Market Trends of Spain Construction Industry

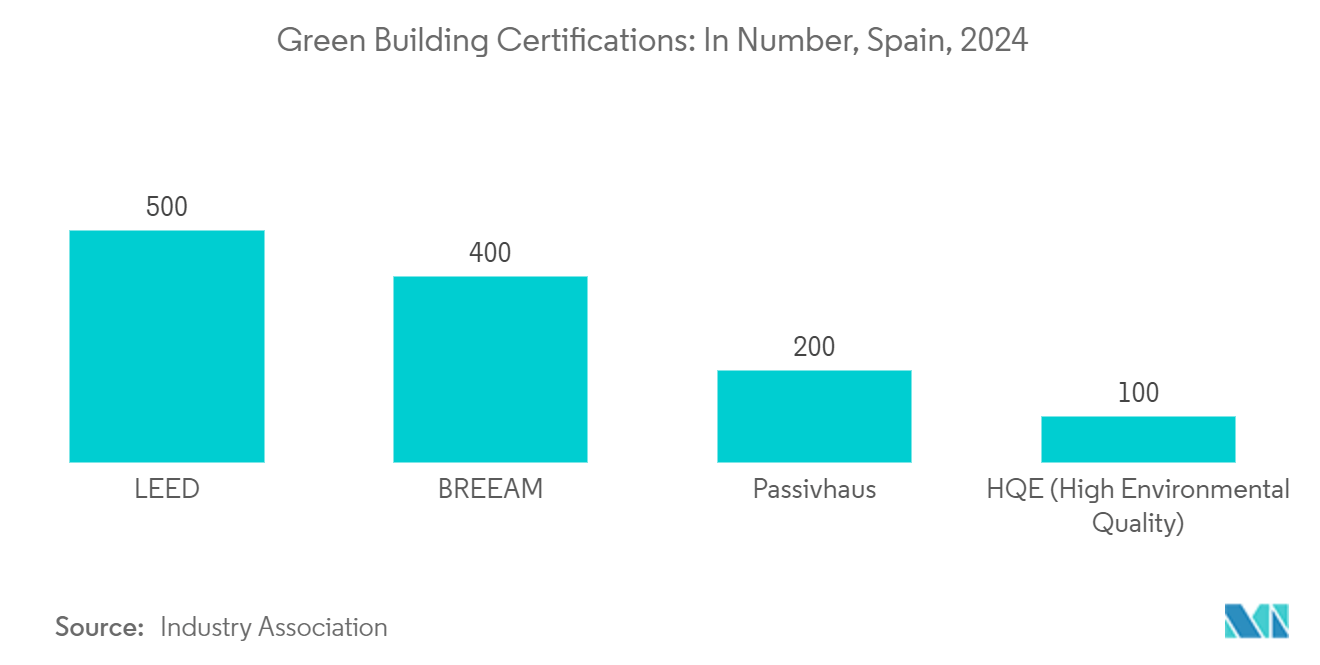

Green and Sustainable Construction

Government policies and market demand are steering a pronounced shift towards energy-efficient buildings, green infrastructure, and sustainable construction practices. In alignment with this trend, the Spanish government is channeling substantial investments into the renovation of 500,000 homes by 2026, prioritizing energy efficiency. Furthermore, there's an escalating demand for green building certifications, such as BREEAM and LEED, spanning residential, commercial, and industrial sectors.

Spain's government is set to revamp 500,000 homes by 2026, underscoring a pronounced focus on energy efficiency. This endeavor underscores a marked surge in green construction activities. In spite of hurdles like escalating costs and labor shortages, the Spanish government has rolled out pivotal initiatives to rejuvenate and expand the construction sector.

According to a report by The Green Building Insider, Spain boasts 166 certified sustainable buildings across various cities. Leading the pack is Madrid, followed closely by Barcelona and the province of Vizcaya. Breaking it down, 98 of these certified buildings serve as offices, 24 are designated for commercial use, and 11 cater to industrial purposes. Notably, the crown jewel of sustainability in Spain is the European Union Intellectual Property Office (EQUIPO) situated in Alicante. Additionally, the AA81 building in Torre Rioja, Madrid, stands out as another prime example, proudly holding the prestigious LEED Platinum certification.

On July 29, Reuters reported from Madrid: The Spanish government has greenlit nearly 300 renewable energy projects, boasting a combined capacity exceeding 28 gigawatts. This move is pivotal for Spain as it strives to achieve its ambitious green energy targets.

In conclusion, Spain's proactive approach towards energy efficiency and sustainable construction is evident through its substantial investments and policy initiatives. These efforts not only aim to meet green energy targets but also position Spain as a leader in sustainable development

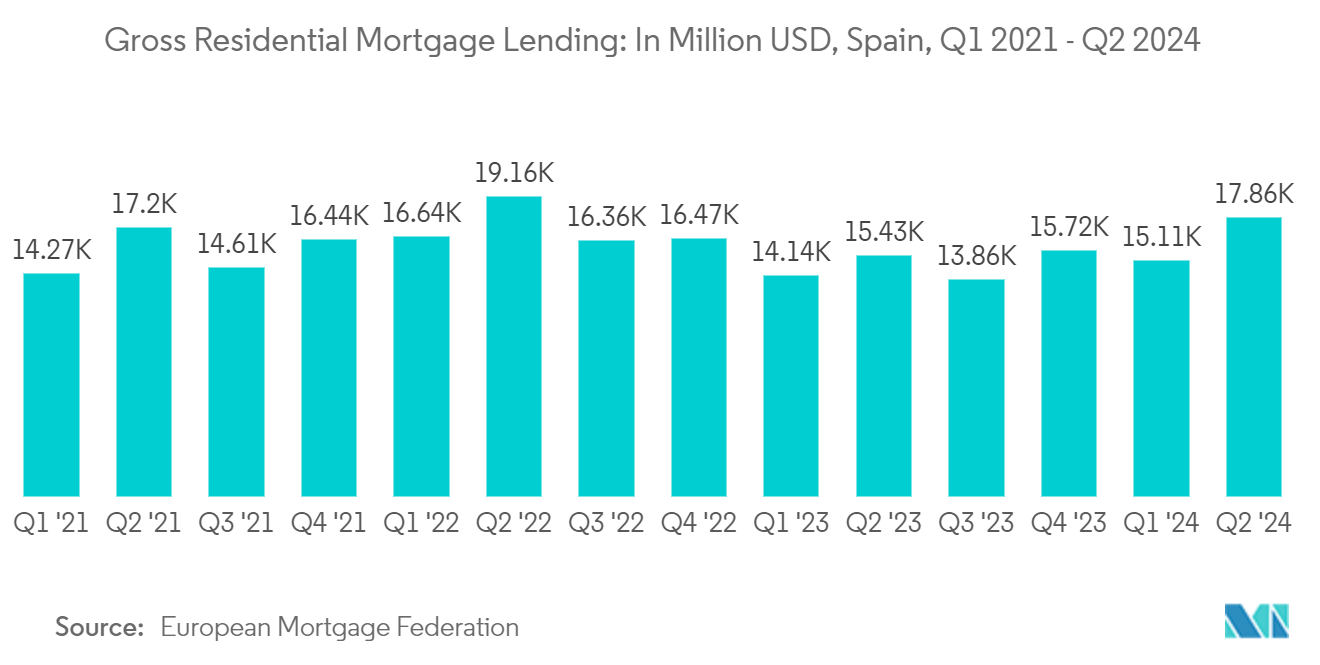

Spain's Construction Market Fueled by Residential Sector

Spain's construction market is witnessing a robust upswing, predominantly driven by the residential sector. Data from industry associations indicate that residential construction approvals are poised to surge in 2024, targeting 120,000 units. This momentum is projected to carry into 2025, with new housing starts anticipated to rise by approximately 15%. Housing sales have shown resilience, marking a 6.1% growth in the initial five months of 2024. Concurrently, new building permits, though at a modest level, recorded a year-on-year uptick of 14.8% between January and May 2024. This buoyancy in the market can be largely attributed to declining interest rates coupled with a rejuvenating economy, fostering a conducive atmosphere for both homebuyers and developers.

However, the market grapples with a persistent imbalance between housing supply and demand, leading to escalating prices. Industry reports highlight a 4.3% year-on-year surge in residential property prices in Q1 2024, underscoring the challenges in catering to the burgeoning demand for housing. This scenario paints a picture of a market where housing production struggles to match the escalating demand, especially in urban locales witnessing heightened population density. Consequently, developers are pivoting towards new residential projects, eager to seize the burgeoning opportunity.

Driving this residential momentum further is the Spanish government's proactive stance on housing. As part of a comprehensive initiative, the government has unveiled plans to construct 43,000 affordable rental homes, channeling a substantial EUR 6 billion (USD 6.32 billion) in funding. This initiative, reported by Dawn Digest in July 2024, not only seeks to alleviate housing shortages but also emphasizes energy efficiency and sustainability in residential constructions. Such endeavors are poised to invigorate construction activities and bolster job creation in the sector.

In conclusion, the residential sector is set to remain a pivotal force in driving Spain's construction market in 2024 and beyond. With supportive government initiatives, a recovering economy, and increasing demand for housing, the sector is well-positioned for sustained growth. However, addressing the supply-demand gap will be critical to ensuring long-term stability and affordability in the market.