Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 11.03 Billion |

| Market Size (2030) | USD 14.69 Billion |

| Growth Rate (2025 - 2030) | 5.91% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Southeast Asia Box Truck Market Analysis by Mordor Intelligence

The Southeast Asia Box Truck Market size is estimated at USD 11.03 billion in 2025, and is expected to reach USD 14.69 billion by 2030, at a CAGR of 5.91% during the forecast period (2025-2030). The rapid growth of e-commerce, mounting zero-emission mandates, and a growing preference for connected vehicles are the primary forces shaping demand. Intensifying competition between established Japanese brands and cost-aggressive Chinese entrants is redefining procurement strategies, while total-cost-of-ownership calculations increasingly favor telematics-enabled fleets. Governments in Indonesia, Thailand, and Malaysia are simultaneously tightening emission standards and offering fiscal incentives for Euro VI and electric trucks, prompting accelerated replacement of older diesel models. In parallel, partnerships such as BYD-Grab are catalyzing large-scale electrification initiatives that will lift unit sales of battery-powered trucks in urban delivery corridors.

Key Report Takeaways

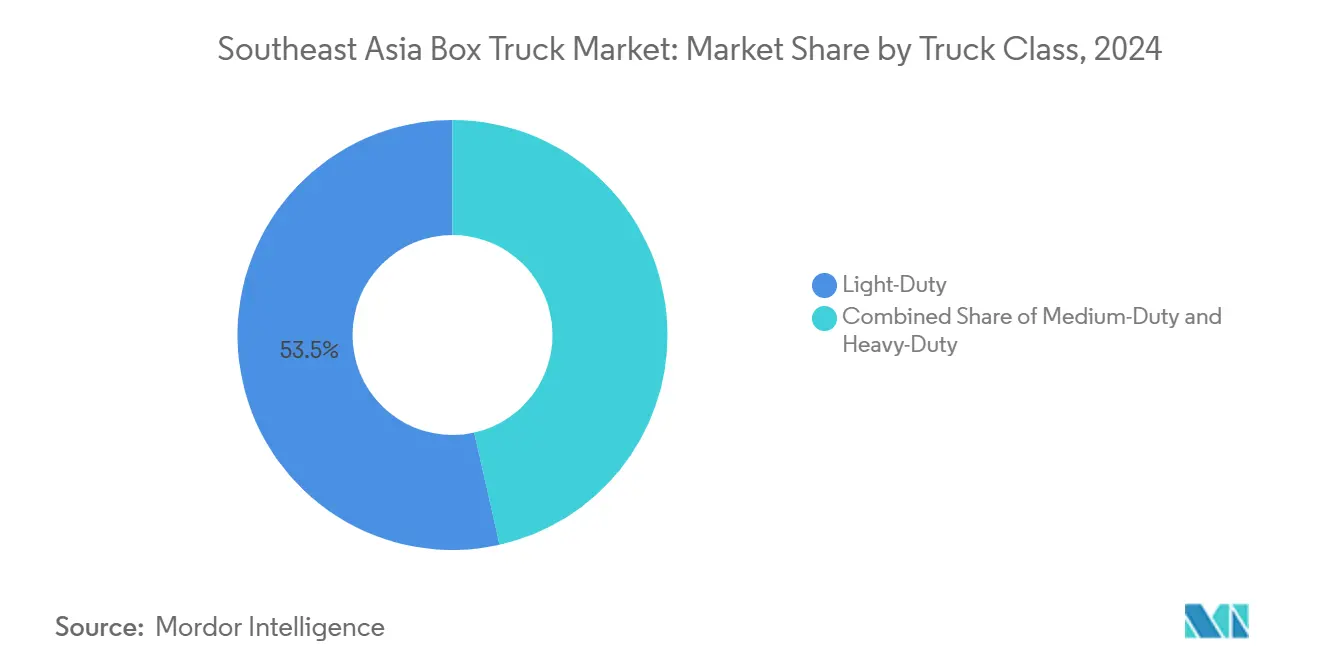

- By truck class, light-duty vehicles captured 53.47% share of the Southeast Asia box truck market size in 2024. Light-duty vehicles are also projected to record the fastest growth, with a 5.93% CAGR between 2025 and 2030.

- By fuel type, diesel engines retained the top position with a 73.14% share of the Southeast Asia box truck market size in 2024, and electric box trucks are poised to grow the quickest at a 6.03% CAGR through 2030.

- By body type, dry-freight boxes dominated the Southeast Asia box truck market with a 63.46% share in 2024, and refrigerated boxes are expected to register the highest CAGR of 6.08% through 2030.

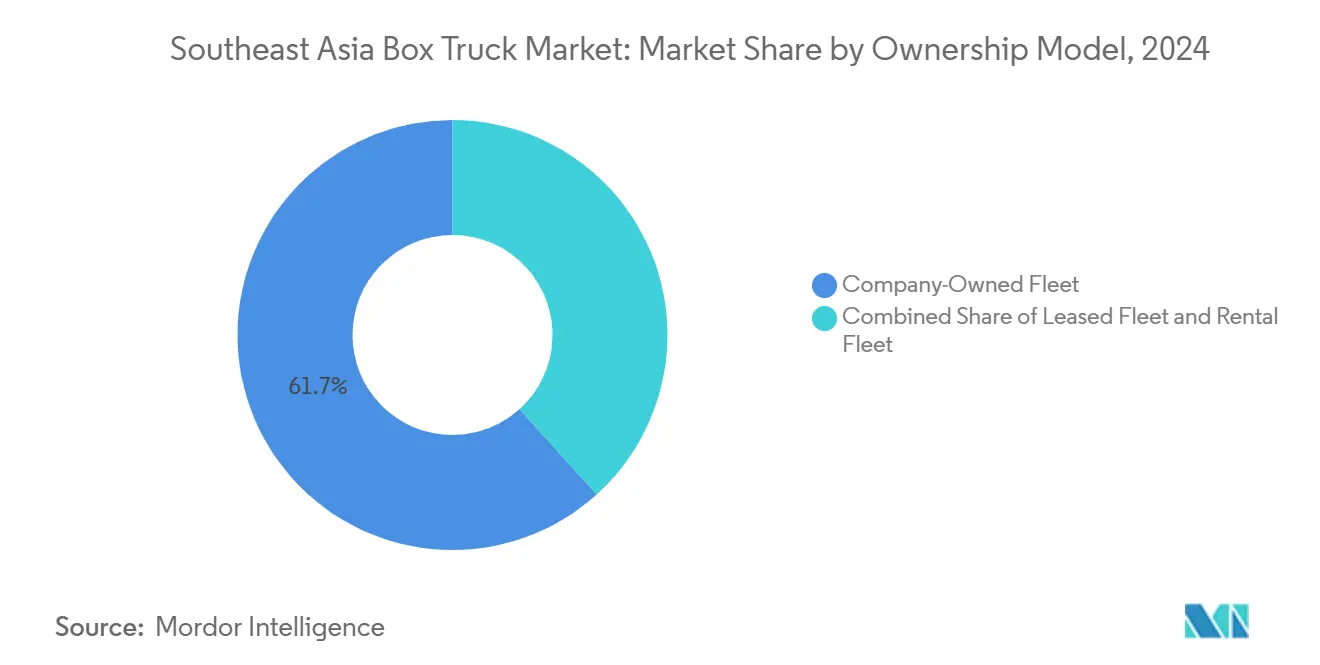

- By ownership model, company-owned fleets accounted for a 61.71% share of the Southeast Asia box truck market size in 2024, and leased fleets are expected to expand at a rate of 6.04% CAGR over the 2025-2030 period.

- By end user, transportation companies led demand, with a 38.83% share of the Southeast Asia box truck market size in 2024. Courier services are set to post the sharpest growth, at a 5.95% CAGR, through 2030.

- By geography, Indonesia commanded a 31.26% share of the Southeast Asia box truck market size in 2024, and Malaysia is expected to log the fastest growth rate of 5.97% during the forecast period.

Southeast Asia Box Truck Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive E-Commerce Parcel Volumes | +1.8% | Indonesia, Thailand, Malaysia, Philippines | Short term (≤ 2 years) |

| Rapid Urbanisation | +1.2% | Indonesia, Vietnam, Philippines | Medium term (2-4 years) |

| Ongoing ASEAN Highway Upgrades | +0.9% | Thailand, Malaysia, Vietnam | Long term (≥ 4 years) |

| Fiscal Incentives | +0.7% | Indonesia, Thailand, Malaysia | Medium term (2-4 years) |

| Cold-Chain Boom | +0.6% | Cambodia, Laos, Myanmar, Vietnam | Long term (≥ 4 years) |

| Singapore Zero-Emission Zone Mandates | +0.4% | Singapore, spillover to Malaysia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive E-Commerce Parcel Volumes

Rising digital spending significantly boosted regional e-commerce in 2023 and is projected to grow exponentially by 2025, triggering unprecedented demand for agile Class 2-3 box trucks capable of same-day fulfillment in crowded urban neighborhoods [1]“e-Conomy SEA 2024,” Google-Temasek-Bain, google.com . Parcel operators are investing in temperature-controlled units for grocery delivery and in-cab telematics to optimize routing. The Philippines exemplifies the surge, with light commercial vehicle registrations increasing slightly year-over-year in Q4 2024 [2]“Motor Vehicle Statistics Q4 2024,” Land Transportation Office, lto.gov.ph . Hyperlocal fulfillment hubs further amplify vehicle rotations, boosting utilization and lowering per-stop costs. Dynamic route planning tools, integrated with fleet management platforms, now underpin pricing models, driving a shift from motorcycles to box trucks for parcels exceeding 25 kilograms. Overall, e-commerce remains the single most significant catalyst for volume growth across the Southeast Asia box truck market.

Rapid Urbanization Driving Last-Mile Demand

By the end of the decade, urban populations in Jakarta, Manila, and Ho Chi Minh City are expected to experience significant growth, resulting in higher population density and shorter dispatch radii. Economic growth is anticipated to continue steadily over the next few years, as estimated by the Asian Development Bank, which highlights the rising consumption of packaged goods in urban centers [3]“Asian Development Outlook 2024,” Asian Development Bank, adb.org . Local regulations that restrict motorcycle deliveries during peak hours create windows during which box trucks dominate last-mile flows. Higher delivery density enhances route efficiency and supports the economics of advanced driver-assistance features, which reduce downtime. Vietnam’s logistics sector directly benefits from these urban trends, with shipment volumes projected to grow exponentially through 2030. Consequently, light-duty truck penetration deepens as operators replace their aging LCV fleets with modern units that meet stricter noise and emission standards.

Ongoing ASEAN Highway & Port Upgrades

ASEAN member states are making significant investments in multimodal corridors, streamlining transit times for freight, particularly benefiting medium-duty box trucks. In Thailand, dual-track railway and motorway projects have reduced the duration of the Bangkok-Chiang Mai journey, facilitating same-day trucking. Malaysia's Westports expansion is expected to significantly increase capacity, leading to higher trucking volumes to Klang Valley warehouses. Vietnam is heavily investing in transport infrastructure over the next few years, bolstering links between industrial parks and ports in Ho Chi Minh City. Logistics parks situated near deep-sea terminals are implementing hub-and-spoke models, with box trucks handling the final leg of the transportation process. Enhanced infrastructure not only reduces fuel consumption per ton-kilometer but also supports operators in upgrading to Euro VI trucks equipped with advanced after-treatment systems.

Fiscal Incentives for Euro VI / Stage V Trucks

Indonesia pairs its rollout of Euro VI standards with import-duty waivers and accelerated depreciation allowances, effectively offsetting the premium costs of selective catalytic reduction systems. Meanwhile, Thailand's EV 3.0 program, which offers significant excise tax cuts for locally assembled zero-emission trucks, has successfully attracted a substantial investment commitment from Isuzu, earmarked for battery production and vehicle assembly. In Malaysia, a full sales tax exemption on components that meet Stage V thresholds is facilitating the entry of advanced models from Japan and Europe. Such incentives are not only shortening payback periods for high-utilization fleets, prompting operators to expedite renewals, but are also hastening the adoption of telematics. This is crucial, as data from connected vehicles is essential for compliance monitoring in the evolving green-freight scorecards.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Acquisition Cost Vs. Light Vans | -0.8% | Indonesia, Philippines, Vietnam | Short term (≤ 2 years) |

| Sparse Alt-Fuel Charging Networks | -0.6% | Regional, concentrated in rural areas | Medium term (2-4 years) |

| Shortage Of EV- & Telematics-Ready Technicians | -0.5% | Regional, acute in smaller cities | Medium term (2-4 years) |

| Stringent Axle-Load Regulations | -0.4% | Thailand, Malaysia, Singapore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition Cost vs. Light Vans

Entry-level box trucks often carry a significant price premium compared to similar vans. This pricing strategy is prompting many owner-operators, who comprise the majority of regional logistics SMEs, to reconsider their choices. In Indonesia and the Philippines, limited access to low-interest financing means many buyers are resorting to cash purchases, making lighter vans a more attractive and financially accessible option. While Chinese truck manufacturers have made strides in bridging the gap, concerns about warranties and uncertainties regarding residual value remain prevalent. Operators recognize the benefits of telematics and extended maintenance intervals in terms of total cost of ownership. However, they hesitate at the prospect of initial expenses. Leasing emerges as a viable solution, but a lack of familiarity with operating-lease structures is hindering its adoption, especially outside of Malaysia and Singapore. Without an improvement in credit availability, the Southeast Asia box truck market risks losing more last-mile share to more affordable van alternatives.

Sparse Alt-Fuel Charging / Gas Networks

Despite rollouts in city centers, only a limited number of commercial-grade chargers are publicly accessible to serve the large population. This limitation confines electric truck missions primarily to urban routes based at depots. In rural areas, the lack of high-capacity charging stations or CNG stations hampers the electrification of medium-duty trucks for intercity shipments. Additionally, permitting timelines from power suppliers and land-use approvals significantly extend project lead times, which deters private investment. The fragmentation of standards among CHAdeMO, CCS2, and GB/T introduces equipment risks for early adopters. While battery-swap pilots, such as Isuzu’s EVision Cycle in Thailand, offer the allure of quicker turnarounds, they necessitate a dense fleet of vehicles to achieve economic viability. Given the current state of infrastructure, diesel and hybrid variants are poised to maintain their dominance in the long-haul and mixed-duty segments of Southeast Asia's box truck market.

Segment Analysis

By Truck Class: Light-Duty Vehicles Anchor Urban Economics

Light-duty trucks secured a commanding 53.47% slice of the Southeast Asia box truck market in 2024, supported by 5.93% CAGR prospects through 2030. Fleet managers favor smaller wheelbases, tighter turning radii, and lower operating costs for navigating congested streets and shuttling between intra-city warehouses. They often pair these vehicles with telematics platforms, such as Hino CONNECT, which offers cost-effective solutions for route optimization and significant fuel savings. Driven by retailers adopting micro-fulfillment strategies, the Southeast Asia box truck market for light-duty units is expected to witness substantial growth in the near future.

Medium-duty trucks, handling heavier payloads, are vital for cold-chain and construction missions. While their market share remains stable, it's also lucrative, due to operators' appreciation for high residuals and sturdy frames. Heavy-duty trucks, which represent a smaller portion of shipments, are indispensable for long-haul and cross-border transportation. Here, stringent ASEAN axle-load regulations favor advanced suspension systems. Connectivity is becoming ubiquitous across truck classes, with aftermarket telematics evolving into standard features, paving the way for pay-per-use insurance models.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Fuel Type: Electric Traction Gains Momentum

Diesel engines are expected to retain 73.14% share of the Southeast Asia box truck market in 2024, whereas electric drivelines are projected to deliver the highest 6.03% CAGR through 2030. In downtown Singapore and other low-emission zones, government incentives, falling battery prices, and stricter emission caps are driving fleets to adopt zero-tailpipe units. Two key economic factors are driving this shift: electricity costs are significantly lower than those of diesel on a per-kilometer basis, and brake-energy regeneration technology substantially reduces the need for service-brake replacements. In the coming years, the market for electric box trucks in Southeast Asia is anticipated to grow considerably. While hybrids and CNG options cater to specific needs—thriving where grid capacity or natural gas prices align with operational costs—gasoline is primarily reserved for short-haul, budget-conscious operators.

BYD, in collaboration with Grab, has pioneered battery leasing and battery-as-a-service packages, alleviating upfront capital burdens and ensuring value at the end of the battery's life. As route-planning algorithms advance, fleets are fine-tuning battery sizes to match mission profiles, striking a balance between payload and range. Additionally, telemetry-driven charging schedules boost asset uptime, further propelling the adoption of electric units in Southeast Asia's box truck market.

By Body Type: Refrigerated Boxes Ride the Cold-Chain Wave

Dry-freight boxes dominate with 63.46% share, addressing general cargo and parcel applications. Refrigerated boxes, however, are experiencing the fastest 6.08% CAGR as Southeast Asians increase consumption of perishable and pharma products. Temperature excursions can slash shelf life by two-fifths, prompting shippers to specify multi-zone refrigeration units with IoT monitoring. The Southeast Asia box truck market share for refrigerated bodies is projected to cross one-fifth among new builds by 2030. Curtain-side formats hold a niche in palletized goods that require side loading, while tail-lift boxes grow in tandem with bulk e-grocery orders in major metros.

Service providers like SJWD Logistics have expanded their cold-chain fleets by a minimal amount in 2024 to meet the rising demand for food-retail contracts. Integrated data loggers now feed compliance dashboards aligned with HACCP standards, permitting real-time intervention and lowering spoilage claims. Refrigerant transitions to lower GWP gases also align with ASEAN’s Kigali Amendment commitments, adding another compliance dimension to body-builder specifications.

By Ownership Model: Leasing Converts Capex to Opex

Company-owned fleets command 61.71% share of the Southeast Asia box truck market in 2024 but face erosion as leasing houses roll out bundled telematics, preventive maintenance, and assured residual buybacks. Leased fleets are expected to post a 6.04% CAGR through 2030, driven in part by IFRS 16 accounting, which keeps operating leases off balance sheets. Subscription-based truck-as-a-service packages are gaining traction in the Southeast Asia box truck industry. These packages bundle monthly fees that encompass the vehicle, insurance, roadside assistance, and software. For example, SafeTruck oversees a significant number of leased cars in Malaysia and Indonesia, leveraging predictive analytics to achieve a notable reduction in vehicle downtime.

Rental fleets meet peak-season spikes and short-term project needs, capturing SME customers who are wary of long-term commitments. Flexible lease terms, ranging from 12 to 48 months, allow for technology refresh cycles that align with evolving emission quotas. Consequently, residual-value management and data-driven asset rotation are becoming core competencies for lessors operating in the Southeast Asia box truck market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Courier Networks Tops the Growth Chart

Transportation firms account for 38.83% share of the Southeast Asia box truck market in 2024, as they manage port-to-warehouse and factory-to-distribution flows. Courier services, buoyed by a 5.95% CAGR outlook, are the fastest-rising clientele, mirroring the digital commerce boom. Mober's recent capital raise, aimed at significantly expanding its electric truck fleet, underscores the industry's growing commitment to sustainability. Simultaneously, retailers are establishing their own fleets to enhance last-mile visibility, often collaborating with third-party tech platforms for efficient dispatch management.

While construction and government sectors represent a niche market, they exhibit consistent demand, often customizing bodies or chassis configurations to suit their unique requirements. Across various segments, AI-driven routing has successfully reduced empty backhaul rates, resulting in notable fuel savings and lower carbon emissions in the Southeast Asian box truck market.

Geography Analysis

In 2024, Indonesia held a dominant 31.26% share of the Southeast Asia box truck market. Indonesia's significant stake underscores its domestic production incentives and unique transport needs as an archipelagic nation. With the Euro VI rollout set for enforcement in the near future, there's a surge in early truck procurements to meet these standards. Meanwhile, port projects in Tanjung Priok and Patimban are bolstering multimodal transport flows. Given that fuel constitutes a substantial portion of operating costs, carriers are increasingly adopting telematics. This shift allows them to monitor consumption and reduce idling effectively.

Malaysia is poised to experience the swiftest growth rate at 5.97% during the forecast period, capitalizing on Westports’ transshipment expansion and Kuala Lumpur’s emergence as a regional retail hub. Its fleet operators benefit from cross-border movements with Singapore and Thailand, achieving enhanced kilometer utilization and improved returns on Euro VI vehicles. Additionally, 5G-enabled vehicle-to-infrastructure pilots on the North-South Expressway are alleviating congestion, bolstering schedule reliability for high-service-level contracts.

In the Southeast Asia box truck market, Thailand, Vietnam, the Philippines, and Singapore each carve out unique niches. Thailand enjoys advantages from established OEM bases and EV subsidies. In contrast, Vietnam dominates, with its trucking industry handling the majority of the nation's cargo, resulting in significant annual volumes. The Philippines thrives on robust household consumption, while Singapore's push for a zero-emission zone accelerates technological advancements in neighboring Malaysian depots. Meanwhile, frontier markets like Cambodia, Laos, and Myanmar are making strides by investing in highways and simplifying customs. They are gradually integrating into cross-border trucking networks, unveiling new demand opportunities.

Competitive Landscape

The Southeast Asia box truck market is moderately fragmented. Isuzu, Hino, and Mitsubishi Fuso collectively hold roughly two-fifths of regional registrations, anchoring brand loyalty through parts availability and dealer coverage. Chinese challengers such as BYD and Foton are pressing on price and electrification, capturing contracts with app-based logistics firms that value TCO savings. The planned merger of Hino, Mitsubishi Fuso, and Toyota with Daimler Truck will harness resources to accelerate battery and software development.

European makers Volvo and Scania focus on premium, safety-oriented fleets, carving out a minimal share with features like Level 2 driver assistance. Start-ups are adding pressure by offering truck-as-a-service models with guaranteed uptime, forcing incumbents to enhance digital after-sales offerings. Partnerships addressing infrastructure—such as Isuzu and Mitsubishi Corporation’s battery-swap pilot in Bangkok—seek to remove charging barriers. Competitive intensity is set to intensify around data ownership, with OEMs vying to embed proprietary telematics that secure service revenue.

Price competition remains acute in the light-duty segment, whereas technology differentiation governs margins in the medium- and heavy-duty ranges. Manufacturers with local assembly and homologation expertise enjoy faster time-to-market for new emission norms, a crucial edge as regulators converge on Euro VI and UNECE safety standards. Overall, scale, connectivity, and compliance form the strategic tripod underpinning long-term positioning across the Southeast Asia box truck market.

Southeast Asia Box Truck Industry Leaders

-

Isuzu Motor Co. Ltd

-

Mitsubishi Fuso Truck and Bus Corporation

-

Ford Motor Company

-

IVECO GROUP Company (CNH Industrial NV)

-

Hino Motors, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: Hino Motors and Mitsubishi Fuso have signed a definitive merger agreement to create a holding company for heavy commercial vehicles, led by Karl Deppen, which will pool their electrification and autonomous R&D efforts.

- March 2024: Isuzu Motors has committed THB 240 billion (approximately USD 6.6 billion) to establishing electric pickup and battery manufacturing lines in Thailand by 2030, aligning with the government’s 30@30 zero-emission policy.

Southeast Asia Box Truck Market Report Scope

A Box truck is a commercial motor vehicle, which is designed in such a way that each axle, from the tip of the cab to the rear of the trailer, is connected by a single frame.

The Southeast Asia box truck market is segmented into type, capacity type, propulsion, application, and country. Based on the type, the market is segmented into refrigerated box trucks and non-refrigerated box trucks. Based on the capacity type, the market is segmented into light-duty box trucks and medium and heavy-duty box trucks. Based on the propulsion, the market is segmented into Internal combustion engines and electric. Based on the application, the market is segmented into Industrial, commercial, and other applications. Based on geography, the market is segmented into Thailand, Indonesia, Vietnam, Malaysia, Singapore, the Philippines, and the Rest of Southeast Asia.

For each segment, market sizing and forecasting have been conducted based on value (USD) and Volume (Units).

By Truck Class

| Light-Duty (Class 2–3) |

| Medium-Duty (Class 4–6) |

| Heavy-Duty (Class 7–8) |

By Fuel Type

| Diesel |

| Gasoline |

| Electric |

| Hybrid |

| CNG/LPG |

By Body Type

| Dry Freight Box |

| Refrigerated Box |

| Curtain Side Box |

| Tail-Lift Box |

By Ownership Model

| Company-Owned Fleet |

| Leased Fleet |

| Rental Fleet |

By End User

| Transportation Companies |

| Retailers |

| Courier Services |

| Construction Firms |

| Government Agencies |

By Geography

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| Rest of Southeast Asia |

| By Truck Class | Light-Duty (Class 2–3) |

| Medium-Duty (Class 4–6) | |

| Heavy-Duty (Class 7–8) | |

| By Fuel Type | Diesel |

| Gasoline | |

| Electric | |

| Hybrid | |

| CNG/LPG | |

| By Body Type | Dry Freight Box |

| Refrigerated Box | |

| Curtain Side Box | |

| Tail-Lift Box | |

| By Ownership Model | Company-Owned Fleet |

| Leased Fleet | |

| Rental Fleet | |

| By End User | Transportation Companies |

| Retailers | |

| Courier Services | |

| Construction Firms | |

| Government Agencies | |

| By Geography | Indonesia |

| Malaysia | |

| Philippines | |

| Singapore | |

| Thailand | |

| Vietnam | |

| Rest of Southeast Asia |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Southeast Asia box truck market in 2025?

The market is expected to reach USD 11.03 billion in 2025 and is projected to grow to USD 14.69 billion by 2030.

Which truck class leads deliveries across Southeast Asian cities?

Light-duty Class 2-3 trucks account for 53.47% of total shipments, offering superior maneuverability for urban routes.

Which fuel type is growing fastest in Southeast Asian box trucks?

Battery-electric models exhibit the fastest 6.03% CAGR as incentives and lower operating costs drive fleet upgrades.

Why are refrigerated box trucks gaining traction?

The rising demand for fresh food and pharmaceutical logistics is driving refrigerated bodies to a 6.08% CAGR through 2030.

What factors drive leasing over ownership in commercial fleets?

High upfront prices, rapid tech obsolescence, and bundled telematics packages are shifting fleets toward 6.04% CAGR growth in leasing.

Which country registers the swiftest growth in box truck demand?

Malaysia leads with a projected 5.97% CAGR to 2030, buoyed by port expansion and cross-border trade flows.

Page last updated on: