall, geographic diversification mitigates single-node risk and strengthens national resilience against weather or labor disruptions.

Competitive Landscape

Spain's pharmaceutical logistics industry competition intensifies as multinationals consolidate their share through acquisitions. DSV’s EUR 14.3 billion (USD 14.8 billion) purchase of Schenker adds 2,000 Spanish employees and broadens biologic handling capacity along the AP-2 corridor. DHL channels 25% of its EUR 2 billion (USD 2.08 billion) health-logistics budget into Iberian upgrades that include GDP-certified pharma hubs equipped with robotics picking arms. UPS integrates Frigo-Trans and BPL telemetry into its Spain control tower, providing real-time lane risk alerts that cut excursion rates by 20%.

Logista grew pharmaceutical distribution by 13.2% in H1 2025, validating scale advantages in domestic last-mile networks. CEVA’s FORPLANET fleet of 1,000 low-carbon vehicles meets tightening emission targets and appeals to ESG-focused pharma clients, helping CEVA secure multi-year vaccine contracts. White-space opportunities invite startups that marry AI planning with electric vans to reduce inner-city congestion. The European Investment Fund’s EUR 350 million (USD 364.5 million) commitment to Kembara Fund accelerates deep-tech solutions such as quantum-safe traceability and hydrogen-powered refrigerated trailers.

Barriers to entry rise with GDP and serialization enforcement. Established incumbents leverage end-to-end quality management systems and multi-temperature warehouses near Madrid and Valencia. Specialized niches are forming around cell-therapy cryogenic corridors and sustainable packaging pools, creating partnership models between carriers, box manufacturers and biotech producers. Overall, market concentration inches upward yet remains open for differentiated service innovators.

Spain Pharmaceutical Logistics Industry Leaders

-

DHL Supply Chain Spain

-

FedEx Express

-

Kuehne + Nagel S.A.

-

United Parcel Service (UPS)

-

C.H. Robinson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DHL Group pledged EUR 2 billion (USD 2.08 billion) by 2030 for global health-logistics upgrades, assigning 25% to EMEA sites, including Spain.

- March 2025: FedEx secured USD 400 million in new healthcare contracts to expand temperature-controlled capacity across Europe.

- January 2025: UPS Healthcare completed the acquisition of Frigo-Trans and BPL, bolstering European cold-chain reach.

- April 2024: CEVA Logistics opened an 18,000 m² GDP-ready facility in Tarragona, lifting its Iberian warehousing footprint above 600,000 m².

Spain Pharmaceutical Logistics Market Report Scope

Pharmaceutical logistics is concerned with the production, processing, and transportation of materials, as well as the resources and activities associated with the handling of manufactured items by their consumers. Logistics businesses are critical to the operation of any pharmaceutical company.

A comprehensive background analysis of the Spain Pharmaceutical Logistics Market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the competitive landscape of the industry. The impact of COVID-19 has also been incorporated and considered during the study.

Spain's pharmaceutical logistics market is segmented by product (generic drugs, branded drugs), by mode of operation (cold chain logistics, non-cold chain logistics), by application (bio-pharma, chemical pharma), and by mode of transport (air shipping, rail shipping, road shipping, sea shipping). The report offers market size and forecasts for the Spain Pharmaceutical Logistics market in value (usd billion) for all the above segments.

| Transportation | Road Freight |

| Air Freight | |

| Sea Freight | |

| Rail Freight | |

| Warehousing & Storage | |

| Value-added Services and Others |

| Cold-Chain Logistics |

| Non-Cold-Chain Logistics |

| Prescription Drugs |

| OTC Drugs |

| Biologics & Biosimilars |

| Vaccines & Blood Products |

| Clinical Trail Materials |

| Cell & Gene Therapies |

| Medical Devices & Diagnostics |

| Veterinary Medicine |

| Others |

| By Service Type | Transportation | Road Freight |

| Air Freight | ||

| Sea Freight | ||

| Rail Freight | ||

| Warehousing & Storage | ||

| Value-added Services and Others | ||

| By Mode of Operation | Cold-Chain Logistics | |

| Non-Cold-Chain Logistics | ||

| By Product Type | Prescription Drugs | |

| OTC Drugs | ||

| Biologics & Biosimilars | ||

| Vaccines & Blood Products | ||

| Clinical Trail Materials | ||

| Cell & Gene Therapies | ||

| Medical Devices & Diagnostics | ||

| Veterinary Medicine | ||

| Others |

Key Questions Answered in the Report

What is the 2025 value of Spain pharmaceutical logistics market?

The market is valued at USD 5.88 billion in 2025 with a projected 4.4% CAGR to 2030.

How fast will cold-chain services grow in Spain through 2030?

Cold-chain logistics is forecast to expand at 5.1% annually, significantly outpacing non-temperature-controlled services.

Which product segment shows the highest growth potential?

Cell & gene therapies will register a 5.9% CAGR, reflecting rising clinical adoption and stringent cryogenic requirements.

Which regions act as primary pharmaceutical gateways in Spain?

Madrid, Barcelona and Valencia host the largest hubs due to their motorway, port and rail connectivity.

What compliance trend shapes logistics investments in 2025?

Full enforcement of EU Falsified Medicines Directive serialization and stricter GDP audits drive upgrades in traceability and monitoring infrastructure.

How are providers addressing labor shortages in Spain?

Major logistics firms deploy automation, robotics and route-optimization software while investing in talent retention to mitigate driver scarcity.

Page last updated on: