Southeast Asia, Middle-East And Africa Small Arms And Ammunition Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

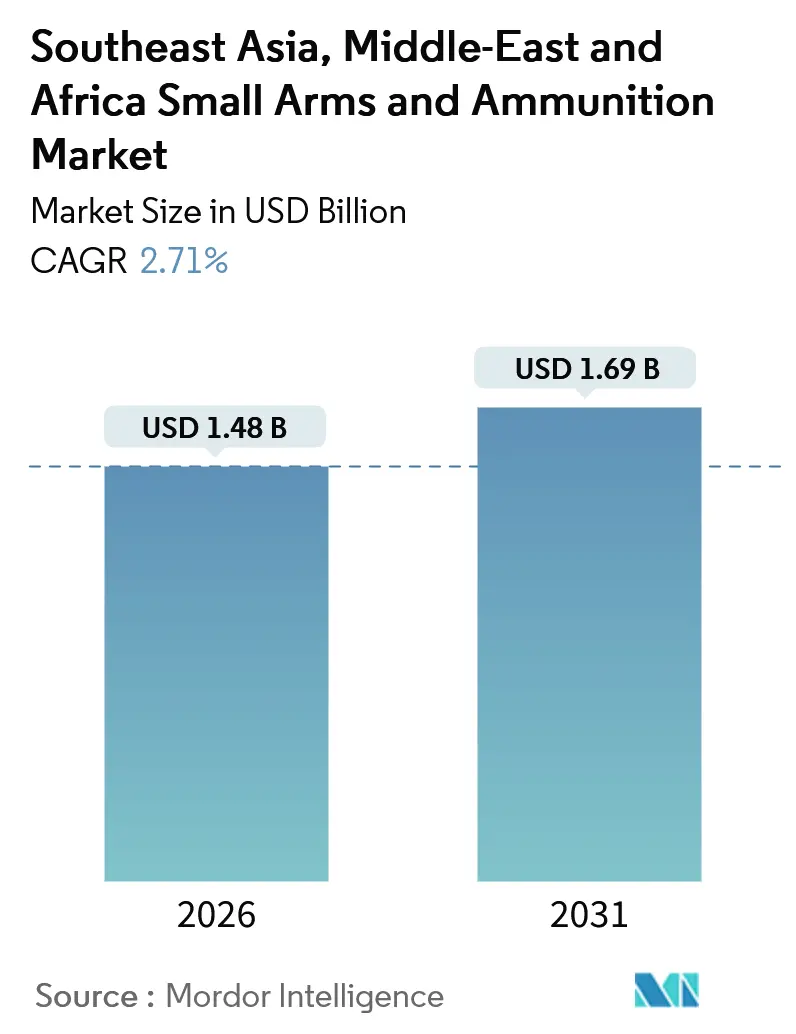

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 1.69 Billion |

| Growth Rate (2026 - 2031) | 2.71% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | South East Asia |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia, Middle-East And Africa Small Arms And Ammunition Market Analysis by Mordor Intelligence

The small arms and ammunition market in Southeast Asia, the Middle East, and Africa was valued at USD 1.48 billion in 2026 and is expected to reach USD 1.69 billion by 2031, registering a CAGR of 2.71%. The market is driven by ongoing counter-terrorism operations, defense modernization initiatives, and local content mandates, which sustain steady demand. However, fluctuations in oil prices and licensing challenges impact annual procurement cycles.

Regional buyers are increasingly adopting next-generation 6.8-millimeter cartridges, modular rifle platforms, and polymer-cased rounds to reduce logistics weight. Gulf and ASEAN governments are utilizing offset clauses to establish joint-venture manufacturing facilities closer to end users. Market competition is shifting from price-focused strategies to capabilities such as technology transfer, serial-number traceability, and efficient after-sales support.

Suppliers with established in-country partnerships, such as PT Pindad, Singapore Technologies Engineering, and Saudi Arabian Military Industries, are better positioned in the market. In contrast, vendors relying solely on imports face extended approval processes due to United Nations Programme of Action audit requirements. Additionally, private security firms protecting pipelines and LNG terminals represent a niche but growing market segment, with demand for durable weapons capable of withstanding harsh environmental conditions such as sand, salt, and tropical humidity.

Key Report Takeaways

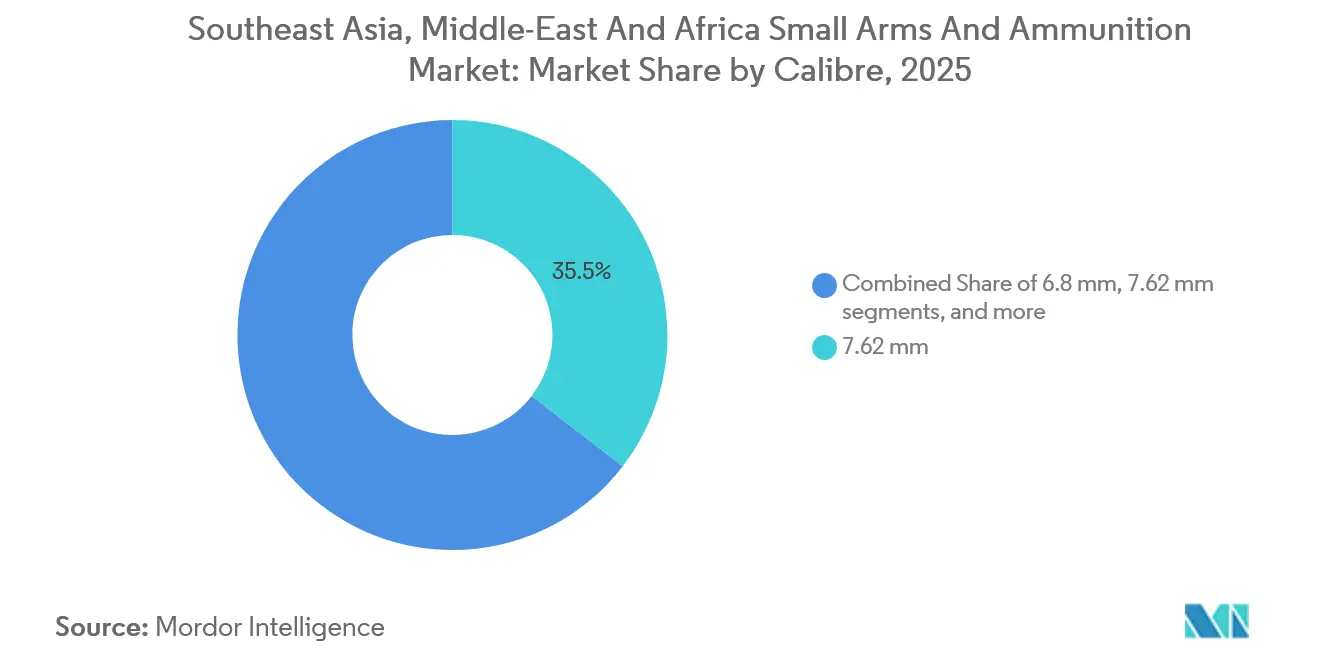

By caliber, 7.62 millimeter rounds led with 35.45% of Southeast Asia, Middle East, and Africa small arms and ammunition market share in 2025, while 6.8 millimeter cartridges are advancing at a 4.16% CAGR through 2031.

By weapon platform, rifles contributed 39.65% of the 2025 revenue, while submachine guns recorded the fastest growth at a 3.23% CAGR through 2031.

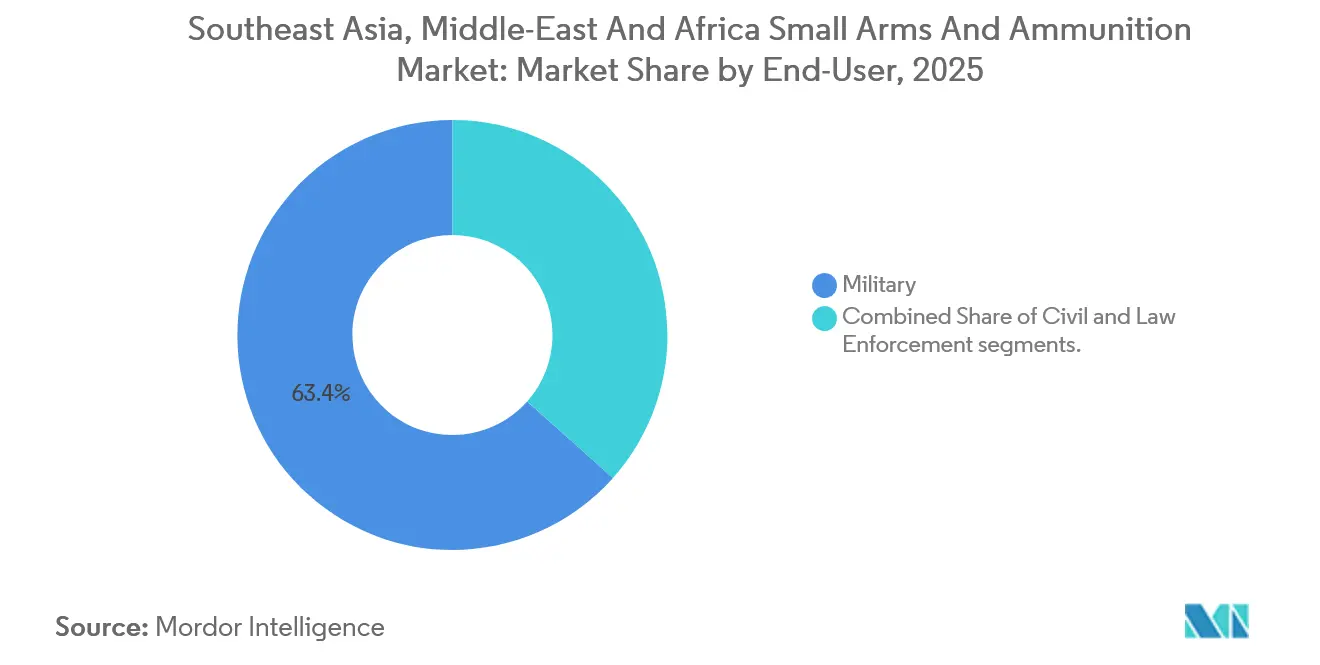

By end user, military customers captured 63.41% of 2025 sales, whereas law enforcement demand is expanding at a 3.11% CAGR, driven by urban security upgrades.

By geography, the Middle East accounted for 40.47% of the 2025 turnover; Africa is forecast to post the fastest growth of 4.01% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia, Middle-East And Africa Small Arms And Ammunition Market Trends and Insights

Drivers Impact Analysis

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counter-terrorism and internal-security procurement surge | +0.60% | Philippines, Indonesia, Saudi Arabia, UAE, Nigeria, Kenya | Short term (≤ 2 years) |

| Military modernisation programmes across SEA and GCC | +0.50% | ASEAN nations, Gulf Cooperation Council states | Medium term (2-4 years) |

| Rising civilian gun ownership and shooting sports demand | +0.20% | UAE, Saudi Arabia, Singapore, Malaysia | Long term (≥ 4 years) |

| Offset and localisation policies boosting in-region production | +0.40% | Saudi Arabia, UAE, Indonesia, Malaysia, Philippines | Medium term (2-4 years) |

| Growth of private-security firms safeguarding energy assets | +0.30% | GCC oil facilities, Nigeria, Angola | Short term (≤ 2 years) |

| E-commerce-enabled grey-market ammunition sales | +0.10% | Concentrated in Southeast Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counter-terrorism and internal-security procurement surge

Armed-group violence and cross-border crime continue to accelerate procurements across Southeast Asia, the Middle East, and Africa's small arms and ammunition market. The Philippine National Police signed USD 21.5 million in 2024 contracts for pistols and carbines to counter Abu Sayyaf attacks, and Indonesia’s Brimob expanded rifle stocks by 15 percent in 2025 to confront separatists in Papua.[1]Reuters Staff, “Indonesia Counter-Terror Procurement,” reuters.com Saudi Arabia’s Ministry of Interior purchased more than 12,000 assault rifles in 2025 after drone incursions from Yemen. Kenya followed suit with 8,500 rifles for border patrols, highlighting the pivot toward compact, quick-deploy weapons fitted with suppressors and modular rails. These procurements underline the growing emphasis on enhancing internal security and counter-terrorism capabilities in the region.

Military modernisation programmes across SEA and GCC

Defense white papers across GCC states and ASEAN members channel spending toward bright optics, suppressors, and modular calibers that extend effective range. The UAE allocated USD 450 million in 2024 to adopt 6.8 millimeter systems, which deliver 30 percent longer reach, echoing the US Army’s Next Generation Squad Weapon logic. Singapore placed an order for 18,000 rifles with ST Engineering in 2025, and Malaysia earmarked USD 180 million for co-produced ordnance by 2028, rewarding vendors that embed technology-transfer clauses. These modernization efforts reflect a strategic shift toward advanced weaponry and collaborative production agreements aimed at strengthening military capabilities.

Rising civilian gun ownership and shooting-sports demand

The consumer segment of the Southeast Asia, Middle East, and Africa small arms and ammunition market, though modest, enjoys high margins. The UAE issued 12,400 new licenses in 2025 under streamlined rules, a 22 percent jump from the prior year.[2]Ministry of Interior UAE, “Civilian Firearm Licensing Statistics 2025,” moi.gov.ae Saudi Arabia granted 8,700 civilian permits in 2024, while Malaysia’s shooting-sports federation added 18 percent more members in 2025. Premium brass-cased ammunition and match-grade projectiles command price premiums, attracting suppliers keen on retail-chain partnerships. The rising interest in shooting sports and civilian gun ownership is creating a niche but profitable market for suppliers in the region.

Offset and localisation policies boosting in-region production

Localization dictates who wins bids. Saudi Arabia achieved 24.89 percent defense-spend localization in 2024 and targets 50 percent by 2030, prompting the establishment of a USD 580 million Rheinmetall joint-venture plant, which opened in 2025. Indonesia enforces a 35 percent local-content rule, which led PT Pindad to license FN Herstal processes. The Philippines’ Republic Act 12024 requires 10 percent reinvestment locally, prompting Israel Weapon Industries to open a barrel-forging line in 2025. Such policies reward entrenched joint ventures while deterring import-only hopefuls. These initiatives are reshaping the competitive landscape by prioritizing local production and technology transfer agreements.

Restraints Impact Analysis

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent import licensing and end-user certification | -0.40% | Southeast Asia, Middle East | Medium term (2-4 years) |

| Oil-price-linked budget volatility in MEA states | -0.50% | GCC states, oil-dependent African economies | Short term (≤ 2 years) |

| Illicit trafficking concerns prompting tighter traceability | -0.20% | Sahel, Horn of Africa, SEA maritime corridors | Medium term (2-4 years) |

| Shift to non-lethal directed-energy crowd-control options | -0.10% | Urban centers in Middle East and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent import licensing and end-user certification

United Nations frameworks require importers to verify end-users, extending procurement cycles in the Southeast Asia, Middle East, and Africa small arms and ammunition market by up to nine months. Singapore’s Arms and Explosives Act delayed three ammunition contracts in 2025, and ISACS marking rules strain smaller factories that cannot fund compliance teams. While incumbents absorb these costs, opportunistic suppliers withdraw, reducing competitive price pressure. The regulatory environment is becoming increasingly stringent, impacting the pace and cost of procurement processes across the region.

Oil-price-linked budget volatility in MEA states

Defense outlays track Brent crude prices, which fell from USD 82 in 2024 to USD 75 in mid-2025, prompting Saudi Arabia to defer a 25,000-rifle tender and Nigeria to cut its 2025 defense allocations by 12 percent.[3]RAND Corporation, “Defense Budget Volatility in the Middle East,” rand.org Vendors respond with flexible payment terms and barter offers tied to crude cargoes, yet revenue-recognition uncertainty weighs on listed manufacturers. The volatility in oil prices continues to influence defense budgets, creating challenges for both governments and suppliers in maintaining consistent procurement plans.

Segment Analysis

By Caliber: Intermediate Cartridges Yield to Next-Generation Ballistics

The 7.62 millimeter segment accounted for 35.45% of 2025 sales, driven by legacy AK inventories. However, funding is increasingly directed toward calibers compatible with Western standards. For instance, Indonesia ordered 42 million 7.62×39 millimeter rounds in 2024 but allocated only 18% of its 2025-2029 small-arms budget to this caliber. In contrast, 6.8 millimeter ammunition is expected to grow at a 4.16% CAGR, the highest in the Southeast Asia, Middle East, and Africa small arms and ammunition market, following US combat tests that demonstrated 20% greater lethality at 600 meters. The 5.56 millimeter caliber remains essential, as evidenced by Malaysia’s order of 28 million rounds in 2025, while 9 millimeter stockpiles expand in tandem with police sidearm upgrades. Niche calibers like .338 Lapua Magnum attract special-operations units but contribute minimally to overall revenue.

The market benefits from caliber diversification as end users seek both backward compatibility and advanced ballistics. Suppliers are offering modular rifles that can accommodate 5.56mm, 6.8mm, and 7.62mm rounds by swapping barrels, thereby reducing lifecycle costs and simplifying logistics. Additionally, advancements in polymer-cased technology promise 30-40% weight reductions, enabling soldiers to carry more ammunition without exceeding load limits.

Note: Segment shares of all individual segments available upon report purchase

By Weapon Platform: Close-Quarters Imperatives Reshape Procurement Priorities

Rifles generated 39.65% of 2025 revenue; however, urban operations strategies are accelerating demand for submachine guns, which are projected to grow at a 3.23% CAGR through 2031. For example, the UAE Presidential Guard procured 4,200 FN P90s in 2025 for VIP protection, while Indonesia’s Brimob acquired nearly 2,800 MP5s in 2024. Handguns are also in high demand, with police forces standardizing on high-capacity semiautomatic pistols; for example, Singapore ordered 8,500 SIG P226s in 2024. Light machine guns and shotguns continue to serve specialized roles, such as suppressive fire and riot control, with shorter replacement cycles in high-tempo units sustaining steady demand.

Procurement priorities in Southeast Asia, the Middle East, and Africa's small arms and ammunition markets now emphasize modularity, corrosion-resistant finishes, and suppressor compatibility over maximum muzzle velocity. Vendors capable of integrating advanced optics and Bluetooth-enabled training sensors command premium pricing.

By End User: Law-Enforcement Modernization Narrows the Military–Civilian Gap

Military organizations accounted for 63.41% of 2025 spending, but law enforcement agencies are experiencing higher growth rates. For instance, the Philippine National Police allocated USD 86 million for small arms through 2026, while Saudi Arabia’s Special Security Forces deployed 12,500 new carbines in 2025, featuring capabilities previously exclusive to special-operations units. Civilian buyers remain a niche but profitable segment, supported by Gulf recreational-shooting initiatives tied to economic diversification efforts.

As urban unrest and organized crime increasingly blur traditional defense boundaries, interior ministries are demanding military-grade reliability in police weapons. This trend drives ammunition manufacturers to produce both crowd-control-optimized 9mm rounds and armor-piercing 5.56mm cartridges, thereby expanding their product portfolios and stabilizing production rates.

Geography Analysis

The Middle East accounted for 40.47% of the 2025 revenue in the Southeast Asia, Middle East, and Africa small arms and ammunition market, supported by Vision 2030 localization initiatives that direct budgets toward domestic production. For example, the Rheinmetall-SAMI plant, launched in 2025 with an annual capacity of 120 million rounds, reduced cartridge imports by 35%. The UAE’s USD 450 million rifle-replacement program highlights the region’s focus on next-generation platforms. At the same time, Oman awarded an 18 million-round ammunition contract to a local producer in 2025, thereby enhancing its self-reliance. However, fluctuations in crude oil prices directly impact order volumes, prompting vendors to offer deferred-payment options.

Southeast Asia’s geographic challenges and insurgent threats necessitate the distribution of stockpiles. Examples include Indonesia’s purchase of 22,000 rifles for Papua units, the Philippines’ PHP 1.2 billion pistol-and-carbine contracts, and Singapore’s order of 18,000 SAR 21 Mk2 rifles. While procurement strategies vary, there is a shared emphasis on lightweight, optics-ready weapons. Offset policies, such as Indonesia’s 35% local-content requirement and Malaysia’s Industrial Collaboration Programme, influence procurement decisions, creating barriers to market entry for some suppliers.

Africa is projected to achieve the fastest growth, with a 4.01% CAGR through 2031. Kenya increased police rifle inventories by 8,500 units in 2024 and doubled plans for ammunition factory output to support regional exports. Nigeria commissioned a 12 million-round production line in Kaduna in 2024 but achieved only 60% capacity due to quality control issues, highlighting the gap between policy ambitions and operational execution. Meanwhile, Denel’s 2025 contract with the South African military demonstrates that established players can still secure contracts despite restructuring challenges.

Competitive Landscape

The small arms and ammunition market in Southeast Asia, the Middle East, and Africa is moderately fragmented, with the five largest suppliers accounting for approximately 38% of the combined revenue. Localization policies have led to the establishment of joint venture plants, creating country-specific mini oligopolies. For instance, SAMI and Rheinmetall in Saudi Arabia, ST Engineering across ASEAN, and PT Pindad in Indonesia benefit from preferred-bidder status under national content regulations. Examples of this include PT Pindad’s export of 12,000 rifles to the Philippines in 2024 and ST Engineering’s acquisition of a 51% stake in a Malaysian distributor in 2025, showcasing how incumbents capitalize on proximity and policy alignment to secure contracts.

Current innovation efforts focus on caliber-convertible rifles, polymer-cased ammunition, and innovative optics. FN Herstal introduced the FN EVOLYS system in 2024, featuring tool-free caliber swaps, which has drawn interest from Saudi Arabia’s National Guard and Malaysia’s police special actions unit. Turkish manufacturers MKEK and Sarsilmaz offer prices up to 30% lower than those of Western competitors, while adhering to ISACS marking standards, enabling them to secure a 15,000-rifle sale to Niger in 2024. However, suppliers without regional production facilities or compliance infrastructure face challenges, including reduced margins due to audit costs and extended bidding cycles.

Southeast Asia, Middle-East And Africa Small Arms And Ammunition Industry Leaders

Singapore Technologies Engineering Ltd.

PT Pindad

Saudi Arabian Military Industries (SAMI)

Israel Weapon Industries (IWI) Ltd.

Elbit Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Saudi Arabian Military Industries (SAMI) and Rheinmetall commenced full-scale production at their specialized ammunition plant in Al-Kharj. The facility has reached its initial production target of 120 million rounds annually, focusing on 5.56 mm and 7.62 mm cartridges, which are critical for small-arms military operations. As the most significant defense localization initiative under Vision 2030, the plant is projected to reduce Saudi Arabia's dependence on European ammunition imports by approximately 35%. This development aligns with the Kingdom's objective of localizing 50% of military spending by 2030, with localization rates standing at around 24.9% as of late 2025.

- January 2026: The Israel Ministry of Defense and the Israel Defense Forces have completed the distribution of thousands of ARAD rifles produced by Israel Weapon Industries to rapid response teams across the country. The rollout marks the completion of a procurement program focused on standardised, domestically produced defense systems. The ARAD was developed for special forces and law enforcement professionals operating in demanding conditions and is based on an advanced AR platform. The 5.56mm rifle features short-stroke gas-piston operation, full ambidextrous controls, a free-floating hammer-forged barrel, and integrated rails to support optics and accessories.

Southeast Asia, Middle-East And Africa Small Arms And Ammunition Market Report Scope

Small arms and ammunition encompass handheld firearms and their corresponding cartridges designed to meet defense, law enforcement, and civilian safety requirements across Southeast Asia, the Middle East, and Africa. The study encompasses the procurement, production, and distribution of rifles, handguns, submachine guns, light machine guns, shotguns, and ammunition in calibers ranging from 5.56 mm to 12.7 mm, serving military forces, law enforcement agencies, private security contractors, and licensed civilian users. The market also includes component-level maintenance, localized manufacturing under offset agreements, and technology transfer arrangements between foreign original equipment manufacturers and regional state-owned ordnance factories.

The Southeast Asia, Middle East, and Africa Small Arms and Ammunition Market is segmented by caliber, weapon platform, end-user, and geography. By caliber, the market is segmented into 5.56 mm, 6.8 mm, 7.62 mm, 9 mm, 12.7 mm, and other calibers. By weapon platform, the market is segmented into handguns, rifles, light machine guns, submachine guns, and shotguns. By end user, the market is segmented into civil, law enforcement, and military segments. By geography, the market is segmented into Southeast Asia (comprising Indonesia, Malaysia, the Philippines, Singapore, and the rest of Southeast Asia), the Middle East (comprising the United Arab Emirates, Saudi Arabia, and the rest of the Middle East), and Africa (comprising South Africa and the rest of Africa). The market sizing and forecasts have been provided in value (USD billion) for all the above segments.

| 5.56 mm |

| 6.8 mm |

| 7.62 mm |

| 9 mm |

| 12.7 mm |

| Other Calibers |

| Handguns |

| Rifles |

| Light Machine Guns (LMGs) |

| Sub-Machine Guns (SMGs) |

| Shotguns |

| Civil |

| Law Enforcement |

| Military |

| Southeast Asia | Indonesia | |

| Malaysia | ||

| Philippines | ||

| Singapore | ||

| Rest of Southeast Asia | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Caliber | 5.56 mm | ||

| 6.8 mm | |||

| 7.62 mm | |||

| 9 mm | |||

| 12.7 mm | |||

| Other Calibers | |||

| By Weapon Platform | Handguns | ||

| Rifles | |||

| Light Machine Guns (LMGs) | |||

| Sub-Machine Guns (SMGs) | |||

| Shotguns | |||

| By End User | Civil | ||

| Law Enforcement | |||

| Military | |||

| By Geography | Southeast Asia | Indonesia | |

| Malaysia | |||

| Philippines | |||

| Singapore | |||

| Rest of Southeast Asia | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Southeast Asia, Middle-East and Africa small arms and ammunition market today?

The market stood at USD 1.48 billion in 2026 and is projected to reach USD 1.69 billion by 2031, growing at a 2.71% CAGR.

Which caliber is growing fastest in regional procurements?

6.8 millimeter ammunition is forecast to expand at a 4.16% CAGR as militaries pursue longer-range, higher-penetration rounds.

Why are localization mandates important for suppliers?

Countries such as Saudi Arabia and Indonesia require up to 50% local content, so foreign vendors must set up joint-venture factories or risk exclusion from tenders.

Which end-user segment is gaining share fastest?

Law-enforcement agencies are increasing purchases at a 3.11% CAGR as urban-security threats rise.

How do oil-price swings affect defense buying in the Middle East and Africa?

Lower crude prices reduce government revenue, often deferring rifle and ammunition tenders or shrinking annual order volumes.

What technologies will shape future regional procurement?

Modular rifles with caliber-conversion kits, polymer-cased ammunition that cuts weight, and smart optics integrated with ballistic calculators are gaining traction.