| Study Period | 2017 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 166.8 Billion |

| Market Size (2030) | USD 273.4 Billion |

| CAGR (2025 - 2030) | 10.39 % |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Spain Foodservice Market Analysis

The Spain Foodservice Market size is estimated at 166.8 billion USD in 2025, and is expected to reach 273.4 billion USD by 2030, growing at a CAGR of 10.39% during the forecast period (2025-2030).

Spain's foodservice industry is experiencing robust growth, driven largely by the revival of international tourism and evolving consumer preferences. In 2022, Spain welcomed 30.2 million international tourists, significantly impacting the foodservice sector's recovery and expansion. The country's rich culinary heritage, combined with its position as a major tourist destination, has led to a diverse restaurant market that caters to both domestic and international palates. This is particularly evident in the increasing popularity of Asian cuisine, with Japan alone contributing 1.49 million tourists in 2022, followed by significant visitors from the Philippines and South Korea at 431,628 each, driving demand for authentic Asian dining experiences.

The Spanish foodservice infrastructure has shown remarkable resilience and adaptation, with 277,539 bar establishments contributing approximately 15% to the country's GDP in 2022. The market is characterized by a mix of traditional and modern formats, with establishments ranging from traditional tapas bars to contemporary dining concepts. The presence of 530 shopping malls across Spain in 2022 has created additional opportunities for foodservice operators, particularly in urban areas where foot traffic is high and consumer spending is concentrated. This retail infrastructure has become a crucial component of the food industry in Spain, providing operators with prime locations to reach their target customers.

Consumer behavior in Spain continues to evolve, with a strong emphasis on coffee culture and social dining experiences. According to recent data, 87% of the Spanish population aged between 18 and 64 drinks coffee daily in 2022, making cafes and coffee shops integral to the country's foodservice landscape. The market has also witnessed a significant shift in dining preferences, with consumers showing increased interest in both traditional Spanish cuisine and international flavors. This has led to the emergence of diverse dining concepts that blend local traditions with global culinary trends, creating unique value propositions for consumers.

The industry is undergoing a digital transformation, particularly in urban areas, with the emergence of new business models and service formats. The presence of 214 cloud kitchens in 2022 demonstrates the market's adaptation to changing consumer preferences and technological advancement. These virtual kitchens are revolutionizing the delivery segment by offering cost-effective solutions for operators while meeting the growing demand for convenient dining options. The integration of digital ordering systems, mobile applications, and delivery platforms has become crucial for success in the market, as operators strive to enhance customer experience and operational efficiency. This digital shift is a significant aspect of the overview of the food industry in Spain.

Spain Foodservice Market Trends

The number of cafes and bars in Spain is growing tremendously, driven by the demand for alcohol and gourmet coffee

- The number of cafes and bars in Spain experienced a YoY growth rate of 12.94% from 2020 to 2022. The Spanish population tends to invest more in alcoholic beverages, leading to frequent visits to bars. In 2021, the per capita expenditure in alcoholic beer was USD 27.49. The growing affinity for gourmet coffee has also prompted operators to expand their coffee chains in major cities.

- From 2020 to 2022, cloud kitchen outlets emerged as the fastest-growing segment. They are projected to register a notable CAGR of 9.43% during the forecast period. The effects of the pandemic have resulted in a surge in online food ordering, with a significant portion of the population in Spain, around 42%, spending money on ordering food through delivery services. As a result, many foodservice companies have begun creating virtual kitchens, intensifying competition in the cloud kitchen market.

- The number of quick service restaurants is also growing in response to consumer preferences for fast-food options such as pizza, hamburgers, sandwiches, and chicken-based snacks. In 2021, 23% of the population in Spain reported visiting different fast-food restaurants. Most quick service restaurants offer a limited menu selection that can be delivered quickly. The leading quick service restaurant chains in Spain with the highest number of stores include Telepizza, McDonald's, Pizza Hut, and Burger King. As of 2022, there were over 714 Telepizza outlets, 569 McDonald's, 765 Pizza Hut, and approximately 650 Burger King outlets. Consequently, the quick service restaurant outlets in Spain are expected to register a CAGR of 5.77% during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

Asian cuisine gains popularity in Spain, driven by Indian, Japanese, and Thai cuisines

- The food industry in Spain has undergone significant changes to cater to customer demand and evolving consumer behavior. Quick service restaurants (QSRs) are experiencing growth in the country, particularly those offering non-traditional fast-food options such as Asian or Mexican cuisine. The growth of pizzerias can be attributed to new store openings and higher revenues per outlet as customers opt for more exotic varieties. Spanish consumers are seeking a touch of innovation and exoticism alongside convenience and speed. In 2022, the average prices for burgers, nachos, and pizza were USD 9.5, USD 11.5, and USD 10.8 per serving, respectively.

- The average order value for the cloud kitchen grew by 8.83% in 2022 compared to the previous year. The expansion of the cloud kitchen segment is being driven by an increase in the demand for online meal delivery. Consumers in Spain spend an average of around USD 24 on online food delivery per order. Online meal ordering and delivery services grew in popularity after the pandemic. Popular online delivery apps are Glovo, Uber Eats, Just Eat, and Deliveroo. Popular dishes offered by cloud kitchens in Spain were burgers, pizza, Pollo Mantequilla, and Indian curries priced at USD 9.5, USD 10.8, USD 13.5, and USD 12, respectively, per serving, in 2022. Asian cuisine holds a significant market share in Spain, with Indian, Japanese, and Thai cuisines being the most popular. Indian cuisine, in particular, is characterized by the Northern Indian approach, featuring flavorful curries and bread. The Indian population in Spain was approximately 70,000 as of 2021, leading to a wide range of full-service restaurants (FSRs) offering Indian cuisine. The prices of Indian curries and Chana Masala were around USD 12.2 and USD 8.9 per 300 g, respectively, in 2022.

Segment Analysis: Foodservice Type

Cafes & Bars Segment in Spain Foodservice Market

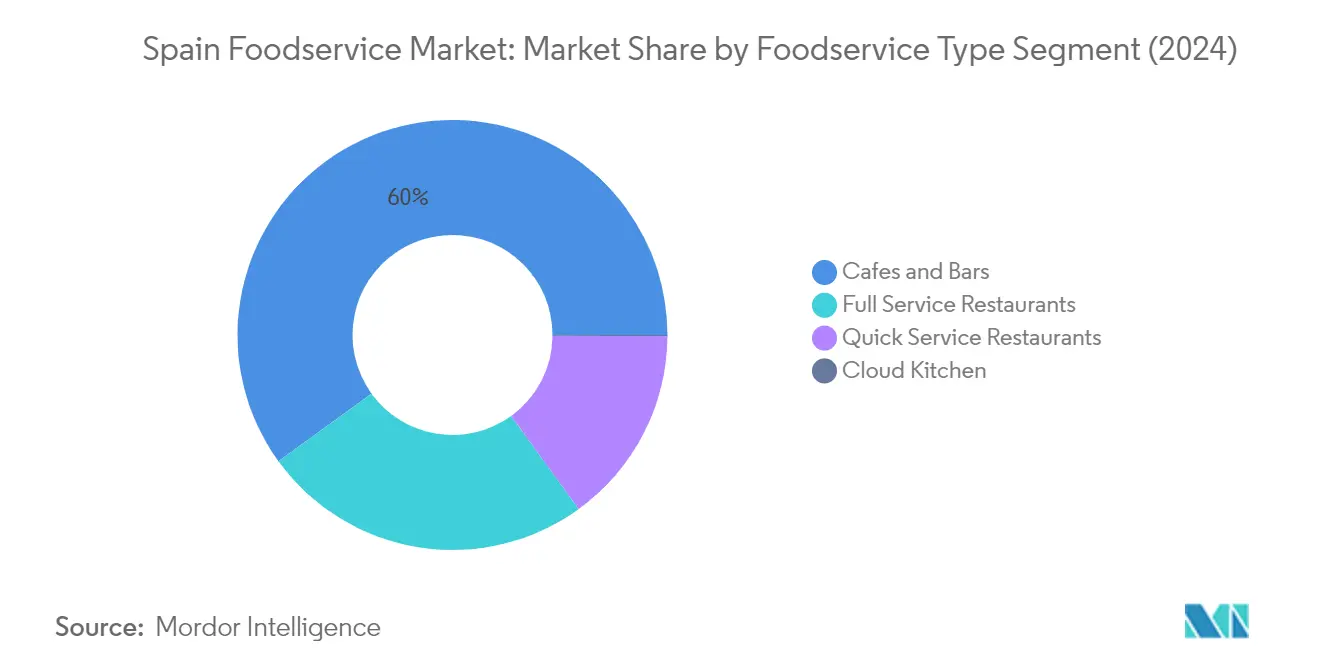

The cafes and bars segment maintains its dominant position in the Spanish food services market, commanding approximately 60% market share in 2024. This substantial market presence can be attributed to Spain's deeply rooted coffee culture and vibrant nightlife scene. The segment's strength is particularly evident in major cities like Madrid, Barcelona, and Valencia, where both international chains and local establishments thrive. The high market share reflects Spanish consumers' strong preference for social dining and drinking experiences, with cafes serving as popular meeting spots for business and leisure. Independent cafes continue to lead the segment, offering aesthetically pleasing environments and diverse regional food and beverage choices that appeal to urban dwellers. The segment's success is further bolstered by Spain's significant tourist influx, who frequently visit local cafes and bars to experience authentic Spanish culture.

Cloud Kitchen Segment in Spain Foodservice Market

The cloud kitchen segment is emerging as the most dynamic sector in the Spanish foodservice market size, projected to grow at approximately 15% annually from 2024 to 2029. This remarkable growth trajectory is driven by increasing internet penetration and the proliferation of food delivery applications across Spain. The segment's expansion is supported by significant venture capital and private equity funding, enabling cloud kitchen companies to scale their operations nationwide. Digital marketing strategies, including social media marketing and in-app offers, play a crucial role in driving customer acquisition. The segment's growth is further accelerated by changing consumer preferences towards convenient dining options and the rising adoption of online food ordering platforms. Cloud kitchens are particularly attractive to entrepreneurs due to their lower overhead costs, high expansion opportunities, and technological advantages in meeting evolving consumer demands.

Remaining Segments in Foodservice Type

The full-service restaurants and quick-service restaurants segments complete the Spanish foodservice market landscape, each serving distinct consumer needs. Full-service restaurants cater to diners seeking complete dining experiences with table service and diverse cuisine options, ranging from traditional Spanish dishes to international fare. These establishments particularly benefit from Spain's tourism industry and business dining sector. Meanwhile, quick-service restaurants serve the growing demand for convenient, affordable dining options, particularly in urban areas and transportation hubs. Both segments have adapted to modern consumer preferences by incorporating digital ordering systems and delivery services while maintaining their distinct service models and target demographics.

Segment Analysis: Outlet

Independent Outlets Segment in Spain Foodservice Market

The independent outlets segment dominates the Spanish food service channel, commanding approximately 68% market share in 2024. The flexibility of operations and the exclusive cuisine options and dining experiences are the main factors promoting the growth of this segment in the nation. Independent outlets are perceived as performing better than chains in several areas, including meeting customer expectations for the dining experience and ambiance, as well as the "table stakes" of food quality, service, value, and menu innovation. The segment is particularly strong in the cafes and bars category, where independent operators can offer unique, locally-inspired experiences. These establishments benefit from their ability to quickly adapt to local preferences and maintain strong connections with their communities, which has helped them maintain their market leadership position.

Chained Outlets Segment in Spain Foodservice Market

The chained outlets segment is demonstrating remarkable growth potential in the Spanish foodservice market, projected to expand at approximately 14% during 2024-2029. This growth is driven by several factors, including the increasing demand for standardized quality and service across locations, particularly in urban areas. International chains are actively expanding their presence through strategic location selections in high-traffic areas such as shopping centers and transportation hubs. The segment's growth is further supported by robust supplier networks, efficient operational systems, and strong brand recognition. Chained outlets are also leading the way in technological adoption, implementing digital ordering systems, loyalty programs, and delivery partnerships, which are increasingly important to Spanish consumers. The segment's expansion is particularly notable in the quick-service restaurant category, where major international brands are introducing innovative menu items and adapting to local tastes while maintaining their global standards.

Segment Analysis: Location

Standalone Segment in Spain Foodservice Market

The standalone segment dominates the Spanish food service report, accounting for approximately 76% market share in 2024. This significant market position can be attributed to the high quality of food, ambiance, and strategic locations of well-known food service establishments in major cities like Madrid, Barcelona, and Marbella. International visitors show a strong preference for dining in well-known and reputable standalone establishments when visiting Spain for business or pleasure, which continues to drive the expansion of these types of restaurants throughout the country. The segment's growth is further supported by the increasing number of fine-dining outlets, with Spain ranking among the top 5 countries globally for Michelin-starred eateries in 2024, featuring numerous prestigious standalone restaurants across different cuisines.

Travel Segment in Spain Foodservice Market

The travel segment is projected to exhibit the strongest growth in the Spanish foodservice market, with an expected CAGR of approximately 15% during 2024-2029. This robust growth is driven by the extensive network of railway stations and airports in the country, along with the increasing number of people utilizing transportation services. The segment's expansion is supported by major in-flight caterers like LSG Sky Chefs, Newrest, Bluma, Air Culinaire, and Inflight Chef Delight, who continue to enhance their service offerings. The presence of nearly 50 major public airports in Spain, combined with the growing railway passenger traffic, creates substantial opportunities for foodservice operators in travel locations, particularly in high-traffic hubs like Adolfo-Suarez Madrid Airport and Barcelona El Prat.

Remaining Segments in Location

The retail, leisure, and lodging segments each play vital roles in shaping the Spanish foodservice market landscape. The retail segment benefits from the growing commercial property sector and shopping mall culture, with foodservice outlets becoming integral parts of retail spaces. The leisure segment capitalizes on Spain's vibrant sports events, cultural festivals, and entertainment venues, offering diverse dining options to attendees. The lodging segment serves the hospitality sector, with hotels and accommodation facilities incorporating various dining concepts to enhance guest experiences. These segments collectively contribute to the market's diversity and cater to different consumer preferences and occasions.

Spain Foodservice Industry Overview

Top Companies in Spain Foodservice Market

The Spanish foodservice market features prominent players like Áreas SAU, McDonald's Corporation, AmRest Holdings SE, Alsea SAB de CV, and Restaurant Brands Iberia, leading the industry through various strategic initiatives. Companies in the food and restaurant industry are increasingly focusing on product innovation through the introduction of plant-based options, gluten-free alternatives, and sustainable packaging solutions to meet evolving consumer preferences. Operational agility is demonstrated through the adoption of digital transformation initiatives, including online ordering systems and delivery partnerships. Strategic expansion moves include both organic growth through new outlet openings and inorganic growth through acquisitions and franchise agreements. Companies are also emphasizing geographical expansion, particularly in high-traffic areas like airports, shopping centers, and tourist destinations, while simultaneously exploring opportunities in residential areas to adapt to changing consumer behaviors.

Fragmented Market with Strong Local Presence

The Spanish food and restaurant industry exhibits a highly fragmented structure with a mix of global chains and local operators competing across various segments. The market is characterized by strong regional players who have established deep roots in local communities through their understanding of Spanish culinary preferences and dining habits. Major international conglomerates operate alongside specialized local players, creating a diverse competitive landscape that spans quick-service restaurants, cafes, bars, and full-service establishments. The market has witnessed significant merger and acquisition activities, particularly in the cloud kitchen and specialty coffee segments, as companies seek to consolidate their positions and expand their service offerings.

The competitive dynamics are shaped by the presence of both independent outlets and chained establishments, with independent operators maintaining a dominant position in the market. Global players are increasingly entering the market through franchise agreements and strategic partnerships with local operators to leverage their market knowledge and established networks. The market has seen a trend of consolidation in certain segments, particularly in the quick-service restaurant sector, where larger chains are acquiring smaller operators to expand their footprint and achieve economies of scale.

Innovation and Adaptation Drive Market Success

For incumbent players to maintain and increase their market share, focus needs to be placed on menu innovation, digital transformation, and sustainability initiatives. Companies must invest in developing unique value propositions that align with local tastes while incorporating global food trends. The adoption of advanced technologies for order management, customer engagement, and delivery operations has become crucial for maintaining competitive advantage. Established players need to continuously evaluate and optimize their location strategies, considering factors such as changing demographics, urbanization patterns, and tourist flows.

New entrants and challenger brands can gain ground by identifying and filling specific market gaps, particularly in emerging segments such as health-focused offerings and specialized cuisine types. Success in the market requires building strong relationships with suppliers, developing efficient supply chain networks, and creating distinctive brand identities that resonate with Spanish consumers. Companies must also prepare for potential regulatory changes, particularly regarding sustainability and food safety standards, while maintaining flexibility to adapt to shifting consumer preferences and economic conditions. The ability to offer competitive pricing while maintaining quality standards remains crucial for both established players and new entrants in this dynamic market. The restaurant industry analysis indicates that understanding the food industry market size is essential for strategic planning and competitive positioning.

Spain Foodservice Market Leaders

-

Alsea SAB de CV

-

AmRest Holdings SE

-

McDonald's Corporation

-

Restaurant Brands Iberia

-

Áreas SAU

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Spain Foodservice Market News

- March 2023: Telepiza launched Megamediana, a medium-sized pizza larger and cheaper than the rest of the sector in the context of smaller products at higher prices. At 33 centimeters, several centimeters bigger than the rest of the medium pizzas in the industry, and a price of USD 8.20, it is also the pizza with the best size/price ratio in the market.

- February 2023: Groupo Ibersol signed an agreement with Pret A Manger to expand into Portugal and Spain to create a solid network of restaurants with a presence in the commercial catering and travel sectors.

- February 2023: The Ibersol Group’s travel catering division was awarded a contract from AENA for 10 new points of sale at Adolfo Suárez Madrid-Barajas airport. The contract will last for eight years and is expected to turn over more than EUR 30 million. In addition, the company was awarded a contract for eight restaurants at César Manrique-Lanzarote International Airport and incorporated six locations in the Air Zone of T1 and two locations in the T1 and T2 Ground Zone.

Free With This Report

We provide a complimentary and exhaustive set of data points on regional and country level metrics that present the fundamental structure of the industry. Presented in the form of 60+ free charts, the section covers difficult to find data on various countries on number of outlets, average order values, and menu analysis by foodservice channels, cuisine specific insights related to full service restaurants and quick service restaurants, market trends and market size insights on cafes, bars & pubs, juice/smoothies bars, specialty tea and coffee shops, and cloud kitchen etc.

Spain Foodservice Market Report - Table of Contents

1. EXECUTIVE SUMMARY & KEY FINDINGS

2. REPORT OFFERS

3. INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4. KEY INDUSTRY TRENDS

- 4.1 Number Of Outlets

- 4.2 Average Order Value

-

4.3 Regulatory Framework

- 4.3.1 Spain

- 4.4 Menu Analysis

5. MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

-

5.1 Foodservice Type

- 5.1.1 Cafes & Bars

- 5.1.1.1 By Cuisine

- 5.1.1.1.1 Bars & Pubs

- 5.1.1.1.2 Cafes

- 5.1.1.1.3 Juice/Smoothie/Desserts Bars

- 5.1.1.1.4 Specialist Coffee & Tea Shops

- 5.1.2 Cloud Kitchen

- 5.1.3 Full Service Restaurants

- 5.1.3.1 By Cuisine

- 5.1.3.1.1 Asian

- 5.1.3.1.2 European

- 5.1.3.1.3 Latin American

- 5.1.3.1.4 Middle Eastern

- 5.1.3.1.5 North American

- 5.1.3.1.6 Other FSR Cuisines

- 5.1.4 Quick Service Restaurants

- 5.1.4.1 By Cuisine

- 5.1.4.1.1 Bakeries

- 5.1.4.1.2 Burger

- 5.1.4.1.3 Ice Cream

- 5.1.4.1.4 Meat-based Cuisines

- 5.1.4.1.5 Pizza

- 5.1.4.1.6 Other QSR Cuisines

-

5.2 Outlet

- 5.2.1 Chained Outlets

- 5.2.2 Independent Outlets

-

5.3 Location

- 5.3.1 Leisure

- 5.3.2 Lodging

- 5.3.3 Retail

- 5.3.4 Standalone

- 5.3.5 Travel

6. COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

-

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Alsea SAB de CV

- 6.4.2 AmRest Holdings SE

- 6.4.3 Comess Group

- 6.4.4 Compass Group PLC

- 6.4.5 Food Delivery Brands

- 6.4.6 Groupo Ibersol

- 6.4.7 McDonald's Corporation

- 6.4.8 Restalia Grupo De Eurorestauracion SL

- 6.4.9 Restaurant Brands Iberia

- 6.4.10 Áreas SAU

7. KEY STRATEGIC QUESTIONS FOR FOODSERVICE CEOS

8. APPENDIX

-

8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter’s Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

List of Tables & Figures

- Figure 1:

- NUMBER OF OUTLET UNITS BY FOODSERVICE CHANNELS, SPAIN, 2017 - 2029

- Figure 2:

- AVERAGE ORDER VALUE BY FOODSERVICE CHANNELS, USD, SPAIN, 2017 VS 2022 VS 2029

- Figure 3:

- SPAIN FOODSERVICE MARKET, VALUE, USD, 2017 - 2029

- Figure 4:

- VALUE OF FOODSERVICE MARKET BY FOODSERVICE TYPE, USD, SPAIN, 2017 - 2029

- Figure 5:

- VALUE SHARE OF FOODSERVICE MARKET, %, BY FOODSERVICE TYPE, SPAIN, 2017 VS 2023 VS 2029

- Figure 6:

- VALUE OF CAFES & BARS FOODSERVICE MARKET BY CUISINE, USD, SPAIN, 2017 - 2029

- Figure 7:

- VALUE SHARE OF CAFES & BARS FOODSERVICE MARKET BY CUISINE, %, SPAIN, 2017 VS 2023 VS 2029

- Figure 8:

- VALUE OF FOODSERVICE MARKET VIA BARS & PUBS, USD, SPAIN, 2017 - 2029

- Figure 9:

- VALUE SHARE OF BARS & PUBS FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 10:

- VALUE OF FOODSERVICE MARKET VIA CAFES, USD, SPAIN, 2017 - 2029

- Figure 11:

- VALUE SHARE OF CAFES FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 12:

- VALUE OF FOODSERVICE MARKET VIA JUICE/SMOOTHIE/DESSERTS BARS, USD, SPAIN, 2017 - 2029

- Figure 13:

- VALUE SHARE OF JUICE/SMOOTHIE/DESSERTS BARS FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 14:

- VALUE OF FOODSERVICE MARKET VIA SPECIALIST COFFEE & TEA SHOPS, USD, SPAIN, 2017 - 2029

- Figure 15:

- VALUE SHARE OF SPECIALIST COFFEE & TEA SHOPS FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 16:

- VALUE OF CLOUD KITCHEN FOODSERVICE MARKET, USD, SPAIN, 2017 - 2029

- Figure 17:

- VALUE SHARE OF CLOUD KITCHEN FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 18:

- VALUE OF FULL SERVICE RESTAURANTS FOODSERVICE MARKET BY CUISINE, USD, SPAIN, 2017 - 2029

- Figure 19:

- VALUE SHARE OF FULL SERVICE RESTAURANTS FOODSERVICE MARKET BY CUISINE, %, SPAIN, 2017 VS 2023 VS 2029

- Figure 20:

- VALUE OF ASIAN FOODSERVICE MARKET, USD, SPAIN, 2017 - 2029

- Figure 21:

- VALUE SHARE OF ASIAN FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 22:

- VALUE OF EUROPEAN FOODSERVICE MARKET, USD, SPAIN, 2017 - 2029

- Figure 23:

- VALUE SHARE OF EUROPEAN FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 24:

- VALUE OF LATIN AMERICAN FOODSERVICE MARKET, USD, SPAIN, 2017 - 2029

- Figure 25:

- VALUE SHARE OF LATIN AMERICAN FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 26:

- VALUE OF MIDDLE EASTERN FOODSERVICE MARKET, USD, SPAIN, 2017 - 2029

- Figure 27:

- VALUE SHARE OF MIDDLE EASTERN FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 28:

- VALUE OF NORTH AMERICAN FOODSERVICE MARKET, USD, SPAIN, 2017 - 2029

- Figure 29:

- VALUE SHARE OF NORTH AMERICAN FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 30:

- VALUE OF OTHER FSR CUISINES MARKET, USD, SPAIN, 2017 - 2029

- Figure 31:

- VALUE SHARE OF OTHER FSR CUISINES FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 32:

- VALUE OF QUICK SERVICE RESTAURANTS FOODSERVICE MARKET BY CUISINE, USD, SPAIN, 2017 - 2029

- Figure 33:

- VALUE SHARE OF QUICK SERVICE RESTAURANTS FOODSERVICE MARKET BY CUISINE, %, SPAIN, 2017 VS 2023 VS 2029

- Figure 34:

- VALUE OF BAKERIES FOODSERVICE MARKET, USD, SPAIN, 2017 - 2029

- Figure 35:

- VALUE SHARE OF BAKERIES FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 36:

- VALUE OF BURGER FOODSERVICE MARKET, USD, SPAIN, 2017 - 2029

- Figure 37:

- VALUE SHARE OF BURGER FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 38:

- VALUE OF ICE CREAM FOODSERVICE MARKET, USD, SPAIN, 2017 - 2029

- Figure 39:

- VALUE SHARE OF ICE CREAM FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 40:

- VALUE OF MEAT-BASED CUISINES FOODSERVICE MARKET, USD, SPAIN, 2017 - 2029

- Figure 41:

- VALUE SHARE OF MEAT-BASED CUISINES FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 42:

- VALUE OF PIZZA FOODSERVICE MARKET, USD, SPAIN, 2017 - 2029

- Figure 43:

- VALUE SHARE OF PIZZA FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 44:

- VALUE OF OTHER QSR CUISINES FOODSERVICE MARKET, USD, SPAIN, 2017 - 2029

- Figure 45:

- VALUE SHARE OF OTHER QSR CUISINES FOODSERVICE MARKET BY OUTLETS, %, SPAIN, 2022 VS 2029

- Figure 46:

- VALUE OF FOODSERVICE MARKET BY OUTLET, USD, SPAIN, 2017 - 2029

- Figure 47:

- VALUE SHARE OF FOODSERVICE MARKET, %, BY OUTLET, SPAIN, 2017 VS 2023 VS 2029

- Figure 48:

- VALUE OF FOODSERVICE MARKET VIA CHAINED OUTLETS, USD, SPAIN, 2017 - 2029

- Figure 49:

- VALUE SHARE OF CHAINED OUTLETS FOODSERVICE MARKET BY FOODSERVICE TYPE, %, SPAIN, 2022 VS 2029

- Figure 50:

- VALUE OF FOODSERVICE MARKET VIA INDEPENDENT OUTLETS, USD, SPAIN, 2017 - 2029

- Figure 51:

- VALUE SHARE OF INDEPENDENT OUTLETS FOODSERVICE MARKET BY FOODSERVICE TYPE, %, SPAIN, 2022 VS 2029

- Figure 52:

- VALUE OF FOODSERVICE MARKET BY LOCATION, USD, SPAIN, 2017 - 2029

- Figure 53:

- VALUE SHARE OF FOODSERVICE MARKET, %, BY LOCATION, SPAIN, 2017 VS 2023 VS 2029

- Figure 54:

- VALUE OF FOODSERVICE MARKET VIA LEISURE LOCATION, USD, SPAIN, 2017 - 2029

- Figure 55:

- VALUE SHARE OF LEISURE FOODSERVICE MARKET BY FOODSERVICE TYPE, %, SPAIN, 2022 VS 2029

- Figure 56:

- VALUE OF FOODSERVICE MARKET VIA LODGING LOCATION, USD, SPAIN, 2017 - 2029

- Figure 57:

- VALUE SHARE OF LODGING FOODSERVICE MARKET BY FOODSERVICE TYPE, %, SPAIN, 2022 VS 2029

- Figure 58:

- VALUE OF FOODSERVICE MARKET VIA RETAIL LOCATION, USD, SPAIN, 2017 - 2029

- Figure 59:

- VALUE SHARE OF RETAIL FOODSERVICE MARKET BY FOODSERVICE TYPE, %, SPAIN, 2022 VS 2029

- Figure 60:

- VALUE OF FOODSERVICE MARKET VIA STANDALONE LOCATION, USD, SPAIN, 2017 - 2029

- Figure 61:

- VALUE SHARE OF STANDALONE FOODSERVICE MARKET BY FOODSERVICE TYPE, %, SPAIN, 2022 VS 2029

- Figure 62:

- VALUE OF FOODSERVICE MARKET VIA TRAVEL LOCATION, USD, SPAIN, 2017 - 2029

- Figure 63:

- VALUE SHARE OF TRAVEL FOODSERVICE MARKET BY FOODSERVICE TYPE, %, SPAIN, 2022 VS 2029

- Figure 64:

- MOST ACTIVE COMPANIES BY NUMBER OF STRATEGIC MOVES, COUNT, SPAIN, 2019 - 2023

- Figure 65:

- MOST ADOPTED STRATEGIES, COUNT, SPAIN, 2019 - 2023

- Figure 66:

- VALUE SHARE OF MAJOR PLAYERS, %, SPAIN

Spain Foodservice Industry Segmentation

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.| Foodservice Type | Cafes & Bars | By Cuisine | Bars & Pubs | |

| Cafes | ||||

| Juice/Smoothie/Desserts Bars | ||||

| Specialist Coffee & Tea Shops | ||||

| Cloud Kitchen | ||||

| Full Service Restaurants | By Cuisine | Asian | ||

| European | ||||

| Latin American | ||||

| Middle Eastern | ||||

| North American | ||||

| Other FSR Cuisines | ||||

| Quick Service Restaurants | By Cuisine | Bakeries | ||

| Burger | ||||

| Ice Cream | ||||

| Meat-based Cuisines | ||||

| Pizza | ||||

| Other QSR Cuisines | ||||

| Outlet | Chained Outlets | |||

| Independent Outlets | ||||

| Location | Leisure | |||

| Lodging | ||||

| Retail | ||||

| Standalone | ||||

| Travel | ||||

Need A Different Region or Segment?

Customize Now

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF