South Korea Used Car Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

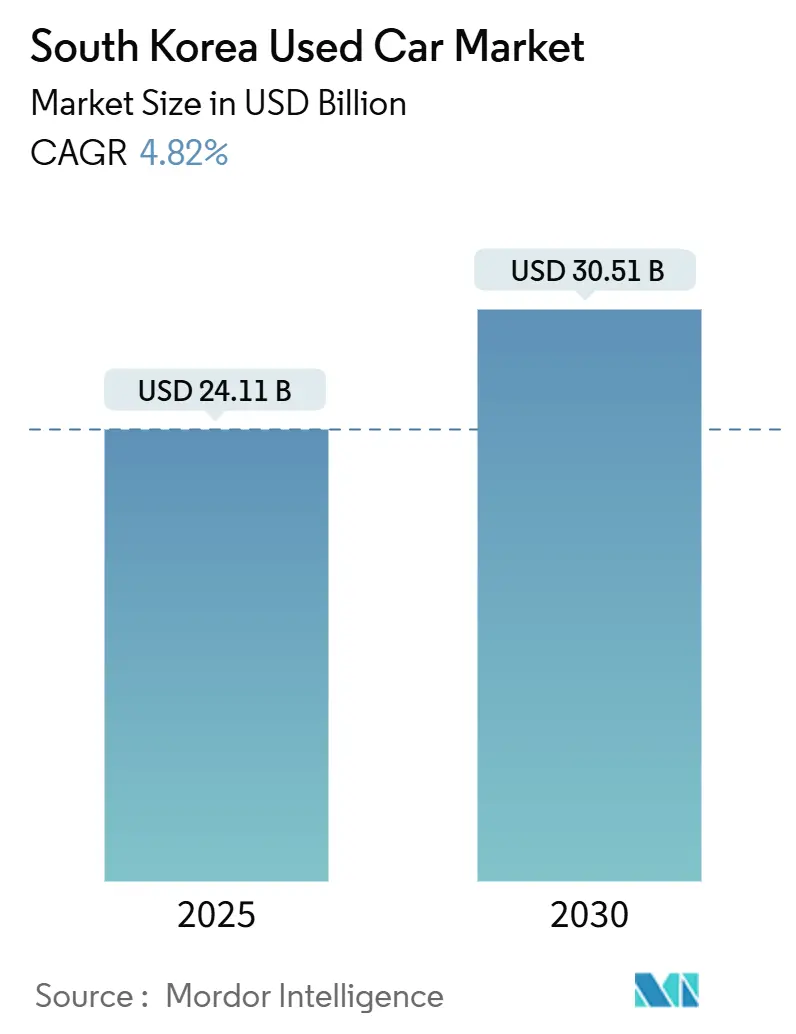

| Market Size (2025) | USD 24.11 Billion |

| Market Size (2030) | USD 30.51 Billion |

| Growth Rate (2025 - 2030) | 4.82% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Used Car Market Analysis by Mordor Intelligence

The South Korea used car market is valued at USD 24.11 billion in 2025 and is projected to reach USD 30.51 billion by 2030, advancing at a 4.82% CAGR. Growth momentum comes from a steady pipeline of three-year lease returns, widening digital access to inventory, and policy support that encourages organized retail formats. Government liquidity of KRW 2 trillion supports inventory financing and technology upgrades. Sedans still dominate but rapidly rising demand for SUVs, battery electric vehicles, and nearly-new inventory is diversifying the supply mix. Digital platforms create pricing transparency that presses unorganized dealers to modernize, while Seoul’s forthcoming emission rules accelerate turnover of older diesel vehicles.

Key Report Takeaways

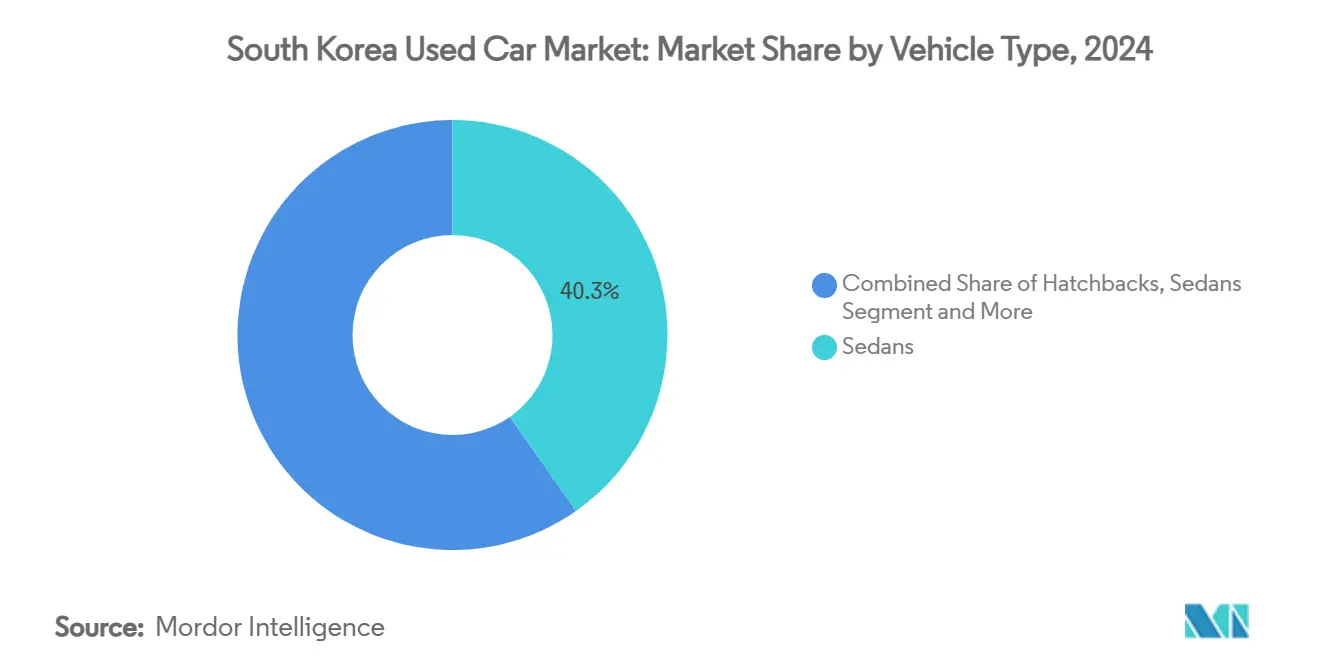

- By vehicle type, sedans led with 40.27% share of the South Korea used car market in 2024; SUVs are forecast to expand at a 6.65% CAGR to 2030.

- By vendor type, organized dealers held 58.53% of the South Korea used car market share in 2024, and the segment will grow at a 5.62% CAGR through 2030.

- By fuel type, petrol powertrains captured 61.08% of the South Korea used car market share in 2024; battery electric vehicles post the highest projected CAGR at 12.21% through 2030.

- By vehicle age, the 3-5 year bracket held a 36.14% of the South Korea used car market share in 2024; the 0-2 year bracket is rising at a 9.53% CAGR.

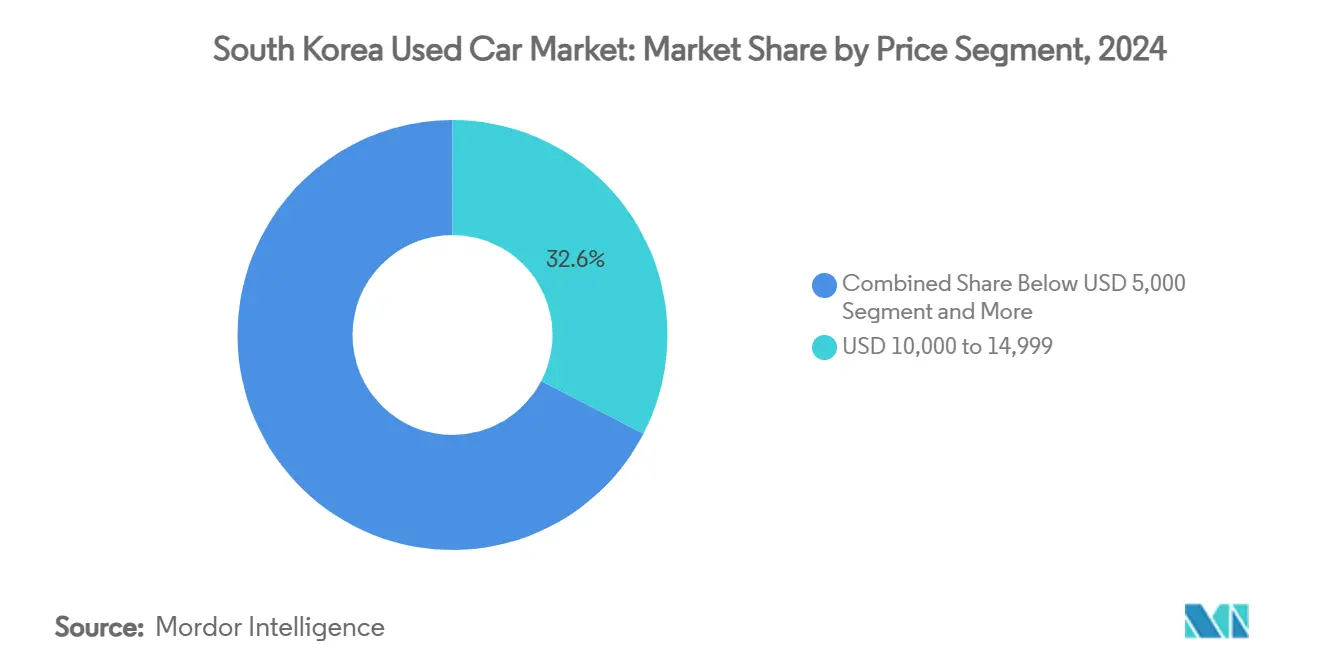

- By price segment, the USD 10,000-14,999 tier accounted for 32.61% of the South Korea used car market share in 2024; the USD 30,000+ tier shows a 10.43% CAGR outlook.

- By sales channel, multi-brand independent dealers managed 55.92% of the South Korea used car market share in 2024; pure-play e-retailers grew at an 8.42% CAGR.

- By ownership, multi-owner vehicles represented 62.44% of the South Korea used car market share in 2024; first-owner resale grows at 5.30% CAGR.

South Korea Used Car Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 3-year Lease-Return Glut | +1.8% | Seoul, Busan, Incheon, Gyeonggi | Short term (≤ 2 years) |

| Digital Marketplaces Boom | +1.2% | Seoul, Busan, Daegu, Gyeonggi | Medium term (2-4 years) |

| EV Resale Deregulation | +0.9% | Seoul, Gyeonggi, Incheon | Medium term (2-4 years) |

| OEM CPO Roll-Out | +0.7% | Seoul, Busan, Daegu, Gyeonggi, Ulsan | Long term (≥ 4 years) |

| SUV Demand Spike | +0.6% | Gyeonggi, Seoul, Busan, Daegu | Medium term (2-4 years) |

| AI Condition Grading | +0.4% | Seoul, Busan, Gyeonggi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Wave of Three-Year Lease Returns Swelling High-Quality Supply

High residual-value lease vehicles re-enter the market in bulk, giving organized dealers superior inventory that attracts buyers focused on warranty cover and lower mileage. These units retain 65.4% of original value after three years, underscoring the premium associated with nearly-new stock. Hyundai and Kia’s dominant domestic production secures a predictable stream of such returns, anchoring dealer margins. Government incentives that remain in place through 2025 further raise conversion rates from lease to purchase, particularly among eco-friendly models. The resulting inventory depth strengthens buyer confidence and supports gradual price normalization[1]“자동차 통계,” Korea Automobile Manufacturers Association, kama.or.kr.

Rising Adoption of Digital Marketplaces and Price-Comparison Apps

Online comparison tools grant shoppers instant visibility into pricing, mileage, and condition, eroding traditional information asymmetries. Dealers are shifting resources into omnichannel models that integrate virtual showrooms with in-person inspections. OEM platforms launched since 2022 offer certified listings and financing in one transaction flow, lifting service quality benchmarks across the sector. The convenience of click-to-buy capabilities is translating into a robust growth for pure-play e-retail, though in-store inspection still seals most high-value deals. Organized dealers therefore embed remote appraisal and video walkthroughs to maintain competitiveness while leveraging their physical infrastructure.

Government Deregulation Opening Resale of Up-To Four-Year-Old EVs with Tax Credits

Policy amendments allow used EV transactions to qualify for subsidies up to KRW 6.5 million, creating an immediate cost-of-ownership advantage over new internal-combustion models. This regulatory nudge is widening the buyer pool for pre-owned EVs and compressing payback periods. Dealers handling electric stock face new operational requirements, including battery health diagnostics and charger-compatibility checks. Regional subsidy limits concentrate activity around Seoul, generating price spreads that mobile wholesalers exploit by reallocating inventory to satellite cities[2]“중고차 등록 현황,” Korea Automobile Importers and Distributors Association, kaida.co.kr.

OEM-Backed Certified-Pre-Owned Roll-Out Post-2022 Law Boosts Buyer Trust

Legislation opened the used retail segment to vehicle manufacturers, allowing branded certification, extended warranties, and integrated financing. Programs such as Hyundai’s H Promise subject each unit to more than 270 inspection points, adding measurable value in the eyes of risk-averse shoppers. These offerings command premium pricing but also create reference standards that independent dealers must match on transparency and after-sales support. Over the long term, OEM participation accelerates consolidation as smaller outlets find it difficult to finance comparable warranty liabilities.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Used-car Price Inflation | -1.4% | Seoul, Busan, Gyeonggi, Incheon | Short term (≤ 2 years) |

| Unorganized Dealer Dominance | -0.8% | Daegu, Gwangju, Ulsan, Jeju | Medium term (2-4 years) |

| Seoul’s 2027 Emission-grade Diesel Ban | -0.6% | Seoul, Gyeonggi, Incheon | Medium term (2-4 years) |

| Vehicle-history Blockchain Hesitation | -0.3% | All regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Used-Car Price Inflation Narrowing Gap with New Cars

Persistent inventory shortages keep used prices elevated, reducing the historical savings that once drew consumers away from new-car showrooms. Manufacturers respond with aggressive financing on new models, tipping cost equations further. Dealers managing used inventory face compressed margins as buyers hold out for promotions or pivot toward new EVs fortified by tax relief. Urban centers feel the squeeze most acutely, where emission rules drive rapid fleet renewal and amplify demand for compliant stock.

Fragmented Unorganized Dealers Keep Trust Deficit and Price Opacity High

Small independent lots without standardized processes generate inconsistent inspection reports and variable pricing, discouraging first-time buyers who prefer transparent digital platforms. Organized dealers capture share by publicizing certified checklists and vehicle-history reports, but rural regions still rely on legacy operators with limited technology adoption. The credibility gap slows market formalization and introduces reputational risk that dampens transaction velocity in price-sensitive segments.

Segment Analysis

By Vehicle Type: SUVs Drive Market Transformation

Sedans retained the largest share at 40.27% in 2024, while SUVs are the fastest-expanding part of the South Korea used car market with a 6.65% CAGR. The shift is propelled by households seeking vehicles that blend commuter comfort with outdoor utility. Government incentives aimed at hybrid and electric SUVs further amplify demand. Dealers capitalize by prioritizing recent lease returns from Hyundai and Kia’s SUV lines, which carry strong residual values and readily available parts. Inventory managers balancing compact sedan supply with SUV demand mitigation reposition hatchbacks toward entry-level buyers who focus on price.

The growing preference for high-stance vehicles strengthens the resale prospects of models that feature advanced driver-assistance systems and low-emission powertrains. Younger families view SUVs as flexible assets that can satisfy recreation without a second vehicle, consolidating purchasing budgets into a single multipurpose unit. Dealers that align reconditioning standards with family-oriented feature sets, such as rear-seat convenience and cargo management, secure faster inventory turnover.

Note: Segment shares of all individual segments available upon report purchase

By Vendor Type: Organized Dealers Consolidate Market Share

Organized dealers captured 58.53% of the South Korea used car market share in 2024 and are projected to expand at 5.62% CAGR, owing to scale advantages in sourcing, certification, and marketing. Larger players streamline inspection, standardize pricing, and offer bundled financing, reducing friction for buyers who value speed and accountability. The South Korea used car market size for organized dealerships is forecast to climb in lock-step with digital investment that supports omnichannel experiences.

Unorganized dealers remain relevant in peripheral provinces where personal networks override formal structures, yet regulatory compliance costs and technology gaps hinder their growth. Consolidators increasingly acquire standalone lots to access local clientele and real estate footprints. The resultant network effects enable larger inventory breadth, attracting online traffic and reinforcing visibility in price-comparison apps.

By Fuel Type: Electric Vehicles Reshape Value Propositions

Petrol listings held 61.08% of the South Korea used car market share in 2024, but battery electric vehicles exhibit a 12.21% CAGR that will materially alter the South Korea used car market structure by 2030. Diesel demand contracts under city emission limits, pushing dealers to pivot toward petrol-hybrid and battery electric stock to avoid stranded assets. The South Korea used car market size for battery electric vehicles grows in tandem with charging infrastructure rollout, encouraging higher residual values and shorter selling cycles.

Dealers that master battery health assessments and warranty transfer logistics capture premiums on nearly-new EVs. Safety-related spikes in listing volumes demonstrate the sensitivity of this segment to brand reputations and incident news. Transparent battery-state disclosures mitigate fear, and certified programs that include replacement guarantees improve buyer confidence.

By Vehicle Age: Premium on Nearly-New Inventory

Vehicles aged 3-5 years account for 36.14% of the South Korea used car market share in 2024, but the 0-2 years bracket posts a 9.53% CAGR on the promise of factory warranty remainder and modern infotainment. Residual-value retention incentivizes financial leasing structures that feed high-quality supply back to the South Korea used car market. Old diesel units risk accelerated depreciation under Seoul’s 2027 ban, prompting exporters to channel these vehicles to overseas markets where regulations are softer.

The age gradient influences workshop demand, as recent models need software updates rather than mechanical overhaul. Dealers offering subscription-type maintenance packages can wrap service revenue around young inventory, stabilizing profits amid price swings.

By Price Segment: Mid-Market Dominance with Premium Growth

The USD 10,000 to 14,999 band locked in 32.61% of the South Korea used car market share in 2024, cementing its role as the sweet spot for middle-income buyers. At the top, the USD 30,000+ tier grows at 10.43% CAGR, buoyed by demand for near-new luxury SUVs and electric vehicles. The South Korea used car market share for premium tiers strengthens as access to financing widens and brand aspiration rises among younger professionals.

Price elasticity varies across regions. Metropolitan buyers often trade up, leveraging competitive leasing offers, while rural buyers gravitate toward utilitarian sedans. Dealers that segment inventory by zip-code demand patterns optimize carrying costs and turnaround time.

Note: Segment shares of all individual segments available upon report purchase

By Sales Channel: Digital Disruption Challenges Traditional Dealers

Multi-brand independents generated 55.92% of the South Korea used car market share in 2024, but pure-play e-retailers' 8.42% CAGR underscores shifting consumer journeys. Hybrid models in which customers reserve vehicles online and finalize transactions offline are becoming standard. Organized networks integrate click-to-finance and doorstep delivery to replicate e-commerce convenience without abandoning the reassurance of showrooms.

Traditional dealers respond with livestreamed walk-around sessions and AI-based price estimators to meet digital expectations. A successful omnichannel strategy blends online lead capture with in-store expertise, preserving dealer relevance while aligning with tech-savvy customer habits.

By Ownership: Multi-Owner Vehicles Dominate Supply

Multi-owner cars make up 62.44% of the South Korea used car market share in 2024, reflecting natural fleet aging and affordability considerations. First-owner resale, expanding at 5.30% CAGR, resonates with buyers prioritizing known maintenance history. Certified-pre-owned channels bolster first-owner resale value by guaranteeing condition and offering factory-backed service, thereby stretching the appeal of recent trade-ins.

For multi-owner units, dealers enhance credibility with blockchain VIN tracking and mandatory inspection uploads. This transparency lessens perceived risk and supports pricing discipline, positioning well-documented older vehicles as budget-friendly yet reliable options.

Geography Analysis

Seoul, Incheon, and Gyeonggi collectively drive a significant turnover, testament to their high incomes, dense populations, and early digital adoption. They also serve as policy laboratories: emission-grade restrictions force owners to shift from diesel to compliant petrol, hybrid, or electric models. Dealers in the capital region use sophisticated online marketing and same-day delivery to match the expectations of tech-literate consumers.

Second-tier hubs, Busan, Daegu, Gwangju, and Ulsan, cater to differing demand: port-linked Busan supports commercial vans, while the industrial belt around Ulsan values fleet reliability and service contracts. These areas tilt toward practical sedans and MPVs, requiring dealers to maintain diversified stock. Government regional development funds help local operators modernize inspection facilities, narrowing the quality gap with capital-area competitors.

Rural provinces still rely on community-based dealers who emphasize relationship selling. Limited charging infrastructure constrains EV adoption, dampening secondary EV prices compared with urban centers. However, the nation’s plan to install 500,000 public chargers by 2025 is expected to unlock pent-up rural demand, creating upside for dealers prepared to deploy mobile service vans and remote inspection tools.

Competitive Landscape

The competitive landscape indicates a moderately concentrated setting that rewards scale without stifling innovation. Leading firms integrate AI-guided condition grading and blockchain verification to elevate consumer trust. Partnerships with OEM leasing arms secure pipelines of recent off-lease vehicles, locking in stock quality and spread control.

Emerging digital-only entrants position themselves on transparency and speed, offering seven-day delivery and no-hassle return policies. This nudges incumbents to accelerate app development, introduce video appraisal, and broaden pick-up logistics. OEM-affiliated dealers exploit brand loyalty to extend certified-pre-owned coverage nationwide. Traditional multi-brand lots that invest in omnichannel touch-points hold their ground, but those ignoring tech upgrades face declining footfall.

Strategic moves recently underscore the push toward customer-centric models: One platform introduced seven-day delivery for its verified stock, while a multi-brand luxury retailer announced a dedicated portal targeting imported used cars. Hyundai inaugurated its own certified division with 272-point checks, reinforcing the manufacturer's commitment to the secondary market.

South Korea Used Car Industry Leaders

-

KB Cha Cha Cha

-

K Car

-

Encar

-

HeyDealer

-

Hyundai Glovis (H Promise)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The largest used-car portal Encar added seven-day delivery to its online purchase service “Encar MEET Go,” enabling consumers to buy dealer-inventory vehicles diagnosed and certified by Encar.

- March 2025: Kolon Mobility Group announced a forthcoming online platform focused on imported used cars, extending its brand portfolio beyond BMW and Rolls-Royce.

South Korea Used Car Market Report Scope

A used car/pre-owned vehicle, or a secondhand car, is a vehicle that previously had one or more retail owners. A certified pre-owned (CPO) vehicle, on the other hand, is a pre-owned vehicle that has been extensively inspected (pre-purchase inspection) and expertly reconditioned. The used car market consists of a wide range of companies involved in the purchasing and selling of pre-owned vehicles through online or offline sales channels.

The South Korea used car market is segmented by vehicle type, vendor type, fuel type, and sales channel. By vehicle type, the market is segmented into hatchbacks, sedans, and sports utility vehicles (SUVs)/multi-purpose vehicles (MPVs). By vendor type, the market is segmented into organized and unorganized. By fuel type, the market is segmented into petrol, diesel, electric, and other fuel types (liquefied petroleum gas, compressed natural gas, etc.). By sales channel, the market is segmented into online and offline.

The report offers market size and forecast value (USD) for all the above segments.

| Hatchbacks |

| Sedans |

| Sport-Utility Vehicles (SUVs) |

| Multi-Purpose Vehicles (MPVs) |

| Others (convertibles, coupes, crossovers, sports cars) |

| Organised |

| Unorganised |

| Petrol |

| Diesel |

| Hybrid (HEV and PHEV) |

| Battery-Electric (BEV) |

| LPG / CNG / Others |

| 0 to 2 Years |

| 3 to 5 Years |

| 6 to 8 Years |

| 9 to 12 Years |

| Above 12 Years |

| Below USD 5,000 |

| USD 5,000 to USD 9,999 |

| USD 10,000 to USD 14,999 |

| USD 15,000 to USD 19,999 |

| USD 20,000 to USD 29,999 |

| USD 30 000 and Above |

| Online Digital Classified Portals |

| Pure-play e-Retailers |

| OEM-Certified Online Stores |

| Offline OEM-Franchised Dealers |

| Multi-brand Independent Dealers |

| Physical Auction Houses |

| Online |

| Offline |

| First-owner Resale |

| Multi-owner |

| By Vehicle Type | Hatchbacks |

| Sedans | |

| Sport-Utility Vehicles (SUVs) | |

| Multi-Purpose Vehicles (MPVs) | |

| Others (convertibles, coupes, crossovers, sports cars) | |

| By Vendor Type | Organised |

| Unorganised | |

| By Fuel Type | Petrol |

| Diesel | |

| Hybrid (HEV and PHEV) | |

| Battery-Electric (BEV) | |

| LPG / CNG / Others | |

| By Vehicle Age | 0 to 2 Years |

| 3 to 5 Years | |

| 6 to 8 Years | |

| 9 to 12 Years | |

| Above 12 Years | |

| By Price Segment | Below USD 5,000 |

| USD 5,000 to USD 9,999 | |

| USD 10,000 to USD 14,999 | |

| USD 15,000 to USD 19,999 | |

| USD 20,000 to USD 29,999 | |

| USD 30 000 and Above | |

| By Sales Channel | Online Digital Classified Portals |

| Pure-play e-Retailers | |

| OEM-Certified Online Stores | |

| Offline OEM-Franchised Dealers | |

| Multi-brand Independent Dealers | |

| Physical Auction Houses | |

| By Source | Online |

| Offline | |

| By Ownership | First-owner Resale |

| Multi-owner |

Key Questions Answered in the Report

What is the current value of the South Korea used car market?

The market stands at USD 24.11 billion in 2025 and is forecast to reach USD 30.51 billion by 2030.

Which segment holds the largest South Korea used car market share?

Sedans lead with 40.27% share, while SUVs are the fastest-growing at a 6.65% CAGR.

How fast is the battery electric vehicle segment growing?

Battery electric vehicles post a 12.21% CAGR, the highest among all fuel types through 2030.

Why are organized dealers expanding faster than unorganized dealers?

Organized dealers provide certified inspections, transparent pricing, and integrated financing, helping them grow at 5.62% CAGR versus slower growth for fragmented independents.

How will Seoul’s 2027 diesel restrictions impact the market?

The policy accelerates turnover of older diesel stock, raising demand for petrol, hybrid, and electric models while pressuring resale values of older diesels.

Page last updated on: