Market Trends of South Sudan Oil and Gas Upstream Industry

This section covers the major market trends shaping the South Sudan Oil & Gas Upstream Market according to our research experts:

Increasing Political Stability is Expected to Drive the Market

The Republic of South Sudan became Africa's 55th country and the world's newest nation in July 2011. Renewed conflicts in late 2013 and July 2016 compromised the development gains achieved since independence and worsened the humanitarian situation. Consequently, South Sudan remains caught in a web of fragility, economic stagnation, and instability a decade after liberation. The signing of a truce in September 2018 and the subsequent formation of a unity government in February 2020 had provided stability and peacebuilding.

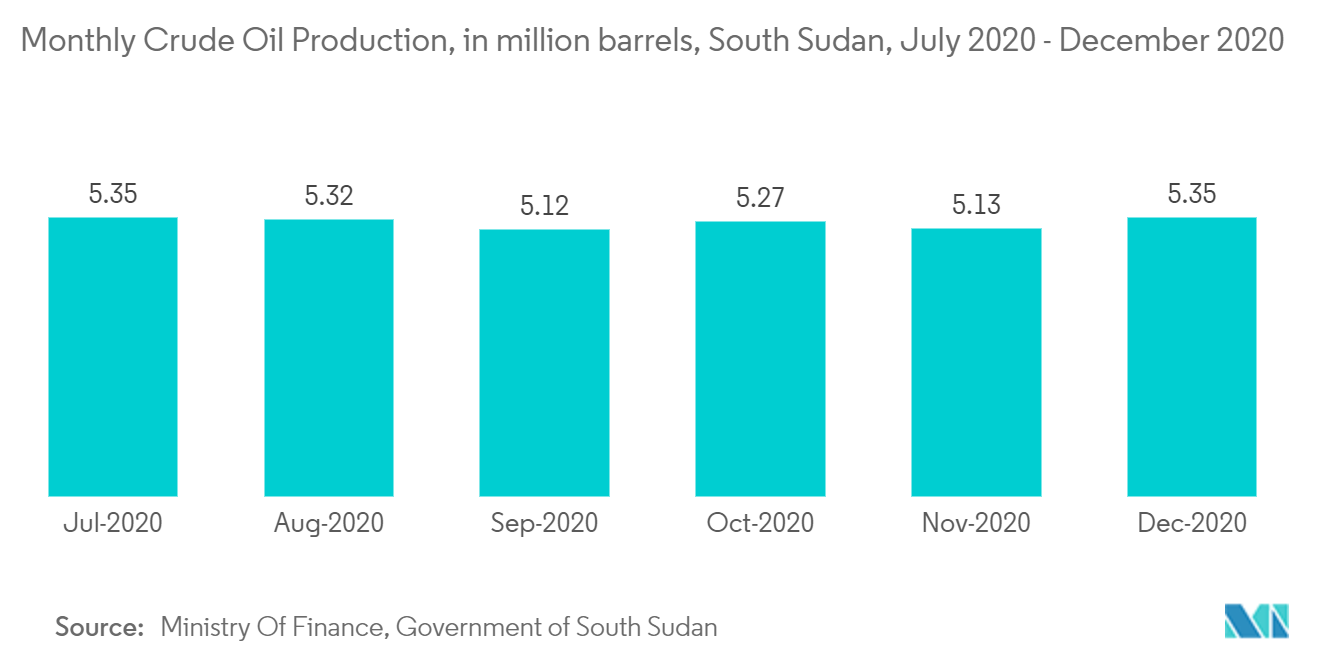

In South Sudan, the civil war and political instability have undermined its ability to increase output to peak production capacity. Low investor confidence and the unfortunate security situation posed severe obstacles to the government's ability to boost crude oil production. However, an end to the conflict significantly increased the growth of the market. In 2020, crude oil production increased four times since 2012.

Additionally, the government of the Republic of South Sudan and the government of the Republic of Sudan entered a number of agreements to cooperate across a range of areas of common interest and committed themselves to implement these agreements, including "The Agreement on Oil and Related Economic Matters (AOREM)."

Under the Cooperation Agreements, South Sudan would have access rights to the GNPOC (Nile Blend) and Petrodar (Dar Blend) processing and transportation facilities located on the territory of Sudan: South Sudan would provide their proportionate share of pipeline fill, which would be delivered to South Sudan at the expiry of the agreement till March 2022.

In February 2020, an intermediate government was formed, and elections were planned to be held within the next three years. This agreement has brought political stability to the country. Thus, the government is focusing on the development of South Sudan, especially in the oil and gas sector, to boost investment opportunities.

In June 2021, the Ministry of Petroleum (MoP) of the Republic of South Sudan launched the country's first Oil Licensing Round. The Oil Licensing Round focuses on attracting interest from a diverse group of foreign investors to a region already home to oil and gas majors from China and Malaysia. The country hopes to welcome back experienced partners and operators following significant progress in returning to peace and stability. With the new data, analysis, and governance mechanisms, the ministry seeks to attract high-quality investors and partners.

Blocks A2, A5, B1, B4, and D2 are up for investment in the First Oil Licensing Round launched in June 2021 by the Ministry of Petroleum. The blocks on offer range between 4000 and 25,000 square kilometers, although most are between 15,000 and 20,000 square kilometers.

Hence, the increased political stability is expected to attract more investments into the market, in turn driving the market during the forecast period.

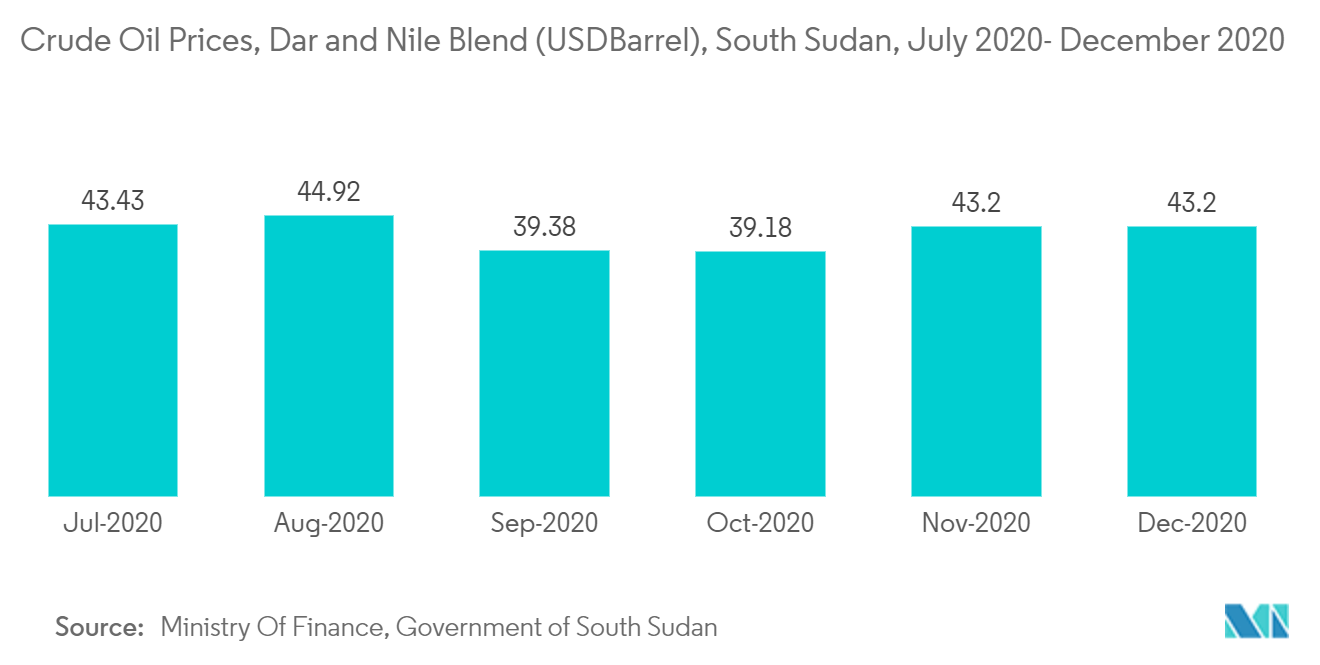

The High Volatility of Oil and Gas Prices is Expected to Hinder the Market

The government revenue in South Sudan is dominated by the oil sector, which depends on oil production. South Sudan is a small open economy that is highly vulnerable to external shocks such as oil prices and the COVID-19 pandemic. This vulnerability is exacerbated by dependency on a single commodity - crude oil - which constitutes about 33% of its gross domestic product (GDP), 90% of the government of South Sudan (GoSS) revenues, and 95% of its exports as of FY 2020.

South Sudan's dependency on oil led to a hard time in 2020, with lower oil prices taking a toll on the country's economy and the COVID-19 pandemic disrupting logistics and supplies.

The most severe economic impact on the country's economy from the pandemic was on the price of crude oil, which dropped to around USD 15.0/barrel during the fourth quarter of FY 2019/2020. According to the Ministry of Finance (GoSS), this price collapse was magnified by the fact that South Sudan pays the government of Sudan USD 24.1/barrel for oil exports through its territory.

The oil sector, which accounts for more than 90% of public revenues, was damaged by the collapse of global oil prices. Public and private consumption, the key growth drivers on the demand side, were also hurt by the pandemic. As a result, real GDP growth declined by 3.6% in 2020 after expanding by 7.4% in 2019.

The reductions in investment from the oil and gas upstream industry and incomes due to significant oil price volatility and contagion on financial markets may act as a hindrance to the market growth during the forecast period.