Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 2.5 Billion |

| Market Size (2031) | USD 3.05 Billion |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Office Furniture Market Analysis by Mordor Intelligence

The South Korea office furniture market size is estimated at USD 2.50 billion in 2026 and is projected to reach USD 3.05 billion by 2031, reflecting a 4.03% CAGR. Tight Grade A office availability in Seoul’s core districts keeps vacancy low and rents firm, pushing occupiers to maximize space efficiency and to favour modular systems and ergonomic seating that compress footprints without sacrificing comfort. Hybrid work is accelerating the shift to activity-based layouts, with flagship corporate fitouts integrating focus rooms, collaboration areas, and social zones that call for diverse furniture typologies. Public-sector demand benefits from the mandatory Green Public Procurement framework that prioritizes KEITI Ecolabel-certified products across central and local agencies, which keeps sustainability features central to purchasing decisions. Electrified desks and related products also face new compliance and substance restrictions under Korea’s expanded EPR and RoHS regime, which is prompting accelerated product upgrades that influence specifications and sourcing plans across the South Korea office furniture market.

Key Report Takeaways

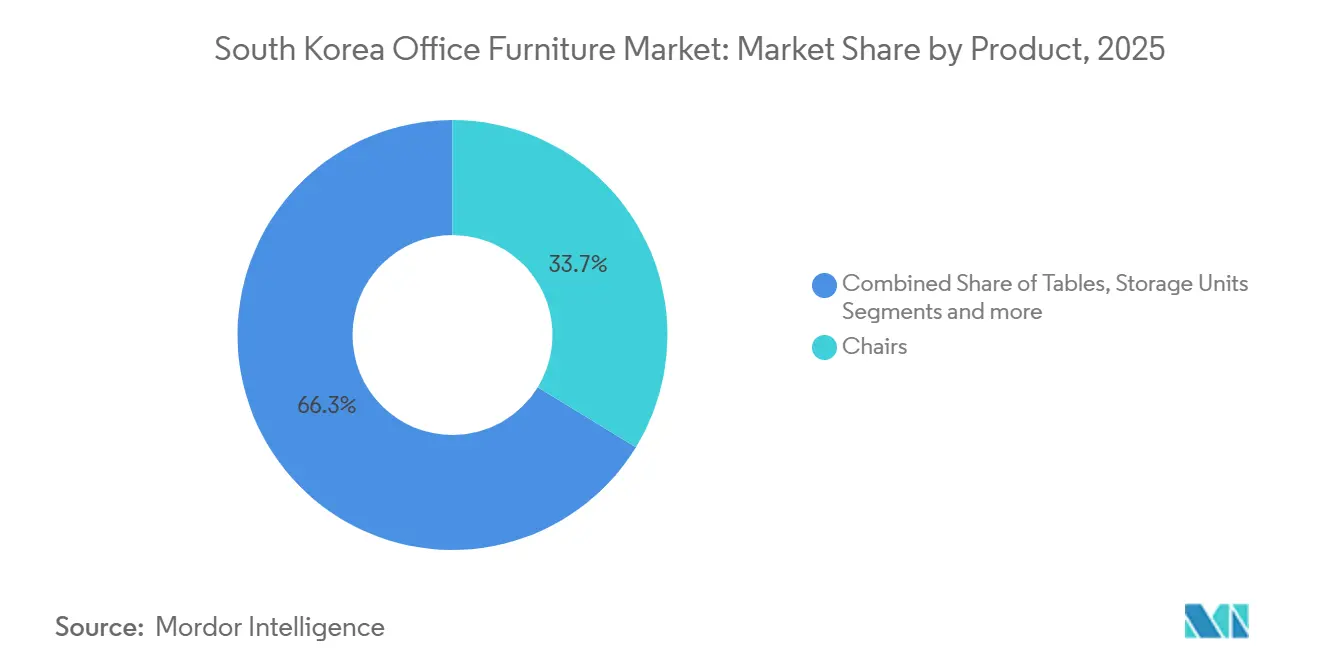

- By product, chairs are the largest category at 33.74% market share in 2025, while sofas and soft seating lead growth at a 5.47% CAGR during 2026–2031

- By material, wood leads with a 42.62% market share in 2025, supported by sustainability adoption, and plastics and polymers are the fastest-growing at a 4.82% CAGR in 2026–2031.

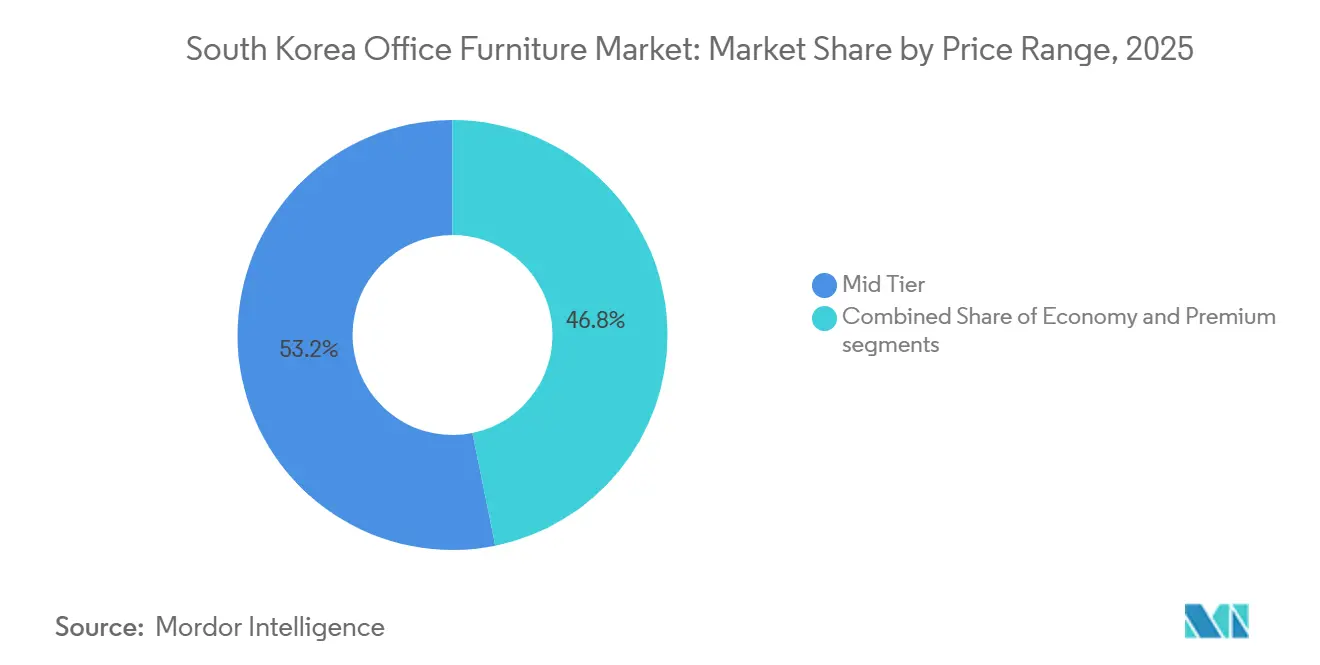

- By price range, mid-tier accounts for the highest volume with 53.19% market share in 2025, while premium lines grow the fastest at a 4.69% CAGR through 2031.

- By end-user, corporate offices are the largest buyer group at 38.10% market share in 2025, and hospitality and retail back-office expand the quickest at a 5.71% CAGR during 2026–2031.

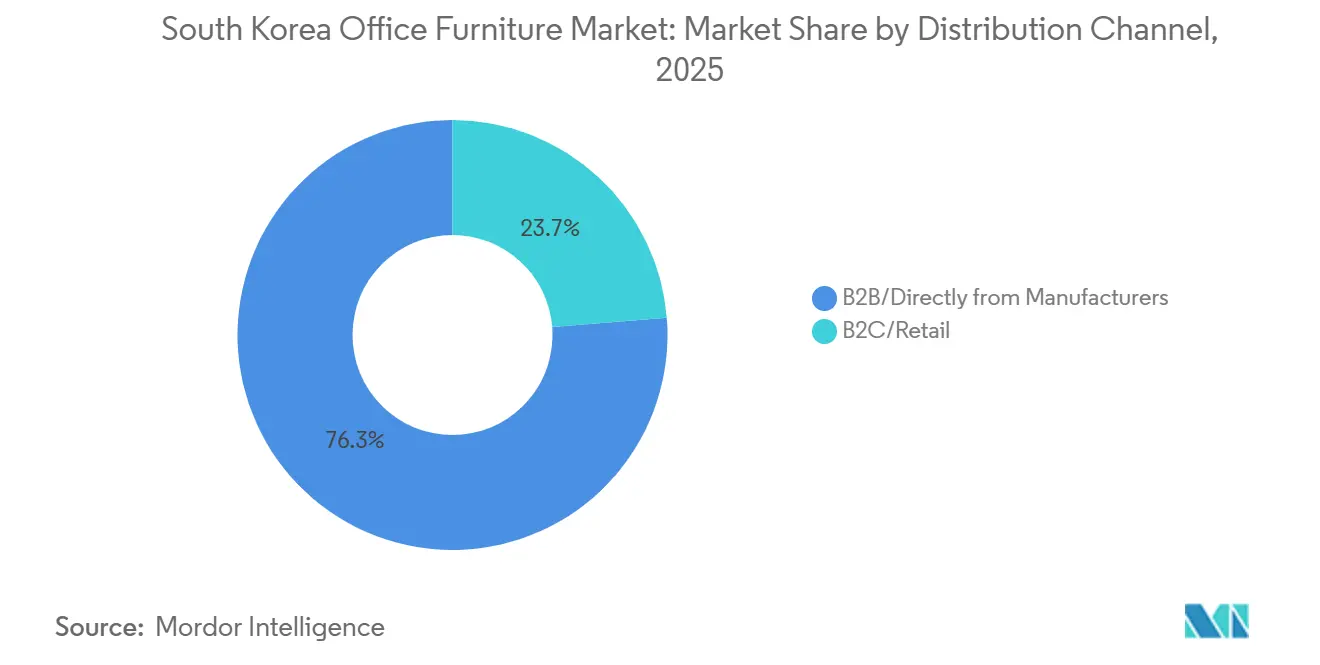

- By Distribution channel, B2B/direct from manufacturers dominates with 76.27% of the market size in 2025, while online within B2C/retail posts the fastest growth at a 6.13% CAGR through 2031.

- Geography: Gyeonggi, including the Seoul Capital Area, is both the largest region at 41.31% share in 2025 and the fastest-growing at a 5.06% CAGR over 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Office Furniture Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | |

|---|---|---|---|

| Tight Grade A Office Availability & Rising Rents In Seoul | +1.8% | Seoul Capital Area, with spill-over to Yeongnam metropolitan centres | |

| Hybrid Work Driving Modular & Collaborative Office Layouts | +1.5% | National, with early adoption in Seoul, Busan, and corporate innovation districts | |

| Growing Focus On Ergonomics & Employee Well-Being | +1.2% | National, led by multinational subsidiaries and public institutions | |

| Rapid Rise In Online Furniture Purchases For Home Offices | +0.9% | National, strongest in the Seoul Capital Area and Gyeonggi Province | |

| Mandatory Keiti Eco-Label Boosting Public-Sector Demand | +1.0% | National, driven by 1,176 national agencies and 30,000 sub-public authorities | |

| Expanded Eee Rohs/Epr Rules Spurring Electrified Desk Upgrades | +0.7% | National, prioritized by regulated public agencies and ESG-conscious corporates | |

| Source: Mordor Intelligence | |||

Tight Grade A Office Availability & Rising Rents In Seoul

Seoul’s Grade A vacancy in the central business district remained tight, which held at historically low levels and maintained quarterly rent growth that keeps occupancy costs elevated for tenants.[1]Source: Jie Sorim, “Seoul’s Office Market Remained Sought After with Low Vacancy Rates,” Cushman & Wakefield, cushmanwakefield.com Limited new supply and a flight-to-quality trend nudge occupiers to refurbish existing space, which stimulates replacement demand in the South Korea office furniture market. Rents posted strong gains since 2020 and were projected to remain firm through 2024, which reinforced densification strategies and a preference for modular systems that maximize utilization per square meter. Cap rate polarization around premium corridors such as Teheran-ro underscores investment in furniture specifications that bolster employee experience in high-rent buildings. Co-working operators also reported resilient performance, which supports sustained demand for adaptable furniture able to cycle across short lease terms and changing team sizes in the South Korea office furniture market.

Hybrid Work Driving Modular & Collaborative Office Layouts

Activity-based working programs in Seoul showcase a deliberate shift from individual workstations to zones for focus, collaboration, and social connection, and they require an expanded mix of seating, tables, dividers, and soft furniture.[2]Source: Frame Editors, “L’Oréal Korea’s Redesigned Office Space Boldly Embraces Hybrid Work,” Frame, frameweb.com With capital constraints, occupiers seek fully fitted and flexible offices, which increases interest in modular systems and leasing models that reduce upfront costs and enable iterative reconfiguration. Flight-to-quality and ESG alignment drive furniture specifications that meet energy, material, and certification expectations, which support bundles that offer verified sustainability within the South Korea office furniture market. New-build relocations and upgrades contribute to re-standardization on cohesive design languages that support hybrid collaboration protocols and incorporate local design cues. Companies are also investing in technology-integrated workstations that incorporate power and data to support hybrid teams, which is shaping the premium end of the South Korean office furniture market.

Growing Focus on Ergonomics & Employee Well-Being

Ergonomic seating has become the most influential category, with leading models featuring multi-point adjustability, third-party certifications, and validated durability that align with corporate procurement criteria. Domestic brands are expanding domestic and overseas distribution and refreshing lineups with compact and small-size offerings, which extend ergonomic standards to diverse user profiles. Component specialists and chair manufacturers continue to prioritize R&D and export channels, which reinforces Korea’s status as a regional hub for ergonomic seating within the South Korean office furniture market. Height-adjustable desks are scaling across price points and formats, ranging from non-electric to electrified versions that enable sit-stand protocols in open-plan settings. Manufacturers are also improving supply resilience and production efficiency to fund ongoing ergonomic innovation while managing volatility in input costs.

Mandatory Keiti Eco-Label Boosting Public-Sector Demand

Korea’s Green Public Procurement program obligates central and subnational agencies to purchase KEITI Ecolabel or Good Recycled Mark-certified items, which structurally elevates compliant demand for office furniture.[3]Source: Korea Environmental Industry & Technology Institute, “Eco Label & Green Consumption,” KEITI, keiti.re.kr Green purchases have expanded severalfold since program inception, and office-related categories are a large share of certified products, which supports a durable baseline for Ecolabel-compliant SKUs in the South Korea office furniture market. Mutual recognition agreements and a multi-year plan to broaden coverage continue to streamline certification and encourage manufacturers to harmonize eco-design across portfolios. Program monitoring links environmental and economic benefits, with quantified emissions reductions and green job creation, reinforcing public spending on sustainable categories. Market leaders that have aligned sourcing, formaldehyde standards, and eco-friendly sales targets are positioned to win larger public tenders within the South Korean office furniture market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | |

|---|---|---|---|

| Volatility In Raw Material Prices (Wood, Steel, Plastics) | -0.8% | National, with upstream import dependencies magnifying exposure | |

| Intense Domestic Competition & Price Pressure In B2B Tenders | -1.2% | National, concentrated in built-in and system furniture for construction | |

| Hybrid Work Reducing Net-New Office Space Demand | -0.6% | National, led by the technology and professional services sectors | |

| Distribution Model Shifts Post-Kftc Ruling Causing Near-Term Channel Disruption | -0.4% | National, particularly affecting established franchise networks | |

| Source: Mordor Intelligence | |||

Volatility In Raw Material Prices (Wood, Steel, Plastics)

Steel demand experienced a downcycle through 2025, followed by signs of stabilization into 2026, which added uncertainty to spot pricing and inventory planning for metal-intensive systems. Resin markets signalled mixed pricing dynamics, with polypropylene facing downward pressure from new capacity additions while certain specialty resins saw targeted price increases, which complicates BOM cost control in seating and desks. Wood supply risk has also evolved due to new deforestation rules in export markets and recovering demand trends, which can raise traceability and sourcing costs that are harder to pass through in price-sensitive tenders. On the competitive front, domestic enforcement actions against bid-rigging in built-in and system furniture have increased financial penalties and legal risk for suppliers, reshaping B2B bidding behavior and compressing margins. Some players restructured distribution or franchise practices after corrective orders, which added near-term channel friction in the South Korea office furniture market. Efficiency programs and disciplined procurement are therefore critical to protect profitability in a contested bid environment while sustaining product development.

Hybrid Work Reducing Net-New Office Space Demand

Vacancy across major districts stayed relatively low, yet the pace of rent increases moderated as hybrid policies normalized, which signals that net-new office footprints may not be the main growth engine over the medium term. The broader shift to value and cost control among occupiers is pressuring total furniture budgets even when per-square-meter specifications rise, which requires suppliers to defend mix and capture replacement cycles within the South Korean office furniture market. The rise of AI and automation is another risk to long-term headcount in certain white-collar roles, which could weigh on aggregate office demand even as densification and redesign continue. Payment and settlement regulations for large retailers and online platforms are tightening, which may change working capital profiles for distributors and digital intermediaries and alter channel economics in the near term. New prohibitions on unfair trade practices, along with shorter settlement cycles, raise compliance costs for platforms, which may consolidate share among scaled operators and require vendor terms to be renegotiated in the South Korean office furniture market. These shifts will favour manufacturers with flexible fulfilment models, omnichannel capabilities, and strong governance that can navigate changing platform rules.

Segment Analysis

By Product: Chairs Dominate; Collaborative Soft Seating Accelerates

Chairs held 33.74% of the South Korea office furniture market share in 2025, and collaborative soft seating shows the fastest trajectory at a 5.47% CAGR through 2031 within the South Korea office furniture market size baseline. The seating mix reflects sustained demand for certified ergonomic designs, with the SIDIZ T50 line meeting ANSI/BIFMA and Greenguard standards while scaling across international channels. Product expansion into compact and small-format models, such as SIDIZ T25 Small Ergonomic, extends multi-point adjustability to a wider range of users and workstation footprints. Retail availability of SIDIZ bestsellers on mainstream marketplaces corroborates broad adoption for both corporate and home-office use. Hybrid work programs keep pushing beyond traditional task-chair plus desk bundles, so buyers favor layouts that mix task seating with lounge pieces and booths to support collaboration and focus space.

Height-adjustable desks remain the natural companion to ergonomic seating, illustrated by PATRA’s T5 Motion Desk range and POUT’s TEKDEC2 MAX UOP electrified standing desk, configured for multiple plug standards to serve domestic and export demand. The expansion of Korea’s EPR and RoHS scope to all electrical and electronic products raises the bar for materials and component selection in powered desks and accessories. Regulatory enforcement in tenders, meanwhile, encourages more transparent pricing and channel practices, keeping storage and modular systems focused on value and documentation. Green Public Procurement requirements also guide demand toward certified furniture across a broad set of public buyers, which supports the adoption of modular storage, screens, and collaboration pieces.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Material: Wood Leads on Sustainability Mandates; Polymers Gain from Electrification

Wood led materials with 42.62% of the South Korean office furniture market share in 2025, reflecting both procurement standards and buyer preference for verified low-emission inputs. Market leaders report 100% third-party certified wood and fiber sourcing, high FSC penetration, and E0-grade panels across portfolios to meet indoor air and compliance targets. FSC frameworks and legality assurance support alignment with Korea’s timber-use rules and global due diligence expectations in export and multi-country supply chains. Process improvements at Korean plants, including scrap rate reductions on wood frame panels, reinforce the cost and sustainability case for wood-centric systems. Public procurement programs that explicitly reference eco-labels and verifiable documentation continue to anchor wood’s position in the materials mix.

Polymers post the fastest growth at a 4.82% CAGR through 2031 as electrified furniture and integrated power modules spread across workpoints and collaboration zones. The broadened EPR and RoHS compliance scope encourages compliant polymer formulations and tighter supplier controls in electronics-adjacent components. Variability in steel demand and trade conditions also plays into material substitution decisions, with Korea’s finished steel demand falling in 2024 and 2025 before a modest stabilization in 2026. For powered desks and cable management parts, polymers that meet substance thresholds and reliability criteria offer a robust route to compliance and weight management. Meanwhile, metal, glass, and textile accents persist across executive and lounge settings, supported by broad product catalogs from domestic system suppliers.

By Price Range: Mid-Tier Anchors Volume; Premium Segment Captures Upgrade Cycles

Mid-range products accounted for 53.19% of South Korea's office furniture market share in 2025, anchoring volume in refurbishments and fit-outs where value and flexibility are priority outcomes. Steady rent growth and cost focus among occupiers strengthen demand for durable finishes, modularity, and ergonomic features that deliver measurable workplace optimization. Integrated manufacturers with nationwide sales, logistics, and installation capabilities continue to win mid-range tenders with standardized systems and fast deployment. Business programs by leading brands, including bulk purchase benefits, reinforce mid-range economics for enterprise rollouts and office consolidations. Institutional buyers also rely on proven mid-range lines for training rooms and classrooms, such as PATRA’s education and lecture desks that balance ergonomic features with accessible pricing.

Premium products show the fastest growth at a 4.69% CAGR through 2031, supported by a flight to quality and ESG alignment that pushes higher specifications in city-center and new-build assets. Upgrades often include height-adjustable workstations, advanced ergonomic seating, and low-emission materials that align with wellness and sustainability protocols. Eco-certified portfolios from domestic leaders, along with documented recycled content and E0-grade wood, help premium bids meet stricter procurement criteria. Public agencies that purchase according to eco-label rules also support higher-spec products when lifecycle and emissions thresholds are required for eligibility. For smart desks and integrated power accessories, electrified compliance requirements direct premium spend toward verifiably compliant designs and suppliers with testing rigor.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End-User: Corporate Offices Anchor Demand; Hospitality Back-Office Surges

Corporate offices represented 38.10% of South Korea's office furniture market size in 2025, reflecting ongoing upgrades to hybrid-capable layouts and ergonomic baselines at scale. Low vacancy in major business districts and disciplined leasing have preserved fit-out momentum, with emphasis on space optimization and flexible floor plans. The leading domestic supplier’s breadth across seating, systems, and collaboration pieces supports comprehensive enterprise deployments and refresh programs. Case examples from corporate projects underscore demand for unified design languages and high-density layouts that enable easy reconfiguration. For multinationals and public institutions, procurement standards continue to favor tested products with third-party certifications and material disclosures.

Hospitality and retail back-office settings record the fastest growth at a 5.71% CAGR through 2031, as multi-purpose furniture packages support front-of-house and staff areas in mixed-use properties. Omnichannel retail investments, including new-format stores, keep driving office and back-of-house upgrades with standardized desks, storage, and collaborative areas. Healthcare and laboratory-adjacent workspaces continue to adopt specialized seating and storage built for technical environments, broadening demand beyond traditional office towers. Government and education buyers add depth through eco-label mandates that standardize eligibility criteria for desks, chairs, and case goods. Korea’s education spend profile supports quality-focused upgrades in learning environments, which keep ergonomic and flexible furniture relevant in classrooms and support spaces.

By Distribution Channel: B2B Direct Manufacturers Dominate; Online B2C Accelerates Digital Shift

B2B direct channels held 76.27% of the South Korean office furniture market share in 2025, driven by corporate tenders and public procurement processes that rely on verifiable eco-performance and installation capabilities. Green Public Procurement mandates that agencies purchase eco-labeled products, which concentrates demand among suppliers with certified portfolios. Distribution models are evolving as manufacturers adopt consignment and other structures following competition and franchise practice reviews. Business programs by leading brands, including transparent volume-based discounts, support enterprise refresh cycles and standardized national rollouts. Ongoing cartel and distribution oversight from KFTC continues to shape pricing behavior and channel terms in large B2B orders.

Online B2C is the fastest-growing route at a 6.13% CAGR through 2031 as omnichannel retail, store-based fulfillment, and price investments expand product access for home-office and small-office buyers. New store formats and mixed-use locations strengthen last-mile coverage and pickup options, which improve service for digital orders. Domestic brands leverage cross-border e-commerce with electrified desks designed for varied plug standards, which support export growth without heavy distribution footprints. Integrated manufacturers continue to build omnichannel capabilities around design consultation, installation, and after-sales service to serve both enterprise and small-business customers. KFTC updates on payment practices and platform

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Gyeonggi, including the Seoul Capital Area, is both the largest region at 41.31% share in 2025 and the fastest-growing at a 5.06% CAGR over 2026–2031, driven by low vacancy, stable rent growth, and persistent headquarters clustering that concentrates corporate spend. Premium corridors maintain low cap rates and draw organizations that justify elevated specifications to support talent attraction, wellness, and hybrid protocols, which sustains demand for ergonomic seating and height-adjustable systems. Co-working and flexible office providers are scaling within the capital region, and their short lease cycles and modular layouts translate into recurring refresh opportunities for the South Korean office furniture market. Retail expansion of large-format concept stores in Seoul has also improved last-mile capabilities for click-and-collect and ship-from-store models that lift B2C sales. Brand activations and showrooms in premium districts further reinforce Seoul’s status as the showcase venue for next-generation workplace concepts in the South Korean office furniture market.

Yeongnam, including Busan and surrounding hubs, benefits from cost advantages and owner-occupier transactions that stimulate refurbishment projects and replacement furniture cycles across existing buildings. Local manufacturing clusters and logistics corridors support vendor proximity and shorter lead times, which is a positive for project conversion and installation schedules. Emerging office districts and innovation zones promote hybrid layouts and collaboration spaces, which lead to balanced demand for systems furniture, seating, and acoustic elements in the South Korean office furniture market. Regional procurement practices continue to reflect the influence of national GPP rules, which help standardize eco-criteria and product documentation. New mixed-use developments in regional cities are also creating retail and showroom nodes that can support omnichannel fulfilment beyond the capital region.

Honam, Hoseo, Gangwon, and Jeju collectively contribute a steady base of demand grounded in public administration, education, tourism, and light industrial activity, each with distinct workspace requirements. Public procurement across these regions aligns with Ecolabel criteria, which reinforces a common product baseline for office equipment and furniture categories within the South Korean office furniture market. Hospitality and travel-linked businesses in Jeju favour modular lounge seating and movable tables, while education and research sites in Hoseo and Gangwon require durable systems and storage. Supplier case studies show the ability of regional manufacturers to execute national projects and export to multiple markets, which underscores the breadth of Korea’s production footprint. Over the forecast period, broader eco-compliance, lifecycle documentation, and disassembly design will likely shape specifications in regional bids across the South Korea office furniture market.

Competitive Landscape

Domestic incumbents hold strong brand equity and installation capacity, with leading players combining product breadth, nationwide service networks, and sustainability practices to serve both public and private demand in the South Korean office furniture market. Firms differentiate through integrated solutions that span planning, delivery, and after-sales service, which remain important in complex office moves and consolidations. Corporate programs to develop low-carbon furniture and to expand certified materials have become part of product roadmaps, which reinforces compliance credentials for regulated purchases. Local competitors also offer specialized seating, conference, and multi-use collections, providing buyers with a wider range of alternatives at various price points within the South Korean office furniture market. These conditions maintain moderate competitive intensity while rewarding vendors that bring credible sustainability, compliance, and fulfillment capabilities to each bid.

International brands operate with mixed regional fundamentals, yet they continue to invest in premium segments, technology-enabled products, and hybrid-ready solutions that resonate with multinational offices. Consumer-facing global retailers are also deepening their presence through store openings and automation of online order fulfilment, which has improved availability and delivery speed for home-office solutions across the South Korean office furniture market. With price investments on targeted SKUs and a circular approach to product life, these retailers capture growing consumer interest in sustainable home-office upgrades. The combination of premium office vendors and scaled retail entrants increases choice and expands service standards for buyers across channels.

Compliance has emerged as a key axis of competition, particularly as Korea expands EPR and RoHS requirements to all electrical and electronic products used within defined voltage thresholds, which captures many sit-stand desks and integrated power modules. Companies that embed compliance at design inception and use verifiable eco-materials can reduce retrofit risk and accelerate public tender eligibility, which confers a sustained advantage in the South Korea office furniture market. Digital-native challengers have leveraged e-commerce to bypass legacy distribution, marketing electrified desks with global plug options, and simplified assembly to serve both export and domestic B2C demand. Over the near term, evolving distributor payment deadlines and platform settlement rules will favour larger intermediaries and manufacturers with robust working-capital management and documented channel governance. These dynamics will help shape how share shifts across B2B and B2C routes over the forecast window in the South Korea office furniture market.

South Korea Office Furniture Industry Leaders

Livart Furniture Co., Ltd.

Fursys Inc.

Sangdo Furniture Co., Ltd

Kaos Co., Ltd.

Patra Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: IKEA Korea opened its fifth store, the 25,000-square-meter IKEA Gangdong, in the I-Park The River mixed-use complex in eastern Seoul on April 17, marking the first South Korean store integrated into shopping, entertainment, and business spaces, featuring 7,400 products with 3,700 available for immediate purchase, a sustainable living shop, a circular hub, and electric vehicle deliveries as part of a 300 million euro investment through 2026.

- May 2024: KOAS Co., a prominent furniture manufacturer from South Korea, debuted its latest brand, 'Space'. This new offering empowers customers to craft their workspaces with a sleek, minimalist aesthetic.

South Korea Office Furniture Market Report Scope

Office furniture refers to the items and fixtures used in an office setting to support various activities such as working, seating, and storage. The South Korean office furniture market is segmented by furniture type, distribution channel, and geography. By furniture type, the market is segmented into seating, tables, storage, desks, and other office furniture types. By distribution channel, the market is segmented into B2B/directly from the manufacturer and B2C/retail, comprising home centres, specialty stores, online, and others. By geography, the market is segmented into the Seoul Capital Area, Yeongnam, Honam, Hoseo, Gangwon, and Jeju. The Market Forecasts are Provided in Terms of Value (USD).

By Product

| Chairs | Employee Chairs |

| Meeting Chairs | |

| Tables | Conference Tables |

| Desks | |

| Other Tables | |

| Storage Units | Filing Cabinets |

| Bookcases & Shelving | |

| Sofas/Soft Seating | |

| Booths and Office Dividers | |

| Other Office Furniture (Stools, Reception Area Furniture, Accessories, Others) |

By Material

| Wood |

| Metal |

| Plastic & Polymer |

| Other Materials |

By Price Range

| Economy |

| Mid-range |

By End-user

| Corporate Offices |

| Healthcare Offices |

| Educational Institutions |

| Government & Public Offices |

| Hospitality & Retail Back-office |

| Others |

By Distribution Channel

| B2B/Directly from Manufacturer | |

| B2C/Retail | Home Centers |

| Specialty Furniture Stores | |

| Online | |

| Other Distribution Channel |

By Geography

| Gyeonggi (Seoul Capital Area) |

| Chungcheong |

| Gangwon |

| Gyeongsang |

| Jeolla |

| Jeju |

| By Product | Chairs | Employee Chairs |

| Meeting Chairs | ||

| Tables | Conference Tables | |

| Desks | ||

| Other Tables | ||

| Storage Units | Filing Cabinets | |

| Bookcases & Shelving | ||

| Sofas/Soft Seating | ||

| Booths and Office Dividers | ||

| Other Office Furniture (Stools, Reception Area Furniture, Accessories, Others) | ||

| By Material | Wood | |

| Metal | ||

| Plastic & Polymer | ||

| Other Materials | ||

| By Price Range | Economy | |

| Mid-range | ||

| By End-user | Corporate Offices | |

| Healthcare Offices | ||

| Educational Institutions | ||

| Government & Public Offices | ||

| Hospitality & Retail Back-office | ||

| Others | ||

| By Distribution Channel | B2B/Directly from Manufacturer | |

| B2C/Retail | Home Centers | |

| Specialty Furniture Stores | ||

| Online | ||

| Other Distribution Channel | ||

| By Geography | Gyeonggi (Seoul Capital Area) | |

| Chungcheong | ||

| Gangwon | ||

| Gyeongsang | ||

| Jeolla | ||

| Jeju | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the outlook for the South Korea office furniture market through 2031?

The South Korea office furniture market size is USD 2.49 billion in 2026 and is projected to reach USD 3.52 billion by 2031, implying a 7.17% CAGR.

Which products lead demand and what is growing fastest in South Korea office furniture?

Chairs led with 33.74% share in 2025, while collaborative soft seating shows the fastest growth trajectory through 2031 as hybrid layouts expand collaboration zones.

How are regulations affecting electrified desks and power-integrated furniture in South Korea?

Presidential Decree No. 35467 expands EPR and RoHS to all electrical and electronic products within defined voltage limits starting January 1, 2026 for EPR, with substance limits of 0.1% for ten restricted substances and 0.01% for cadmium

How does Green Public Procurement shape buying for South Korea office furniture?

The program requires 1,176 national agencies and 30,000 sub-public authorities to purchase KEITI Ecolabel or Good Recycled Mark products, with total green purchases reaching 3.8 trillion won in 2021 and office-related categories forming a large share of certified items.

Which sales channels matter most for South Korea office furniture?

B2B is the largest route at 52.38% in 2025, while B2C is the fastest growing at a 12.38% CAGR through 2031 on the back of omnichannel and online fulfillment.

Which region is the demand center within South Korea office furniture?

The Gyeonggi, including the Seoul Capital Area accounts for 41.74% in 2025 and is set to grow at a 7.87% pace through 2031, supported by tight vacancy and headquarters clustering.