Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

| Growth Rate | 2.56% CAGR |

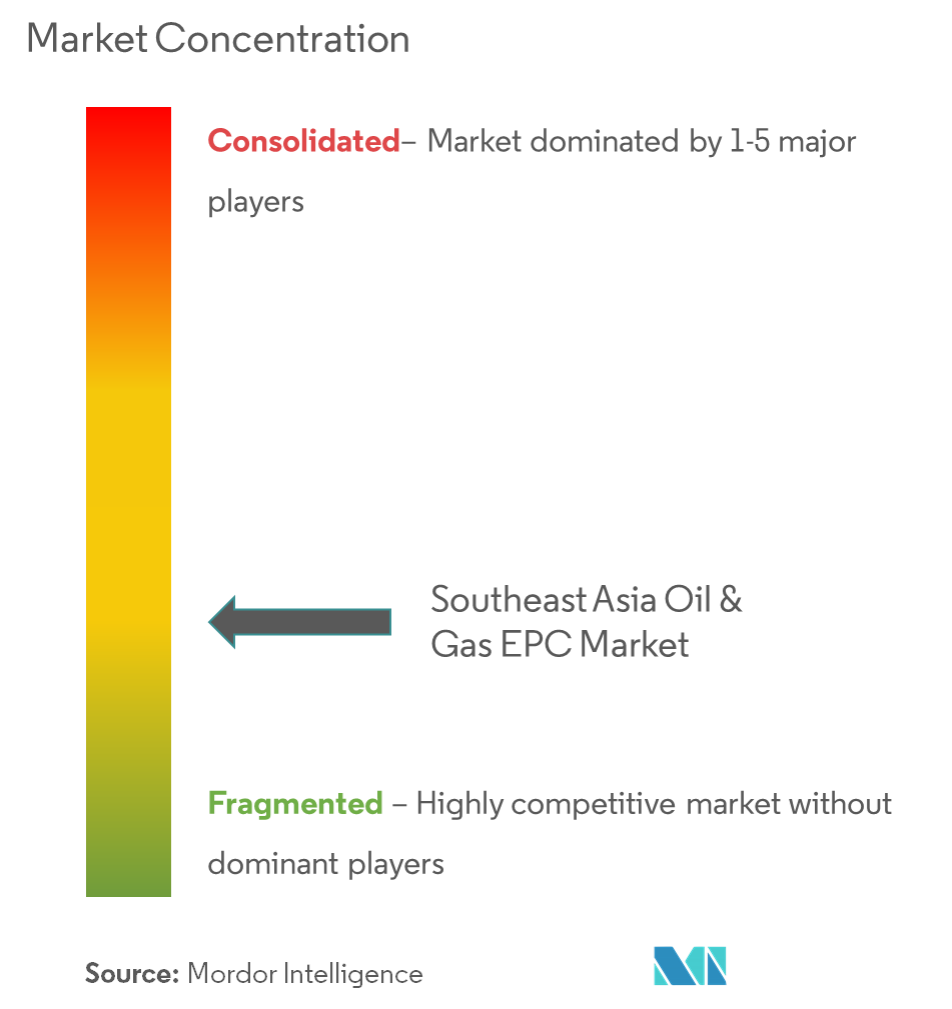

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Oil and Gas EPC Market Analysis by Mordor Intelligence

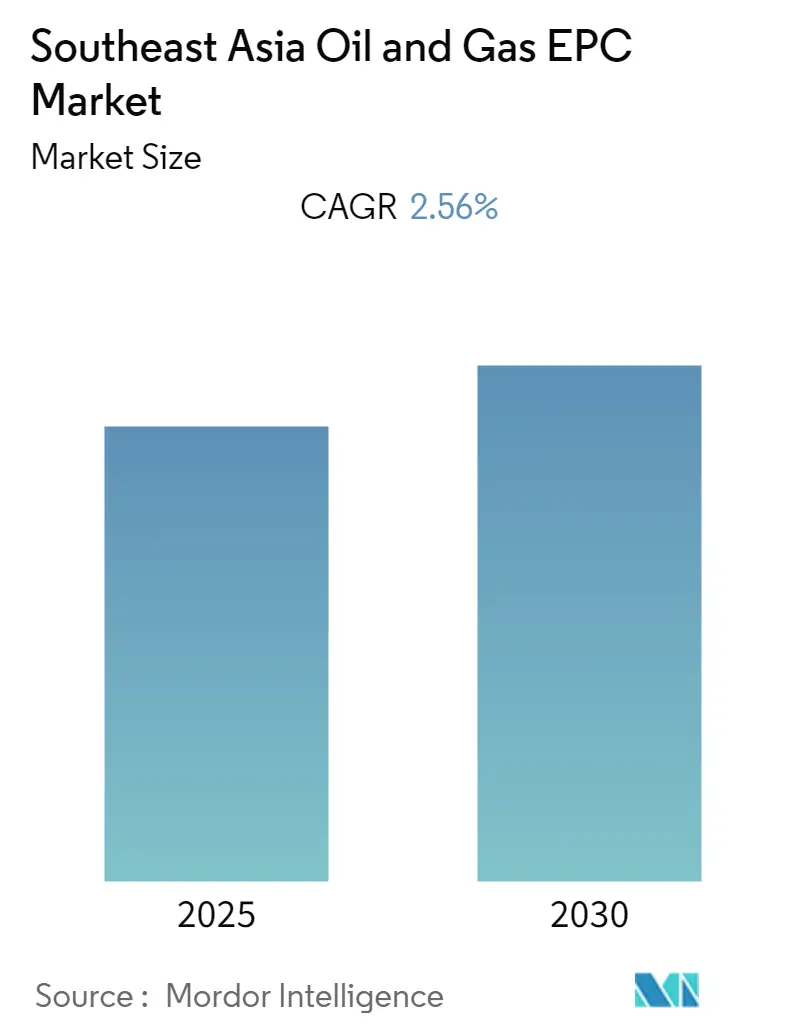

The Southeast Asia Oil and Gas EPC Market is expected to register a CAGR of 2.56% during the forecast period.

The Southeast Asian oil and gas EPC market continues to evolve amid changing regional energy dynamics and infrastructure development initiatives. The region's strategic position along major global shipping routes has established it as a crucial hub for oil and gas infrastructure activities, particularly in downstream operations. Singapore maintains its position as the regional refining powerhouse with a capacity of 1,514 thousand barrels daily, highlighting the robust downstream infrastructure in the region. This has led to increased investment in modernization and expansion projects across multiple countries, as they aim to enhance their processing capabilities and meet growing domestic demand.

The upstream sector is witnessing renewed interest in exploration and development activities, particularly in deepwater areas. Malaysia's proven oil reserves of 2.7 billion barrels underscore the significant hydrocarbon potential in the region, driving continued investment in exploration and production infrastructure. Countries are actively working to attract foreign investment through improved regulatory frameworks and attractive production sharing contracts, leading to the development of new fields and enhancement of existing ones.

Infrastructure development remains a key focus across the region, with significant investments in pipeline networks, storage facilities, and LNG terminals. Thailand's growing dependence on LNG imports, reaching 5.61 million tons, exemplifies the regional trend toward developing robust gas infrastructure. This has spurred the development of multiple LNG receiving terminals and regasification facilities across Southeast Asia, as countries work to ensure energy security and meet growing domestic demand.

The industry landscape is characterized by increasing technological integration and a focus on operational efficiency. Indonesia's operational portfolio of 184 oil and gas contract areas demonstrates the scale of ongoing activities in the region. Major EPC contractors are adopting advanced project management techniques and digital technologies to optimize project execution and reduce development timelines. This technological evolution is particularly evident in complex offshore projects, where innovative oil and gas engineering services are being employed to overcome technical challenges and improve project economics.

Southeast Asia Oil and Gas EPC Market Trends and Insights

Growing Downstream Infrastructure Development

The rapid expansion of downstream infrastructure across Southeast Asia is serving as a major driver for the Oil & Gas EPC market. The region has witnessed significant investments in refinery expansions and new Petrochemical EPC complexes, particularly in countries like Malaysia, Indonesia, and Singapore. Malaysia has established three major integrated petrochemical complexes (IPCs) in Kerteh, Gebeng, and Pasir Gudang-Tanjung Langsat, demonstrating the region's commitment to expanding its downstream capabilities. These developments have created substantial opportunities for EPC contractors involved in complex facility construction and integration projects.

The push for self-reliance in petroleum product manufacturing has led to multiple refinery projects across the region. Singapore maintains the largest refining capacity at 1,514 thousand barrels daily, setting a benchmark for regional infrastructure development. Countries like Brunei are making significant strides with projects such as Phase 2 of the Pulau Muara Besar Refinery & Petrochemical Complex, while Indonesia has announced plans to double its refining capacity to reach 2.2 million barrels per day. This widespread expansion of downstream facilities continues to generate substantial EPC contracts and creates long-term opportunities for industry participants.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Exploration and Production Activities

The extensive hydrocarbon reserves and ongoing exploration activities in Southeast Asia are driving significant demand for EPC services in the upstream sector. Indonesia alone possesses 44.2 trillion cubic feet of proven gas reserves and maintains 60 sedimentary basins, with 36 basins in Western Indonesia already thoroughly explored. The geological diversity and untapped potential of these basins continue to attract exploration investments, creating opportunities for EPC contractors in developing new production facilities and infrastructure.

The region has also witnessed intensified exploration efforts, exemplified by Indonesia's completion of its longest 2D seismic survey in Jambi Merang KKP, covering 31,908 km and examining 35 basins from a total of 128 basins. This comprehensive survey, encompassing six producing basins, seven discovery basins, and multiple unexplored areas, indicates the scale of potential future development projects. The continuous discovery of new hydrocarbon resources and the need to develop these findings into productive assets creates sustained demand for EPC services across the upstream sector, highlighting the critical role of Oil and Gas Project Management.

Rising International Investment and Partnerships

The increasing presence of international oil and gas companies in Southeast Asia has become a significant driver for the EPC market. Major international firms, including Chevron's Caltex, ExxonMobil, and Shell PLC, have established substantial operations in the region, particularly in Singapore's energy sector. These companies bring significant capital investment and technical expertise, creating opportunities for large-scale EPC projects in petrochemical and refining assets. The establishment of Singapore as the Asia-Pacific hub for downstream and chemical businesses has attracted billions in foreign investment, driving demand for sophisticated EPC services.

The region has also witnessed growing collaboration between local and international EPC contractors, leading to technology transfer and capacity building in the sector. International partnerships have enabled the execution of increasingly complex projects, from offshore exploration facilities to integrated petrochemical complexes. These collaborations have enhanced the capability of regional EPC providers while ensuring access to cutting-edge technology and project management expertise. The continued interest from international investors in developing Southeast Asia's oil and gas infrastructure creates a robust pipeline of EPC projects across the upstream, midstream, and downstream sectors, emphasizing the importance of Oil and Gas Construction.

Segment Analysis: Sector

Downstream Segment in Southeast Asia Oil and Gas EPC Market

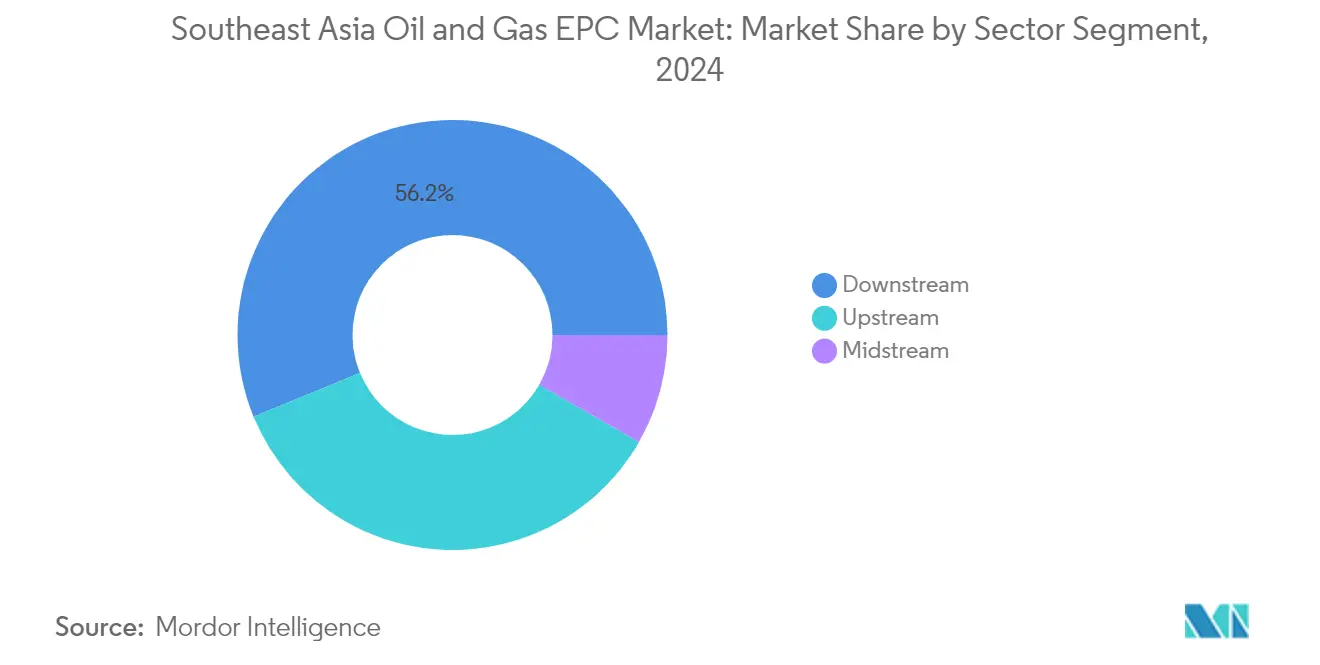

The downstream segment dominates the Southeast Asia Oil and Gas EPC market, commanding approximately 56% market share in 2024. This significant market position is driven by extensive oil and gas infrastructure development across the region. Major projects like the Pengerang Energy Complex in Malaysia, Long Son Refinery in Vietnam, and Sriracha Refinery Expansion in Thailand are contributing substantially to the segment's dominance. The segment's strength is further reinforced by Singapore's position as a major refining hub with a capacity of 1,514 thousand barrels daily, followed by Thailand and Indonesia's growing refining capabilities. Countries across Southeast Asia are actively expanding their downstream infrastructure to reduce dependence on imported refined products and establish themselves as key players in the regional petrochemical EPC market.

Midstream Segment in Southeast Asia Oil and Gas EPC Market

The midstream segment is projected to experience robust growth between 2024-2029, driven by increasing investments in LNG infrastructure and pipeline EPC networks across Southeast Asia. This growth is supported by significant projects like the Trans-ASEAN Gas Pipeline system (TAGP) and multiple LNG terminal developments. Countries such as Vietnam, the Philippines, and Myanmar are actively developing new LNG import terminals and storage facilities to meet growing energy demands. The segment's expansion is further bolstered by Indonesia's strategic pipeline EPC projects, including the Trans-Kalimantan gas pipeline and Borneo gas pipeline, along with Malaysia's extensive natural gas pipeline network development plans. These infrastructure developments are crucial for supporting the region's growing energy demands and establishing Southeast Asia as a significant LNG hub.

Remaining Segments in Sector

The upstream segment maintains a significant presence in the Southeast Asian Oil and Gas EPC market, focusing on exploration and production activities. This segment is particularly active in countries like Indonesia, Malaysia, and Thailand, where numerous offshore and onshore development projects are underway. The segment's importance is underscored by various field development projects, including Indonesia's Natuna D Alpha gas field and Malaysia's deepwater projects in Sarawak and Sabah. The upstream sector continues to play a crucial role in the region's energy security and economic development, with national oil companies and international players investing in new exploration and production technologies.

Southeast Asia Oil and Gas EPC Market Geography Segment Analysis

Southeast Asia Oil and Gas EPC Market in Malaysia

Malaysia dominates the Southeast Asian oil and gas EPC market, commanding approximately 32% of the total market share in 2024. The country's prominence stems from its extensive offshore operations in the Malay Basin, Sabah, and Sarawak basins, coupled with significant investments in both upstream and downstream sectors. Malaysia's strategic advantage lies in its comprehensive approach to oil and gas infrastructure development, particularly evident in its extensive natural gas pipeline network spanning over 2,468 km. The country's national energy company, Petronas, continues to accelerate final investment decisions for upstream projects, while simultaneously expanding its downstream capabilities through major integrated petrochemical complexes in Kerteh, Gebeng, and Pasir Gudang-Tanjung Langsat. The government's focus on becoming a regional petrochemical player has attracted substantial foreign investment, particularly in areas like Pengerang, where major refinery and petrochemical projects are underway. Malaysia's commitment to expanding its LNG infrastructure and position as a marine fuel hub further strengthens its market leadership.

Southeast Asia Oil and Gas EPC Market in Indonesia

Indonesia's oil and gas EPC market demonstrates remarkable potential through its diverse geographical profile, encompassing 60 sedimentary basins, including 36 in Western Indonesia that have been thoroughly explored. The country's strategic initiatives, particularly through SKK Migas, have created a robust framework for upstream development and exploration activities. The government's commitment to expanding pipeline networks and reducing oil dependency has led to significant investments in gas infrastructure development, including household gas pipeline construction designated as strategic national projects. Indonesia's downstream sector is witnessing substantial growth with multiple refinery expansion programs under the Refinery Development Master Plan and New Grass Root Refinery programs. The country's focus on developing integrated energy solutions, coupled with favorable policies for international investors, has created a conducive environment for EPC projects across the value chain. The presence of both state-owned enterprises and international players has fostered technological advancement and operational efficiency in project execution.

Southeast Asia Oil and Gas EPC Market in Thailand

Thailand's oil and gas EPC market showcases significant dynamism through its comprehensive approach to energy infrastructure development. The country's strategic focus on expanding its LNG infrastructure to address growing domestic demand has created numerous opportunities for EPC projects, particularly in terminal construction and pipeline EPC development. Thailand's commitment to reducing dependency on energy imports has driven substantial investments in upstream exploration and production activities, particularly in the Gulf of Thailand. The country's robust downstream sector, supported by major refinery upgrade projects and petrochemical complex developments, continues to attract international EPC contractors. Thailand's emphasis on modernizing its energy infrastructure, coupled with supportive government policies, has created a favorable environment for both domestic and international players in the EPC market. The integration of advanced technologies and focus on operational efficiency has positioned Thailand as a key player in the regional energy landscape.

Southeast Asia Oil and Gas EPC Market in Vietnam

Vietnam's oil and gas EPC market exhibits strong growth potential, particularly in its offshore sector development and downstream expansion initiatives. The country's strategic location and substantial proven reserves have attracted significant interest from international investors and EPC contractors. Vietnam's ambitious plans for developing LNG infrastructure, including multiple terminals and regasification facilities, demonstrate its commitment to diversifying its energy portfolio. The country's focus on modernizing its refining capabilities through projects like the Long Son Refinery and Dung Quat refinery expansion showcases its dedication to achieving energy self-sufficiency. Despite geopolitical challenges in the South China Sea region, Vietnam continues to advance its energy infrastructure development through strategic partnerships and technological collaboration. The government's supportive policies and focus on attracting foreign investment have created numerous opportunities for EPC projects across the entire oil and gas value chain.

Southeast Asia Oil and Gas EPC Market in Other Countries

The broader Southeast Asian region, encompassing countries such as Brunei, Singapore, Cambodia, Myanmar, and the Philippines, presents diverse opportunities in the oil and gas EPC market. Each country brings unique strengths and development focuses, from Brunei's ambitious downstream projects to Singapore's established position as a regional refining hub. Myanmar's emerging upstream sector and the Philippines' focus on LNG infrastructure development demonstrate the region's varied growth trajectories. These markets are characterized by increasing government support for oil and gas infrastructure development, growing foreign investment interest, and expanding opportunities across the entire oil and gas value chain. The collective development of these markets, supported by regional cooperation initiatives and cross-border projects, contributes significantly to the overall growth and diversification of the Southeast Asian oil and gas EPC sector.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Top Companies in Southeast Asia Oil and Gas EPC Market

The Southeast Asian oil and gas EPC market features prominent global players like TechnipFMC, Saipem, Bechtel Corporation, Fluor Corporation, John Wood Group, and Petrofac Limited, alongside regional leaders such as PT Barata Indonesia and PT Meindo Elang Indah. These companies are increasingly focusing on technological innovation through integrated project delivery models and digital transformation initiatives to enhance operational efficiency. Strategic partnerships and joint ventures have become crucial for securing major contracts, with companies combining their complementary capabilities to handle complex projects. The industry witnesses continuous investment in expanding service portfolios, particularly in areas like LNG infrastructure and petrochemical integration. Companies are also adapting their operational models to accommodate sustainable practices and environmental considerations while maintaining cost competitiveness in project execution.

Market Structure Reflects Global-Local Partnership Dynamic

The Southeast Asian oil and gas EPC market demonstrates a unique blend of global engineering giants and established local players, creating a competitive landscape that emphasizes collaborative approaches to project execution. Global players bring advanced technical expertise and project management capabilities, while local companies contribute essential regional knowledge and established relationships with national oil companies. The market structure is characterized by strategic alliances between international and domestic firms, particularly evident in major projects across Indonesia, Malaysia, and Thailand, where local content requirements play a significant role in contract awards. This dynamic has led to the emergence of hybrid operational models where global-local partnerships have become the preferred approach for securing and executing large-scale projects.

The market shows moderate consolidation with a clear distinction between tier-one global contractors and specialized regional players focusing on specific market segments or geographical areas. Merger and acquisition activities are primarily driven by the need to enhance technological capabilities, expand geographical presence, and strengthen service offerings in specific sectors such as LNG infrastructure or offshore projects. Companies are increasingly pursuing strategic acquisitions to gain access to new markets, technologies, or specialized expertise, particularly in emerging areas like renewable energy integration and digital project management solutions. The industry also witnesses vertical integration trends as companies seek to offer comprehensive solutions across the entire project lifecycle.

Innovation and Adaptability Drive Market Success

Success in the Southeast Asian oil and gas EPC market increasingly depends on companies' ability to offer innovative project delivery models while maintaining cost efficiency and technical excellence. Incumbent players are strengthening their market position by investing in digital technologies, developing integrated service offerings, and building strong local partnerships. The ability to manage complex projects while maintaining flexibility in contract structures and pricing models has become crucial for maintaining a competitive advantage. Companies are also focusing on developing specialized expertise in high-growth areas such as LNG infrastructure and petrochemical integration, while simultaneously building capabilities in sustainable energy solutions to address evolving market demands.

For new entrants and emerging players, success hinges on developing niche expertise, forming strategic alliances with established players, and demonstrating strong local market understanding. The market shows increasing emphasis on technological capabilities, particularly in areas like project digitalization and sustainable engineering solutions. Regulatory compliance, particularly regarding local content requirements and environmental standards, continues to shape competitive strategies. Companies must also address the growing importance of risk management capabilities, especially in handling large-scale projects with complex financing structures. The ability to navigate relationships with state-owned enterprises and adapt to changing energy policies remains crucial for long-term success in the market. Additionally, the integration of project management practices in oil and gas and engineering services in oil and gas is essential for achieving excellence in project execution and maintaining a competitive edge in the industry.

Southeast Asia Oil and Gas EPC Industry Leaders

TechnipFMC plc

Saipem SpA

Bechtel Corporation

Fluor Corporation

PT. JGC Indonesia

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- In August 2021, Hyundai Engineering Co. won a USD 256 million order from Thailand's third-largest refiner, IRPC Pcl, to revamp its refinery with a total capacity of 215,000 barrels per day in Rayong. Hyundai Engineering Co. has to upgrade its refinery, allowing the Thai integrated petrochemical company to produce cleaner diesel of Euro V standard. The construction started in August 2021, and the refinery is expected to come into operation by 2024 with new facilities such as a Diesel Hydrotreating Unit (DHT) and upgraded existing plants.

- In 2020, the Indonesia Deepwater Development, developed by Chevron and partners Pertamina, Eni Indonesia, and Sinopec, focused on the Gendalo, Gehem, Bangka, and Gandang fields situated in the Kutal Basin in water depths ranging from 610 to 1,829 meters. According to the operator plan, the project will be developed in two stages. Stage one will include the Bangka field's development, while stage two will develop the Gendalo, Gehem, and Gandang fields. The project is expected to have the procurement and installation of 630 kilometers of pipelines, 80 kilometers of umbilicals, and 120 subsea flowline connections.

Southeast Asia Oil and Gas EPC Market Report Scope

The Southeast Asian oil and gas EPC market includes:

Sector

| Upstream |

| Midstream |

| Downstream |

Geography

| Indonesia |

| Malaysia |

| Thailand |

| Rest of Southeast Asia |

| Sector | Upstream |

| Midstream | |

| Downstream | |

| Geography | Indonesia |

| Malaysia | |

| Thailand | |

| Rest of Southeast Asia |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current Southeast Asia Oil and Gas EPC Market size?

The Southeast Asia Oil and Gas EPC Market is projected to register a CAGR of 2.56% during the forecast period (2025-2030)

Who are the key players in Southeast Asia Oil and Gas EPC Market?

TechnipFMC plc, Saipem SpA, Bechtel Corporation, Fluor Corporation and PT. JGC Indonesia are the major companies operating in the Southeast Asia Oil and Gas EPC Market.

What years does this Southeast Asia Oil and Gas EPC Market cover?

The report covers the Southeast Asia Oil and Gas EPC Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Southeast Asia Oil and Gas EPC Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.