Southeast Asia Advertising Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

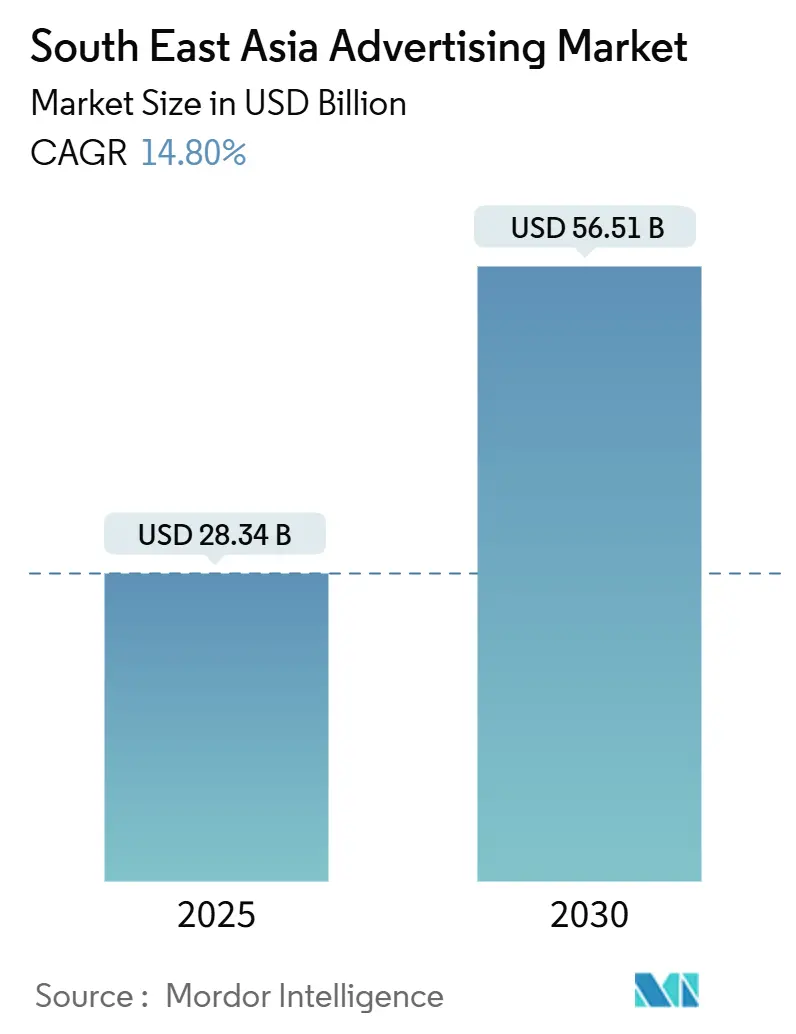

| Market Size (2025) | USD 28.34 Billion |

| Market Size (2030) | USD 56.51 Billion |

| Growth Rate (2025 - 2030) | 14.80% CAGR |

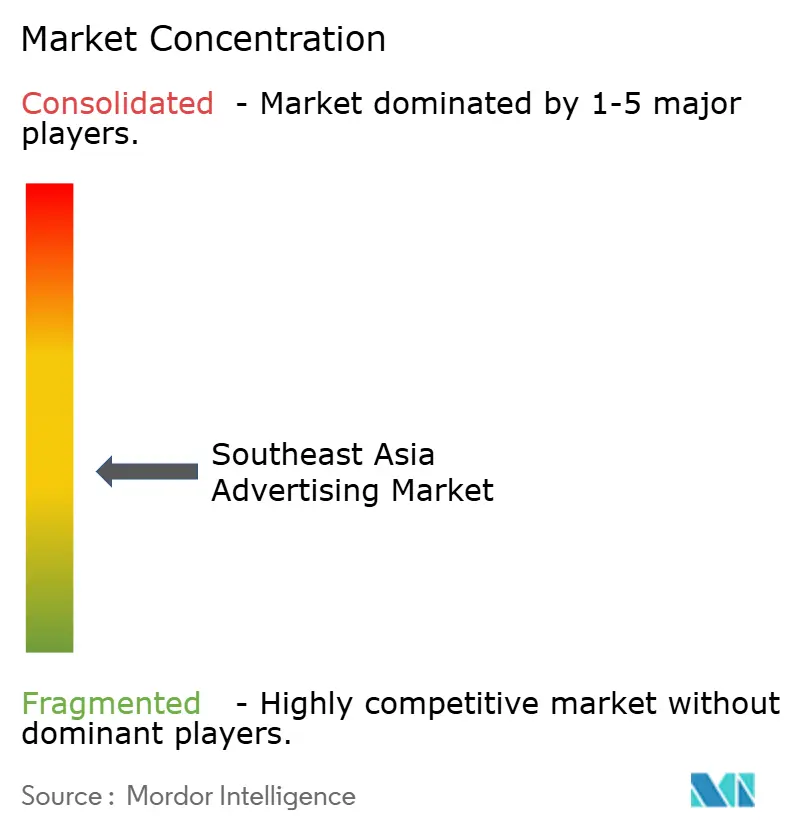

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Southeast Asia Advertising Market Analysis by Mordor Intelligence

The South East Asia Advertising market size stands at USD 28.34 billion in 2025 and is forecast to reach USD 56.51 billion by 2030, expanding at a 14.8% CAGR. Revenue growth rides on rapid mobile-first digital adoption, AI-enabled campaign optimization, and government grants that help small businesses advertise online. While traditional channels still concentrate spending, the shift toward automated, data-rich formats is unmistakable, especially as monthly mobile data usage per smartphone is set to climb from 13 GB in 2023 to 59 GB by 2030.[1]GSMA, “The Mobile Economy Asia Pacific 2024,” GSMA.COM Super-app ecosystems, expanding retail media networks, and stronger measurement standards for Digital Out-of-Home (DOOH) are widening the channel mix and enhancing return on ad spend for brands across the region.

Key Report Takeaways

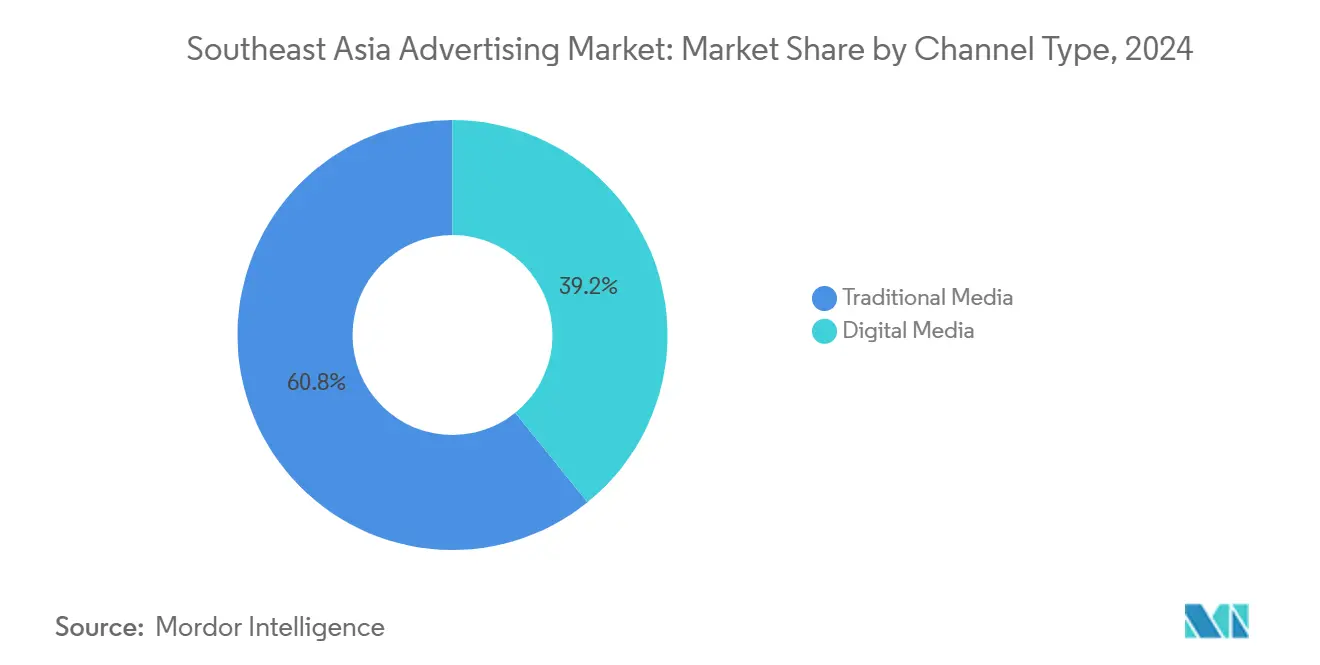

- By channel type, traditional media led with 60.8% revenue share of the Southeast Asia Advertising market in 2024, whereas digital media is projected to grow at 15.6% CAGR through 2030.

- By advertising medium, television held 29.8% of the Southeast Asia Advertising market share in 2024, while Digital Out-of-Home is advancing at a 16.1% CAGR to 2030.

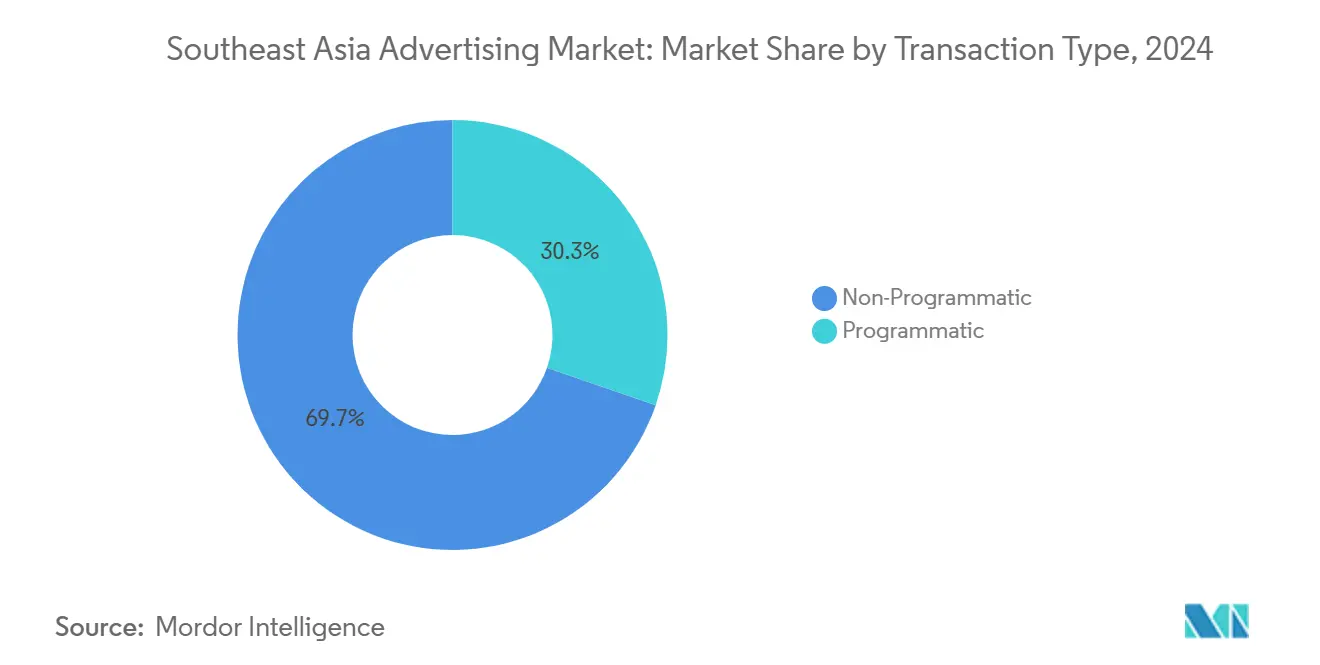

- By transaction type, non-programmatic buying captured a 69.7% share of the Southeast Asia Advertising market in 2024; programmatic approaches record the fastest CAGR at 15.7% through 2030.

- By end-user industry, Fast-Moving Consumer Goods accounted for 29.2% of the Southeast Asia Advertising market size in 2024, but retail and e-commerce are forecast to expand at 16% CAGR to 2030.

- By country, Singapore commanded a 32.8% share of the Southeast Asia Advertising market in 2024, whereas Vietnam posts the highest projected CAGR at 16.3% through 2030.

Southeast Asia Advertising Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising mobile broadband penetration | +3.2% | APAC core, strongest in Vietnam, Indonesia | Medium term (2-4 years) |

| Accelerated uptake of programmatic DOOH | +2.8% | Singapore, Malaysia, Thailand urban centers | Short term (≤ 2 years) |

| Government-led digital-first SME incentives | +2.1% | Singapore, Malaysia, Indonesia, Philippines | Long term (≥ 4 years) |

| AI-driven dynamic creative optimization | +1.9% | Global, early adoption in Singapore, Thailand | Medium term (2-4 years) |

| Super-app advertising ecosystems | +2.4% | Indonesia, Singapore, Malaysia, Thailand | Short term (≤ 2 years) |

| Cross-border e-commerce boom | +2.6% | Regional, concentrated in major cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Mobile Broadband Penetration

Mobile connectivity is redefining ad reach across the Southeast Asia Advertising market. GSMA projects that monthly data usage will surge more than fourfold by 2030, opening space for high-bit-rate video and immersive formats that were previously bandwidth-constrained. With Indonesia’s fixed broadband penetration below 20%, mobile is the default digital gateway, prompting advertisers to adopt location-based targeting and video-first creative. Faster speeds also enrich the data available to programmatic platforms, turning real-time engagement metrics into the primary mechanism for buying and optimizing inventory.

Accelerated Uptake of Programmatic DOOH

Digital billboards now stream dynamic ads shaped by live weather or traffic feeds. A July 2024 deal between Moving Walls and GroupM gave Malaysian buyers verified DOOH inventory, mitigating historical viewability doubts.[2]Moving Walls, “GroupM Partnership for Verifiable DOOH in Malaysia,” MOVINGWALLS.COM In dense Singapore and Bangkok, algorithmic scheduling lets brands rotate creative by daypart, congested routes, or in-market behaviors pulled from mobile devices. Standard-setting bodies such as the Open Measurement in Out-of-Home Group released open-source impression frameworks, bringing the accountability that advertisers expect from online channels.

Government-Led Digital-First SME Incentives

Policy pushes are turning traditional mom-and-pop stores into online advertisers. Singapore’s SMEs Go Digital has enrolled 30,000 companies in starter tech packs. Indonesia’s MSMEs Go Digital crossed 9.2 million firms, each now pursuing search, social, or marketplace ads to win customers in crowded e-commerce ecosystems. Cash-grant programs in Malaysia and ASEAN-wide training from Go Digital ASEAN accelerate onboarding and create a snowball effect in ad spend, because every digitized merchant must build online visibility to survive.

AI-Driven Dynamic Creative Optimization

Regional adopters such as FreakOut employ predictive algorithms that swap imagery, calls-to-action, or language variants in milliseconds, raising click-through rates while shrinking production cycles. Vietnam’s 89% enterprise AI adoption rate signals a receptive environment. As South East Asia hosts dozens of ethnicities and languages, AI’s ability to localize at scale is invaluable, allowing a single campaign shell to deliver culturally tuned iterations without manual editing. Real-time performance feedback loops further let buyers fine-tune bids and placements.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High fragmentation of publisher inventory | -1.8% | Malaysia, Indonesia, Philippines rural areas | Medium term (2-4 years) |

| Opaque agency rebate practices | -1.4% | Regional, strongest in Singapore, Thailand | Short term (≤ 2 years) |

| Stringent personal-data regulations | -2.1% | Singapore, Malaysia, Thailand, Indonesia | Long term (≥ 4 years) |

| Limited measurement standards for DOOH | -1.2% | Urban centers across region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Fragmentation of Publisher Inventory

Malaysia counts more than 300 billboard owners, forcing buyers to stitch together campaigns piecemeal.[3]CtrlShift, “AMP Marketplace Launch,” CTRLSHIFT.COM CtrlShift’s AMP marketplace now aggregates inventory from seven major publishers, but scale remains limited. Smaller digital publishers across Indonesia and the Philippines compound the problem, lacking common ad-tech stacks or transparency in pricing. Fragmentation raises transaction costs, deters new entrants, and slows the growth trajectory of programmatic spend within the Southeast Asia Advertising market.

Opaque Agency Rebate Practices

Regulatory probes in neighboring India uncovered rebate and price-collusion issues at global holding groups, spurring brand-side calls for stricter audits. In Southeast Asia, rebate secrecy undermines media efficiency, nudging some advertisers toward in-house trading desks. Heightened compliance duties under local Personal Data Protection Acts add complexity and increase liability for agencies that cannot demonstrate transparent data handling.

Segment Analysis

By Channel Type: Digital Acceleration Reshapes Traditional Dominance

Traditional channels retained a 60.8% share of the South East Asia Advertising market in 2024, buoyed by entrenched TV viewership among rural and older audiences. Yet the segment’s modest growth contrasts with digital media’s 15.6% CAGR, signaling an irreversible consumption pivot fueled by smartphones and cheaper data plans. Rapid gains stem from programmatic buying efficiencies and granular targeting that television or print cannot match. Thailand marked a pivotal moment in 2024 when digital ad spend surpassed TV, taking 45% versus 35%, underlining consumer migration to online video and social feeds.

Digital’s advance is accelerated further by cross-border e-commerce campaigns demanding real-time localization, a capability only algorithmic channels can deliver. Meanwhile, cinema and classic outdoor formats remain relevant in dense metros, where premium audiences value immersive, brand-safe settings. Still, the differential in performance metrics, attribution, and audience data tilts budgets heavily toward digital, reinforcing a feedback loop that reshapes the spending mix of the Southeast Asia Advertising market over the forecast period.

By Advertising Medium: Television Dominance Faces DOOH Disruption

Television’s 29.8% stake in 2024 still positions it as the most lucrative single medium, reflecting both legacy habit and mass-reach efficiency. However, Digital Out-of-Home exhibits the highest trajectory at 16.1% CAGR, aided by falling screen costs, 5G connectivity, and standardized impression counting frameworks. Advertisers appreciate DOOH’s ability to refresh creative by daypart or trigger ads based on localized stimuli such as weather or traffic congestion.

Traditional print and radio keep niche appeal, newspaper inserts among older readers, and commuter-time radio ads on high-congestion routes, but their share contracts as measurement gaps widen. Cinema capitalizes on blockbuster releases for premium placements, yet venue capacity caps growth. Digital advertising covering search, social, display, and OTT video continues to siphon dollars from broadcast budgets, riding on better attribution models and AI-enhanced creative testing that optimize in-flight performance for brands across the Southeast Asia Advertising market.

By Transaction Type: Programmatic Revolution Accelerates

Non-programmatic deals held 69.7% of 2024 spend, sustained by direct relationships and premium sponsorship packages that emphasize human negotiation. Nonetheless, programmatic trading’s 15.7% CAGR signals rapid automation of the Southeast Asia Advertising market. The model’s appeal lies in efficiency gains, precise audience overlays, and dynamic pricing. Private marketplaces and header-bidding setups bridge the gap for cautious brands, allowing real-time bidding while preserving brand safety.

FreakOut’s June 2024 integration of predictive AI into its exchange showcases the layering of machine learning onto bidding engines, enabling creatives to morph in sync with audience sentiment. DOOH is the newest frontier; algorithmic scheduling now optimizes billboard inventory similar to online display, adjusting in seconds instead of days. As more publishers onboard supply-side platforms, the share of automated deals will expand, slowly shrinking the manual insertion order market.

By End-User Industry: FMCG Leadership Yields to Retail Innovation

Fast-moving Consumer Goods dominated with 29.2% of the Southeast Asia Advertising market size in 2024, relying on continuous brand-building and impulse-purchase reinforcement. Yet retail and e-commerce’s 16% CAGR points to a structural pivot. Marketplace operators are transforming into media sellers, carving out self-serve dashboards where merchants bid for shelf-space-like ad inventory. Shopee’s GMV heft intensifies this phenomenon, while TikTok Shop recorded USD 4.4 billion GMV in 2024, blending content and commerce in one scroll.

Automotive, BFSI, and Telecom maintain healthy spends tied to product launches and service renewals, and Healthcare benefits from aging populations and rising preventive care messaging. Travel advertising rebounds post-pandemic, targeting pent-up wanderlust through mobile-first video journeys. Across categories, AI-driven personalization increases relevance, allowing smaller budgets to punch above their weight in the Southeast Asia Advertising industry.

Geography Analysis

Singapore’s dominance is anchored in its 32.8% share of the Southeast Asia Advertising market revenue, a position reinforced by advanced ad-tech stacks and a regulatory framework that codifies data-handling standards under the Personal Data Protection Act. Urban density ensures near-instant audience aggregation for DOOH screens, while SMEs Go Digital funnels new local advertisers online. Multinational agencies cluster here, streamlining cross-border media orchestration for campaign rollouts across ASEAN.

Vietnam, growing at 16.3% CAGR, leverages rising middle-class disposable income and nationwide 4G/5G upgrades. Government pushes to digitize SMEs, and high AI adoption rates allow even regional banks and CPG firms to test predictive-creative formats at scale. The market’s youthful demographics embrace short-form video and live commerce, nudging budgets from display banners to interactive streaming.

Indonesia, Thailand, Malaysia, and the Philippines collectively account for a sizable portion of the Southeast Asia Advertising market. Indonesia’s geographic sprawl challenges national targeting, but super-app ecosystems help advertisers zero in on provincial clusters. Thailand’s inflection point digital spend surpassing TV recalibrates media mixes, while Malaysia grapples with fragmented inventory yet benefits from standardized DOOH metrics through GroupM-Moving Walls collaboration. The Philippines taps its English-speaking talent pool to export creative services, feeding an upward cycle of domestic expertise and ad tech innovation. Secondary markets such as Cambodia and Laos remain nascent but could scale rapidly once basic infrastructure milestones are met.

Competitive Landscape

The Southeast Asia Advertising market is moderately fragmented, with holding companies Dentsu, GroupM, Omnicom, Publicis, and Havas maintaining a broad service moat yet losing exclusivity as region-native independents and tech platforms expand. These incumbents still command high-value brand mandates, integrating TV planning with social, search, and DOOH. However, transparency concerns over rebates spur some multinationals to demand third-party audits or experiment with in-house buying units.

Super-apps such as Grab and Gojek complicate the ecosystem by offering advertisers closed-loop data spanning ride-hailing, payments, and delivery, potentially bypassing traditional agencies. Retail media networks on Shopee or Lazada similarly sell performance-based placements that capture spend once reserved for display or search. Agencies are increasingly integrating AI-driven tools into their campaign planning to maintain a competitive edge. For instance, FreakOut has partnered with Neurons to utilize neuroanalytics for predicting attention hotspots. Meanwhile, GroupM's DOOH verification platform is elevating accountability and performance tracking by incorporating web-style metrics into digital billboards.[4]FreakOut, “Partnership with Neurons,” FREAKOUT.COM Mid-tier players focus on publisher aggregation, cross-language creative, and first-party data compliance to differentiate.

Looking ahead, the winners will be firms that combine automation, measurable outcomes, and privacy-ready data models. Consolidation is likely among small outdoor owners and boutique digital shops seeking scale. Yet regulatory tightening on personal data and the need for multilingual content keep entry barriers high, underscoring why expanded capabilities rather than mere price competition will define leadership in the Southeast Asia Advertising market.

Southeast Asia Advertising Industry Leaders

-

Dentsu International Asia Pte. Ltd.

-

GroupM Asia Pacific Holdings Ltd.

-

Omnicom Media Group Asia Pacific Pte. Ltd.

-

Publicis Groupe SA

-

Havas Media Asia Pacific Pte. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Shopee expanded its advertising platform to full-funnel retail-media solutions across Southeast Asia, letting brands engage consumers from discovery to post-purchase notifications.

- July 2025: GroupM allied with local measurement tech firms to install unified cross-platform attribution across Malaysia, Singapore, and Thailand, helping multinationals re-allocate budgets with comparable metrics.

- June 2025: TikTok Shop launched AI-driven dynamic product ads in Vietnam and the Philippines, adjusting creative in real time against user cues and stock levels.

- May 2025: Grab debuted GrabAds Enterprise, a programmatic suite for large advertisers featuring granular audience clusters pulled from ride-hailing, food delivery, and payments data.

- April 2025: Dentsu International purchased a majority stake in AdAsia Holdings for USD 85 million, upgrading its automated buying stack and local language command in Thailand and Vietnam.

- March 2025: Moving Walls finished rolling out AI-powered DOOH analytics on 500+ billboards in Malaysia and Singapore, enabling performance-based pricing models.

Southeast Asia Advertising Market Report Scope

The study focuses on the current market dynamics in the Southeast Asian advertising industry. The key metrics captured in the study include advertising spending, the share of advertising spending per medium, the OOH market and DOOH market dynamics, and forecasts. The impact of COVID-19 on the DOOH industry is also analyzed in the market estimation and future projections. The disrupting factors impacting the market's growth in the near future have also been covered in the study.

The Southeast Asian advertising market is segmented by advertising spend by medium (television, newspaper, magazine, radio), DOOH segmentation by application (billboard, transit, street furniture, malls), and country. The report offers market forecasts and size in value (USD) for all the above segments.

| Traditional Media |

| Digital Media |

| Television |

| Digital Advertising |

| Radio |

| Cinema |

| Out-of-Home (OOH) |

| Digital OOH (DOOH) |

| Programmatic |

| Non-Programmatic |

| Fast-Moving Consumer Goods (FMCG) |

| Retail and E-commerce |

| Automotive |

| BFSI |

| Telecom and IT |

| Healthcare and Pharma |

| Travel and Tourism |

| Other End-User Industries |

| Singapore |

| Malaysia |

| Indonesia |

| Thailand |

| Vietnam |

| Philippines |

| Other Countries (Cambodia, Laos, Myanmar, Brunei, Timor-Leste) |

| By Channel Type | Traditional Media |

| Digital Media | |

| By Advertising Medium | Television |

| Digital Advertising | |

| Radio | |

| Cinema | |

| Out-of-Home (OOH) | |

| Digital OOH (DOOH) | |

| By Transaction Type | Programmatic |

| Non-Programmatic | |

| By End-User Industry | Fast-Moving Consumer Goods (FMCG) |

| Retail and E-commerce | |

| Automotive | |

| BFSI | |

| Telecom and IT | |

| Healthcare and Pharma | |

| Travel and Tourism | |

| Other End-User Industries | |

| By Country | Singapore |

| Malaysia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Other Countries (Cambodia, Laos, Myanmar, Brunei, Timor-Leste) |

Key Questions Answered in the Report

What is the current value of the South East Asia Advertising market?

The market is valued at USD 28.34 billion in 2025 and is on track to double by 2030.

Which channel type is growing fastest in Southeast Asian advertising?

Digital media leads with a projected 15.6% CAGR through 2030, outpacing all traditional formats.

Why is Vietnam considered the fastest-expanding ad market in the region?

Vietnam combines 16.3% CAGR, high AI adoption, and expanding broadband coverage, driving rapid ad-spend gains.

How significant is programmatic buying across Southeast Asia today?

Although non-programmatic still holds 69.7% share, programmatic channels are growing at 15.7% CAGR and gaining ground each year.

What role do super-apps play in regional advertising strategies?

Super-apps like Grab integrate payments, logistics, and commerce, offering closed-loop data that boosts targeting precision and campaign ROI.

Page last updated on: