Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 2.96 Billion |

| Market Size (2031) | USD 3.67 Billion |

| Growth Rate (2026 - 2031) | 4.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Over-the-counter (OTC) Drugs Market Analysis by Mordor Intelligence

The Spain Over-the-counter Drugs Market size is estimated at USD 2.96 billion in 2026, and is expected to reach USD 3.67 billion by 2031, at a CAGR of 4.43% during the forecast period (2026-2031).

Continued reimbursement cuts, faster Rx-to-OTC switches, and an aging population that self-medicates for minor ailments are widening the customer base while easing pressure on primary-care clinics.[1]Ministerio de Sanidad, “Sistema Nacional de Salud Annual Report 2025,” Ministerio de Sanidad, sanidad.gob.es Tablet formats still dominate volume but consumer willingness to pay more for gummies, sprays, and other convenient delivery systems is lifting average selling prices. The European Medicines Agency’s 2024 reclassification of pantoprazole and cetirizine expanded the number of non-prescription molecules on Spanish shelves, encouraging manufacturers to introduce dose-flexible packs priced below reimbursed prescription equivalents. Urban millennials fuel double-digit online growth while coastal tourism triggers seasonal spikes in analgesics, sunscreens, and rehydration salts.[2]Instituto Nacional de Estadística, “Population Figures at 1 January 2026,” Instituto Nacional de Estadística, ine.es Multinationals leverage global brand equity whereas Spanish incumbents rely on direct distribution to protect shelf space and margins.

Key Report Takeaways

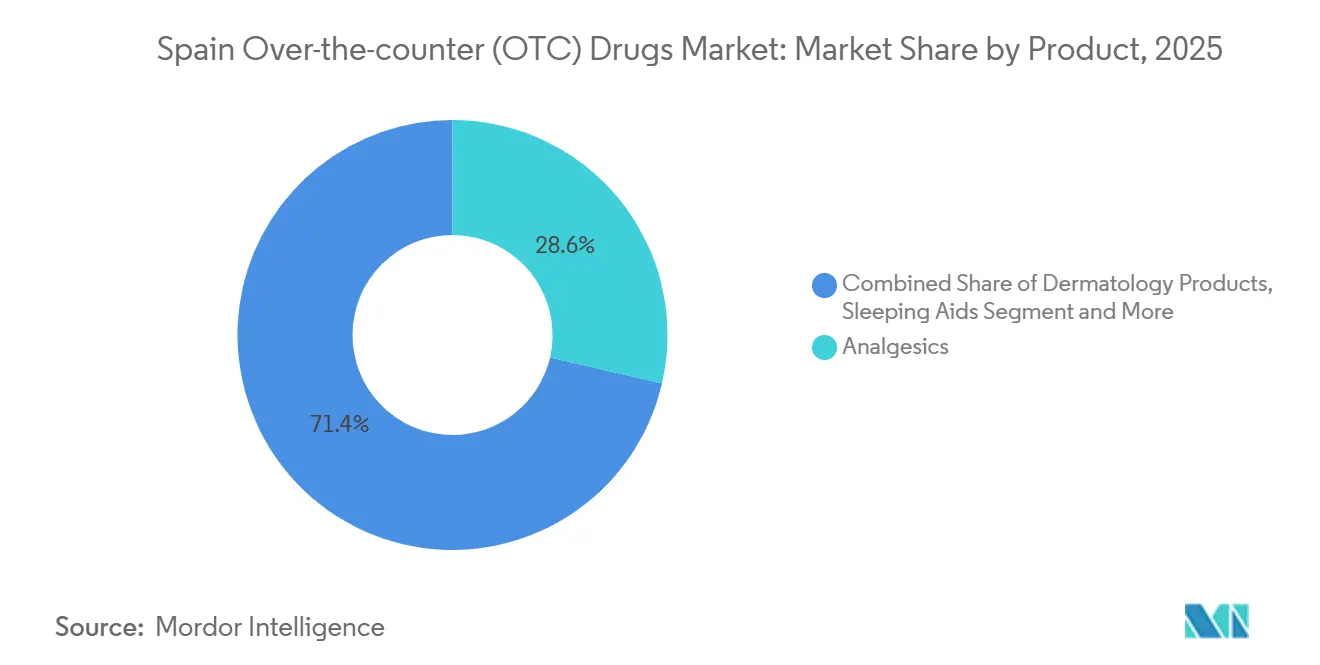

- By product category, analgesics led with 28.62% of Spain over the counter (otc) drugs market share in 2025; sleep aids are forecast to expand at a 7.36% CAGR through 2031.

- By dosage form, tablets and capsules accounted for 41.57% of the Spain over the counter (otc) drugs market size in 2025, while gummies, sprays, and drops are projected to grow at 7.55% CAGR to 2031.

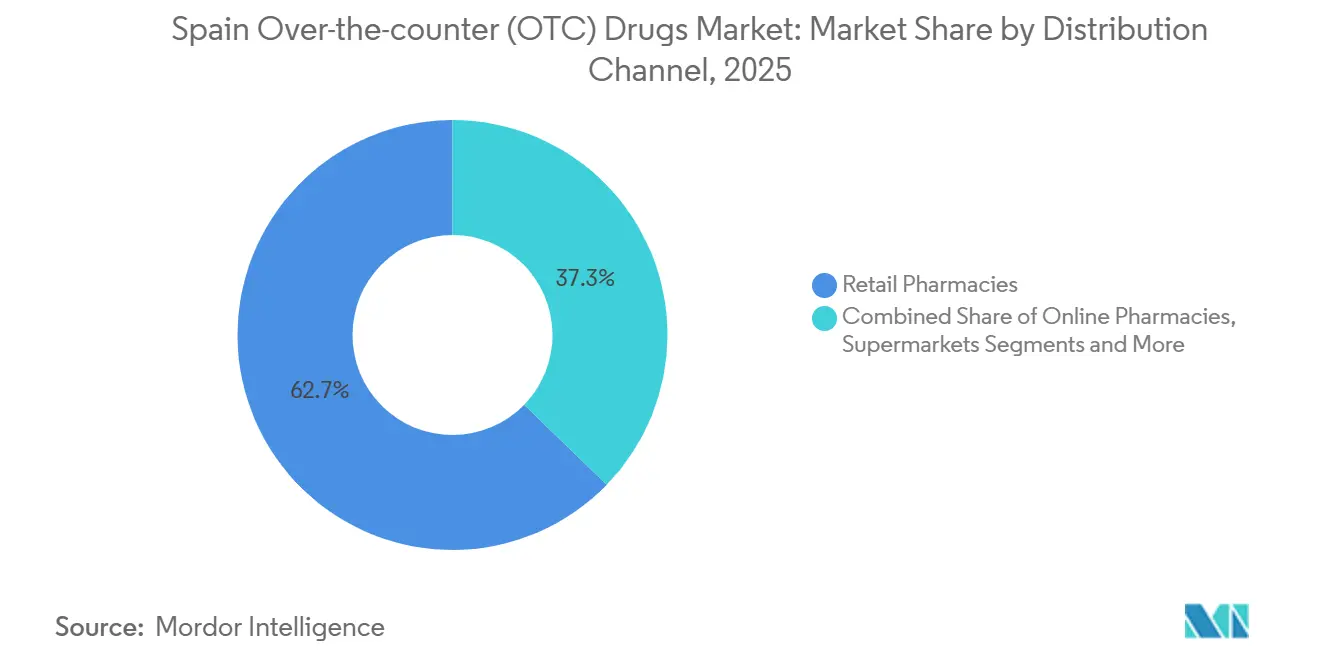

- By distribution channel, retail pharmacies captured 62.73% revenue in 2025, whereas online pharmacies record the highest projected 8.62% CAGR through 2031.

- By consumer demographic, adults held 57.92% of consumption in 2025, yet the geriatric cohort is advancing at an 8.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Over-the-counter (OTC) Drugs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rx-to-OTC switches accelerating post-EU reclassification | +0.9% | National, early uptake in Catalonia and Madrid | Medium term (2–4 years) |

| Growing preference for self-care among aging population | +1.2% | National, concentrated in Galicia, Asturias, Castile and León | Long term (≥4 years) |

| Expansion of e-pharmacy and click-and-collect models | +0.8% | National, led by Madrid, Barcelona, Valencia | Short term (≤2 years) |

| High tourism inflow boosting point-of-sale volumes | +0.6% | Balearic Islands, Canary Islands, Costa del Sol, Costa Brava | Short term (≤2 years) |

| Regional reimbursement cuts driving OTC uptake | +0.7% | National, most pronounced in Andalusia, Valencian Community, Murcia | Medium term (2–4 years) |

| Emerging CBD-based OTC remedies | +0.3% | National, pilot adoption in Catalonia and Basque Country | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rx-to-OTC Switches Accelerating Post-EU Reclassification

The European regulator downgraded pantoprazole 20 mg and cetirizine 10 mg in 2024, and AEMPS mirrored the decision within three months, allowing pharmacies nationwide to dispense both molecules without prescriptions. Manufacturers quickly introduced lower-dose packs priced 20–30% below prescription equivalents, helping price-sensitive patients who previously delayed treatment. Cinfa’s 14-tablet pantoprazole pack at EUR 6.50 (USD 7.10) undercut a leading multinational rival by EUR 3.00. General-practitioner visits for minor gastric complaints fell 8% in 2025, freeing capacity for chronic-disease management. The policy therefore expands access, lowers out-of-pocket costs, and reduces strain on the public health system, jointly lifting the Spain over the counter (otc) drugs market.

Growing Preference for Self-Care Among Aging Population

Spain counted 9.8 million residents aged 65 and above in 2025, equal to 20.8% of all citizens, and demographic forecasts suggest the share will reach 25% by 2030. Retirees favor familiar brands, consult pharmacists about drug–drug interactions, and self-fund vitamins and minerals excluded from public reimbursement, sustaining steady demand for analgesics, laxatives, and vitamin D. Faes Farma’s Fisiogen cognitive-health line grew sales 18% in 2025 on the back of targeted newspaper ads and pharmacy loyalty programs. WHO guidelines published in 2024 encourage older adults to manage minor ailments themselves, reinforcing the strategic pivot toward geriatric-focused portfolios. As these consumers purchase repeatedly for chronic conditions, they underpin the Spain over the counter (otc) drugs market’s long-run volume growth.

Expansion of E-Pharmacy and Click-and-Collect Models

An amended Royal Decree in 2024 permits licensed pharmacies to sell non-prescription medicines online once they register with AEMPS and display the EU common logo. Online channels captured 8.2% of OTC revenue in 2025, up from 5.1% two years prior, with click-and-collect accounting for 60% of digital orders. PromoFarma reported 1.2 million active users and an average basket value of EUR 35 (USD 38) in 2025. Digital ads face fewer creative constraints than prescription categories, so brands deploy price-comparison engines and targeted coupons to acquire new customers. The convenience premium appeals most to 18–40-year-olds in urban centers, cementing the Spain over the counter (otc) drugs market’s fastest-growing channel.

High Tourism Inflow Boosting Point-of-Sale Volumes

Spain welcomed 85 million visitors in 2024, restoring arrivals to above pre-pandemic levels and injecting EUR 110 billion (USD 120 billion) into the economy.[3]United Nations World Tourism Organization, “Tourism Recovery Dashboard 2025,” United Nations World Tourism Organization, unwto.org Coastal pharmacies report that tourists contribute up to 20% of July-August OTC turnover, predominantly on premium-priced analgesics, sunscreens, and rehydration salts. These sales lift per-unit margins because international travelers prefer branded products they recognize from home markets. Pharmacies stock multilingual packaging and hire English-speaking staff to minimize misuse risk. Nonetheless, the seasonality forces outlets in Ibiza and Málaga to build inventories six months early, tying up working capital yet providing an important revenue cushion for the Spain over the counter (otc) drugs market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk of misdiagnosis and delayed professional care | –0.4% | National, higher incidence in rural areas | Medium term (2–4 years) |

| Rising substance-abuse flags for codeine combinations | –0.3% | National, concentrated in Madrid, Barcelona, Seville | Short term (≤2 years) |

| Stringent Spanish advertising code CAP 2024 | –0.2% | National | Short term (≤2 years) |

| Price-containment pacts with regional health authorities | –0.3% | Catalonia, Basque Country, Navarra | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Risk of Misdiagnosis and Delayed Professional Care

Ready OTC access can mask serious conditions and postpone specialist consultations. A 2024 study tracking 1,200 self-medicating heartburn patients found that 9% later received diagnoses of Barrett’s esophagus or early gastric cancer after delaying endoscopy eight months on average. Chronic headache sufferers who rely on analgesics risk overlooking hypertension or intracranial lesions. Although AEMPS mandates on-pack warnings to seek medical advice if symptoms persist beyond 10 days, compliance audits in 2025 showed that 30% of consumers ignore the guidance. Some chains deploy digital triage tools that flag red-flag symptoms, yet adoption outside large cities remains limited. The resulting disease-progression costs temper the positive trajectory of the Spain over the counter (otc) drugs market.

Rising Substance-Abuse Flags for Codeine Combinations

Emergency-room visits linked to codeine overdose rose 12% year on year to 4,800 in 2024, with adolescents and young adults representing 40% of incidents. AEMPS introduced sales-log requirements and single-pack limits in mid-2025 to curb misuse, yet stakeholders fear a shift to illicit channels. The EMA’s pharmacovigilance committee is reviewing codeine safety, and a move to prescription-only status would erase about EUR 25 million (USD 27 million) from OTC shelves. While public-health benefits are clear, revenue contraction and tighter pharmacist workload may restrain near-term growth in the Spain over the counter (otc) drugs market.

Segment Analysis

By Product: Sleep Aids Outpace Traditional Categories

Analgesics generated 28.62% of revenue in 2025, but sleep aids are forecast to record a 7.36% CAGR to 2031, the quickest of any category. The Spain over the counter (otc) drugs market size for sleep aids is expected to expand as digital-device exposure prolongs wakefulness among urban professionals. Melatonin gummies and valerian capsules resonate with consumers seeking drug-free solutions, and EFSA’s 2024 approval of a health claim stating that 1 mg melatonin reduces sleep-onset latency legitimizes marketing. Spanish players launched affordable gummy lines priced below EUR 10 per monthly supply, while multinationals promote premium herbal blends with sustained-release technology.

Growing consumer interest in preventive health also lifts vitamins, minerals, and supplements, while dermatology products benefit from high UV exposure in coastal regions. Cough, cold, and flu remedies remain a seasonal staple, reinforced by lingering COVID-19 circulation. Gastrointestinal products serve both aging residents managing chronic reflux and tourists adjusting to new cuisines. Weight-control and ophthalmic segments retain niche status because advertising rules restrict bold efficacy claims, yet they round out pharmacy assortments, ensuring comprehensive choice within the Spain over the counter (otc) drugs market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Dosage Form: Gummies and Sprays Gain Traction

Tablets and capsules still accounted for 41.57% of value in 2025, but novel forms are eroding share. Gummies, sprays, and drops are projected to climb 7.55% CAGR, thanks to palatability, perceived naturalness, and on-the-go convenience. Consumers accept a 30–40% price premium per dose, which lifts category profitability. For example, Bayer’s vitamin C oral spray targets commuters who want quick immune support without water.

Liquids and syrups remain critical in pediatrics, yet sachets and chewables are winning over parents who prefer spill-proof administration. Topical creams and transdermal patches see steady demand for dermatology and localized pain relief. Powders and granules hold a niche for rehydration salts and fiber supplements. The dosage-form shift reflects broader expectations that OTC remedies integrate seamlessly into daily routines, reinforcing growth prospects for the Spain over the counter (otc) drugs market.

By Distribution Channel: Online Pharmacies Surge

Retail pharmacies commanded 62.73% of sales in 2025 due to Spain’s dense network of 22,000 outlets and the advisory role of pharmacists. However, online players are forecast to post an 8.62% CAGR, the steepest among channels, supported by the 2024 clarification of e-pharmacy rules. The Spain over the counter (otc) drugs market size for online sales climbs as urban millennials prioritize price transparency and 24-hour delivery. Click-and-collect mitigates cold-chain risks and allows face-to-face counseling at pickup.

Supermarkets and hypermarkets remain barred from carrying pharmacist-supervised medicines, limiting their share to vitamins and first-aid supplies. Drug-parapharmacy chains broaden assortments with cosmetics and wellness items, capturing convenience shoppers. Secondary channels such as vending machines and gas stations fill emergency needs but contribute minimal volume. As digital literacy spreads across age groups, hybrid omnichannel models will shape the Spain over the counter (otc) drugs market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Consumer Demographic: Geriatric Segment Accelerates

Adults aged 19–59 represented 57.92% of volume in 2025, yet the geriatric cohort is set to grow at 8.01% CAGR through 2031. This acceleration stems from Spain’s median age of 45 years and a forecast leap to 25% seniors by 2030. Seniors buy OTC products to manage arthritis pain, constipation, and osteoporosis, and they purchase vitamins that public insurance does not cover. The Spain over the counter (otc) drugs market size for geriatric consumers benefits from multibrand loyalty programs that bundle blood-pressure checks and medication reviews.

Faes Farma distributes cognitive-health sachets via senior centers, generating strong word-of-mouth endorsements. Younger adults experiment with novel flavors and delivery forms, driving gummies and effervescent tablets. Pediatrics lags due to Spain’s low birth rate of 7.9 per 1,000 in 2024, prompting brands to reposition children’s products for family use. Altogether, demographic nuances guide portfolio decisions across the Spain over the counter (otc) drugs market.

Geography Analysis

Spain’s internal diversity creates regional demand clusters that shape strategy. Catalonia and Madrid, representing 30% of the population, accounted for an outsized share of value in 2025, buoyed by higher disposable incomes, dense pharmacy networks, and robust e-commerce penetration. Barcelona alone hosted 800 pharmacies for 1.6 million residents, ensuring five-minute walk-in access for most citizens. Online purchases reached 12% of Catalonia’s OTC volume, twice the national average, even though price-ceiling agreements trim branded margins. The Spain over the counter (otc) drugs market captures incremental volume here through premium-format launches and digital loyalty schemes.

Andalusia, the most populous community, displays a dual profile. Coastal provinces such as Málaga and Cádiz experience summer demand spikes 40% above average due to tourist inflows, while inland areas favor low-priced generics. Andalusia’s 2024 formulary cuts shifted EUR 60 million (USD 65 million) of products to out-of-pocket purchases, buoying local OTC sales despite lower per-capita incomes. The Valencian Community and Galicia follow national patterns but skew toward geriatric consumption because their median ages exceed the Spanish average.

Island regions punch above their demographic weight. The Balearic Islands sold an estimated EUR 40 million (USD 43 million) in OTC products to 14 million visitors in 2024, focusing on sunburn relief and anti-diarrheal tablets. Pharmacies stock multilingual leaflets and employ seasonal staff fluent in English and German. The Basque Country and Navarra exhibit the highest per-capita OTC spending at EUR 68 (USD 74) in 2025, propelled by higher incomes and proactive health cultures. Although price-containment pacts cap yearly increases, consumers continue to trade up to sustained-release and effervescent formats, supporting value growth within the Spain over the counter (otc) drugs market.

Competitive Landscape

The top five multinationals, GSK, Bayer, Sanofi, Reckitt Benckiser, and Johnson & Johnson—held roughly half of revenue in 2025, while Spanish incumbents Cinfa, Almirall, Faes Farma, and Esteve together captured another 25%. The remaining 30% remains fragmented among regional brands and private-label suppliers, giving the Spain over the counter (otc) drugs market a moderately concentrated structure. Multinationals rely on global R&D pipelines and marketing clout to sustain premium prices for legacy brands such as Nurofen, Voltaren, and Doliprane.

Domestic players counter with vertical integration. Cinfa manufactures in Navarra and delivers directly to 22,000 pharmacies, slashing logistics costs and enabling rapid replenishment during flu season. Faes Farma exploits niche categories such as cognitive health and women’s wellness, where branded clinical data differentiates from generics. Almirall filed a European patent in 2024 for a transdermal patch combining CBD and lidocaine, signaling intent to pioneer cannabinoid-based analgesia once regulatory barriers fall.

Strategic patterns include portfolio premiumization—shifting customers from generic ibuprofen to fast-acting gel capsules—and omnichannel rollout, with direct-to-consumer sites that bypass pharmacy margins. Perrigo and STADA grow by supplying pharmacy private-labels, siphoning price-sensitive buyers. Only 15% of outlets used AI inventory tools in 2025, leaving efficiency gains on the table. Mergers remain rare as family-owned pharmacies retain ownership restrictions, but supply-side collaborations to co-manufacture gummies and sprays illustrate incremental consolidation within the Spain over the counter (otc) drugs market.

Spain Over-the-counter (OTC) Drugs Industry Leaders

Sanofi SA

GlaxoSmithKline PLC

Bayer

Reckitt Benckiser Group PLC

P&G Health

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Cooper Consumer Health reported the successful Spain-wide launch of Nicotinell nicotine-replacement therapy through its multi-country omnichannel platform.

- November 2025: Karo Healthcare entered an exclusive license with Moberg Pharma to commercialize MOB-015, an antifungal under the Lamisil brand, across Europe including Spain.

Spain Over-the-counter (OTC) Drugs Market Report Scope

Over-the-counter (OTC) medications do not need a doctor's prescription. This convenience for consumers enables the direct purchase of medicines.

The Spain Over-the-Counter (OTC) drugs market is segmented by product, dosage form, distribution channel and consumer demographics. By Product, the market is segmented into Cough, Cold & Flu, Analgesics, Dermatology, Gastrointestinal, VMS, Weight-loss, Ophthalmic, Sleep Aids, Others. By Dosage Form, market is segmented by Tablets & Capsules, Liquids & Syrups, Topicals, Powders & Granules, Others. By Distribution Channel, market is segmented by Retail Pharmacies, Online Pharmacies, Supermarkets, Drug-Parapharmacy Chains, Others. By Consumer Demographic, market is segmented by Adults, Geriatric, Pediatric.The report offers the value (in USD million) for the above segments.

By Product

| Cough, Cold & Flu Products |

| Analgesics |

| Dermatology Products |

| Gastrointestinal Products |

| Vitamin, Mineral & Supplements (VMS) |

| Weight-loss/Dietary Products |

| Ophthalmic Products |

| Sleep Aids |

| Other Product Types |

By Dosage Form

| Tablets & Capsules |

| Liquids & Syrups |

| Topicals (Creams/Ointments/Patches) |

| Powders & Granules |

| Others (Sprays, Drops, Gummies) |

By Distribution Channel

| Retail Pharmacies |

| Online Pharmacies |

| Supermarkets/Hypermarkets |

| Drug-Parapharmacy Chains |

| Other Channels (Gas stations, Vending) |

By Consumer Demographic

| Adults (19–59 yrs) |

| Geriatric (≥60 yrs) |

| Pediatric (0–18 yrs) |

| By Product | Cough, Cold & Flu Products |

| Analgesics | |

| Dermatology Products | |

| Gastrointestinal Products | |

| Vitamin, Mineral & Supplements (VMS) | |

| Weight-loss/Dietary Products | |

| Ophthalmic Products | |

| Sleep Aids | |

| Other Product Types | |

| By Dosage Form | Tablets & Capsules |

| Liquids & Syrups | |

| Topicals (Creams/Ointments/Patches) | |

| Powders & Granules | |

| Others (Sprays, Drops, Gummies) | |

| By Distribution Channel | Retail Pharmacies |

| Online Pharmacies | |

| Supermarkets/Hypermarkets | |

| Drug-Parapharmacy Chains | |

| Other Channels (Gas stations, Vending) | |

| By Consumer Demographic | Adults (19–59 yrs) |

| Geriatric (≥60 yrs) | |

| Pediatric (0–18 yrs) |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Spain over the counter (otc) drugs market in 2026?

It was valued at USD 2.96 billion in 2026 and is on track to reach USD 3.67 billion by 2031.

Which product category is expanding the fastest?

Sleep aids lead with a projected 7.36% CAGR through 2031, driven by melatonin gummies and herbal blends.

What channel is gaining share most quickly?

Online pharmacies, supported by click-and-collect and 24-hour delivery, are forecast to post an 8.62% CAGR.

Why are Rx-to-OTC switches important for growth?

Reclassification of molecules such as pantoprazole immediately broadens self-medication options and reduces GP visits.

How do regional price caps affect manufacturers?

Caps squeeze margins in Catalonia, the Basque Country, and Navarra, prompting firms to favor premium formats outside control.

What is the main demographic driver?

Spain’s aging population—set to reach 25% seniors by 2030—is boosting demand for analgesics, vitamins, and laxatives.