Market Overview

| Study Period | 2021 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2021 - 2023 |

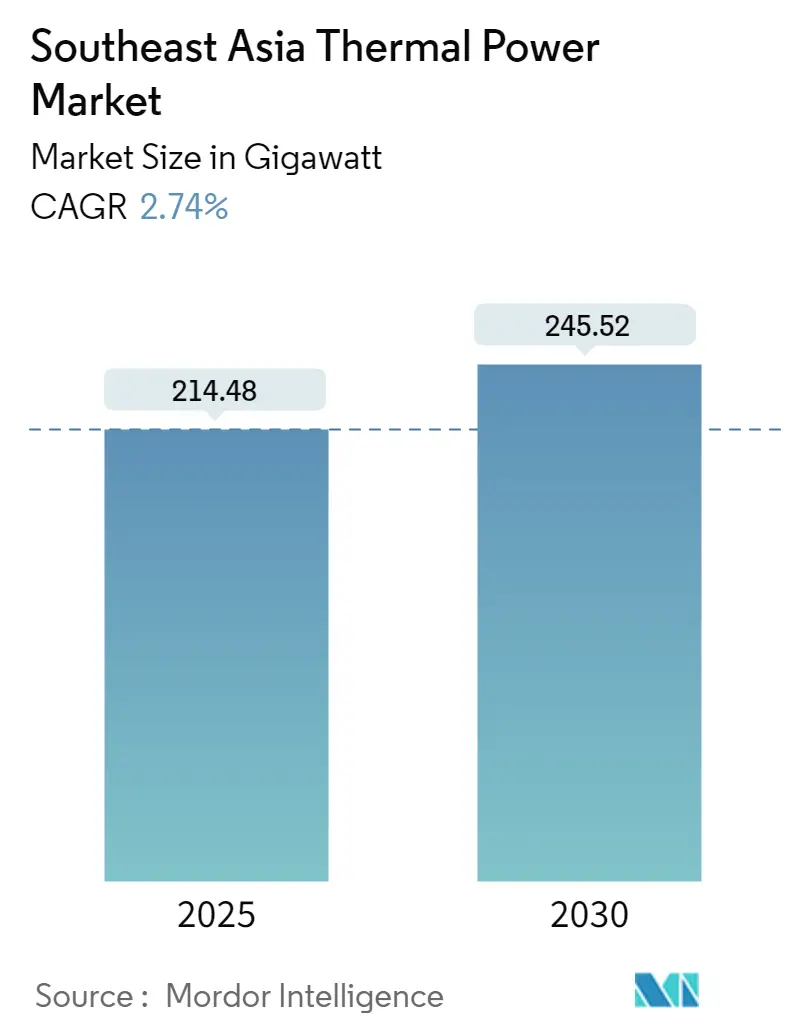

| Market Volume (2025) | 214.48 gigawatt |

| Market Volume (2030) | 245.52 gigawatt |

| Growth Rate (2025 - 2030) | 2.74% CAGR |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Southeast Asia Thermal Power Market Analysis by Mordor Intelligence

The Southeast Asia Thermal Power Market size is estimated at 214.48 gigawatt in 2025, and is expected to reach 245.52 gigawatt by 2030, at a CAGR of 2.74% during the forecast period (2025-2030).

The Southeast Asian thermal power landscape is undergoing a significant transformation driven by evolving energy policies and environmental commitments. Countries across the region are actively restructuring their energy portfolios, with a notable shift towards cleaner thermal power sources. This transition is particularly evident in the power generation sector, where, according to the Gas Exporting Countries Forum (GECF), gas-fired capacity is projected to reach approximately 200 GW by 2050. The region's commitment to environmental sustainability is reflected in recent policy decisions, with major economies like Indonesia and Vietnam pledging to phase out coal-based thermal power generation by the 2040s.

The natural gas sector is emerging as a cornerstone of Southeast Asia's energy transition strategy, driven by its lower environmental impact compared to traditional fossil fuel power sources. Industry forecasts indicate that gas-fired generation is expected to contribute to 30% of the increase in electricity supply by 2050, marking a significant shift in the region's energy mix. This transformation is supported by extensive infrastructure development, including new LNG terminals and processing facilities across multiple countries. The expansion of natural gas infrastructure is particularly notable in countries like Vietnam, where plans are underway to increase the gas-to-power ratio to over 28-30% by 2045.

The region's power demand dynamics are experiencing substantial evolution, shaped by rapid industrialization and urbanization. Current projections indicate that electricity demand in Southeast Asia is expected to reach 2,690 terawatt-hours (TWh) by 2050, necessitating significant investments in thermal power plant infrastructure. This growth trajectory is driving the development of more efficient and environmentally conscious thermal power facilities, particularly in major economies like Indonesia, Vietnam, Thailand, and the Philippines, which are expected to lead in electricity consumption.

The thermal power sector is witnessing significant technological advancements, particularly in combined cycle power gas turbine (CCGT) technology and clean coal technologies. These developments are accompanied by substantial investments in natural gas infrastructure, with projections indicating that natural gas demand in ASEAN countries' power sector will increase by approximately 110 billion cubic meters over the next three decades, reaching 200 bcm by 2050. This technological evolution is complemented by the development of new LNG terminals and processing facilities, enhancing the region's capacity to utilize cleaner thermal energy sources efficiently.

Southeast Asia Thermal Power Market Trends and Insights

Rising Power Demand and Industrial Growth

The rapid industrialization and urbanization across Southeast Asia have led to a substantial increase in electricity demand, serving as a primary driver for the thermal power market. The region has witnessed one of the fastest-growing electricity demand rates globally, with thermal power generation increasing by approximately 6% annually over the last two decades. This surge in demand is primarily attributed to the growing ownership of household appliances, air conditioners, and the increasing consumption of goods and services across the urban centers of Southeast Asia.

The industrial sector's expansion has particularly intensified the need for reliable baseload power generation, which thermal power plants effectively provide. For instance, Vietnam's electricity generation witnessed remarkable growth from 26.6 TWh in 2000 to 234.5 TWh in 2020, highlighting the massive scale of power demand growth in the region. This trend continues as Southeast Asia's electricity consumption is projected to more than double to 961 terawatt-hours by 2040, driven by significant demographic and economic growth, necessitating substantial investments in thermal power infrastructure to ensure a stable power supply.

Understand The Key Trends Shaping This Market

Download PDF

Abundant Coal Reserves and Cost Advantages

The availability of substantial coal reserves in the region, particularly in Indonesia, which possesses 34.87 billion tons of coal reserves—the highest in Southeast Asia—continues to drive the thermal power market. The economic advantage of coal-based power generation, coupled with well-established infrastructure and expertise in operating coal-fired plants, makes it an attractive option for meeting the region's growing energy demands. This is evidenced by ongoing programs such as Indonesia's initiative to add 35 GW of coal-fired power plants to its national grid, supplemented by an additional 7 GW of coal power projects.

The cost-effectiveness of coal-based generation, particularly in comparison to alternative power sources, remains a significant driver for thermal power development in the region. The existing grid infrastructure has been optimized for coal-based thermal power plants, making it economically viable to continue utilizing this resource. Furthermore, the ease of handling and transportation of coal compared to natural gas or oil, combined with the region's extensive experience in operating coal-fired facilities, contributes to its continued dominance in the power generation mix.

Development of Natural Gas Infrastructure

The expanding natural gas infrastructure across Southeast Asia is emerging as a crucial driver for the thermal power market, particularly as countries seek to transition toward cleaner energy sources. The region has witnessed significant developments in LNG infrastructure, with nine LNG receiving terminals operating across five ASEAN countries, boasting a total capacity of 38.75 million metric tons per annum (MTPA). Additionally, three new LNG liquefaction trains under construction are expected to add a net liquefaction capacity of 5.8 MTPA, strengthening the region's capability to utilize natural gas for power generation.

The discovery and development of new gas fields are further propelling the growth of gas-based thermal power generation. Notable developments include Vietnam's Ca Voi Xanh gas project, which holds estimated reserves of 150 billion cubic meters, and Indonesia's Natuna D Alpha gas field with approximately 200 trillion cubic feet of natural gas content. These resources, coupled with the construction of new gas-fired power plants such as the 500-megawatt Muara Karang Power Plant in Indonesia, demonstrate the region's commitment to expanding its gas-based power generation capacity. The development of LNG-to-power projects, including Vietnam's planned 1.5 GW LNG-to-power plant in the Quang Tri province, further illustrates the growing importance of natural gas infrastructure in driving the thermal power market.

Segment Analysis: Cycle

Closed Cycle Segment in Southeast Asia Thermal Power Market

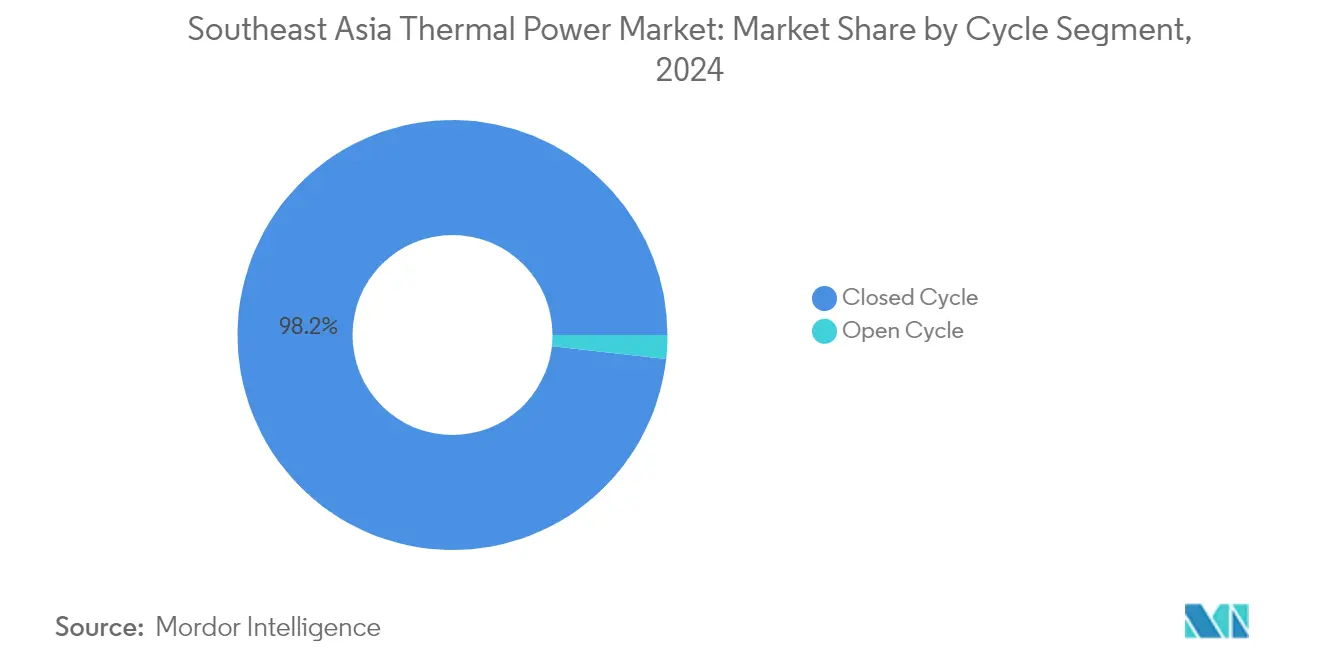

The closed cycle segment dominates the Southeast Asia thermal power market, accounting for approximately 98% of the total market share in 2024. This dominance is attributed to the segment's superior thermal efficiency (56-60%) and better part-load performance compared to open cycle systems. Closed cycle systems are particularly favored for new power plant installations due to their ability to achieve higher energy output through heat recovery systems and thermal power turbine steam turbines. The technology's growing adoption is driven by its lower environmental footprint, better grid stability characteristics, and superior baseload operation capabilities. Major developments in the segment include significant investments in combined cycle gas power plants across the region, particularly in countries like Indonesia, Vietnam, and Thailand. The segment's growth is further supported by the falling costs of closed-cycle technology and its long-term economic advantages despite higher initial capital requirements.

Remaining Segments in Cycle Segmentation

The open cycle segment represents a smaller portion of the Southeast Asia thermal power market, primarily serving specific niche applications. These systems are mainly utilized in remote off-grid locations, island communities, and offshore applications where quick start-up capabilities and lower installation costs are prioritized over efficiency. While open cycle systems offer advantages such as simpler operation, lower installation costs, and easier load control, their lower efficiency and higher emissions have limited their adoption in new large-scale power projects. The segment continues to serve specific market needs, particularly in areas where grid infrastructure is limited or where rapid response capabilities are required for peak load management.

Southeast Asia Thermal Power Market Geography Segment Analysis

Thermal Power Market in Indonesia

Indonesia maintains its dominant position in Southeast Asia's thermal power landscape, commanding approximately 37% of the region's total installed capacity in 2024. The country's thermal power sector is primarily driven by its vast coal reserves and growing electricity demand from its increasing population and industrial sectors. The state-owned utility company, Perusahaan Listrik Negara (PLN), continues to play a pivotal role in the power generation infrastructure, though recent reforms have opened doors for increased private sector participation. The country's energy mix is diversifying, with a growing emphasis on natural gas-fired thermal power plants to complement its substantial coal-based generation. Despite environmental concerns, Indonesia maintains a pragmatic approach to thermal power, balancing its commitment to renewable energy transition while ensuring energy security and economic growth. The government's focus on expanding electricity access across its numerous islands continues to drive thermal power development, particularly in regions where renewable alternatives are not yet economically viable.

Thermal Power Market in Vietnam

Vietnam emerges as the most dynamic market in Southeast Asia's thermal power sector, projected to grow at approximately 13% during the 2024-2029 period. The country's rapid industrialization and urbanization continue to drive substantial investments in thermal power infrastructure. Vietnam's power sector is undergoing significant transformation, with a strategic shift towards cleaner thermal power technologies, particularly gas-fired thermal power plants. The country's ambitious power development plans include substantial investments in LNG infrastructure and gas-to-power projects, reflecting its commitment to reducing reliance on coal while maintaining energy security. The government's focus on modernizing the power sector has attracted significant foreign investment and technological partnerships. Despite challenges in grid infrastructure and project implementation, Vietnam's thermal power sector demonstrates remarkable resilience and adaptability. The country's balanced approach to energy development, incorporating both conventional thermal power and renewable sources, positions it as a key growth market in the region.

Thermal Power Market in Thailand

Thailand maintains its position as a significant player in Southeast Asia's thermal power market, with natural gas dominating its thermal power generation portfolio. The country's well-developed gas infrastructure and strategic location in the region support its robust thermal power sector. Thailand's energy policy focuses on optimizing its thermal power fleet while gradually transitioning to cleaner energy sources. The Electricity Generating Authority of Thailand (EGAT) continues to modernize its thermal power plants, implementing advanced technologies to improve efficiency and reduce environmental impact. The country's thermal power sector benefits from strong regulatory frameworks and established public-private partnership models. Thailand's commitment to energy security has led to significant investments in LNG infrastructure, supporting the expansion of gas-fired thermal power generation. The thermal power sector continues to play a crucial role in supporting Thailand's industrial growth and maintaining grid stability.

Thermal Power Market in Malaysia

Malaysia's thermal power sector demonstrates remarkable stability, supported by its well-developed infrastructure and strategic energy policies. The country's thermal power landscape is characterized by a balanced mix of coal and natural gas-fired plants, with increasing emphasis on high-efficiency technologies. Malaysia's thermal power sector benefits from strong institutional frameworks and an established independent power producer (IPP) ecosystem. The government's focus on modernizing existing thermal power infrastructure while planning for future capacity needs reflects a pragmatic approach to energy security. The country's thermal power plants play a crucial role in supporting its growing manufacturing sector and urban development. Malaysia's strategic location and well-developed gas infrastructure provide advantages for thermal power development. The sector continues to evolve with an increasing focus on environmental compliance and efficiency improvements.

Thermal Power Market in Other Countries

The thermal power markets in other Southeast Asian countries, including the Philippines, Singapore, Brunei, Myanmar, Cambodia, and Laos, each present unique characteristics and development trajectories. These markets are characterized by varying levels of infrastructure development, regulatory frameworks, and energy demand patterns. While some countries focus on modernizing existing thermal power infrastructure, others are in the early stages of developing their thermal power capacity. The role of international partnerships and technology transfer remains crucial in these markets. Environmental considerations and access to financing increasingly influence thermal power development decisions. These countries continue to balance the need for reliable power supply with environmental commitments and economic constraints. Regional cooperation and cross-border power trading initiatives are shaping the evolution of thermal power markets in these nations.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Top Companies in Southeast Asia Thermal Power Market

The thermal power market in Southeast Asia features a mix of state-owned utilities and international technology providers driving innovation and growth. Companies are increasingly focusing on digital transformation initiatives, incorporating AI, IoT, and machine learning technologies to enhance operational efficiency and reduce emissions in thermal power plants. Strategic partnerships and collaborations between local utilities and global technology providers have become commonplace, particularly in areas of plant modernization and efficiency improvements. Operational agility is being achieved through the implementation of digital twin technologies and predictive maintenance solutions, while product innovation centers around cleaner combustion technologies and enhanced turbine designs. Market expansion strategies are predominantly focused on upgrading existing infrastructure rather than new plant construction, reflecting the region's evolving energy policies and environmental considerations.

State-owned Enterprises Lead Regional Power Generation

The Southeast Asian thermal power market exhibits a moderately fragmented structure dominated by state-owned enterprises in each country, alongside global technology and equipment providers. Major state utilities like Vietnam Electricity, Indonesia Power, and the Electricity Generating Authority of Thailand maintain significant control over their respective domestic markets, while international players like Siemens, General Electric, and other technology providers compete primarily in the thermal power equipment and services segment. The market's structure reflects the strategic importance of power generation to national interests, with state-owned enterprises maintaining majority control over generation assets while partnering with private sector players for technology and expertise.

The market has witnessed significant merger and acquisition activity, particularly in cross-border investments and technology partnerships. Regional utilities are increasingly pursuing strategic alliances to enhance their technological capabilities and operational efficiency, while international players are strengthening their presence through local partnerships and joint ventures. The trend toward consolidation is particularly evident in the power plant modernization and efficiency improvement segments, where technology providers are acquiring local service companies to enhance their market presence and service capabilities.

Innovation and Efficiency Drive Market Success

Success in the Southeast Asian thermal power market increasingly depends on companies' ability to balance operational efficiency with environmental compliance. Incumbent players are focusing on modernizing existing assets through digital technologies and efficiency improvements, while also diversifying their generation portfolio to include cleaner technologies. Market share growth strategies center around developing comprehensive solution offerings that combine equipment supply, maintenance services, and digital optimization tools. Companies are also investing in research and development to improve plant efficiency and reduce emissions, recognizing these as key differentiators in a market with growing environmental consciousness.

For new entrants and contenders, success lies in developing specialized expertise in specific market segments such as plant modernization, efficiency improvement, or digital solutions. The high concentration of end-users in industrial and urban areas necessitates strong relationships with key industrial customers and state utilities. Regulatory frameworks increasingly favor efficient and lower-emission technologies, creating opportunities for companies with advanced technological solutions. The threat of substitution from renewable energy sources is driving companies to focus on flexibility and efficiency in thermal power generation, with successful players developing solutions that complement rather than compete with renewable energy sources.

Southeast Asia Thermal Power Industry Leaders

-

Indonesia Power PT

-

Electric Power Development Co., Ltd

-

Electricity Generating Authority of Thailand

-

Vietnam Electricity

-

Malakoff Corporation Berhad

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- In January 2022, Indonesia banned the export of coal due to concerns that low supplies at domestic power plants could lead to widespread blackouts. The Indonesian Government justified the ban as it could lead almost 20 power plants with a power capacity of 10,850 megawatts to run out of coal.

- In October 2022, the first of two 2.7-GW natural gas-fired combined cycle power plants located 130 kilometers southeast of Bangkok, Thailand, commenced operations. The Gulf SRC (GSRC) power plant is the first gas-fired independent power project built by the two companies under their joint venture, Independent Power Development Co. (IPD). Gulf Energy Development holds a 70.0% equity interest in IPD, while Mitsui holds 30%.

Southeast Asia Thermal Power Market Report Scope

Thermal power generation is the process of generating electricity using direct heat from burning fuel or steam created by burning oil, natural gas, coal, and others to rotate generators and create electricity.

The Southeast Asia thermal power market is segmented by source and cycle. By source, the market is segmented into oil, natural gas, nuclear, and coal. By cycle, the market is segmented into an open cycle and a closed cycle. The report also covers the market size and forecasts for the Southeast Asia thermal power market across major countries. For each segment, the market sizing and forecasts have been done based on capacity (MW).

By Source

| Oil |

| Natural Gas |

| Coal |

| Other Sources (Bioenergy and Nuclear) |

By Cycle

| Open Cycle |

| Closed Cycle |

By Geography

| Indonesia |

| Thailand |

| Malaysia |

| Vietnam |

| Philippines |

| Rest of South East Asia |

| By Source | Oil |

| Natural Gas | |

| Coal | |

| Other Sources (Bioenergy and Nuclear) | |

| By Cycle | Open Cycle |

| Closed Cycle | |

| By Geography | Indonesia |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Philippines | |

| Rest of South East Asia |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the Southeast Asia Thermal Power Market?

The Southeast Asia Thermal Power Market size is expected to reach 214.48 gigawatt in 2025 and grow at a CAGR of 2.74% to reach 245.52 gigawatt by 2030.

What is the current Southeast Asia Thermal Power Market size?

In 2025, the Southeast Asia Thermal Power Market size is expected to reach 214.48 gigawatt.

Who are the key players in Southeast Asia Thermal Power Market?

Indonesia Power PT, Electric Power Development Co., Ltd, Electricity Generating Authority of Thailand, Vietnam Electricity and Malakoff Corporation Berhad are the major companies operating in the Southeast Asia Thermal Power Market.

What years does this Southeast Asia Thermal Power Market cover, and what was the market size in 2024?

In 2024, the Southeast Asia Thermal Power Market size was estimated at 208.60 gigawatt. The report covers the Southeast Asia Thermal Power Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Southeast Asia Thermal Power Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: