Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

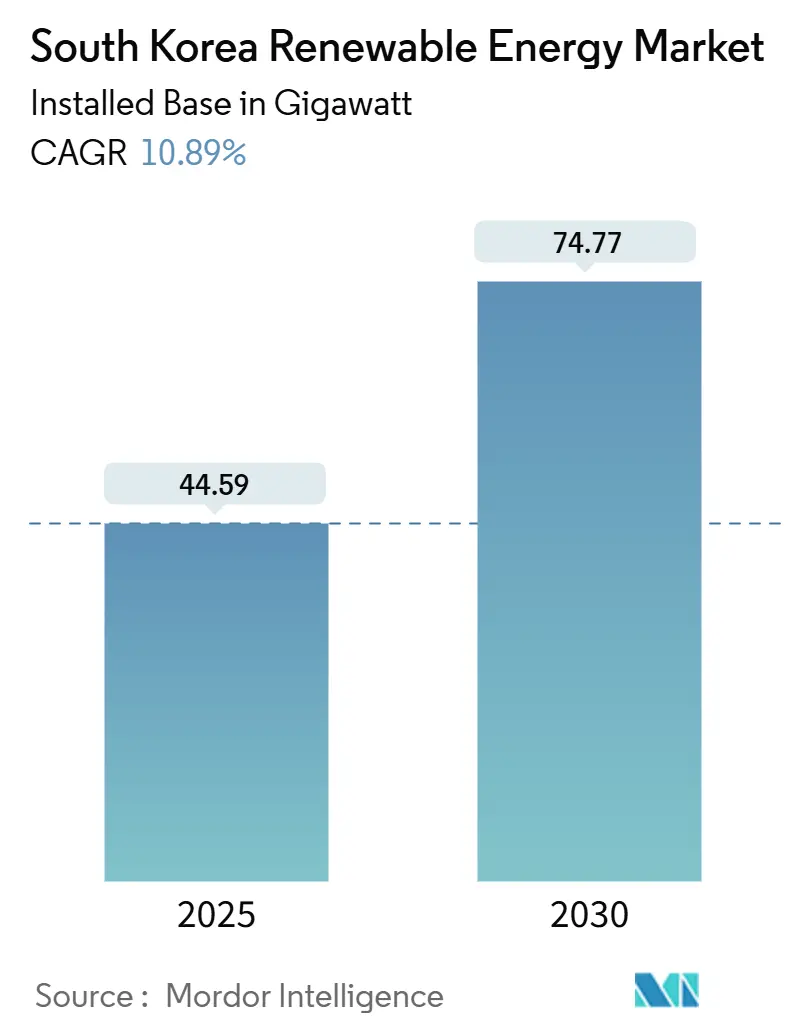

| Market Volume (2025) | 44.59 gigawatt |

| Market Volume (2030) | 74.77 gigawatt |

| Growth Rate (2025 - 2030) | 10.89% CAGR |

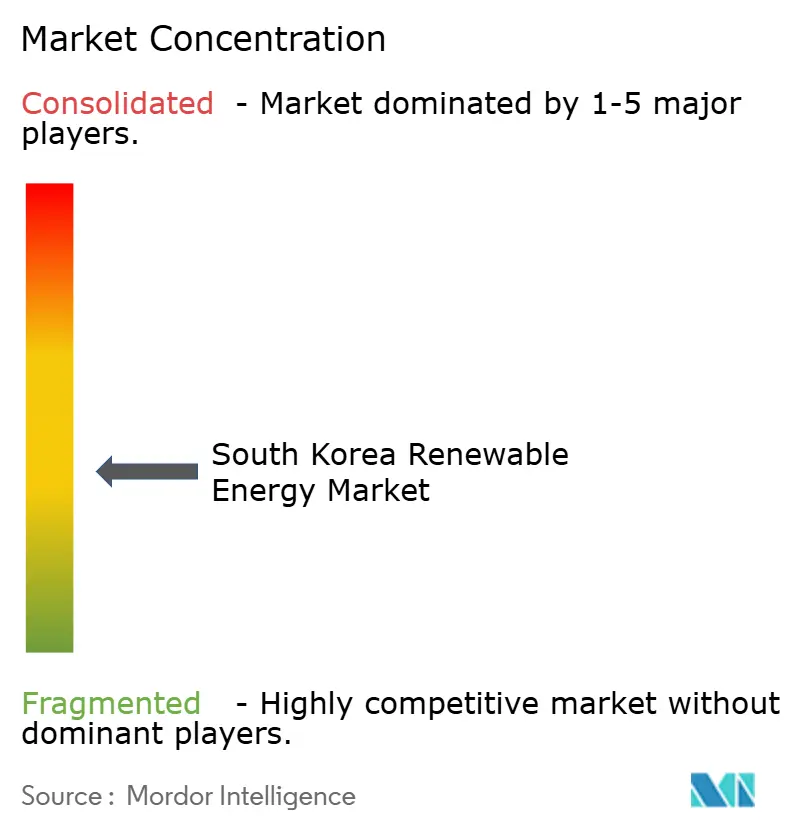

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Renewable Energy Market Analysis by Mordor Intelligence

The South Korea Renewable Energy Market size in terms of installed base is expected to grow from 44.59 gigawatt in 2025 to 74.77 gigawatt by 2030, at a CAGR of 10.89% during the forecast period (2025-2030).

Strong policy alignment with the 11th Basic Plan, a streamlined offshore wind permitting law, and rising corporate power purchase agreements jointly underpin capacity additions. Grid digital-twin deployment, mandatory REC quotas, and 1.2 trn won port upgrades for large-turbine handling accelerate the South Korean renewable energy market by lowering integration and logistics barriers. Jeju Island’s utility-scale storage pilots, KEPCO’s 29.3 trn won transmission plan, and nuclear-powered hydrogen projects further expand the technology mix as utilities pivot from thermal fleets to diversified renewables. Land-acquisition disputes and 30-month EIA cycles remain the primary bottlenecks; however, ongoing legal challenges and procedural reforms aim to ease these frictions and sustain the momentum of the South Korean renewable energy market.

Key Report Takeaways

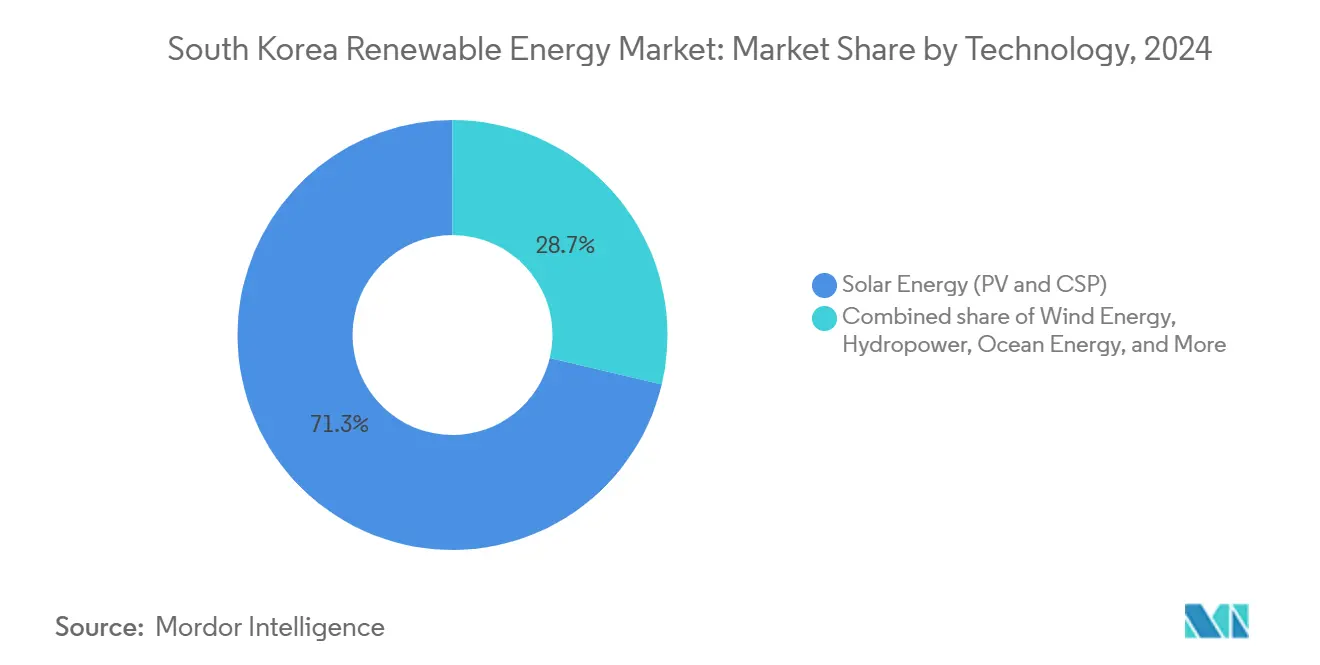

- By technology, solar energy commanded 71.3% of the South Korean renewable energy market share in 2024, while wind energy is projected to grow at a 36.6% CAGR between 2025 and 2030.

- By end-user, utilities held 59.9% of the South Korean renewable energy market share in 2024 and are expected to expand at a 12.9% CAGR through 2030.

South Korea Renewable Energy Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Rapid Decline in Utility-Scale Solar LCOE Across South Korea | +2.1% | National, concentrated in Jeolla and Gyeonggi provinces | Medium term (2-4 years) | |

| Mandatory REC Quotas Pushing Corporates Toward PPAs | +1.8% | National, with Seoul metropolitan area leading adoption | Short term (≤ 2 years) | |

| Offshore Wind Port Infrastructure Subsidies Near Mokpo & Ulsan | +2.9% | Southwest and Southeast coastal regions | Long term (≥ 4 years) | |

| Hydrogen-to-Power Pilots Backed by KEPCO & SK E&S | +1.2% | Ulsan and Pohang industrial clusters | Long term (≥ 4 years) | |

| Jeju "Carbon-Free Island" 2030 Target Accelerating Storage-Coupled RE | +1.5% | Jeju Province, with mainland spillover effects | Medium term (2-4 years) | |

| Grid Modernization Investments (KEPCO Digital Twin Roll-out) | +2.3% | National grid infrastructure, priority on transmission corridors | Medium term (2-4 years) | |

| Source: Mordor Intelligence | ||||

Rapid Decline in Utility-Scale Solar LCOE Across South Korea

Utility-scale module prices fell 27% between early 2024 and 2025 as Hanwha Q CELLS and OCI ramped 50-100 MW projects, widened domestic wafer pulls, and benefited from tariff exemptions on imported trackers. Developers installed 1.2 GW of new solar capacity in 1H 2024, reinforcing South Korea's 71.3% solar lead in the renewable energy market. LCOE parity versus LNG is expected by 2026, shifting corporate buyers toward multi-megawatt PPAs. Despite a KRW 300.2 bn loss from oversupply, Hanwha's expanded Q ANTUM line underpins price competitiveness and secures future volume.[1]Business Korea, "Hanwha Solutions Reports 300.2 Billion Won Operating Loss," businesskorea.co.kr

Mandatory REC Quotas Pushing Corporates Toward PPAs

The Renewable Portfolio Standard requires large producers to generate 25% of their energy from renewable sources by 2026, following the implementation of direct PPAs after the Electric Utility Act amendments.[2]Mayer Brown energy alert, “South Korea opens door for direct PPAs,” MAYERBROWN.COM Hyundai’s 610 GWh, twenty-year deal exemplifies first-mover industrial demand and signals mounting pressure on peers to adopt renewable sourcing. While PPA electricity lacks REC eligibility, utilities now design hybrid structures that link certificates with hedged supply, broadening liquidity and stabilizing the South Korean renewable energy market.

Offshore Wind Port Infrastructure Subsidies Near Mokpo & Ulsan

A KWR 1.2 trillion harbor overhaul delivered heavy-lift cranes, deep-water quays, and marshalling yards capable of handling 15-MW nacelles, resulting in a 20% reduction in logistics costs. The government awarded 1.9 GW across December 2024 auctions and holds a 58.8 GW pipeline, driving the wind segment’s 36.6% CAGR and altering the South Korea renewable energy market technology mix.

Grid Modernisation Investments (KEPCO Digital Twin Roll-out)

KEPCO's KWR 29.3 trillion expansion adds 10,173 circuit kilometers and embeds a cloud-based digital twin that simulates congestion and dispatch in real-time. The 4 GW Donghaean #2 HVDC line will transport southeast renewables to Seoul, which accounts for 40% of the nation's demand. These upgrades ensure the South Korean renewable energy market can scale without curtailment spikes.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Land Acquisition Challenges for Ground-Mounted Solar in Gyeonggi & Chungcheong | -1.6% | Gyeonggi and Chungcheong provinces, urban periphery areas | Short term (≤ 2 years) | |

| Curtailment Risk Owing to 154 kV Congestion on Southwest Corridor | -1.2% | Southwest transmission corridor, Jeolla to Seoul route | Medium term (2-4 years) | |

| Local-content Rules Inflating Offshore-Wind CapEx | -0.7% | Offshore wind development zones, coastal manufacturing regions | Medium term (2-4 years) | |

| Slow Environmental Impact Assessment (EIA) Approval Cycle (>30 months) | -1.9% | National, with particular delays in environmentally sensitive areas | Long term (≥ 4 years) | |

| Source: Mordor Intelligence | ||||

Land Acquisition Challenges for Ground-Mounted Solar in Gyeonggi & Chungcheong

Setback ordinances of 100-1,000 m eliminate up to 70% of candidate plots and inflate build costs by 25%.[3]Solutions for Our Climate press office, “Citizens challenge solar-setback rules,” SOF.OR.KR Constitutional appeals filed in February 2025 target these rules as scientifically unfounded. Without repeal, capital will shift to rooftop or offshore wind, eroding solar’s current preeminence within the South Korean renewable energy market.

Slow Environmental Impact Assessment Approval Cycle (Above 30 months)

Haewoori offshore wind completed its EIA in July 2024, following a multi-year review, which illustrates a 30-month average that extends the financing risk.[4]Energy Global news desk, “Haewoori offshore wind EIA completed,” ENERGYGLOBAL.COM The March 2025 Wind Power Promotion Act pledges single-window clearance, but the entrenched agency is still delaying project realisation.

Segment Analysis

By Technology: Wind Acceleration Challenges Solar Dominance

Solar energy maintained a 71.3% share of the South Korean renewable energy market in 2024, yet wind’s 36.6% CAGR signals a shift. The South Korean renewable energy market size for offshore wind could exceed 25 GW by 2030 if the entire auction pipeline reaches financing. Removal of local-content quotas cut turbine CapEx by up to 20%, attracting Ørsted and Equinor, while CS Wind localised tower production. Hydropower, bioenergy, and geothermal energy remain niche options, given resource limits and the refocusing of subsidies.

A 15-MW turbine roll-out, floating-foundation pilots off Ulsan, and deeper water leasing rounds reinforce wind’s catching-up trajectory. The South Korea renewable energy market share for solar may narrow as port capacity, HVDC links, and corporate decarbonisation tilt spending toward higher-capacity-factor wind farms.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: Utilities Drive Market Transformation

Utilities controlled 59.9% of installed capacity in 2024 and posted a 12.9% CAGR through 2030 as KEPCO subsidiaries spearhead multi-GW tenders. K-RE100 uptake and Hyundai’s record PPA indicate that commercial-industrial buyers are scaling rapidly, yet non-REC eligibility tempers wider adoption. Residential growth lags, capsized by setback ordinances and limited rooftop area, though virtual-power-plant pilots harness new 540 MW/3,240 MWh storage contracts. As reform widens PPA eligibility, the South Korean renewable energy industry can progressively rebalance reliance away from incumbent utilities.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Due to strong coastal winds and deep-water ports, Jeolla provinces dominate the South Korean renewable energy market. The 8.2 GW Sinan complex anchors this lead, bolstered by the KWR 1.2 trillion infrastructure package that equips Mokpo to service turbines exceeding 15 MW. Grid plans allocate 2 GW of dedicated HVDC export capacity from Sinan to the Seoul load center once the Donghaean #2 link comes online in 2027. Robust local content incentives also foster nacelle and blade facilities that feed domestic and export orders.

Jeju Island pioneers integrated renewables, with its 16.2% renewable penetration in 2020 and the goal of achieving carbon neutrality by 2030, creating an experimental sandbox. ABB’s synchronous condenser and Hitachi’s VSC converter keep the island grid balanced despite rising variable output. Battery storage cut curtailment by 1,847 MWh between 2015 and 2019, and a green-hydrogen pilot positions Jeju as a template for mainland replication. Lessons from frequency management and rotating-inertia substitution inform national standards slated for 2026.[5]Hitachi Energy case notes, “First VSC converter on Jeju,” HITACHIENERGY.COM

Industrial East Coast hubs Ulsan and Pohang are evolving into hydrogen valleys. KHNP broke ground on the country’s first nuclear-powered electrolyser in October 2025, while SK E&S advanced a USD 16 billion complex targeting 250,000 t H₂ annually. These clusters leverage proximity to steel mills and petrochemical plants, generating anchor demand for clean molecules and stabilizing renewable energy flows. Conversely, land-tight Gyeonggi and Chungcheong provinces struggle with ground-mounted solar permitting, prompting developers to opt for pricier rooftops or rural areas with longer grid feeds.

Competitive Landscape

Market concentration is moderate. KEPCO’s generation subsidiaries maintain extensive pipelines but face new competition from Ørsted, Equinor, and Vena Energy in the offshore wind sector. Joint ventures such as ESVAGT-KMC Line’s service-operation-vessel tie-up fill marine capability gaps, while CS Wind-Vestas localization agreements secure power supply. Technology leadership is shifting toward 15-MW-plus turbines, with Siemens Gamesa and GE Vernova positioning themselves for the next tender round.[6]CS Wind announcement, “CS Wind-Vestas joint venture,” CSWIND.COM

Domestic conglomerates pursue vertical integration. Hanwha Q CELLS controls upstream polysilicon, modules, and EPC services, giving the firm leverage in price negotiations yet exposing it to global oversupply swings. SK E&S combines LNG trading, renewables, and hydrogen, hedging commodity volatility. KHNP’s HK$1.166 billion green nuclear bond diversifies funding and underscores nuclear-renewable synergies. Meanwhile, smaller IPPs exploit direct-PPA rules to carve out retail niches.

Cost competitiveness supplants legacy relationships as the primary criterion for tender. Developers can bundle storage or hydrogen gain evaluation points under the 2025 auction guidelines. Fleet-wide digitalization adopted by KEPCO sets performance benchmarks, prompting OEMs to embed predictive analytics into their operations and maintenance (O&M) contracts. International entrants deliver expertise in floating foundations and multi-terminal HVDC, accelerating the transfer of skills into local supply chains.

South Korea Renewable Energy Industry Leaders

-

Korea Electric Power Corporation (KEPCO)

-

Hanwha Q CELLS Co., Ltd

-

Korea Midland Power Co., Ltd (KOMIPO)

-

Korea South-East Power Co., Ltd (KOSEP)

-

SK E&S Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: Doosan Enerbility and Korea Western Power signed an MoU to develop and export 90 MW hydrogen turbines.

- May 2025: The government tendered 540 MW/3,240 MWh of grid-scale batteries to mitigate renewable curtailment risk.

- April 2025: KHNP broke ground on the nation’s first nuclear-powered hydrogen plant, targeting a production rate of 4 tons per day.

- March 2025: KHNP floated Asia’s first green nuclear bond, raising Hong Kong dollars 1.166 billion for next-generation technologies.

South Korea Renewable Energy Market Report Scope

Renewable energy refers to energy sources that are replenished naturally and are therefore considered sustainable and environmentally friendly. Examples of renewable energy sources include solar, wind, hydropower, geothermal, and biomass. These sources of energy are considered renewable because they are replenished naturally and continuously, unlike non-renewable sources of energy such as fossil fuels (coal, oil, and gas), which are finite resources that will eventually be depleted.

South Korean renewable energy is segmented by type. By type, the market is segmented into hydro, wind, solar, and other types. For each segment, market sizing and forecasts have been done based on megawatts (MW).

By Technology

| Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) |

| Hydropower (Small, Large, PSH) |

| Bioenergy |

| Geothermal |

| Ocean Energy (Tidal and Wave) |

By End-user

| Utilities |

| Commercial and Industrial |

| Residential |

| By Technology | Solar Energy (PV and CSP) |

| Wind Energy (Onshore and Offshore) | |

| Hydropower (Small, Large, PSH) | |

| Bioenergy | |

| Geothermal | |

| Ocean Energy (Tidal and Wave) | |

| By End-user | Utilities |

| Commercial and Industrial | |

| Residential |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the South Korea renewable energy market today?

It stood at 44.59 GW in 2025 and is forecast to reach 74.77 GW by 2030.

Which technology is growing fastest?

Wind energy post the highest 36.6% CAGR for 2025-2030.

Why are corporate PPAs important in South Korea?

Direct PPAs let firms such as Hyundai secure long-term renewable supply outside KEPCO’s monopoly, supporting REC compliance and fixed pricing.

What grid upgrades are planned to support renewables?

KEPCO will add 10,173 circuit-km and a 4 GW HVDC link to Seoul, plus a nationwide digital-twin platform by 2034.

What is the main hurdle for new solar farms?

Municipal setback ordinances remove much developable land, prompting legal challenges and cost increases.

How is hydrogen linked to renewable growth?

Nuclear-powered electrolysers and SK’s USD 16 bn complex will supply clean hydrogen for 6,500 GWh of power bids, providing flexible back-up to variable renewables.

Page last updated on: