Market Size of Southeast Asia Bioplastics Industry

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| Forecast Data Period | 2024 - 2029 |

| Historical Data Period | 2019 - 2022 |

| CAGR | > 10.00 % |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Southeast Asia Bioplastics Market Analysis

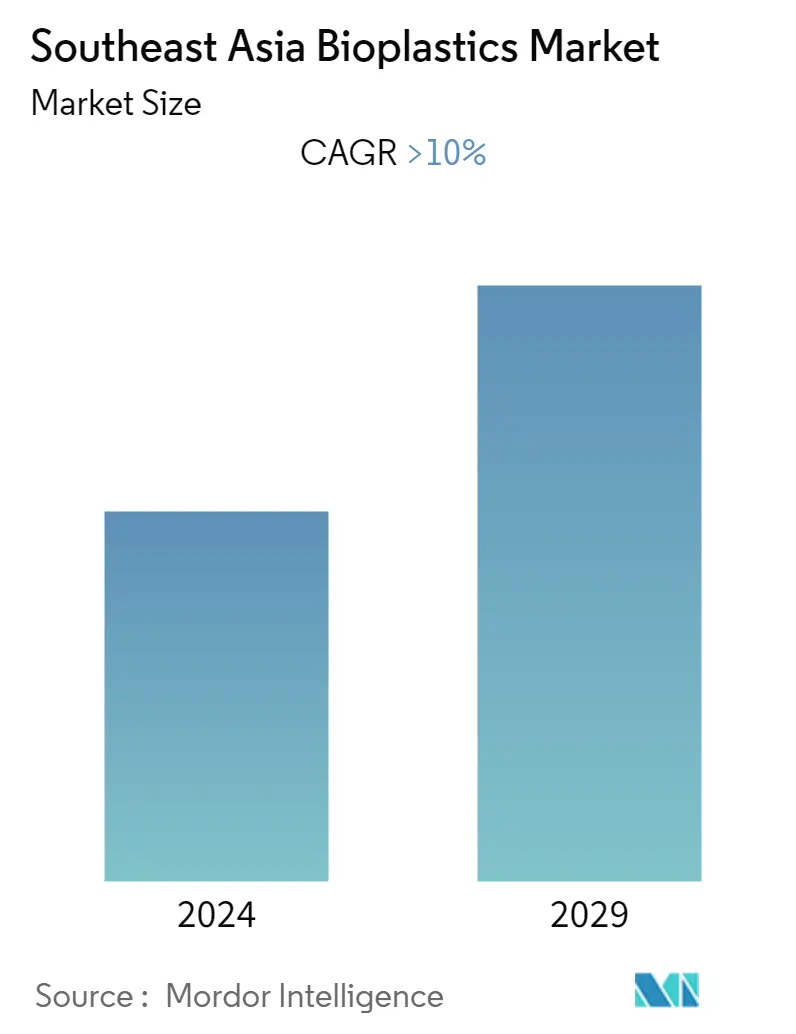

The Southeast Asia bioplastics market is expected to register a CAGR of over 10% during the forecast period.

COVID-19 negatively impacted the production and supply of bioplastics during the lockdown. However, the demand from the packaging segment surged due to the increasing use of online food and e-commerce service during the pandemic. After 2020, the market improved steadily due to the continuous activities in the Southeast Asian region.

- Growing demand for bioplastics in packaging and environmental factors encouraging a paradigm shift is expected to drive the bioplastics market's growth in Southeast Asia.

- However, the availability of cheaper alternatives is the primary factor hindering the market's growth.

- Growing use in the electronics industry will likely be an opportunity.

- Indonesia is expected to dominate the bioplastics market in Southeast Asia and is also likely to witness the highest CAGR during the forecast period.

Southeast Asia Bioplastics Industry Segmentation

Bioplastics are a type of plastic produced from natural resources such as sugar cane, sugar beet, corn starch, potato starch, vegetable fats and oils, wood pulp, wheat straw, and other natural resources. To get the final product, these natural resources follow numerous processes, such as hydrolysis and fermentation, dehydration/esterification/compounding, and polymerization.

The Southeast Asia bioplastics market is segmented by type, application, and geography. By type, the market is segmented into bio-based biodegradables (starch-based, polylactic acid (PLA), polyhydroxyalkanoates (PHA), polyesters (PBS, PBAT, and PCL), and other bio-based biodegradables) and bio-based non-biodegradables (bio polyethene terephthalate (PET), bio polyethene, bio polyamides, bio poly trimethylene terephthalate, and other non-biodegradables). By application, the market is segmented into flexible packaging, rigid packaging, automotive and assembly operations, agriculture and horticulture, construction, textiles, electrical and electronics, and other applications. The report also covers the market size and forecasts for the bioplastics market in 5 major countries across the Southeast Asia region. For each segment, the market sizing and forecasts have been done based on volume (kilotons).

| Type | |||||||

| |||||||

|

| Application | |

| Flexible Packaging | |

| Rigid Packaging | |

| Automotive and Assembly Operations | |

| Agriculture and Horticulture | |

| Construction | |

| Textiles | |

| Electrical and Electronics | |

| Other Applications |

| Geography | |

| Indonesia | |

| Malaysia | |

| Philippines | |

| Singapore | |

| Thailand | |

| Rest of Southeast Asia |

Southeast Asia Bioplastics Market Size Summary

The Southeast Asia bioplastics market is poised for significant growth, driven by increasing demand in the packaging sector and a shift towards environmentally friendly alternatives. The market experienced a downturn during the COVID-19 pandemic due to disruptions in production and supply chains. However, the surge in demand for packaging solutions, particularly from the e-commerce and food sectors, has spurred recovery. The region's focus on sustainable practices and the growing use of bioplastics in flexible packaging are key factors propelling market expansion. Despite challenges posed by the availability of cheaper conventional plastics, the market is expected to benefit from opportunities in the electronics and automotive industries. Indonesia is anticipated to lead the market, supported by its robust palm oil industry and innovative bioplastic applications.

The bioplastics market in Southeast Asia is characterized by its consolidation, with major players like TotalEnergies Corbion and Indorama Ventures Public Company Limited driving innovation and production. The region's diverse applications of bioplastics, ranging from packaging to agriculture and construction, underscore its potential for growth. Initiatives such as tax exemptions in Thailand and new manufacturing facilities in Indonesia and Thailand further bolster the market's prospects. The development of bioplastics from agricultural byproducts, such as palm oil waste in Malaysia, highlights the region's commitment to sustainable solutions. As the demand for eco-friendly materials continues to rise, the Southeast Asia bioplastics market is set to experience robust growth over the forecast period.

Southeast Asia Bioplastics Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Drivers

-

1.1.1 Growing Demand for Bioplastics in Packaging

-

1.1.2 Environmental Factors Encouraging a Paradigm Shift

-

-

1.2 Restraints

-

1.2.1 Availability of Cheaper Alternatives

-

1.2.2 Other Restraints

-

-

1.3 Industry Value Chain Analysis

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Suppliers

-

1.4.2 Bargaining Power of Consumers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitute Products and Services

-

1.4.5 Degree of Competition

-

-

-

2. MARKET SEGMENTATION (Market Size in Volume)

-

2.1 Type

-

2.1.1 Bio-based Biodegradables

-

2.1.1.1 Starch-based

-

2.1.1.2 Polylactic Acid (PLA)

-

2.1.1.3 Polyhydroxy Alkanoates (PHA)

-

2.1.1.4 Polyesters (PBS, PBAT and PCL)

-

2.1.1.5 Other Bio-based Biodegradables

-

-

2.1.2 Bio-based Non-biodegradables

-

2.1.2.1 Bio Polyethylene Terephthalate (PET)

-

2.1.2.2 Bio Polyethylene

-

2.1.2.3 Bio Polyamides

-

2.1.2.4 Bio Polytrimethylene Terephthalate

-

2.1.2.5 Other Non-biodegradables

-

-

-

2.2 Application

-

2.2.1 Flexible Packaging

-

2.2.2 Rigid Packaging

-

2.2.3 Automotive and Assembly Operations

-

2.2.4 Agriculture and Horticulture

-

2.2.5 Construction

-

2.2.6 Textiles

-

2.2.7 Electrical and Electronics

-

2.2.8 Other Applications

-

-

2.3 Geography

-

2.3.1 Indonesia

-

2.3.2 Malaysia

-

2.3.3 Philippines

-

2.3.4 Singapore

-

2.3.5 Thailand

-

2.3.6 Rest of Southeast Asia

-

-

Southeast Asia Bioplastics Market Size FAQs

What is the current Southeast Asia Bioplastics Market size?

The Southeast Asia Bioplastics Market is projected to register a CAGR of greater than 10% during the forecast period (2024-2029)

Who are the key players in Southeast Asia Bioplastics Market?

TotalEnergies Corbion , PTT MCC Biochem Co., Ltd. , Indorama Ventures Public Company Limited , AN PHÁT BIOPLASTICS and THANTAWAN INDUSTRY PLC are the major companies operating in the Southeast Asia Bioplastics Market.