| Study Period | 2024 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Volume (2025) | 73.78 gigawatt |

| Market Volume (2030) | 93.27 gigawatt |

| CAGR | 4.80 % |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Southeast Asia Hydropower Market Analysis

The Southeast Asia Hydropower Market size in terms of installed base is expected to grow from 73.78 gigawatt in 2025 to 93.27 gigawatt by 2030, at a CAGR of 4.8% during the forecast period (2025-2030).

The Southeast Asian hydropower landscape is undergoing significant transformation driven by regional cooperation and cross-border power trading initiatives. According to the International Hydropower Association (IHA), the region had an installed hydropower capacity of 51.96 GW in 2021, demonstrating the sector's substantial presence. A notable development in this direction is the June 2022 power integration agreement between Laos and Singapore, where Laos will export between 30-100 MW of hydroelectricity to Singapore under the Laos-Thailand-Malaysia-Singapore Power Integration Project. This marks a significant step toward establishing an integrated ASEAN power grid and demonstrates the growing importance of regional energy cooperation.

The industry is witnessing a shift toward strategic partnerships and technological modernization. In March 2022, ANDRITZ and the Electricity Generating Authority of Thailand (EGAT) signed a significant Memorandum of Understanding to explore and expand business opportunities for hydropower projects in Thailand and surrounding Southeast Asian countries. This collaboration focuses on expanding and digitalizing hydropower facilities while developing rehabilitation and automation projects, indicating a growing emphasis on modernizing existing infrastructure rather than just building new facilities. The partnership approach is becoming increasingly common as countries seek to leverage expertise and resources across borders.

Environmental considerations and sustainable development practices are reshaping project implementation strategies across Southeast Asia. Many countries are now focusing on run-of-river projects and smaller hydropower plants to minimize environmental impact. This shift is particularly evident in Thailand, where hydroelectric power's contribution to total electricity consumption decreased to 2.2% in 2021, leading to a greater emphasis on environmental impact assessments and sustainable development practices. Countries are increasingly adopting hybrid approaches, combining hydropower with other renewable energy sources to create more sustainable and reliable power generation systems.

The sector faces significant challenges related to irrigation and water resource management. According to the International Commission for Irrigation and Drainage, only 23.29% of Thailand's cultivated area is under irrigation, highlighting the need for better water resource management. This has led to an increased focus on multipurpose hydropower projects that serve both energy generation and irrigation needs. The industry is witnessing a trend toward developing projects that can balance hydropower generation with agricultural requirements, particularly in countries with significant agricultural sectors like Vietnam, Thailand, and Indonesia, where water resource management is crucial for economic development.

Southeast Asia Hydropower Market Trends

Supportive Government Policies to Promote Hydropower Projects

The Southeast Asian hydropower market is significantly driven by strong government support and favorable policies promoting renewable energy adoption. The Association of Southeast Asian Nations (ASEAN) Plan of Action for Energy Cooperation (APAEC) 2021-2025 has set an ambitious target to achieve 35% renewable generation in installed power capacity by 2025, requiring the deployment of approximately 35-40 GW of renewable energy capacity. This regional commitment has led to increased investments in hydropower technology projects, as demonstrated by Indonesia's initiation of construction works for the Mentarang Induk hydroelectric facility in March 2023, with a substantial investment of USD 2.6 billion.

Government initiatives have also facilitated international cooperation in hydropower development across the region. In January 2024, Vietnam Electricity (EVN) signed 19 power purchase agreements for 2,689 MW of electricity from 26 hydropower plants in Laos, showcasing the strong interstate collaboration in developing hydropower resources. The economic viability of these projects is further supported by the competitive levelized cost of energy (LCOE), which, according to the International Renewable Energy Agency, stood at USD 0.048/kWh for newly commissioned hydropower projects in 2022, making it an attractive option for both governments and private investors.

Understand The Key Trends Shaping This Market

Download PDF

Growing Power Demand and Need for Clean Energy

The rapid industrialization and urbanization across Southeast Asia have created a substantial increase in power demand, driving the development of hydropower generation projects as a reliable source of clean energy. Vietnam, a key market in the region, is projected to experience power demand growth of 6-7% during 2021-2030, necessitating significant capacity additions in renewable energy sources. The country's commitment to meeting this growing demand while achieving emission reduction targets has led to increased investment in both large-scale and run-of-river hydropower projects, with an estimated untapped potential of 11 GW in run-of-river small-scale hydro alone.

The drive for clean energy is also evident in recent developments across other Southeast Asian nations. In November 2023, the Philippines demonstrated its commitment to expanding clean energy capacity with the launch of a 1.4 MW run-of-river hydropower plant by Repower Energy Development Corporation, capable of generating 8 gigawatt-hours annually. This trend is further supported by Laos's power development plan, which aims to exceed 14 gigawatts of hydropower capacity by 2025, representing a significant portion of its targeted 30% renewable energy mix. These developments highlight the region's strong focus on leveraging hydro energy to meet growing energy demands while transitioning towards cleaner energy sources. Additionally, the potential of pumped storage hydropower is being explored to enhance energy storage solutions in the region.

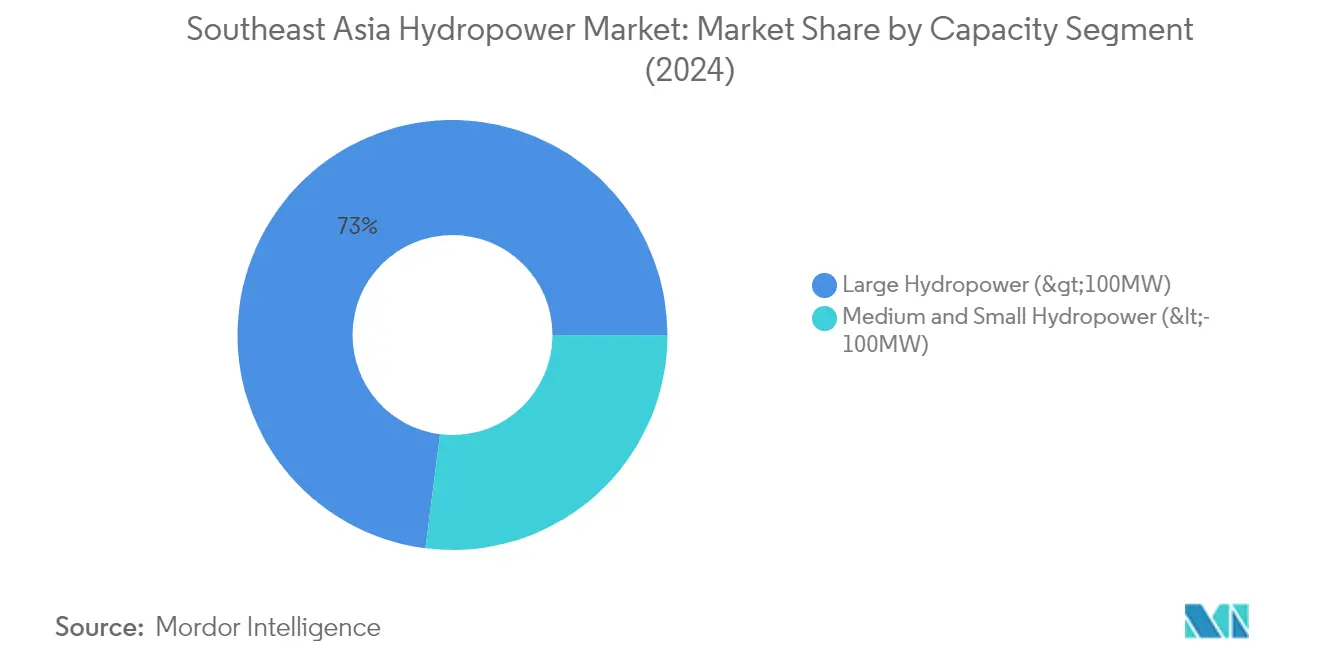

Segment Analysis: By Capacity

Large Hydropower Segment in Southeast Asia Hydropower Market

The large hydropower segment, defined as installations greater than 100 MW, dominates the Southeast Asia hydropower market with approximately 73% market share in 2024. This segment's prominence is driven by several major projects under development across the region, particularly in countries like Vietnam, Indonesia, and Laos. The segment's growth is supported by increasing electricity demand, government initiatives for renewable energy development, and significant foreign investments, especially from Chinese and Japanese companies. Large hydropower plants provide essential benefits, including stable baseload power generation, flood control capabilities, and irrigation support for agricultural activities. The segment's expansion is further bolstered by technological advancements in turbine efficiency and dam construction techniques, though environmental and social considerations continue to influence project development decisions.

Medium and Small Hydropower Segment in Southeast Asia Hydropower Market

The medium and small hydropower segment, encompassing installations less than 100 MW, represents a vital component of the Southeast Asian hydropower landscape. This segment is particularly significant in remote and rural areas where large-scale projects are not feasible or environmentally sustainable. Small hydropower projects typically have shorter development timelines, lower environmental impacts, and face fewer social resistance issues compared to their larger counterparts. The segment benefits from various government incentives, including feed-in tariffs and simplified approval processes in countries like the Philippines and Indonesia. These projects often operate on a run-of-river basis, which helps maintain natural river flows and minimizes environmental disruption. The segment's growth is supported by an increasing focus on distributed generation and rural electrification programs across the region.

Southeast Asia Hydropower Market Geography Segment Analysis

Southeast Asia Hydropower Market in Vietnam

Vietnam dominates the Southeast Asian hydropower landscape, commanding approximately 32% of the region's total installed capacity in 2024. The country's extensive network of rivers, including the Mekong and its tributaries, provides an ideal foundation for hydropower development. Vietnam's hydropower sector benefits from its diverse geographical features, with 60% of its hydropower potential concentrated in the North, 27% in the Central Region, and 13% in the South. The country has already developed nearly 60% of its total hydropower potential, making it a mature market in the region. While large-scale hydropower projects dominate the landscape, there remains significant untapped potential for run-of-river small hydropower of around 11 GW. The government's commitment to renewable energy integration, coupled with the sector's role in providing baseload power and grid stability, continues to drive investment in both new projects and the expansion of existing facilities. However, the sector faces challenges related to climate change impacts on water levels and growing environmental concerns over large-scale projects.

Southeast Asia Hydropower Market in Indonesia

Indonesia represents one of the most dynamic markets in the Southeast Asian hydropower sector, with projections indicating a remarkable growth rate of approximately 17% between 2024 and 2029. The archipelagic nation possesses substantial untapped hydropower potential, particularly in Papua Island (22.4 GW), Kalimantan Island (21.6 GW), and Sumatra Island (15.6 GW). The government's commitment to decarbonizing the energy sector, aiming for 31% renewable energy in total energy supply by 2050, has created a favorable environment for hydropower development. The country's unique geography, comprising thousands of islands, presents both challenges and opportunities for hydropower development, particularly in the small hydropower and mini hydropower segments. The regulatory framework, including the Build-Own-Operate (BOO) business scheme and favorable tariff structures for hydropower projects, has created an attractive investment environment. Despite the challenges of environmental concerns and complex terrain, Indonesia's hydropower sector continues to attract significant domestic and international investment, particularly in run-of-river projects and small-scale installations.

Southeast Asia Hydropower Market in Laos

Laos has established itself as a crucial player in the Southeast Asian hydropower sector, leveraging its strategic location within the Mekong River basin and its tributaries. The country's position as a major electricity exporter to neighboring countries, including Thailand, Vietnam, and Cambodia, has driven significant investment in hydropower infrastructure. With nearly 78 dams in operation and memorandums of understanding signed for 246 additional hydroelectric power projects, Laos continues to expand its hydropower capacity aggressively. The country's development strategy focuses on both large-scale projects along the Mekong mainstream and smaller installations on its tributaries. International partnerships, particularly with Chinese and Thai companies, have been instrumental in project development and financing. However, the sector faces increasing scrutiny regarding environmental sustainability and social impacts, particularly concerning the Mekong River ecosystem and local communities.

Southeast Asia Hydropower Market in Malaysia

Malaysia's hydropower sector demonstrates a balanced approach to development, with a strong focus on both large hydropower projects and run-of-river installations. The country's formal recognition of large hydropower as part of its renewable energy definition has created new opportunities for sector growth. The market structure is characterized by strong utility company leadership, with entities like Tenaga Nasional Berhad and Sarawak Energy Berhad driving development. Malaysia's approach to hydropower development emphasizes environmental sustainability and social responsibility, particularly in project planning and implementation. The country has identified significant potential for run-of-river hydroelectric power plants, with numerous sites suitable for development. The government's supportive policy framework, including feed-in tariffs for small hydropower projects, has created a conducive environment for private sector participation and technological innovation.

Southeast Asia Hydropower Market in Other Countries

The remaining Southeast Asian countries, including Thailand, the Philippines, Cambodia, Singapore, Brunei, and Timor-Leste, each contribute uniquely to the regional hydropower landscape. Thailand's mature market focuses on modernizing existing facilities and exploring innovative solutions like floating solar integration with hydropower assets. The Philippines emphasizes run-of-river projects due to seismic considerations, while Cambodia's development is closely tied to Mekong River management policies. Singapore's limited geographical features restrict hydropower development, while Brunei and Timor-Leste focus on small-scale installations suitable for their terrain and demand patterns. These markets collectively demonstrate the diverse approaches to hydropower development in Southeast Asia, ranging from large utility-scale projects to small, community-focused installations.

Get Analysis on Important Geographic Markets

Download PDF

Southeast Asia Hydropower Industry Overview

Top Companies in Southeast Asia Hydropower Market

The Southeast Asian hydropower market features prominent players like Andritz AG, General Electric, Vietnam Electricity Construction JSC, and Toshiba Corporation leading the industry through various strategic initiatives. Companies are increasingly focusing on technological innovation and R&D investments to develop advanced hydropower technology solutions, particularly in areas like hydro turbine efficiency and digital monitoring systems. The market witnesses active collaboration between local and international players through joint ventures and partnerships to leverage complementary strengths and expand market presence. Operational excellence is being prioritized through the implementation of advanced maintenance techniques and predictive analytics to optimize plant performance. Companies are also emphasizing sustainability and environmental compliance while expanding their project portfolios, with many players incorporating eco-friendly designs and practices in their hydropower developments.

Market Structure Shows Regional Power Dynamics

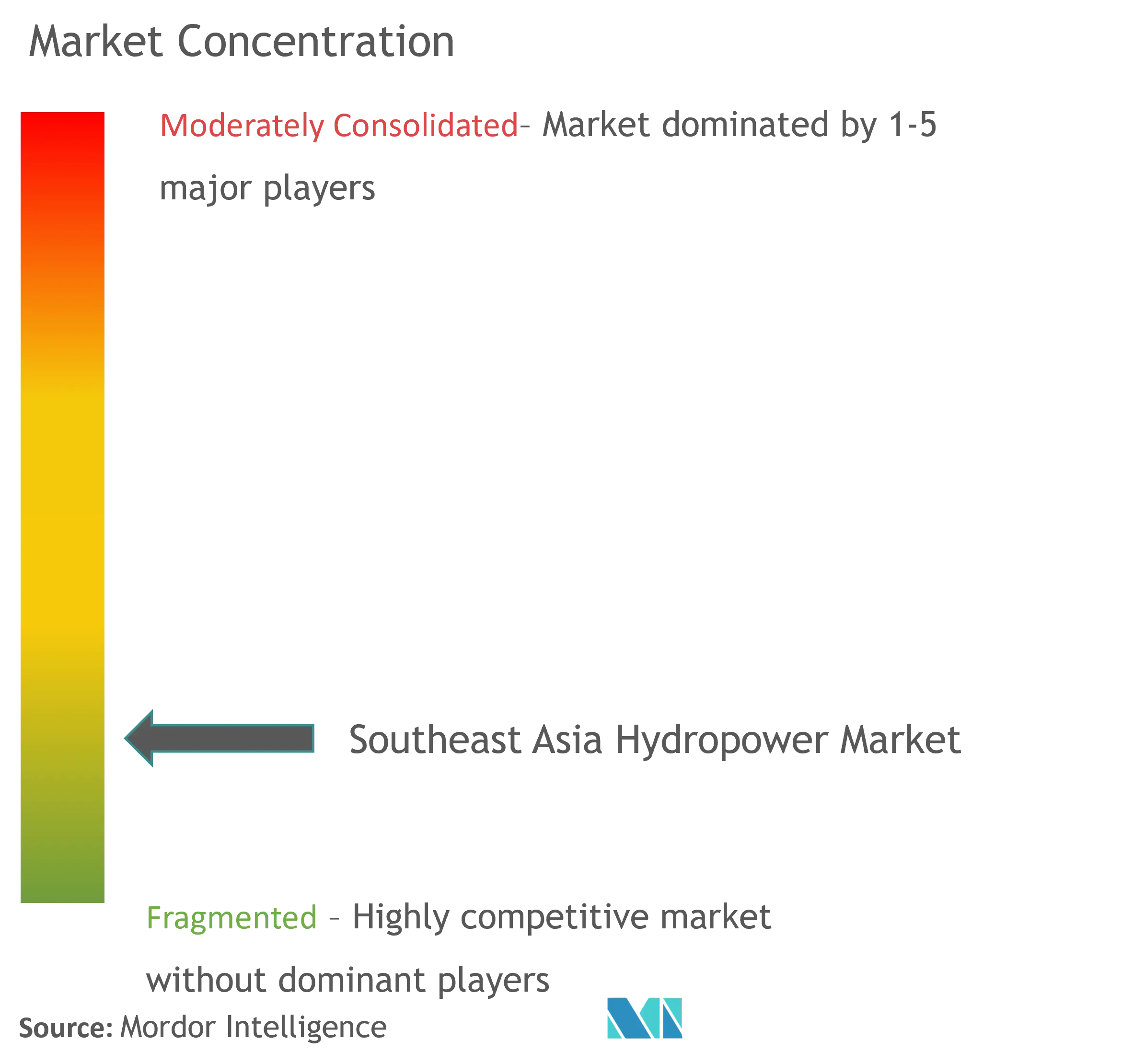

The Southeast Asian hydropower market exhibits a moderately consolidated structure with a mix of state-owned enterprises and private sector players shaping the competitive landscape. State utilities like Vietnam Electricity, Thailand's EGAT, and Malaysia's Tenaga Nasional maintain significant market positions in their respective countries, while global equipment manufacturers and EPC contractors compete for project opportunities across the region. The market demonstrates strong regional interconnections, with cross-border power trading and joint development projects becoming increasingly common among neighboring countries. Local companies often partner with international technology providers to enhance their capabilities and maintain competitiveness in the market.

The industry has witnessed several strategic mergers and acquisitions aimed at consolidating market positions and expanding geographical reach. International players are increasingly establishing local subsidiaries and forming strategic alliances with regional companies to strengthen their market presence and navigate local regulatory environments. The competitive dynamics are further influenced by the growing participation of Chinese companies, particularly in project development and equipment supply, while Japanese and European firms maintain their traditional strengths in technology and quality standards. Market entry barriers remain relatively high due to substantial capital requirements and the need for specialized technical expertise.

Innovation and Sustainability Drive Future Success

Success in the Southeast Asian hydropower market increasingly depends on companies' ability to integrate technological innovation with sustainable practices while maintaining cost competitiveness. Market incumbents are focusing on modernizing existing facilities through digitalization and automation, while also expanding their project portfolios with new developments that incorporate advanced environmental protection measures. Companies are investing in developing specialized expertise in areas such as small hydropower and pumped storage facilities to diversify their offerings and capture emerging market opportunities. The ability to provide comprehensive solutions, from project planning to long-term maintenance services, is becoming a crucial differentiator in the market.

Future market success will require companies to effectively address environmental concerns while meeting growing energy demands across the region. Players must navigate complex regulatory environments and demonstrate strong stakeholder management capabilities, particularly in addressing community concerns and environmental impact assessments. The development of innovative financing models and the ability to leverage government support mechanisms will be crucial for project development. Companies that can effectively combine technical expertise with strong local market understanding, while maintaining high environmental and social standards, will be better positioned to capture market opportunities and maintain competitive advantages in the evolving market landscape.

Southeast Asia Hydropower Market Leaders

-

Vietnam Electricity Construction JSC

-

Tenaga Nasional Berhad

-

Andrtiz AG

-

PT Perusahaan Listrik Negara

-

Electricity Generating Authority of Thailand

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Southeast Asia Hydropower Market News

- January 2024: Nexif Ratch Energy Investments Pte. Ltd, an owner/operator of clean-energy power, acquired the 30 MW Minh Luong hydropower plant, a run-of-river facility with peak-hour storage in Lao Cai province, Vietnam. The acquisition strengthens the Nexif Ratch Energy portfolio’s growth path in renewables and will create a stable and recurring income through a long-term power purchase agreement.

- February 2024: The French development agency, Agence Française de Développement, announced that it is seeking to engage individual regional or international specialists to form a panel of experts to provide technical assistance services for the development of the 1.2 GW Bac Ai pumped-storage hydropower plant in the Ninh Thuan province of Vietnam.

Southeast Asia Hydropower Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Hydropower Installed Capacity and Forecast in GW, till 2029

- 4.3 Renewable Energy Mix, 2023

- 4.4 List of Major Upcoming Hydropower Projects, By Major Countries, Southeast Asia

- 4.5 List of On-going and Upcoming Hydropower Tenders, Southeast Asia

- 4.6 List of Major Hydropower Consulting Companies and Consortiums, Southeast Asia

- 4.7 Recent Trends and Developments

- 4.8 Government Policies and Regulations

-

4.9 Market Dynamics

- 4.9.1 Drivers

- 4.9.1.1 Increasing Investments in Hydropower Generation

- 4.9.1.2 Favorable Government Policies

- 4.9.2 Restraints

- 4.9.2.1 Adoption of Other Alternative Clean Energy Sources

- 4.10 Supply Chain Analysis

-

4.11 Porter's Five Forces Analysis

- 4.11.1 Bargaining Power of Suppliers

- 4.11.2 Bargaining Power of Consumers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes Products and Services

- 4.11.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Type

- 5.1.1 Large Hydropower

- 5.1.2 Small Hydropower

- 5.1.3 Pumped Storage

-

5.2 By Geography

- 5.2.1 Vietnam

- 5.2.2 Indonesia

- 5.2.3 Malaysia

- 5.2.4 Laos

- 5.2.5 Philippines

- 5.2.6 Thailand

- 5.2.7 Rest of Southeast Asia

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Vietnam Electricity Construction JSC

- 6.3.2 Andritz AG

- 6.3.3 Electricity Generating Authority of Thailand

- 6.3.4 PT Perusahaan Listrik Negara

- 6.3.5 Tenaga Nasional Berhad

- 6.3.6 Toshiba Corporation

- 6.3.7 General Electric Company

- 6.3.8 Aboitiz Power Corporation

- 6.3.9 Power Construction Corporation of China Ltd

- *List Not Exhaustive

- 6.4 Market Ranking Analysis

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Innovations in Efficient Hydropower Turbines

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Southeast Asia Hydropower Industry Segmentation

Hydropower, or hydroelectric power, is one of the largest and oldest renewable energy sources, which uses the natural flow of moving water to generate electricity. Hydropower technologies generate electricity by the elevation difference created by a dam or diversion structure between water flowing in one direction and out in the other direction.

The Southeast Asian hydropower market is segmented by type and geography. By type, the market is segmented into large hydropower, small hydropower, and pumped storage. The report also covers the installed capacity and forecasts for the Southeast Asian hydropower market across the major countries. The installed capacity and forecasts for each segment have been considered in Gigawatts (GW).

| By Type | Large Hydropower |

| Small Hydropower | |

| Pumped Storage | |

| By Geography | Vietnam |

| Indonesia | |

| Malaysia | |

| Laos | |

| Philippines | |

| Thailand | |

| Rest of Southeast Asia |

Need A Different Region or Segment?

Customize Now

Southeast Asia Hydropower Market Research FAQs

How big is the Southeast Asia Hydropower Market?

The Southeast Asia Hydropower Market size is expected to reach 73.78 gigawatt in 2025 and grow at a CAGR of 4.80% to reach 93.27 gigawatt by 2030.

What is the current Southeast Asia Hydropower Market size?

In 2025, the Southeast Asia Hydropower Market size is expected to reach 73.78 gigawatt.

Who are the key players in Southeast Asia Hydropower Market?

Vietnam Electricity Construction JSC, Tenaga Nasional Berhad, Andrtiz AG, PT Perusahaan Listrik Negara and Electricity Generating Authority of Thailand are the major companies operating in the Southeast Asia Hydropower Market.

What years does this Southeast Asia Hydropower Market cover, and what was the market size in 2024?

In 2024, the Southeast Asia Hydropower Market size was estimated at 70.24 gigawatt. The report covers the Southeast Asia Hydropower Market historical market size for years: 2024. The report also forecasts the Southeast Asia Hydropower Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Southeast Asia Hydropower Market Research

Mordor Intelligence provides a comprehensive analysis of the hydropower and hydroelectricity sectors. We leverage decades of expertise in energy market research. Our detailed report covers the full range of hydroelectric power infrastructure. This includes everything from large hydropower installations to micro hydropower systems. The analysis encompasses hydropower plant operations, hydroelectric facility management, and hydro energy technologies. It is available in an easy-to-download report PDF format, offering actionable insights for industry stakeholders.

The report examines key aspects of hydroelectric dam construction and water energy utilization. It also delves into water power systems, providing a detailed analysis of hydroelectric generator specifications and hydro turbine technologies. Stakeholders gain valuable insights into pumped storage hydropower developments and hydraulic power systems. Additionally, it highlights emerging hydropower technology trends. The analysis covers various market segments, from renewable hydropower to mini hydropower and small hydropower installations. It also examines hydropower generation efficiency and hydroelectric equipment innovations across Southeast Asia's diverse energy landscape.