Market Overview

| Study Period | 2017 - 2028 |

|---|---|

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2028 |

| Market Size (2024) | USD 2.21 Billion |

| Market Size (2028) | USD 2.75 Billion |

| Growth Rate (2024 - 2028) | 5.64% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spain Adhesives Market Analysis by Mordor Intelligence

The Spain Adhesives Market size is estimated at 2.21 billion USD in 2024, and is expected to reach 2.75 billion USD by 2028, growing at a CAGR of 5.64% during the forecast period (2024-2028).

Spain's adhesives industry is experiencing significant transformation driven by major infrastructure and technological developments. The Spanish government has announced substantial investments in infrastructure development, including a EUR 24.2 billion commitment to rail infrastructure improvements over the next five years. This infrastructure push is complemented by the establishment of new industrial facilities, exemplified by Amazon Web Services' launch of its seventh European infrastructure region in Spain, marking a significant expansion of industrial capacity that requires advanced industrial adhesives solutions.

The packaging sector continues to be a cornerstone of adhesive consumption in Spain, particularly in food and beverage applications. The industry has demonstrated remarkable resilience, with carton board production reaching 321.6 thousand tons despite market challenges. The food packaging segment is witnessing steady growth, driven by increasing demand for packaged meat, seafood, processed fruits, and vegetables. Packaging adhesives have emerged as a preferred choice in packaging applications, with consumption reaching approximately 201 thousand tons in the packaging industry.

The construction sector is undergoing substantial transformation through the Next Generation EU recovery plan, which emphasizes energy-efficient building construction and renovation. According to Spain's National Statistics Institute (INE), residential construction is projected to maintain a steady pace of around 135,000 new units annually through 2025. This sustained growth in construction activity is creating robust demand for specialized construction adhesives solutions that meet both structural requirements and environmental standards.

The aerospace and defense sectors are emerging as significant growth drivers for advanced adhesive applications. The Spanish government has designated the aerospace sector as a Strategic Project for Economic Recovery and Transformation (PERTE), committing EUR 4.5 billion in investments by 2025, including EUR 2.3 billion from the private sector. The establishment of the Spanish Space Agency in 2023 further underscores the country's commitment to aerospace development, creating new opportunities for high-performance aerospace adhesives solutions in critical applications.

Spain Adhesives Market Trends and Insights

With the advancement in plastic recyclability and demand from the food and beverage industry, plastic packaging to lead the packaging industry

- Packaging is one of the fastest-growing industries in terms of design and technology for protecting and enhancing products' safety and longevity. The Spanish packaging industry has been majorly driven by the rapid growth of the food and beverages industry in recent years. The agri-food industry is the most promising sector in Spain and the fourth-largest agri-food market in Europe, with over 30,000 companies. Owing to the high-level promotion of country brands, Spain has positioned itself as a major exporter of food and drinks worldwide.

- Due to the COVID-19 pandemic, the country-wide lockdowns and temporary shutdown of manufacturing facilities caused several issues, including disruptions in supply chains and imports and exports. As a result, the country's packaging production declined by 6% in 2020 compared to the previous year, significantly affecting the market. Packaging production is majorly driven by paper and paperboard in the country, which accounts for nearly 52% of the packaging produced in 2021. However, with the advancement of plastic recyclability, the plastic production segment is likely to register the fastest growth of around 4.27% CAGR during the forecast period.

- The growth of the packaging industry in Spain is in line with the growing demand for fresh food domestically. The growing interest in public health issues post-pandemic, along with the emerging e-commerce activities across the nation, is likely to boost the growth of the food processing industry and further drive the demand for packaging over the coming years.

Understand The Key Trends Shaping This Market

Download PDF

Increasing EVs demand and government investment of public and private e-mobility investments worth EUR 24 billion to boost the automotive demand

- Spain is the second-largest automobile producer in Europe, after Germany. Spanish automotive suppliers produced EUR 35,822 million worth of products in 2019, of which 60% were exported inside and outside the European region.

- Automobile production in the country has been almost constant in the past few years. In 2019, the country produced about 28,22,355 units, registering a meager growth rate of 0.1% over 2018. The country produced about 22,68,185 units of vehicles in 2020. Automotive vehicle production contracted by 18.6% in 2020 as the COVID-19 pandemic halted the supply chain.

- In the first three quarters of 2021, automotive production increased by 4% over Q1-Q3 of 2020 and reached 1,592,277 vehicles. The country's automotive industry is likely to witness moderate demand during the forecast period. However, in 2021, the country produced about 2,098,133 vehicles, which was a decline of 8% from 2020. The semiconductor chip shortage and supply chain restrictions negatively affected the production of automotive vehicle units in the country.

- The automotive production shortfalls have recently worsened, and a strong rebound is expected in 2022, with output increasing by 18%. The Spanish electric vehicles market should benefit from the Next Generation EU fund, which supports suppliers in their shift toward e-mobility. Additionally, the Spanish government has announced public and private e-mobility investments worth EUR 24 billion over the coming three years.

Understand The Key Trends Shaping This Market

Download PDF

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Increasing government investments including the Priority Project for Economic Recovery and Transformation (PERTE) leads the aerospace industry

- Increasing demand for sports footwear and the usage of automation and robotics in production lines to reduce production cost, the footwear industry is likely to propel

- Investments including National Recovery and Resilience Plan (NRRP) worth EUR 1 billion for affordable housing to lead the construction industry

- Increasing furniture demand and rising exports is likely to boost the woodworking and joinery

Segment Analysis: End User Industry

Packaging Segment in Spain Adhesives Market

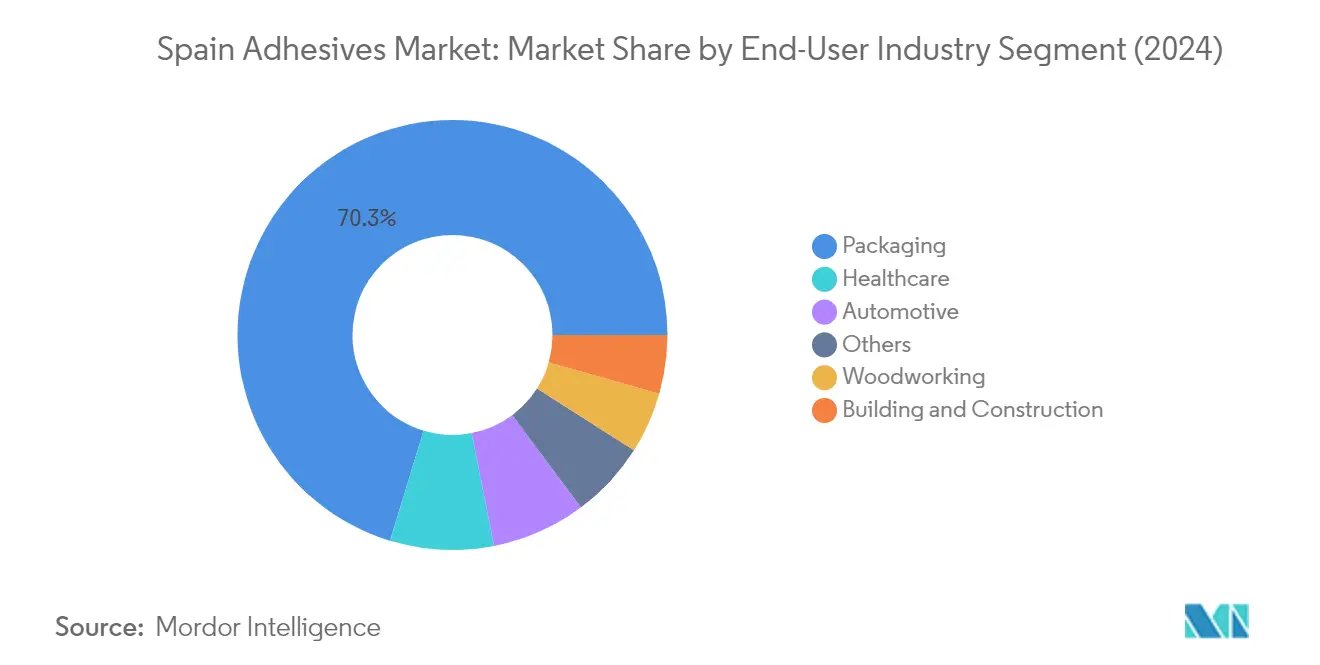

The packaging segment dominates the Spain adhesives market, accounting for approximately 70% of the total market value in 2024. This significant market share is driven by the extensive use of pressure-sensitive adhesives in various packaging applications, including labels, tapes, carton sealing and joining, and laminating. The segment's dominance is further strengthened by the robust growth of the food and beverage industry in Spain, which is the fourth-largest agri-food market in Europe with over 30,000 companies. The growing interest in public health issues, coupled with emerging e-commerce activities across the nation, continues to boost the growth of the food processing industry and drive the demand for packaging adhesives. Additionally, factors such as rising demand for packaged meat and seafood, processed fruits and vegetables, and widespread usage of liquid cartons for tomato pastes and purees are fostering adhesive consumption in flexible packaging applications.

Building & Construction Segment in Spain Adhesives Market

The building and construction segment is experiencing substantial growth in the Spanish adhesives market. Under the 2021-2026 National Recovery and Resilience Plan (NRRP), the Spanish government has allocated significant funds for constructing affordable and energy-efficient rental housing. The future industry growth is anticipated to be fueled by investments in public sector infrastructure, digitalization, energy-efficient housing renovations, and a green circular economy, all funded by the European Union. The general outlook for the Spanish construction industry remains favorable, with increasing demand for construction adhesives in applications such as flooring, garage doors, windows, tile insulation, and various other construction applications. The segment's growth is further supported by Amazon Web Services' infrastructure expansion and the Spanish government's plans to invest in rail infrastructure development.

Remaining Segments in End User Industry

The Spanish adhesives market encompasses several other significant segments including healthcare, automotive, aerospace, footwear and leather, and woodworking and joinery. The healthcare segment is driven by the country's comprehensive medical care system and growing medical device production, which increasingly relies on medical adhesives. The automotive segment benefits from Spain's position as one of Europe's largest automobile producers, particularly with the increasing focus on electric vehicle production. The aerospace segment leverages Spain's strong position in both civil and military aviation markets. The footwear and leather segment maintains steady demand due to Spain's position among the top footwear producers globally. The woodworking and joinery segment continues to be supported by Spain's significant furniture manufacturing industry and growing exports, with a notable reliance on wood adhesives.

Segment Analysis: Technology

Water-borne Segment in Spain Adhesives Market

Water-borne adhesives dominate the Spanish adhesives market, holding approximately 51% market share in 2024. These adhesives are primarily formulated as dispersions or emulsions, with dispersed polymer particles typically ranging from 50-300 nm in diameter. Their widespread adoption is driven by their position as an ideal substitute for solvent-borne adhesives, offering similar curing and adhesion properties while being more environmentally friendly. The segment's strength is particularly evident in applications involving porous substrates like wood, paper, textiles, and leather. In the packaging industry, water-borne adhesives are preferred for their excellent bonding capabilities with cardboard, paper, and pulp substrates. The segment's dominance is further reinforced by acrylic resin-based formulations, which account for nearly 45% of water-borne adhesives, particularly in tape and wrap applications across various industries.

Hot Melt Segment in Spain Adhesives Market

The hot melt adhesives segment is experiencing robust growth in the Spanish market, projected to grow at approximately 7% through 2024-2029. This growth is primarily driven by their increasing adoption in express delivery and packaging applications, where their ease of application provides significant advantages. These thermoplastic adhesives, available in various diameter formats such as 12mm, 15mm, or 43mm, offer operational flexibility within temperature ranges of 60-200 degrees centigrade. The segment's expansion is further supported by the booming e-commerce industry in Spain, which is creating substantial demand for efficient packaging solutions. Hot melt adhesives are particularly valued for their compatibility with wood substrates and their ability to replace traditional metallic fasteners, offering both cost and weight advantages in various applications.

Remaining Segments in Technology

The Spanish adhesives market encompasses several other important technology segments, including reactive adhesives, solvent-borne, and UV-cured adhesives. Reactive adhesives play a crucial role in automotive and structural applications, offering superior bonding strength and durability. Solvent-borne adhesives, while facing environmental scrutiny, continue to maintain their position in specific applications where their unique properties are essential. UV-cured adhesives have carved out a significant niche in high-precision applications, particularly in electronics and medical device manufacturing, where rapid curing and precise application are critical. Each of these segments contributes uniquely to the market's diversity, serving specific industrial needs and applications where their particular characteristics provide optimal performance.

Segment Analysis: Resin

VAE/EVA Segment in Spain Adhesives Market

The VAE/EVA segment dominates the Spanish adhesives market, holding approximately 26% market share in 2024. This segment's prominence can be attributed to its versatile applications across various industries, particularly in woodworking, packaging, and construction sectors. VAE/EVA adhesives are experiencing strong growth with a projected growth rate of around 7% during 2024-2029, driven by their eco-friendly nature and superior bonding properties. The increasing focus on sustainable solutions in the Spanish construction and packaging industries has significantly boosted the demand for VAE/EVA adhesives. These adhesives offer excellent adhesion to substrates such as wood, paper, and plastics, making them ideal for furniture manufacturing and packaging applications. Additionally, their lower VOC emissions compared to traditional adhesives have made them particularly attractive in light of stringent environmental regulations in Spain.

Acrylic Segment in Spain Adhesives Market

The acrylic adhesives segment represents a significant portion of the Spanish adhesives market, demonstrating robust growth potential. Acrylic adhesives are gaining traction due to their exceptional durability and versatility across multiple applications, particularly in the construction and automotive sectors. These adhesives exhibit superior resistance to environmental factors such as UV radiation and temperature variations, making them ideal for outdoor applications. The segment's growth is further supported by increasing demand from the furniture industry, where acrylic adhesives are preferred for their strong bonding capabilities with various substrates including wood, glass, and ceramics. The rising adoption of pressure-sensitive adhesives in the packaging industry, particularly for pressure-sensitive applications, continues to drive market expansion. Additionally, the segment benefits from ongoing technological advancements that enhance the performance characteristics of acrylic adhesives, making them more appealing to end-users across various industries.

Remaining Segments in Resin

The Spanish adhesives market encompasses several other important resin segments, including polyurethane adhesives, epoxy adhesives, silicone, and cyanoacrylate, each serving specific industrial applications. Polyurethane adhesives are particularly valued in the automotive and construction sectors for their exceptional strength and flexibility. Epoxy adhesives maintain a strong presence in high-performance applications, especially in aerospace and industrial assembly. Silicone-based adhesives are crucial in applications requiring high-temperature resistance and flexibility, particularly in electronics and construction. Cyanoacrylate adhesives, known for their rapid curing properties, serve various industrial and consumer applications. Each of these segments contributes uniquely to the market's diversity, offering specialized solutions for specific bonding requirements and continuing to evolve with technological advancements and changing industry needs.

Competitive Landscape

Top Companies in Spain Adhesives Market

The leading companies in the Spanish adhesives market are actively pursuing innovation and operational excellence to maintain their competitive positions. Product development efforts are primarily focused on sustainable solutions, including water-based formulations and eco-friendly alternatives with lower VOC emissions. Companies are strengthening their distribution networks through strategic partnerships and expanding their manufacturing capabilities to enhance market presence. Operational agility is being achieved through investments in advanced production technologies and digitalization initiatives. The market leaders are also focusing on customized solutions for specific end-user industries, particularly in packaging, construction, and automotive segments. Strategic moves include vertical integration to secure raw material supply chains and horizontal expansion through acquisitions to broaden product portfolios.

Market Structure Shows Mixed Global-Local Presence

The Spanish adhesives market exhibits a fragmented structure with a mix of global conglomerates and local specialists competing for market share. Global players like Henkel, Sika, and H.B. Fuller leverage their extensive research capabilities and established brand presence to serve diverse industry segments. Local companies maintain their competitive edge through specialized product offerings and a deep understanding of regional market dynamics. The market demonstrates moderate consolidation, with the top five companies collectively holding a notable market share, while numerous smaller players cater to niche applications and specific geographic regions.

The market is characterized by ongoing consolidation activities as larger companies seek to strengthen their position through strategic acquisitions of local players. These acquisitions are primarily aimed at gaining access to established distribution networks, specialized technologies, and regional customer bases. Global companies are establishing local manufacturing facilities to better serve the Spanish market, while domestic players are forming strategic alliances to enhance their technological capabilities and expand their product portfolios. The competitive landscape is further shaped by the presence of both diversified chemical companies and specialized adhesive manufacturers.

Innovation and Sustainability Drive Future Success

Success in the Spanish adhesives market increasingly depends on companies' ability to develop innovative, sustainable solutions while maintaining cost competitiveness. Incumbent players are focusing on strengthening their research and development capabilities to create advanced formulations that meet evolving industry requirements, particularly in high-growth segments like electric vehicles and energy-efficient construction. Market leaders are investing in digital technologies to optimize their operations and enhance customer service capabilities. Companies are also developing comprehensive sustainability strategies, including circular economy initiatives and bio-based product development, to align with regulatory requirements and changing customer preferences.

For contenders looking to gain market share, success factors include developing specialized product offerings for underserved market segments and establishing strong relationships with key end-users. Companies must navigate the increasing concentration of end-user industries, particularly in the automotive and packaging sectors, by offering customized solutions and technical support services. The risk of substitution from alternative bonding agents necessitates continuous innovation in adhesive formulations and application methods. Future regulatory changes, particularly regarding environmental standards and chemical safety, will require companies to maintain flexible production capabilities and invest in compliant technologies. Building strong distribution networks and technical service capabilities remains crucial for both established players and new entrants.

Spain Adhesives Industry Leaders

-

3M

-

H.B. Fuller Company

-

Henkel AG & Co. KGaA

-

Huntsman International LLC

-

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2022: Henkel introduced new products, such as Loctite Liofol LA 7818 RE / 6231 RE and Loctite Liofol LA 7102 RE / 6902 RE, to promote recyclability in the packaging industry.

- February 2022: H.B. Fuller announced the acquisition of Fourny NV to strengthen its Construction Adhesives business in Europe.

- October 2021: 3M introduced a new generation of acrylic adhesives, including 3M Scotch-Weld Low Odor Acrylic Adhesive 8700NS Series, 3M Scotch-Weld Flexible Acrylic Adhesive 8600NS Series, and 3M Scotch-Weld Nylon Bonder Structural Adhesive DP8910NS.

Spain Adhesives Market Report Scope

Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, Woodworking and Joinery are covered as segments by End User Industry. Hot Melt, Reactive, Solvent-borne, UV Cured Adhesives, Water-borne are covered as segments by Technology. Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, VAE/EVA are covered as segments by Resin.

End User Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking and Joinery |

| Other End-user Industries |

Technology

| Hot Melt |

| Reactive |

| Solvent-borne |

| UV Cured Adhesives |

| Water-borne |

Resin

| Acrylic |

| Cyanoacrylate |

| Epoxy |

| Polyurethane |

| Silicone |

| VAE/EVA |

| Other Resins |

| End User Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking and Joinery | |

| Other End-user Industries | |

| Technology | Hot Melt |

| Reactive | |

| Solvent-borne | |

| UV Cured Adhesives | |

| Water-borne | |

| Resin | Acrylic |

| Cyanoacrylate | |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| VAE/EVA | |

| Other Resins |

Need A Different Region or Segment?

Customize Now

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF