Market Trends of Spain Office Real Estate Industry

Madrid's Growing Demand for Premium and Flexible Office Spaces

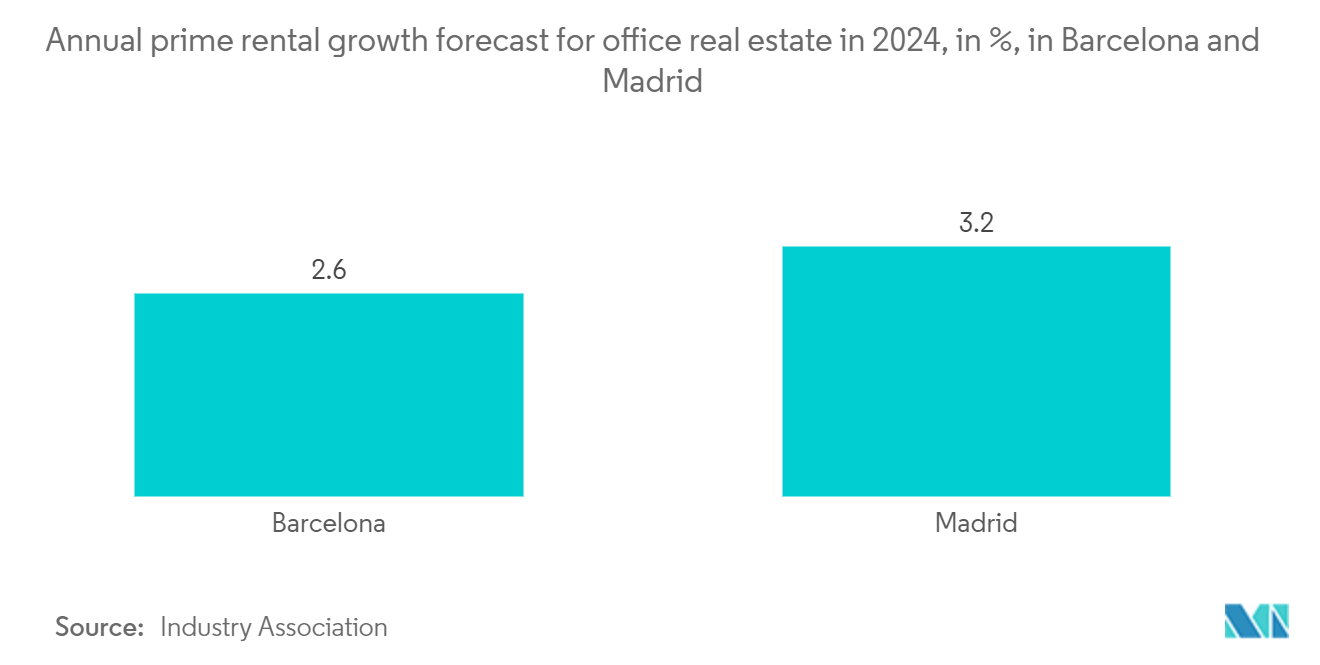

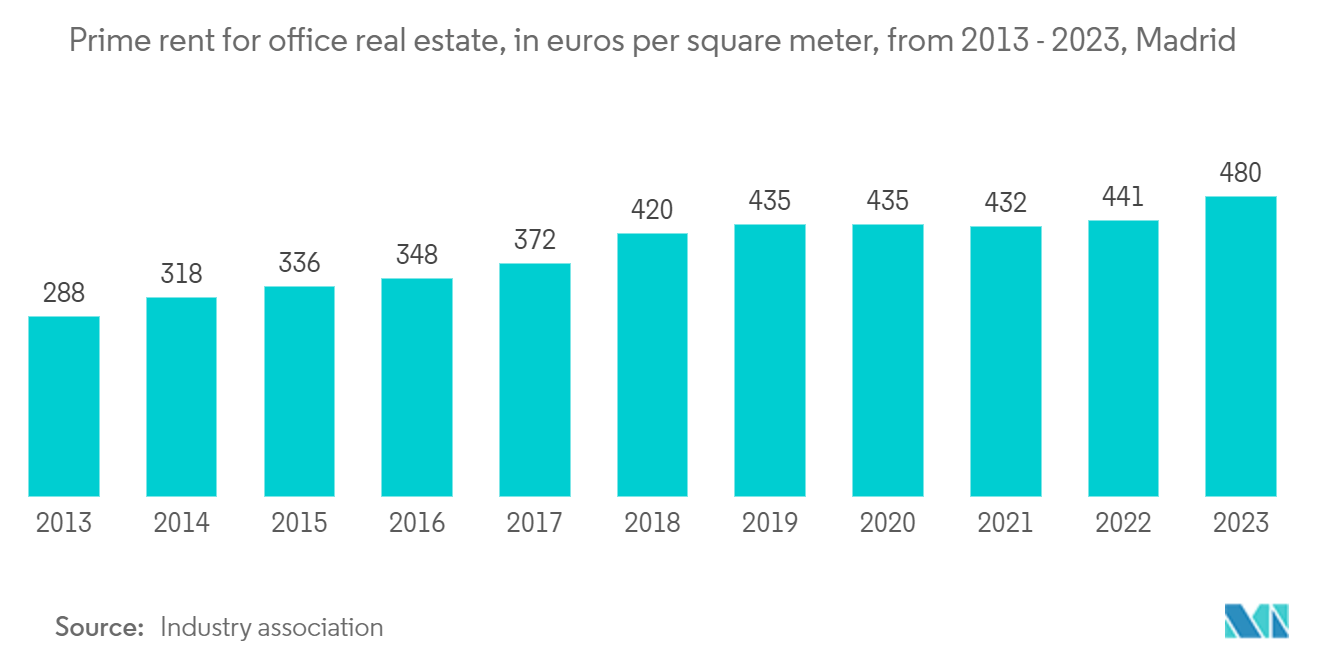

Madrid's office real estate market is witnessing robust demand for premium spaces, driving a consistent uptick in prime rent levels. This rent surge is particularly pronounced in the city's central business districts (CBD), where vacancies are scarce and businesses are gravitating towards contemporary, adaptable office solutions. For instance, in Q1 2024, prime rents in Madrid's CBD surged, fueled by a tight supply and fierce competition for top-tier spaces. A February 2024 report highlighted that, despite overarching market uncertainties, corporate tenants' strong demand propelled prime rent levels in Madrid's CBD.

Another notable trend in Madrid's office landscape is the rising allure of refurbished spaces. These revamped offices are fetching premium rents as companies prioritize modern amenities and versatile layouts. A testament to this trend is Johnson & Johnson's recent lease of nearly 9,000 sq m in Pozuelo de Alarcón, a coveted office hotspot. This deal, spotlighted in early 2024's market roundup, underscores the escalating appetite for top-tier office spaces in prime, accessible locales, mirroring the broader shift towards flexible, high-end environments.

Moreover, the proliferation of flexible office spaces is significantly influencing the rise in prime rents across Madrid. Operators such as Loom and Regus are clinching substantial leases in prime spots like the Ruiz Picasso Building and Castellana 86. A Q1 2024 industry report noted that these adaptable spaces are reshaping the office landscape, with businesses increasingly leaning towards solutions that support hybrid work models. Coupled with the demand for modern features, this trend is poised to keep prime rents on an upward trajectory throughout 2024.

Demand for Premium Office Locations in Central Hubs

In Spain, the demand for premium office locations in central business districts remains strong as companies emphasize accessibility and high-quality work environments. Major cities, particularly Madrid and Barcelona, continue to attract significant interest in premium office spaces, especially in areas offering prestigious addresses and proximity to key business hubs.

A key driver of this demand is the ongoing revitalization of central business districts. In Madrid, the Azca area, a historically prominent location, is undergoing extensive redevelopment, drawing top-tier corporations such as Deloitte and Google. Notable projects like Castellana 69 are introducing cutting-edge office spaces designed with sustainability and modern amenities in mind, catering to the evolving needs of businesses. Similarly, in Barcelona, the 22@ district has become a focal point for demand, driven by the presence of international firms and a concentration of innovative industries, further solidifying its reputation as a hub for business activity.

In addition to established commercial districts, new developments in Madrid’s financial landscape, such as the Madrid Nuevo Norte project, are expected to significantly enhance the city’s appeal to international investors. This ambitious project is set to deliver over 1.6 million square meters of commercial real estate, positioning Madrid as a strategic destination for multinational corporations seeking premium office locations. The initiative forms part of a broader urban transformation strategy aimed at providing modern, high-quality office spaces and reinforcing Madrid’s status as a global business hub.

Although hybrid work models have influenced overall office demand, businesses aiming to maintain a prestigious presence continue to gravitate toward prime office locations. Across Spain, companies are consolidating their operations in premium areas, balancing flexibility with the need for strategic locations and superior quality. This trend highlights the enduring importance of central business hubs in shaping office space decisions in 2024, as businesses prioritize accessibility, reputation, and operational efficiency.