Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

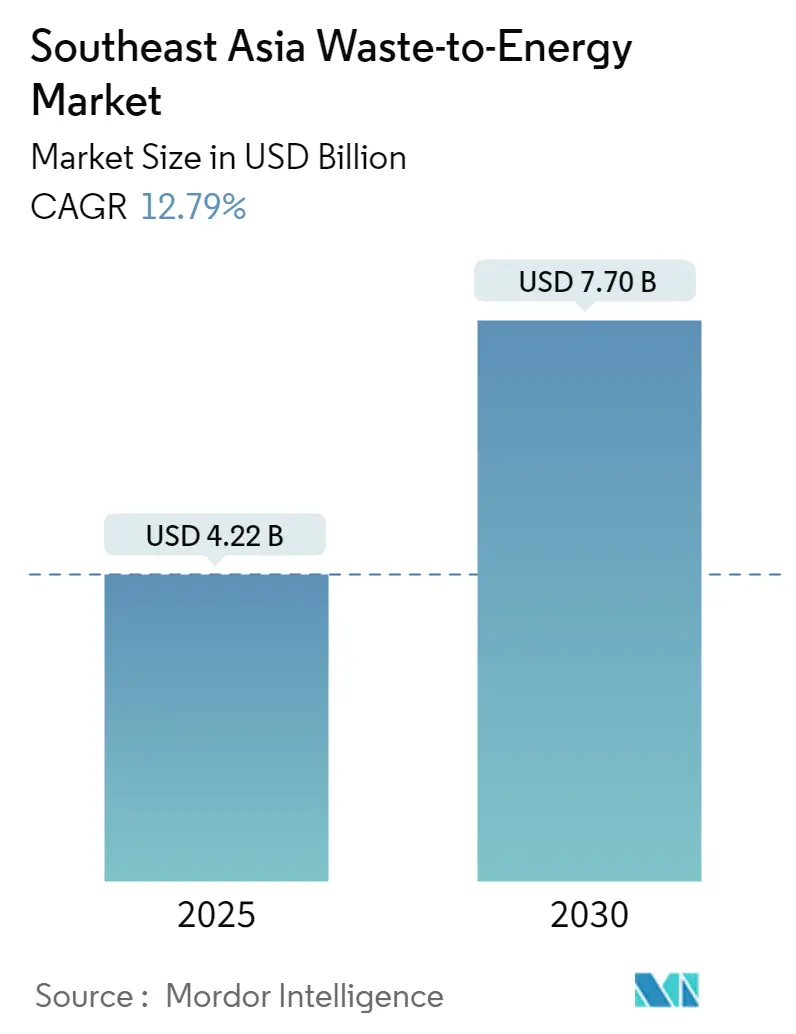

| Market Size (2025) | USD 4.22 Billion |

| Market Size (2030) | USD 7.70 Billion |

| Growth Rate (2025 - 2030) | 12.79% CAGR |

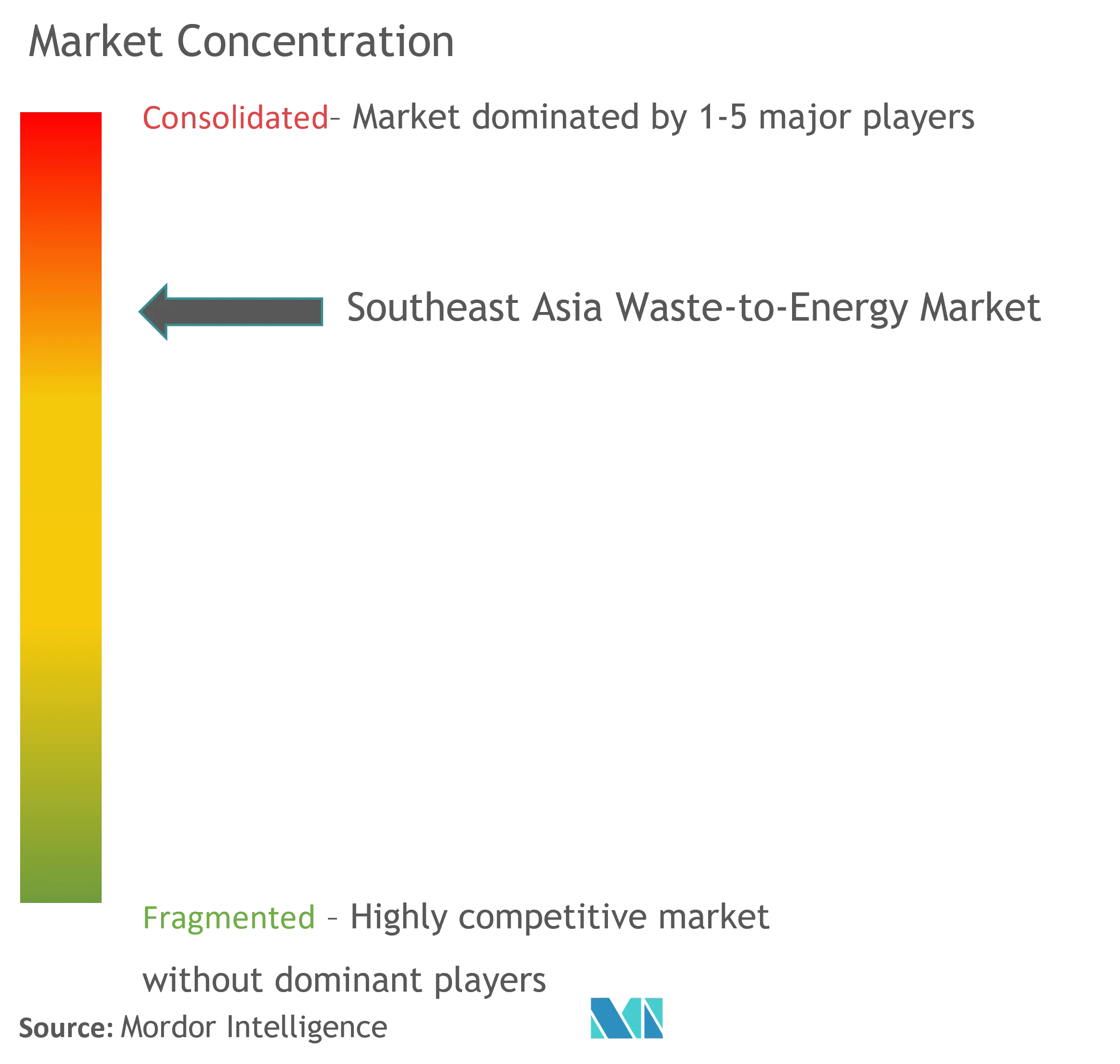

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Waste-to-Energy Market Analysis by Mordor Intelligence

The Southeast Asia Waste-to-Energy Market size is estimated at USD 4.22 billion in 2025, and is expected to reach USD 7.70 billion by 2030, at a CAGR of 12.79% during the forecast period (2025-2030).

The Southeast Asian waste-to-energy sector is experiencing significant transformation driven by rapid urbanization and industrialization across the region. Countries are increasingly adopting comprehensive waste management strategies to address growing environmental concerns while simultaneously meeting their energy needs. Vietnam, as a prime example, anticipates power consumption to grow between 10-12% annually through 2030, highlighting the urgent need for renewable waste energy sources. This surge in energy demand, coupled with limited landfill capacity and environmental concerns, has prompted governments across the region to accelerate their waste-to-energy initiatives.

Technological advancement and innovation are reshaping the industry landscape, with emerging solutions like Dendro Liquid Energy (DLE) gaining prominence. This waste treatment technology demonstrates remarkable efficiency, generating four times more electricity compared to conventional methods while maintaining zero emissions and eliminating effluent problems at plant sites. The integration of such advanced technologies is transforming waste management facilities into sophisticated energy generation centers, capable of processing diverse waste streams while minimizing environmental impact.

Policy frameworks and government initiatives are playing a pivotal role in market development. Thailand's Alternative Energy Development Plan exemplifies this commitment, targeting 3,600 MW of biogas utilization. Similarly, Indonesia has implemented presidential regulations to accelerate waste-to-energy project development across major cities, while Malaysia's Ministry of Housing and Local Government has announced plans to establish six waste-to-energy plants by 2025. These policy initiatives are complemented by attractive feed-in tariffs and investment incentives, creating a favorable environment for market growth.

The market is witnessing substantial project developments and investments across the region. In Singapore, the development of the Tuas Nexus Integrated Waste Management Facility represents a significant milestone, with an investment exceeding USD 1.5 billion. The facility, scheduled for completion in 2024, will feature a 2,900 tons per day waste-to-energy facility and a 250 tons per day materials recovery facility. Similarly, Vietnam has approved multiple large-scale projects, including waste-to-energy facilities in Ho Chi Minh City Municipality capable of processing up to 9,300 TPD, demonstrating the region's commitment to sustainable waste management solutions.

Southeast Asia Waste-to-Energy Market Trends and Insights

Growing Waste Generation and Urbanization

The rapid urbanization across Southeast Asia has created an unprecedented surge in waste management, making it one of the most critical drivers for the waste-to-energy market. The region is experiencing one of the fastest-growing urban population rates globally, with most countries generating predominantly organic waste, accounting for approximately 50% or more of total waste generation across all countries except Singapore. This significant proportion of organic waste presents an ideal opportunity for waste valorization and waste recycling, particularly through technologies like anaerobic digestion and thermal treatment methods.

The increasing waste management challenges have prompted various initiatives across the region. For instance, in January 2023, Harvest Waste from the Netherlands initiated studies for a thermal waste-to-energy project in Vietnam's Mekong Delta province of Soc Trang, with an estimated investment of USD 100 million. Similarly, in May 2023, the Melaka state government in Malaysia expedited the construction of their Waste-to-Energy plant at the Sungai Udang Sanitary Solid Waste Disposal Site, advancing the completion date from 2026 to 2024, demonstrating the urgent need to address growing waste management challenges.

Understand The Key Trends Shaping This Market

Download PDF

Supportive Government Policies and Regulatory Framework

Government support through favorable policies and regulatory frameworks has emerged as a crucial driver for the waste-to-energy market across Southeast Asia. Various countries have implemented attractive incentive schemes to encourage investment in waste-to-energy projects. For instance, Vietnam has established one of the region's most competitive feed-in tariffs for power generation from solid waste, offering USD 0.1005 per kWh for direct burning and USD 0.0728 per kWh for burning gases from landfills. These rates are notably higher than those offered for other renewable energy sources like wind and solar power, demonstrating the government's commitment to promoting waste-to-energy solutions.

The regulatory support extends beyond just financial incentives. Countries across the region offer comprehensive support packages including tax holidays, import duty exemptions for equipment, land rent exemptions, and access to low-interest loans. Malaysia, for example, has implemented a robust framework combining feed-in tariffs with investment tax allowances and the Small Renewable Energy Programme (SREP), which allows renewable projects with up to 10 MW capacity to sell their electricity output to the government under 21-year license agreements. These supportive policies have created a conducive environment for both domestic and international investors to participate in the waste-to-energy sector.

Rising Energy Demand and Need for Sustainable Sources

The escalating energy demand across Southeast Asia has become a significant driver for the waste-to-energy market, as countries seek to diversify their energy sources while addressing environmental concerns. Thailand, for instance, witnessed an electricity consumption growth of more than 3% between 2021 and 2022, highlighting the region's growing energy needs. This increasing demand, coupled with the push for sustainable energy solutions, has positioned waste-to-energy as a viable option for both waste management and energy generation.

The transition toward renewable energy sources has gained significant momentum across the region. In Malaysia, the total renewable energy installed capacity reached 9,044 MW in 2022, demonstrating a remarkable growth rate exceeding 20% between 2018 and 2022. This growth trajectory aligns with various national renewable energy targets and sustainability goals across Southeast Asian countries. Waste-to-energy technologies are particularly attractive as they offer a dual benefit - addressing waste management challenges while contributing to the renewable energy mix, making them an integral part of the region's sustainable development strategy. The integration of biogas and bioenergy solutions further enhances the potential of waste recycling and alternative fuel sources, supporting the region's commitment to sustainable energy.

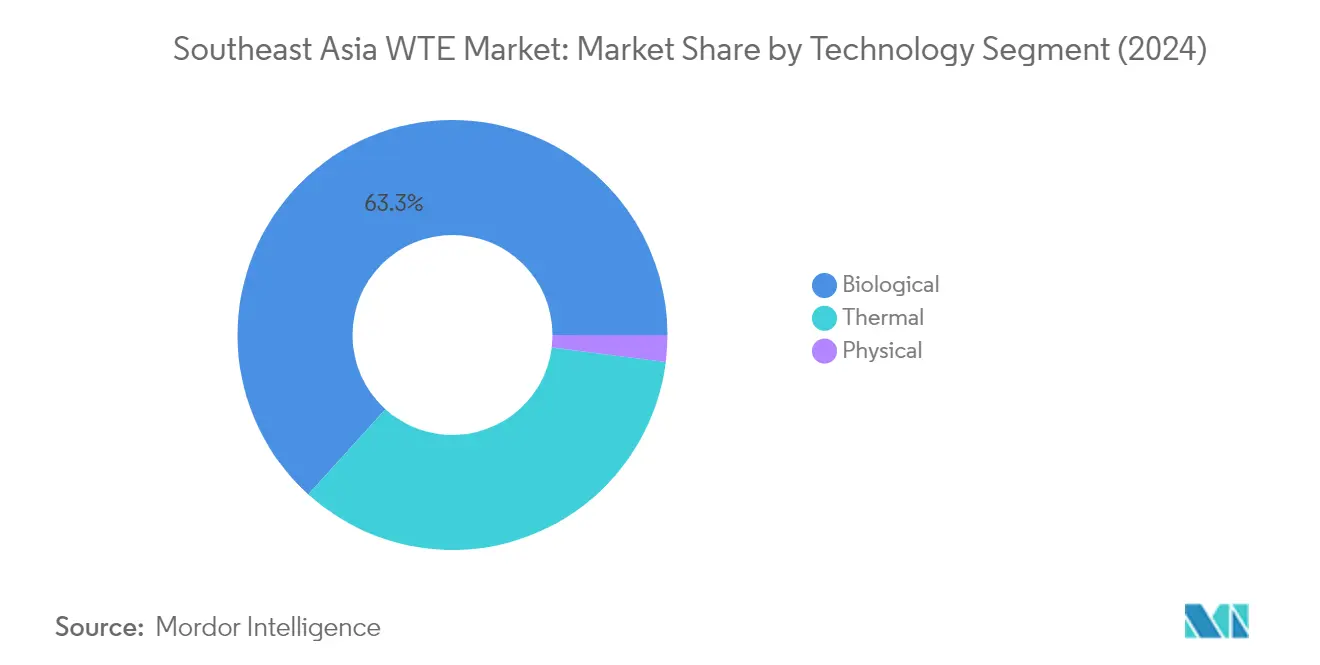

Segment Analysis: Technology

Biological Segment in Southeast Asia WTE Market

The biological segment has emerged as the dominant force in the Southeast Asia waste-to-energy market, commanding approximately 63% of the market share in 2024. This segment's prominence can be attributed to the increasing developments and upcoming projects in biological WTE facilities across the region, particularly in countries like Malaysia, Thailand, and Vietnam. The segment's growth is primarily driven by its advantages over traditional waste incineration methods, including lower environmental impact and better handling of organic waste. The biological treatment method effectively uses microbes to produce fuel from waste, particularly organic waste, through processes like fermentation and biogas formation. Government support through feed-in tariffs and other incentives, especially in countries like Malaysia and Thailand, has further strengthened this segment's position in the market.

Remaining Segments in Technology Segmentation

The thermal and physical segments complete the technology landscape in the Southeast Asia waste-to-energy market. The thermal segment, which includes technologies like waste incineration, co-processing, and waste pyrolysis/waste gasification, plays a crucial role in waste volume reduction and energy generation, particularly in densely populated urban areas. Singapore, for instance, has successfully implemented several thermal WTE facilities to address its waste management challenges. The physical segment, while smaller in market share, focuses on improving the physical and chemical properties of solid waste through processes like refuse-derived fuel (RDF) production. This segment is gaining traction in countries like Indonesia and Thailand, where governments are promoting RDF facilities to address specific waste management needs and reduce dependency on traditional disposal methods.

Southeast Asia Waste-to-Energy Market Geography Segment Analysis

Waste-to-Energy Market in Singapore

Singapore stands as the dominant force in Southeast Asia's waste-to-energy market, commanding approximately 25% of the regional market share in 2024. The country's advanced waste management infrastructure and stringent environmental regulations have positioned it as a leader in waste-to-energy technology adoption. Singapore's commitment to sustainable waste management is exemplified by its integrated waste management facilities, which combine multiple waste treatment technologies to maximize energy recovery. The country's approach to waste-to-energy is particularly noteworthy for its focus on thermal treatment technologies, which have proven highly efficient in reducing waste volume while generating substantial amounts of renewable energy. The government's proactive stance in implementing advanced waste treatment solutions, coupled with significant investments in infrastructure development, has created a robust ecosystem for waste-to-energy projects. The presence of major industry players and continuous technological innovations has further strengthened Singapore's position in the market. The country's success in waste-to-energy implementation serves as a model for other Southeast Asian nations seeking to develop similar capabilities.

Waste-to-Energy Market in Indonesia

Indonesia emerges as the most dynamic market in the region, with projections indicating a remarkable growth rate of approximately 23% during the forecast period 2024-2029. The country's rapid urbanization and increasing waste generation have created significant opportunities for waste-to-energy development. Indonesia's government has implemented comprehensive policies and incentives to attract investments in the sector, including feed-in tariffs and tax benefits for waste-to-energy projects. The country's approach to waste-to-energy development is particularly notable for its focus on both thermal and biological waste treatment technologies, allowing for diverse waste treatment solutions. The government's commitment to reducing landfill dependency and increasing renewable energy generation has led to the development of numerous waste-to-energy facilities across major cities. The market's growth is further supported by strong private sector participation and international collaborations in project development. The country's vast geographical spread and growing urban population continue to drive the expansion of waste-to-energy infrastructure, making it an increasingly attractive market for investors and technology providers.

Waste-to-Energy Market in Thailand

Thailand has established itself as a key player in Southeast Asia's waste-to-energy sector, driven by its comprehensive renewable energy development plans and supportive regulatory framework. The country's approach to waste-to-energy development is characterized by a balanced mix of technologies, including both thermal and biological treatment methods. Thailand's success in the sector is underpinned by its well-developed waste collection infrastructure and strong government support for renewable energy projects. The country has implemented various initiatives to promote waste-to-energy development, including attractive feed-in tariffs and investment incentives. The market's growth is further supported by increasing environmental awareness and the need for sustainable waste management solutions in urban areas. Thailand's waste-to-energy sector benefits from strong private sector participation and technological expertise, with numerous international companies actively involved in project development. The government's commitment to increasing renewable energy capacity and reducing dependence on fossil fuels continues to drive market expansion.

Waste-to-Energy Market in Malaysia

Malaysia has emerged as a significant player in the Southeast Asian waste-to-energy market, driven by its strong commitment to sustainable waste management and renewable energy development. The country's approach to waste-to-energy is characterized by a focus on innovative technologies and efficient waste treatment solutions. Malaysia's market development is supported by comprehensive government policies promoting renewable energy and environmental sustainability. The country has successfully attracted both domestic and international investments in waste-to-energy projects through various incentive schemes and supportive regulations. The market's growth is further enhanced by increasing urbanization and the need for efficient waste management solutions in major cities. Malaysia's waste-to-energy sector benefits from strong technological capabilities and a well-developed infrastructure network. The government's emphasis on circular economy principles and sustainable development continues to create new opportunities for market expansion.

Waste-to-Energy Market in Other Countries

The waste-to-energy market in other Southeast Asian countries, including Vietnam, the Philippines, Myanmar, Cambodia, Laos, and Brunei, demonstrates varying levels of development and potential. These markets are characterized by increasing awareness of sustainable waste management practices and growing interest in renewable energy solutions. While some countries are in the early stages of market development, others are rapidly advancing their waste-to-energy capabilities through government initiatives and international partnerships. The development of waste-to-energy infrastructure in these countries is driven by factors such as urbanization, environmental concerns, and the need for sustainable energy sources. Many of these markets are experiencing growing interest from international investors and technology providers, particularly in countries with supportive regulatory frameworks and investment incentives. The future development of these markets will likely be influenced by factors such as government policies, technological advancement, and access to financing.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Top Companies in Southeast Asia Waste-to-Energy Market

The Southeast Asian waste-to-energy market features prominent players like Mitsubishi Heavy Industries, Keppel Corporation, Welle Environmental Group, Veolia Environment, Hitachi Zosen, China Everbright Environment Group, Martin GmbH, and Babcock & Wilcox Volund. These companies are actively pursuing technological innovations in areas such as automated operations, predictive maintenance, and AI-driven plant optimization to enhance operational efficiency. Strategic partnerships and joint ventures, particularly between local and international players, have become increasingly common to leverage complementary strengths and expand market presence. Companies are focusing on developing comprehensive end-to-end solutions, from waste management to energy recovery, while also investing in research and development for more efficient waste treatment technology. The market has seen a significant trend towards digital transformation, with companies implementing smart monitoring systems and integrated waste management platforms to improve plant performance and reduce operational costs.

Market Dominated by Strategic Partnerships and Integration

The Southeast Asian waste-to-energy market exhibits a mix of global conglomerates and regional specialists, with international players often partnering with local entities to navigate market-specific challenges and regulatory requirements. The market structure is characterized by a moderate level of consolidation, with major players like Keppel Seghers and Mitsubishi Heavy Industries maintaining strong positions through their established presence and technological expertise. The competitive landscape is increasingly shaped by public-private partnerships, particularly in countries like Singapore and Thailand, where government initiatives play a crucial role in market development.

The market has witnessed significant merger and acquisition activity, with companies like Keppel Seghers acquiring stakes in specialized firms to enhance their technological capabilities and service offerings. Joint ventures have become a preferred mode of market entry and expansion, as demonstrated by collaborations between companies like PT Jakarta Propertindo and Fortum. These strategic alliances are not only facilitating technology transfer but also helping companies share project risks and leverage local market knowledge while maintaining competitive advantages in their respective areas of expertise.

Innovation and Localization Drive Future Success

For established players to maintain and expand their market share, a multi-faceted approach combining technological innovation, local market understanding, and operational excellence is essential. Companies need to focus on developing cost-effective solutions that address specific regional waste management challenges while meeting increasingly stringent environmental regulations. Building strong relationships with local authorities and waste management agencies has become crucial, as government support and policy alignment significantly influence project success. The ability to offer flexible financing models and demonstrate successful track records in similar markets is becoming increasingly important for maintaining competitive advantage.

New entrants and challenger companies can gain ground by focusing on niche market segments or specific technological solutions that address unmet needs in the waste-to-energy value chain. Success factors include developing innovative business models that can overcome the high capital requirements typical of the industry, while also building strong local partnerships to navigate regulatory frameworks and secure project approvals. Companies must also consider the increasing emphasis on environmental sustainability and circular economy principles, as these factors significantly influence customer preferences and regulatory requirements. The ability to demonstrate clear environmental benefits and social value creation will become increasingly important for both incumbents and new entrants in securing new projects and maintaining market position. Additionally, focusing on waste valorization can provide a competitive edge by turning waste into valuable resources.

Southeast Asia Waste-to-Energy Industry Leaders

Mitsubishi Heavy Industries Ltd

Keppel Corporation

PT Yokogawa Indonesia

Veolia Environment SA

Hitachi Zosen Corp

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2023: The Thailand Board of Investment (BOI) approved an investment for promoting applications worth a combined USD 1.1 billion in projects, including the manufacturing of electric vehicles (EV), the generation of renewable energy from waste, data centers, and travel and tourism infrastructure and equipment. Further, C&G Environmental Protection (Thailand) Co., Ltd. received approval for a USD 0.13 billion investment in a 35-megawatt power generation project that will produce electricity from waste. The facility will be located in the area of the Nong Khaem Solid Waste Disposal Center in Bangkok.

- September 2022: PT Jakarta Propertindo (Jakpro), a city-owned developer, announced that the construction of Jakarta's inaugural waste-to-energy incinerator in Sunter, North Jakarta, will begin by the end of 2022.

Southeast Asia Waste-to-Energy Market Report Scope

Waste-to-energy (WtE) refers to converting various waste materials into usable forms of energy, such as electricity, heat, or fuel. It involves the application of different technologies to extract energy from waste, thereby reducing the volume of waste that needs to be landfilled or incinerated. The most common waste materials used in waste-to-energy processes include municipal solid waste (MSW), biomass, agricultural residues, industrial waste, and wastewater sludge. These waste materials are typically rich in organic content, which can be harnessed for energy generation.

The Southeast Asia Waste-to-Energy Market is segmented by technology and geography. By technology, the market is segmented into physical, thermal, and biological. The report also covers the market size and forecasts for the Southeast Asia Waste-to-Energy market across the major countries in the region. Each segment's market sizing and forecasts are based on revenue (USD).

Technology

| Physical | |

| Thermal | Incineration |

| Co-processing | |

| Pyrolysis/gasification | |

| Biological | Anaerobic Digestion |

Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}

| Malaysia |

| Indonesia |

| Thailand |

| Singapore |

| Vietnam |

| Rest of Southeast Asia |

| Technology | Physical | |

| Thermal | Incineration | |

| Co-processing | ||

| Pyrolysis/gasification | ||

| Biological | Anaerobic Digestion | |

| Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)} | Malaysia | |

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Vietnam | ||

| Rest of Southeast Asia | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Southeast Asia Waste-to-Energy Market?

The Southeast Asia Waste-to-Energy Market size is expected to reach USD 4.22 billion in 2025 and grow at a CAGR of 12.79% to reach USD 7.70 billion by 2030.

What is the current Southeast Asia Waste-to-Energy Market size?

In 2025, the Southeast Asia Waste-to-Energy Market size is expected to reach USD 4.22 billion.

Who are the key players in Southeast Asia Waste-to-Energy Market?

Mitsubishi Heavy Industries Ltd, Keppel Corporation, PT Yokogawa Indonesia, Veolia Environment SA and Hitachi Zosen Corp are the major companies operating in the Southeast Asia Waste-to-Energy Market.

What years does this Southeast Asia Waste-to-Energy Market cover, and what was the market size in 2024?

In 2024, the Southeast Asia Waste-to-Energy Market size was estimated at USD 3.68 billion. The report covers the Southeast Asia Waste-to-Energy Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Southeast Asia Waste-to-Energy Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.