Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

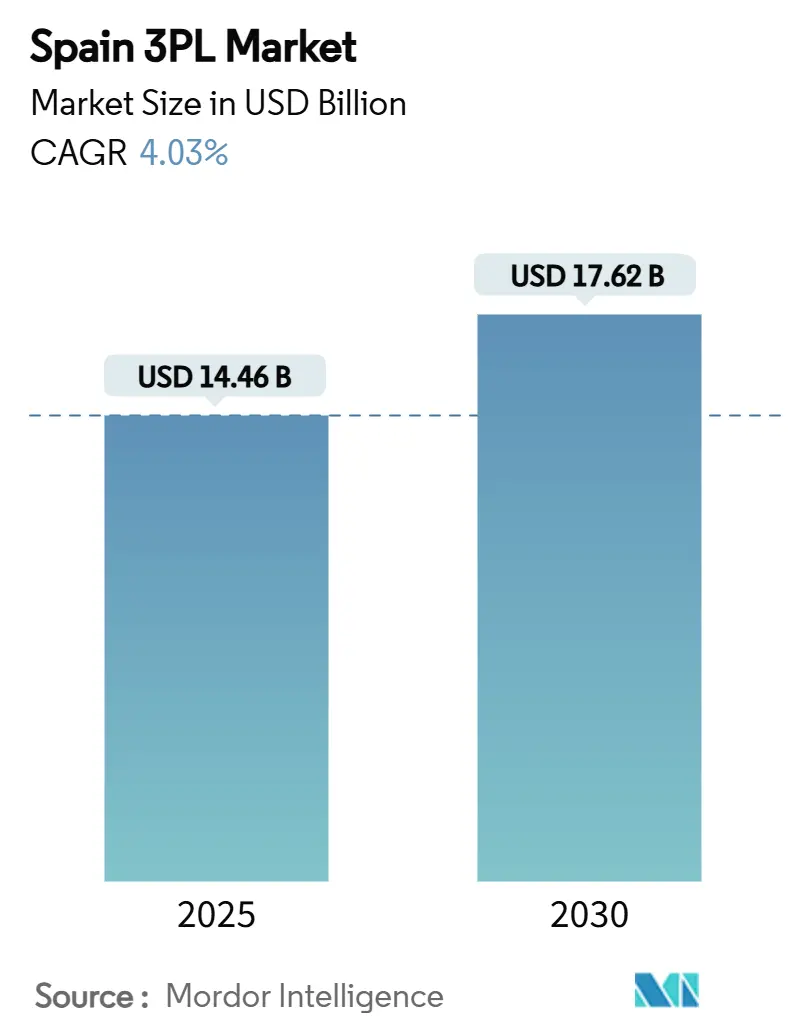

| Market Size (2025) | USD 14.46 Billion |

| Market Size (2030) | USD 17.62 Billion |

| Growth Rate (2025 - 2030) | 4.03% CAGR |

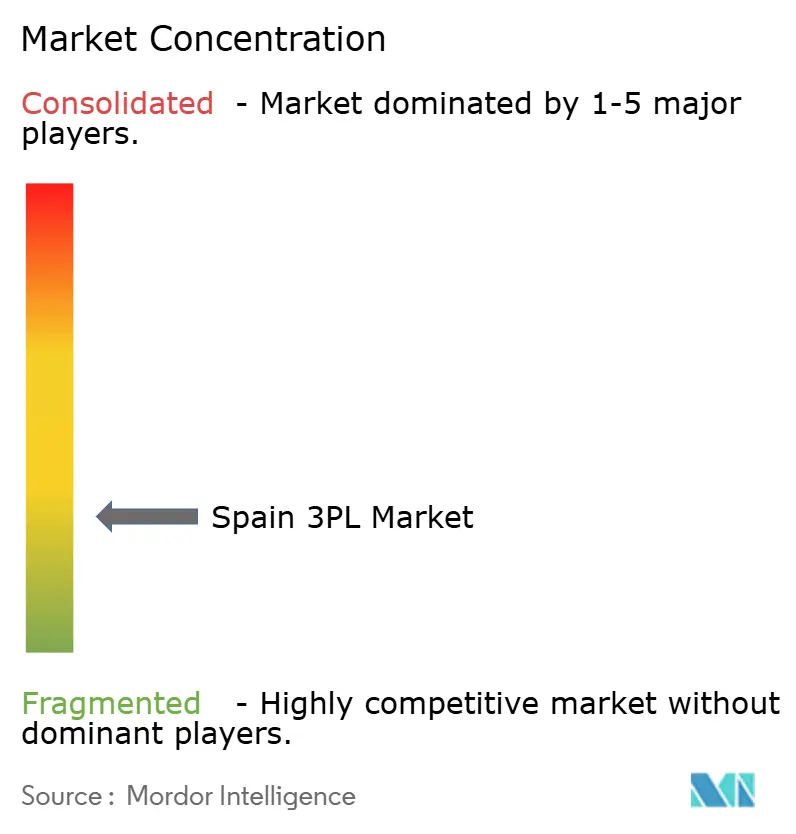

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spain 3PL Market Analysis by Mordor Intelligence

Spain third-party logistics market size stands at USD 14.46 billion in 2025 and is forecast to reach USD 17.62 billion by 2030, reflecting a 4.03% CAGR through the period. Spain’s role as a European gateway, the rapid shift toward outsourced fulfillment, and multimodal corridor upgrades underpin the upward trajectory. E-commerce’s geographic spread beyond Madrid and Barcelona, resilient nearshoring inflows from Northern Europe, and government-backed rail electrification projects jointly widen the addressable base for third-party logistics service providers. Digital tax incentives now reward AI-enabled route optimization while green-mobility policies raise demand for electric urban fleets. Heightened competition among domestic and multinational carriers accelerates pricing transparency and forces broader adoption of value-added warehousing, real-time visibility platforms, and asset-light alliances that de-risk capital exposure.

Key Report Takeaways

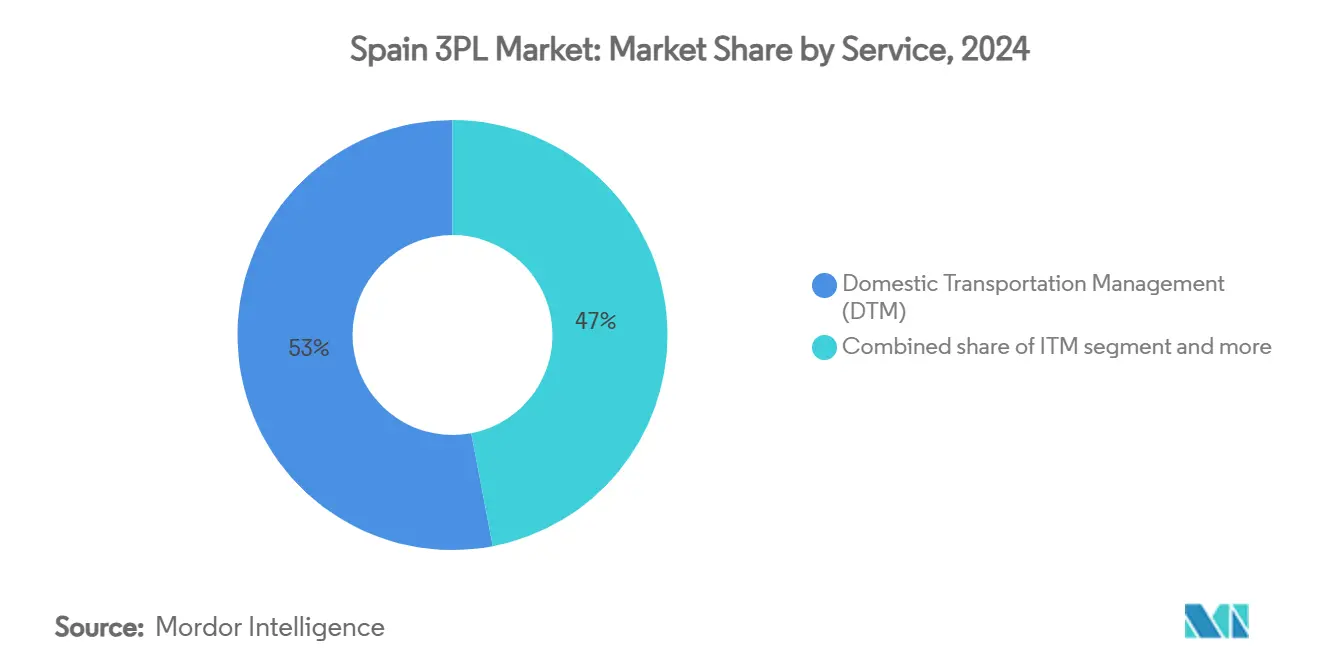

- By Service, Domestic Transportation Management held 53% of Spain third-party logistics market share in 2024, while Value-Added Warehousing & Distribution is projected to grow fastest at a 7.80% CAGR to 2030.

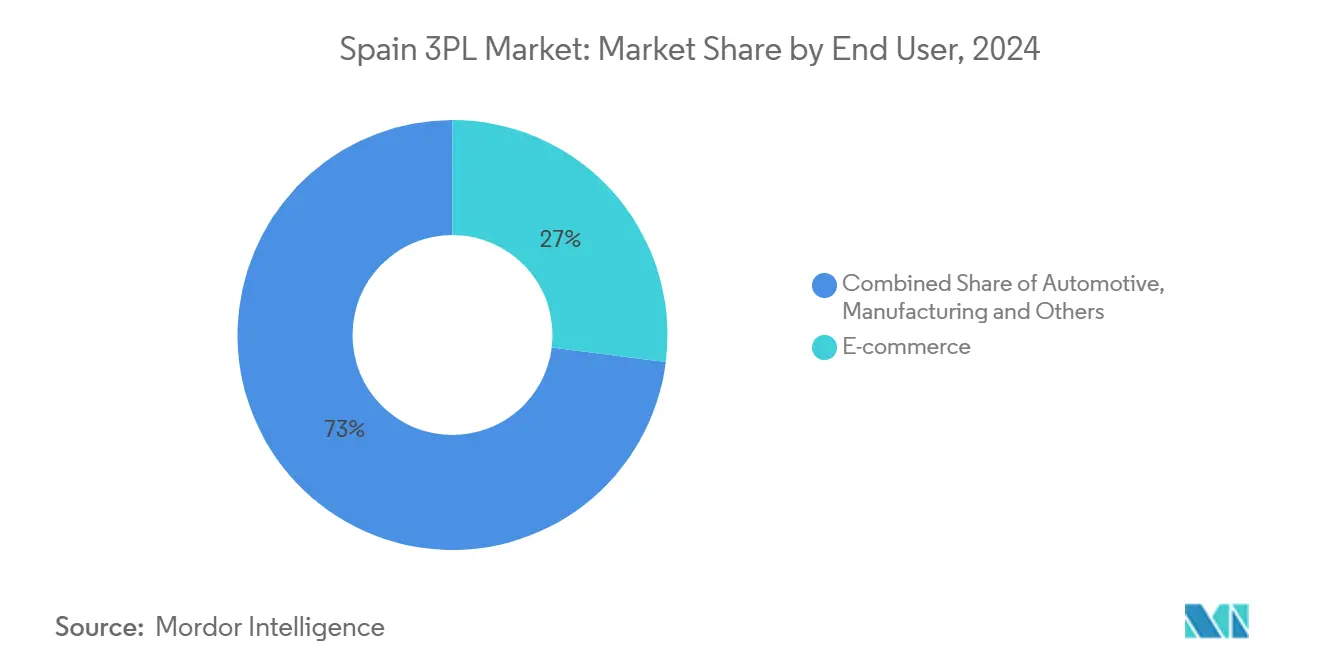

- By End User, E-commerce dominated with 27% revenue share in 2024; Food & Beverages is slated for the quickest expansion at 6.70% CAGR through 2030.

- By Logistic Model, Asset-Light providers retained 41% of Spain third-party logistics market share in 2024, yet Hybrid models are expected to rise at a 6.90% CAGR by 2030.

Spain 3PL Market Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce volumes requiring outsourced logistics services | +1.2% | National, with concentration in Madrid, Barcelona, Valencia | Short term (≤ 2 years) |

| Growing demand for temperature-controlled logistics for pharma & food | +0.8% | National, with emphasis on Mediterranean coastal regions | Medium term (2-4 years) |

| Government infrastructure investments in intermodal transport corridors | +0.6% | National, focusing on TEN-T corridors | Long term (≥ 4 years) |

| Nearshoring of European supply chains to Spain boosting warehousing demand | +0.9% | Northern Spain, Catalonia, Madrid logistics hubs | Medium term (2-4 years) |

| Rise of collaborative urban micro-hubs to meet zero-emission zones | +0.4% | Major metropolitan areas: Madrid, Barcelona, Valencia | Short term (≤ 2 years) |

| Digitization tax incentives spurring AI-enabled 3PL operations | +0.3% | National, with higher adoption in industrial regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce Volumes Requiring Outsourced Logistics Services

Spain’s online buyer base is expected to climb toward 40 million users in 2025, solidifying nationwide reliance on contracted fulfillment partners. Amazon’s USD 327 million logistics center in Asturias typifies the infrastructure scale now demanded by 48-hour delivery guarantees. Third-party providers respond with micro-fulfillment hubs that position inventory nearer to dense consumer pockets, a shift illustrated by studies showing Barcelona needs more than 1,000 such urban sites to meet current parcel volumes. Robotics-enabled sortation lines and AI-driven slotting solutions further compress fulfillment cycle times during peak shopping seasons. Greater delivery frequency, however, compels 3PLs to redesign trunk routes so that high-capacity trailers replenish urban depots overnight, mitigating daytime congestion costs[1]Martin Tokar, “Spain – E-Commerce,” U.S. Department of Commerce, trade.gov.

Growing Demand for Temperature-Controlled Logistics for Pharma & Food

Heightened vaccine distribution, stricter EU food-safety rules, and a switch to fresh consumer habits combine to lift Spain’s cold-chain utilization. Schmitz Cargobull’s acquisition of Spanish telematics firm Atlantis Global System demonstrates how trailer makers are embedding sensor networks to keep payload readings verifiable end-to-end. AI demand forecasting now underpins capacity planning so that refrigerated slots are allocated dynamically rather than by static contracts, preserving margins despite energy-price volatility. On the pharmaceutical side, compliance with Good Distribution Practice drives premium tariffs for GDP-certified storage zones, offering revenue defense in an otherwise price-competitive landscape. Emerging controlled-atmosphere chambers broaden produce export options, extending shelf life for Mediterranean perishables shipped northward. Blockchain pilots add immutable traceability, an essential feature as Spanish regulators intensify random cold-chain audits.

Government Infrastructure Investments in Intermodal Transport Corridors

Spain secured USD 263 million in Connecting Europe Facility grants devoted to rail electrification, port shore power, and digital freight platforms. Signature projects include USD 85 million for Zaragoza–Teruel–Sagunto rail upgrades and USD 45.8 million for harbor electrification at Barcelona, Valencia, and Gijón. These works shorten dwell times for containers transitioning from sea to land legs, a boon for Spain third-party logistics market operations seeking schedule reliability on Mediterranean and Atlantic corridors. Standardized loading protocols coupled with real-time consignment tracking will allow 3PLs to issue single multimodal invoices, cutting administrative overhead. Long-term rail competitiveness promises to draw bulk and FMCG shippers away from congested highways, freeing road capacity for high-velocity parcel traffic[2]Patricia Gutiérrez, “Spain Secures CEF Funding for Intermodal Corridors,” Ministerio de Transportes y Movilidad Sostenible, mitma.gob.es.

Nearshoring of European Supply Chains to Spain Boosting Warehousing Demand

Manufacturers re-position inventories closer to EU consumption zones, and Spain’s labor cost advantage over Northern Europe captures that pivot. Goldman Sachs-backed Newdock already exceeded its initial USD 1.09 billion Iberian budget to assemble a multi-country platform anchored in Madrid and Catalonia. Spain now counts 82.9 million m² of logistics parks across 279 sites, evidence of deep institutional capital inflows. Atitlan added a USD 109 million vehicle in Valencia to supply Class A warehouses that serve dual Iberian and Maghreb routes. Proximity to southern ports also hedges against Channel disruptions, underscoring Spain’s strategic appeal for diversified European sourcing models.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High diesel fuel prices increasing transport costs | -0.7% | National, with higher impact on long-haul routes | Short term (≤ 2 years) |

| Driver shortage and wage pressures | -0.9% | National, with acute shortages in industrial regions | Medium term (2-4 years) |

| Urban noise & emission regulations limiting night-time deliveries | -0.3% | Major metropolitan areas with zero-emission zones | Short term (≤ 2 years) |

| Rail network interoperability constraints reduce multimodal efficiency | -0.4% | Cross-border corridors, particularly Spain-France connections | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Diesel Fuel Prices Increasing Transport Costs

Fuel accounts for about one-quarter of total road freight expense, and 2025 volatility keeps margins thin despite statutory surcharge clauses. Madrid–Paris contract rates climbed 3.5% in Q4 2024 to USD 1,588 after currency conversion, illustrating the fragile rebound phase. Carriers resort to dynamic routes that weigh tolls, traffic, and refueling points so service-level agreements remain intact without blanket price hikes. Fleet owners test LNG and hybrid trucks on high-volume corridors, leveraging government subsidies to diversify energy exposure. Persistent variability nevertheless prompts shippers to explore rail for predictable budget planning, moderately dampening Spain third-party logistics market demand for long-haul trucking[3]Irene Nieto, “Weekly Fuel Price Report,” Ministerio de Transportes y Movilidad Sostenible, mitma.gob.es.

Driver Shortage and Wage Pressures

Only 3% of Spanish truck drivers are younger than 25, aggravating succession risk as 72% surpass the age of 50. Roughly 15,000 additional drivers are needed each year, yet restrictive licensing timelines and lifestyle concerns deter entrants. Wage inflation heats up as fleets outbid one another for scarce labor, especially on refrigerated and cross-border runs. 3PLs counter by elevating depot automation and experimenting with platooning trials that let one driver oversee multiple tractor-trailers on controlled stretches. Parallel efforts to recruit non-EU nationals progress slowly amid regulatory vetting, signaling a structural constraint for Spain third-party logistics market providers through mid-term horizons.

Segment Analysis

By Service: Value-Added Warehousing Gains Momentum

Domestic Transportation Management retained a 53% revenue slice in 2024, underscoring Spain’s highway-centric freight patterns and the enduring need for nationwide milk-run schedules. Spain third-party logistics market size for Value-Added Warehousing & Distribution is projected to expand at 7.80% CAGR, faster than any other service line. Rising e-commerce returns handling, customization, and kitting tasks push warehouse operators to embed automated sorters, pick-by-voice, and carton right-sizing machines. Meanwhile, International Transportation Management accelerates on the back of refurbished Mediterranean port capacity that funnels Maghreb trade into northern Spain depots. CEVA Logistics’ 18,000 m² Tarragona facility illustrates how sustainability add-ons—photovoltaic roofing and LED lighting—are now table stakes for contract awards.

The resurgence of freight rail, spurred by state electrification grants, sparks integrated service packages where truck drayage at origin and destination bookends a rail middle-haul. Air freight volumes, though minor by tonnage, yield attractive margins for life-science shippers demanding two-to-eight-degree routings. Bulk commodities funnel through coastal Ro-Ro and container terminals, yet many 3PLs cross-sell customs clearance and trade-finance documentation to lift yields above pure tonnage fees, as omnichannel retailers seek one-hour click-to-door delivery, micro-fulfillment add-ons inside legacy DCs proliferate, validating the premium placed on inventory proximity in Spain third-party logistics market contracts.

Note: Segment shares of all individual segments available upon report purchase

By End User: Cold-Chain Innovation Accelerates Food Flows

E-commerce preserved its 27% lead in 2024 thanks to an active online shopper community and high basket-repeat frequencies. Spain third-party logistics market size for Food & Beverages is forecast to ramp at 6.70% CAGR as temperature-controlled fleets migrate toward multi-compartment trucks capable of mixed-temperature drops. Pharmaceutical shippers prize 3PLs that hold GDP certificates and run redundant power sources, a niche that commands double-digit yield premiums. Automotive logistics steadies after chip shortages ease, while technology hardware flows increase as OEMs shift final assembly into Iberian plants. The life-sciences segment adds resilient baseline demand because Spain houses over 500 medicine production sites that export across Schengen borders.

Changing consumer appetite for fresh meal kits amplifies same-day cold-chain dispatches, requiring 3PLs to blend rapid cross-dock designs with traceability blockchains. Producers like Essity invested USD 26.2 million to co-locate manufacturing and warehousing, signaling tighter integration between plant yards and distribution docks. Renewable-energy equipment forms an outsize but cyclical flow that benefits from project-cargo specialists who handle blades, nacelles, and grid hardware. Overall, Spain third-party logistics market providers that master both sub-zero and ambient consolidation cycles secure longer contract tenures and higher switching costs.

Note: Segment shares of all individual segments available upon report purchase

By Logistics Model: Hybrid Networks Balance Flexibility and Control

Asset-Light specialists keep 41% of 2024 revenue, capitalizing on brokerage platforms and subcontracted fleets that scale demand swings without ballooning depreciation charges. Spain third-party logistics market size tied to Hybrid models is poised for a 6.90% CAGR through 2030, signaling a market pivot toward mixed ownership where key cross-docks and IT platforms remain proprietary, but middle-mile rigs are chartered. ID Logistics’ absorption of Logiters typifies this model: warehouse licenses stay in-house while transport legs rely on spot capacity. Asset-heavy portfolios persist where pharmaceutical, chemical, or ADR cargo mandates single-tenant warehouses, yet even these operators offload peak flows to aggregators during holiday surges.

Market participants stress that capital-light balance sheets attract lower financing costs and favor expansion into secondary cities where land acquisition remains affordable. Conversely, shippers increasingly request service-level guarantees that only owned facilities can assure, pushing providers toward hybrid footprints that fuse reliability with variable cost levers. Spain's third-party logistics market contracts now often include volume-triggered rate reviews, encouraging 3PLs to toggle between their own assets and spot hire according to demand patterns. Regulatory pushes for CO₂ tracking also influence model choice, since fleet ownership eases data capture for emissions audits.

Geography Analysis

Spain’s freight sector contributes 4.58% to GDP and supports more than 1 million jobs across 218,000 firms, anchoring the socio-economic importance of Spain third-party logistics market operations. Madrid and Catalonia form twin distribution poles, fusing airport cargo centers, inland terminals, and dense population catchments. Valencia’s port handles rising transshipment to Italy and North Africa, while Andalusia leverages Algeciras and Málaga to channel perishables outbound and manufacturing inputs inbound.

Basque Country logistics clusters pivot around automotive and steel verticals, complemented by an upgraded Atlantic corridor that trims door-to-door times into France. Galicia exploits Vigo and A Coruña ports for fishing exports, yet digital freight platforms now encourage small local fleets to access national contract pools. Aragón ascended rapidly after Amazon Web Services earmarked USD 17.17 billion for hyperscale data hubs that necessitate continuous server component deliveries and reverse logistics of retired hardware.

Overall, Spain's third-party logistics market providers distribute 33.5 million m² of warehouse stock, a 33% rise in three years, with Merlin Properties, Prologis, and Logicor jointly controlling roughly one-third of the supply. Ongoing rail interoperability projects around Irún should ease gauge-change delays, widening Basque cross-border opportunities by 2027. Structural incentives for zero-emission zones in Barcelona and Madrid fuel demand for short-haul electric vans, nudging network redesign toward spoke-and-hub micro-depots within city limits.

Competitive Landscape

Spain’s third-party logistics arena remains moderately fragmented, with no single carrier exceeding 10% of gross revenue. Multinationals such as DHL, GEODIS, and DSV square off against regionally entrenched groups like Grupo Sesé, Logista, and Azkar, creating brisk price discovery and continuous service refinement. Technology adoption acts as the decisive separator: DHL eCommerce’s pact with CTT Expresso targets USD 1.09 billion of Iberian parcel revenue, combining API-enabled label generation with shared last-mile rounds.

GEODIS expanded reverse-logistics capabilities at Torija to cater to omnichannel fashion, reducing carbon impact through circular inventory flows. DSV emphasizes control tower solutions that stream IoT telemetry into predictive ETA dashboards, attracting automotive clients seeking synchronized inbound flows. Domestic mid-caps respond by forging vertical specializations—pharma, temperature-sensitive groceries, or project cargo—to secure defensible niches where scale alone offers limited advantage.

Institutional investors accelerate consolidation by backing platform plays; for instance, Brookfield and Prologis vie for brownfield conversions around Zaragoza and Seville. Yet the entrance barrier for brokerage-first entrants remains low, perpetuating a long tail of micro-fleets that haul under white-label contracts. Spain third-party logistics market participants that blend automation, ESG compliance, and near real-time cost transparency earn preferential spots on multi-year tenders, nudging the field toward gradual—but not rapid—concentration.

Spain 3PL Industry Leaders

-

Carcaba

-

CEVA Logistics

-

DSV

-

FM Logistic

-

Groupe CAT

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DHL earmarked USD 2 billion for “DHL Health Logistics” to scale life-science and healthcare services, expanding GDP-certified capacity nationwide.

- March 2025: Templus, backed by ICG and Teras Capital, announced a USD 327 million program to build 20 Spanish data centers by 2025, spurring ancillary logistics demand for high-value IT hardware.

- December 2024: DHL eCommerce and CTT Expresso revealed a partnership to manage over 1 million parcels daily across Iberia, pending antitrust clearance.

- May 2024: Amazon Web Services confirmed USD 17.17 billion investment in Aragón infrastructure through 2034, with the first five sites operational in 2025.

Spain 3PL Market Report Scope

A 3PL (third-party logistics) provider offers outsourced logistics services, encompassing anything that involves managing one or more facets of procurement and fulfillment activities.

The Spain Third Party Logistics (3PL) Market is segmented by service (domestic transportation management, international transportation management, and value-added warehousing and distribution) and end-user (manufacturing & automotive, oil & gas and chemicals, distributive trade (wholesale and retail trade including e-commerce), pharma & healthcare, construction, and other end users). The report offers market size and forecasts for the Spain Third Party Logistics (3PL) Market in Value (USD) for all the above segments.

By Service

| Domestic Transportation Management (DTM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| International Transportation Management (ITM) | Roadways |

| Railways | |

| Airways | |

| Waterways | |

| Value-Added Warehousing & Distribution (VAWD) |

By End User

| Automotive |

| Energy & Utilities |

| Manufacturing |

| Life Sciences & Healthcare |

| Technology & Electronics |

| E-commerce |

| Consumer Goods & FMCG |

| Food & Beverages |

| Others |

By Logistics Model

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet & Warehouses) |

| Hybrid |

| By Service | Domestic Transportation Management (DTM) | Roadways |

| Railways | ||

| Airways | ||

| Waterways | ||

| International Transportation Management (ITM) | Roadways | |

| Railways | ||

| Airways | ||

| Waterways | ||

| Value-Added Warehousing & Distribution (VAWD) | ||

| By End User | Automotive | |

| Energy & Utilities | ||

| Manufacturing | ||

| Life Sciences & Healthcare | ||

| Technology & Electronics | ||

| E-commerce | ||

| Consumer Goods & FMCG | ||

| Food & Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet & Warehouses) | ||

| Hybrid | ||

Key Questions Answered in the Report

What is the projected value of Spain’s third-party logistics market in 2030?

The market is expected to reach USD 17.62 billion by 2030, reflecting a 4.03% CAGR.

Which service segment is expanding the fastest in Spanish 3PL?

Value-Added Warehousing & Distribution is forecast to grow at a 7.80% CAGR through 2030.

Why is food and beverage logistics gaining momentum?

Rising demand for temperature-controlled deliveries and fresh grocery e-commerce drives a 6.70% CAGR in this vertical.

How are infrastructure upgrades influencing logistics in Spain?

USD 263 million in EU grants for rail and port electrification lowers transit times and boosts multimodal reliability.

What labor issue poses a risk to Spanish freight operators?

A severe driver shortage, with 72% of truckers older than 50, elevates wage pressures and threatens capacity.

Which logistics model is becoming more popular?

Hybrid approaches that blend owned depots with subcontracted fleets are projected to rise at a 6.90% CAGR.

Page last updated on: