Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

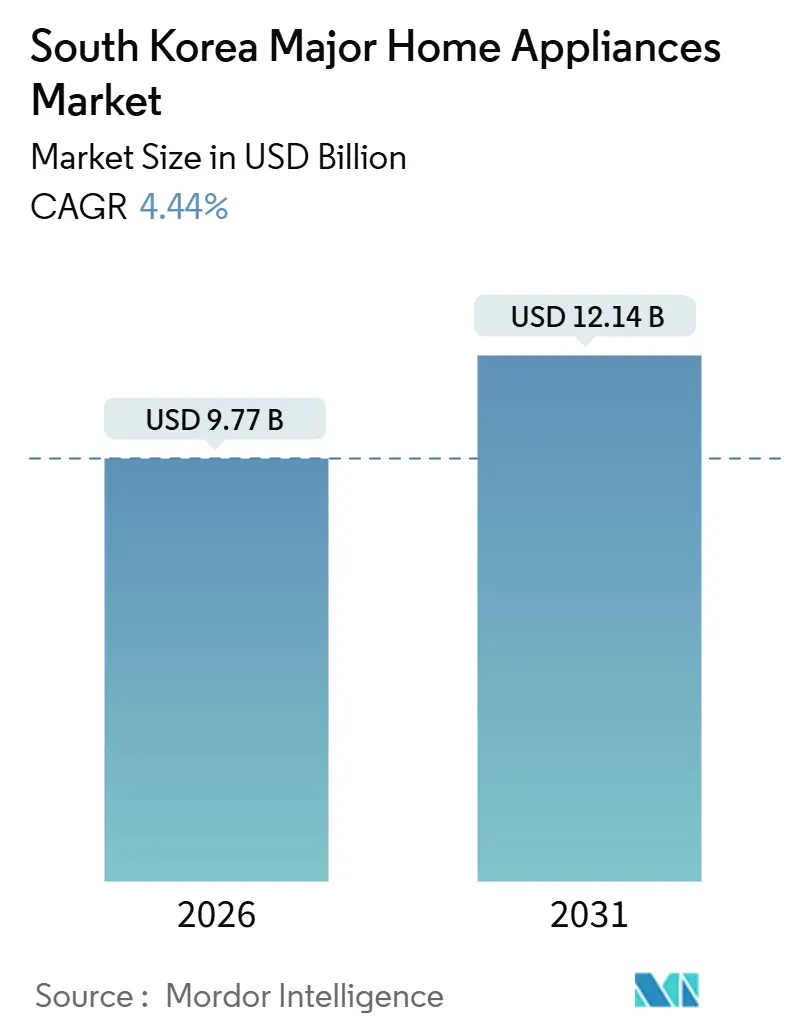

| Market Size (2026) | USD 9.77 Billion |

| Market Size (2031) | USD 12.14 Billion |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

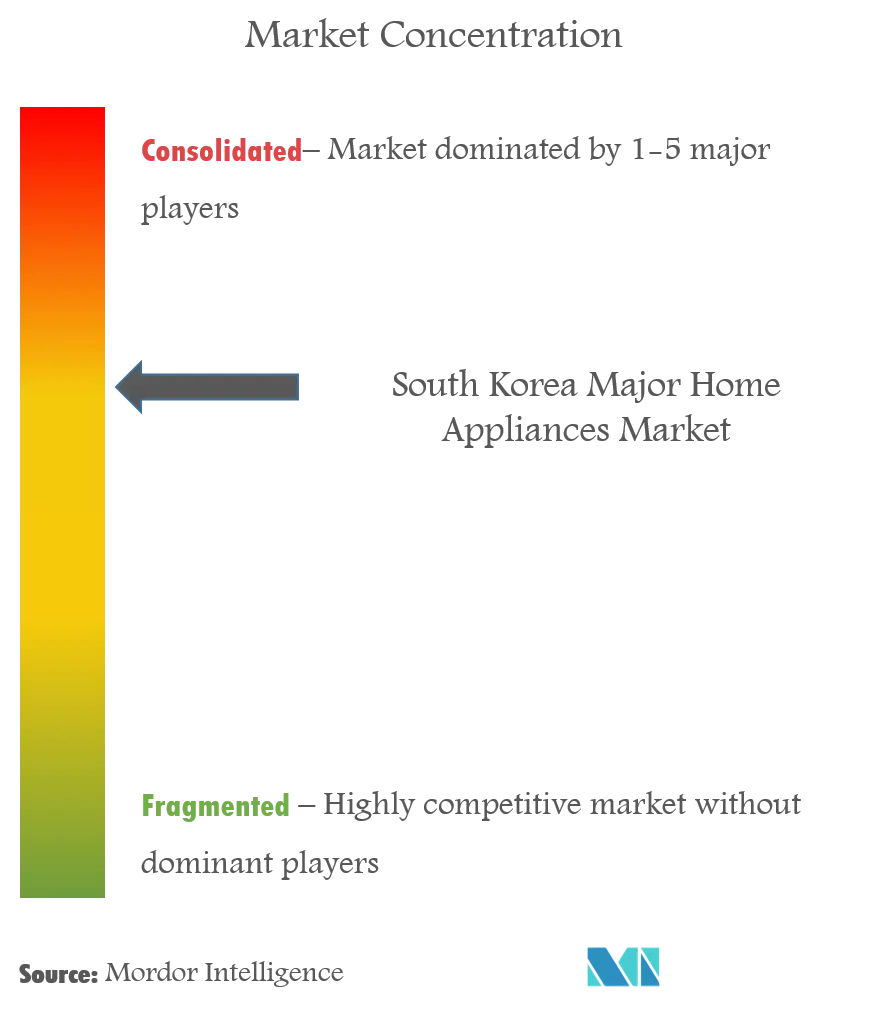

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Major Home Appliances Market Analysis by Mordor Intelligence

The South Korea major home appliances market size is USD 9.77 billion in 2026 and is projected to reach USD 12.14 billion by 2031, expanding at a 4.44% CAGR. Refrigerators lead revenue with a 30.15% share in 2025, while dishwashers remain a niche category that is now growing fastest at a 4.62% CAGR as single-person households favor compact, rental-ready formats suited to smaller living spaces. July 2025’s Top Efficiency Appliance Rebate Program unlocks a 10% refund for Grade-1 products within a 267.1 billion won budget cap, lifting first-month consumer spending to 882 billion won and helping trigger 29% year-on-year sales gains for participating retailers[1]Source: Korea Bizwire, “Energy Efficiency Rebate Program Boosts Appliance Sales,”Korea Bizwire, koreabizwire.com. Minimum Energy Performance Standards restrict substandard models and require Grade-1 units in the public sector, which embeds replacement demand across both households and institutions. The South Korea major home appliances market benefits from ecosystem-led differentiation, where seven-year software support for new AI-enabled models and tighter energy rules together reinforce premium segments that offer visibility on margins over the forecast horizon.

Key Report Takeaways

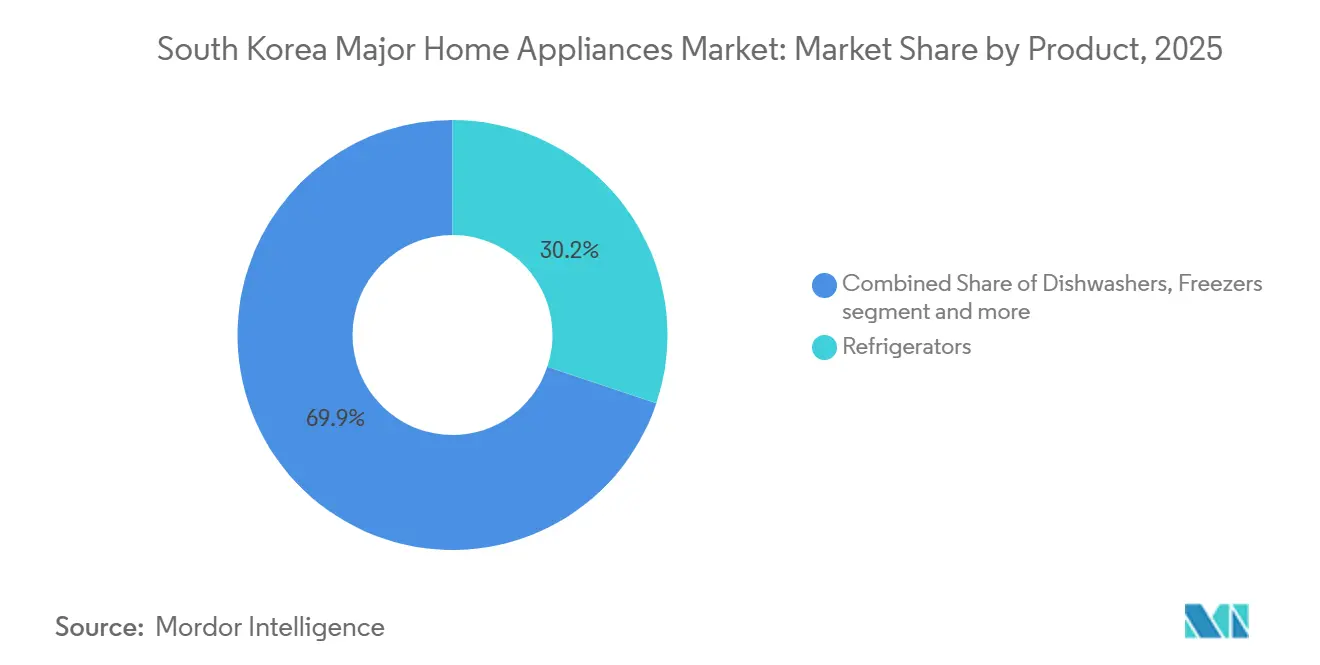

- By product, refrigerators led with 30.15% of the South Korea major home appliances market share in 2025; dishwashers are forecast to expand at a 4.62% CAGR through 2031.

- By distribution channel, multi-brand stores held 38.72% of the South Korea major home appliances market share in 2025, while online recorded the highest projected CAGR at 5.84% through 2031.

- By geography, Gyeonggi Province accounted for 35.38% of the South Korea major home appliances market share in 2025, and Gyeongsang is projected to grow at a 5.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Major Home Appliances Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce penetration is accelerating appliance sales | +0.8% | Global, strongest in the Seoul Capital Area and Gyeonggi due to logistics density | Short term (≤ 2 years) |

| Mandatory efficiency labels and standards elevating replacement demand | +1.2% | National, with early gains in public-sector buildings in Seoul, Busan, and Incheon | Medium term (2-4 years) |

| Smart-home adoption is fueling connected appliance uptake | +0.9% | National, with Seoul Capital Area and Gyeonggi leading | Medium term (2-4 years) |

| Government rebate program for replacing Grade-3 or lower appliances | +1.3% | National, metropolitan areas benefit from higher participation rates | Short term (≤ 2 years) |

| Rise of single-person households driving demand for premium compact formats | +0.9% | National, with spillover concentrated in Seoul, Busan, and Gyeonggi urban cores | Long term (≥ 4 years) |

| Export-oriented manufacturing clusters are shortening domestic refresh cycles | +0.4% | Gyeongsang Province and Chungcheong, due to proximity to semiconductor supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Penetration Accelerating Appliance Sales

Online channels post a 5.84% CAGR, the fastest among distribution modes for the South Korea major home appliances market, as nationwide digital adoption lifts transactions that rely on mobile-first behavior. The National Logistics Basic Plan enables warehouse automation and shortens bulky-goods delivery times to same-day windows in dense areas, which improves conversion for refrigerators and washing machines sold online. Blockchain-linked e-receipts strengthen trade-in funnels and bring forward replacement cycles for premium users who value speed and convenience in service flows. The economics of online fulfillment favor compact and mid-tier products that renters can install without technicians, while built-in and high-end units keep moving through specialist retail due to installation complexity. Samsung and LG promote augmented-reality previews through app ecosystems to reduce return rates and strengthen system lock-in across connected devices, which further widens the capability gap with smaller brands that lack software reach.

Mandatory Efficiency Labels and Standards Elevating Replacement Demand

Tighter Minimum Energy Performance Standards prohibit production or sale below fifth-grade efficiency and require Grade-1 units for public-sector procurement, which directly raises the replacement rate across key categories in the South Korea major home appliances market. Draft amendments extend coverage to additional categories like electric fans using BLDC motors and clothes dryers, reinforcing the pipeline of compliant products before deadlines in 2026 and 2027. Upgrading to inverter-based systems reduces power bills and shortens payback periods for households that adopt premium-grade models with smart energy features. Field data from the 2010-era EPR pilot showed that introducing mandatory labeling drove refrigerator recycling rates from 48% to 87%, demonstrating that information asymmetry—not purchase price—was the primary barrier[2]Source: Ministry of Environment, “Extended Producer Responsibility (EPR),” Ministry of Environment, www.thegpsc.org. Manufacturers that lead in inverter compressors and eco-friendly refrigerants build an advantage that translates into brand preference and stickier upgrade paths within connected homes.

Smart-Home Adoption Fueling Connected Appliance Uptake

Korea’s connected-home base benefits from early 5G rollout and the scale of Samsung’s SmartThings platform, which now spans hundreds of millions of global users and underpins seamless device orchestration in the South Korea major home appliances market[3]Source: Samsung Global Newsroom, “A Home Companion Making Daily Life More Effortless,” Samsung Global Newsroom, news.samsung.com. Builder pre-installation in premium apartments normalizes plug-and-play experiences and removes friction at move-in, which nudges households toward smart refrigerators, washing machines, and air quality devices tied to a unified hub. Dynamic tariffs from the utility side strengthen the case for automated scheduling, as appliances shift cycles to off-peak hours through AI features to lower bills. The competitive tension centers on closed versus open ecosystems, with incumbents pushing end-to-end integrations while budget challengers adopt Matter standards to appeal to renters and mixed-brand households. Samsung’s 2026 integration of Google Gemini into its Bespoke AI Family Hub refrigerator expands food recognition and shares cooking parameters with synced ovens, which illustrates how AI elevates device utility while raising switching costs in the South Korea major home appliances market.

Government Rebate Program for Replacing Grade-3 or Lower Appliances

Grade-1 purchases up to 300,000 won per item, creating a clear near-term pull for energy-efficient models across the South Korea major home appliances market. First-month results registered 662,000 applications drawing 88.2 billion won in rebates, implying 882 billion won in total consumer spending and triggering 29% year-on-year sales lifts for participating retailers; one air-purifier partner saw sales jump 584%, and a rental corporation reported a 92% increase with dehumidifier demand spiking sixteen-fold[4]Source: CHOSUNBIZ, “Top-efficiency appliance rebate boosts Korean appliance sales by reviving demand,” CHOSUNBIZ, biz.chosun.com. Rental products qualify for the benefit, which supports subscription models that bundle maintenance and lower up-front costs for compact appliances like dishwashers. Policy debate continues over the distribution of benefits, but the program’s structure brings forward the retirement of older stock and accelerates the diffusion of high-efficiency baselines. The replacement effect is most visible in metropolitan areas with robust retail participation and strong awareness of energy-label criteria.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Household penetration approaching saturation | -0.7% | National, refrigerators and washing machines exceed 95% penetration | Long term (≥ 4 years) |

| Shrinking average floor space is limiting demand for large-format appliances | -0.3% | Urban cores in Seoul, Busan, and Incheon, with many single-person homes under 40 m² | Long term (≥ 4 years) |

| Extended-producer-responsibility recycling costs are squeezing margins | -0.5% | National obligations expanded in 2026 to all electrical and electronic products. | Medium term (2-4 years) |

| Volatile steel and resin prices linked to regional geopolitical shocks | -0.9% | National, compounded by reciprocal tariffs and resin-price spikes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Household Penetration Approaching Saturation

Refrigerators and washing machines are already in almost every home, which shifts growth from first-time purchases to replacement cycles in the South Korea major home appliances market. New-build housing slows compared with prior periods, so the traditional move-in wave contributes less to volume than in past cycles. Consumers facing higher rates and prices extend ownership periods for larger appliances, which lengthens the interval between purchases. Premium households still replace faster to capture AI features and aesthetics, while lower-income cohorts stretch lifespans through repairs, which results in a bifurcated pattern that masks nuance in simple penetration metrics. Dishwashers stand out as a penetration gap where compact and rental-ready formats can scale despite saturation in core white goods.

Shrinking Average Floor Space Limiting Demand for Large-Format Appliances

Nearly half of single-person homes occupy less than 40 square meters, which constrains demand for large-capacity refrigerators and washers in dense urban cores. Consumers pivot toward French-door models with optimized internal organization and stackable or combo laundry formats that reclaim vertical space. Premium compact models can maintain price points when they bundle AI features, voice control, and app diagnostics that lift perceived value without increasing size. Built-in solutions gain traction in renovations where integrated designs free up countertops and reduce clutter in smaller kitchens. Regional variations persist in less dense provinces, which require inventory strategies that balance compact demand with residual interest in large formats.

Segment Analysis

By Product: Refrigerators Lead Revenue While Dishwashers Post Segment's Fastest Growth

Refrigerators account for 30.15% of 2025 revenue, giving them the largest position in the South Korea major home appliances market, while households favor feature-dense formats that fit smaller urban layouts. Premium configurations with AI vision, flexible compartments, and app-based monitoring lift revenue share even as average unit sizes moderate in dense markets. Dishwashers remain under 5% penetration, but the category becomes the fastest mover at a 4.62% CAGR as compact and rental-ready units solve constraints around space and up-front cost. Rental eligibility within the national rebate program reduces barriers for first-time adopters and supports the expansion of subscription packages that include maintenance and consumables. This pattern elevates compact formats that monetize software, connectivity, and design as part of value creation in the South Korea major home appliances market.

Dishwashers continue to show momentum as both households and small businesses standardize on convenience and hygiene features that match space limitations in dense housing. Washing machines hold a significant base, with AI cycles and resource optimization reducing energy and water use while improving convenience in laundry workflows. Air conditioners contribute a meaningful share and align with the national push toward high-efficiency systems and heat pump adoption under a broader decarbonization plan. Ovens and induction cooktops benefit from compact kitchens that reward built-in designs and precise temperature control as part of premium cooking experiences. The South Korea major home appliances industry aligns product roadmaps to software-supported features and over-the-air updates, which convert white goods into long-lived platforms with serviceable add-ons.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Multi-Brand Stores Anchor Sales Yet Online Posts Fastest CAGR

Multi-brand stores retain 38.72% of 2025 sales as shoppers evaluate physical attributes and seek bundled services like installation, extended warranties, and take-back of old units. Brand-exclusive outlets complement this with immersive showrooms and ecosystem demos that drive attachment to connected platforms and premium aesthetics. The online channel posts the fastest 5.84% CAGR as same-day fulfillment becomes more common for bulky items and as mobile-first purchasing becomes a preferred path for compact appliances in the South Korea major home appliances market size context for channel growth. Virtual try-out tools reduce measurement and fit errors and lower return rates, which helps profitability at comparable delivery fees. Government procurement rules that restrict purchases to Grade-1 products concentrate institutional demand in brands with rapid compliance track records.

The channel mix reflects distinct product economics, as online excels in compact and mid-tier units while built-in and ultra-premium remain anchored offline due to site measurement, specialty installation, and synchronized scheduling with renovations. Subscription rentals now account for a rising share of online appliance transactions as consumers substitute monthly fees for up-front payments and receive scheduled maintenance. Exclusive brand outlets absorb higher operating costs, yet they serve as IoT integration hubs where connected experiences across refrigeration, laundry, air care, and energy management encourage multi-device adoption in the South Korea major home appliances industry. Regulatory oversight on pricing and cross-border marketplace practices will influence discounting headroom and sourcing transparency for imported appliances. The net outcome is a hybrid path where online and offline reinforce each other through showrooms, service integration, and digitized trade-in journeys in the South Korea major home appliances market.

Geography Analysis

Gyeonggi Province holds 35.38% of the 2025 demand and anchors the South Korean major home appliances market share through the density and income profile of the Seoul Capital Area. Strong logistics nodes enable faster delivery times, and high apartment penetration with builder-installed IoT infrastructure creates favorable conditions for connected premium models. Growth moderates as living space shrinks and primary demand is saturated, yet premium features maintain pricing power despite compact footprints. Single-person homes in the province exceed the national average, which amplifies demand for mini-refrigerators, stackable combos, and compact dishwashers with rental options. The region sets trends that diffuse nationwide through online channels and brand-exclusive showrooms that showcase ecosystem integrations in the South Korea major home appliances market.

Gyeongsang posts the fastest projected 5.47% CAGR as engineering-heavy workforces and industrial clusters support frequent product refreshes and early adoption of AI-enabled models. Provincial AI programs earmark 1.19 trillion won through 2030 for factory transformation, which strengthens pilot-to-production cycles and speeds deployment of new SKUs in the South Korea major home appliances market size for regional momentum linked to industrial policy. Busan’s construction cycle supports built-in appliance adoption at the premium end, while white-collar households upgrade more frequently to connected products that fit compact city layouts. Co-location with advanced assembly and component suppliers bolsters the pace of learning across iterations and reduces lead times for parts that enable AI on-device performance. The region, therefore, balances premium residential demand with institutional and commercial requirements tied to local manufacturing strength in the South Korea major home appliances market.

Chungcheong, Gangwon, Jeolla, and Jeju together account for a meaningful share of revenue with slower CAGRs due to older demographics and more detached housing, which dampen the pace of smart adoption compared to the capital area. Each area maintains distinct niches, including commercial cooling tied to agriculture or tourism, and HVAC demand linked to year-round hospitality operations. Provincial enforcement timelines for energy codes and ZEB-aligned building standards roll out unevenly, which staggers the onset of mandated efficiency upgrades. Regions with earlier enforcement pull demand forward for Grade-1 units in procurement and new construction, then normalize as code cycles complete. Retailers and brands align inventory strategies to local housing patterns and price sensitivity to sustain conversion across the South Korea major home appliances market.

Competitive Landscape

Market concentration remains high as LG Electronics and Samsung Electronics together hold half of 2025 revenue, while the top five brands collectively exceed two-thirds of the South Korea major home appliances market. The leading players leverage vertical integration, semiconductor expertise, and cloud ecosystems to defend share through cross-device functionality and long software support cycles. Platform lock-in raises switching costs as SmartThings users prefer compatible upgrades to preserve orchestration of refrigeration, laundry, air care, and cleaning devices. New entrants from China undercut on price in robot vacuums and selected washer formats, but they face a platform gap where over-the-air updates, service networks, and integrations remain thinner. Policy-driven efficiency criteria, certification timing, and procurement rules continue to shape shelf space and bid outcomes that favor early movers in compliance in the South Korea major home appliances market.

Strategic moves focus on AI-first products, integrated services, and expansion into higher-margin adjacencies like industrial and data-center HVAC equipment. Samsung announced a transaction to acquire FläktGroup in 2025 to extend its reach into mission-critical cooling as data-center demand scales with AI workloads. LG operationalizes its AI in Action approach across ThinQ-enabled devices and explores partnerships that monetize predictive maintenance and energy optimization within connected homes. Product pipelines emphasize on-device AI with chipsets designed for local inference to avoid cloud latency for functions like object recognition and environmental sensing. Competitive intensity persists in under-penetrated categories like dishwashers and in nascent heat pump systems that align with decarbonization goals and building code trajectories in the South Korea major home appliances market.

Tariff exposure and resin volatility pressure cost structures, and encourage materials innovation that reduces weight while maintaining rigidity and thermal performance. Long-dated supply agreements cushion the impact for some inputs, yet pricing resets and currency swings require margin defense through mix shifts toward premium and connected models. Standards engagement and interoperability initiatives influence the balance between closed and open ecosystems and guide investment in developer tools for third-party integration. The South Korea major home appliances market therefore centers competition on platform economics, service attachment, and lifecycle value rather than only unit shipments or hardware specs.

South Korea Major Home Appliances Industry Leaders

LG Electronics

Samsung Electronics

Winia Electronics

SK Magic (Dong Yang Magic)

Coway Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: LG Electronics unveiled LG CLOiD™, an AI-enabled home robot designed to perform household chores and integrate with LG’s ThinQ smart-home ecosystem, representing its “Zero Labor Home” vision for AI-driven domestic automation.

- December 2025: Samsung’s Bespoke AI Jet Bot Steam Ultra robot vacuum: Samsung introduced the Bespoke AI Jet Bot Steam Ultra, featuring AI object and liquid recognition, Qualcomm Dragonwing AI processing, and EasyPass Wheel tech for better navigation and cleaning performance.

South Korea Major Home Appliances Market Report Scope

Major appliances comprise major household appliances such as refrigerators, freezers, dishwashers, and ovens, among others. A complete background analysis of the South Korean major home appliances Industry, which includes an assessment of the industry associations, overall economy, emerging market trends by segments, significant changes in the market dynamics, and market overview, is covered in the report. The report also offers profiles of key players operating in the market.

The South Korean major home appliances market is segmented by product into refrigerators, freezers, dishwashers, washing machines, cookers and ovens, and other products, by distribution channel into supermarkets and hypermarkets, specialty stores, E-Commerce, and other distribution channels.

The report offers market size and forecasts for the South Korean major home appliances market in value (USD) for all the above segments.

By Product

| Refrigerators |

| Freezers |

| Washing Machines |

| Dishwashers |

| Ovens (Incl. Combi & Microwave) |

| Air Conditioners |

| Other Major Home Appliances (hoods, hobs, etc.) |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Region

| Chungcheong |

| Gangwon |

| Gyeonggi |

| Gyeongsang |

| Jeolla |

| Jeju |

| By Product | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances (hoods, hobs, etc.) | |

| By Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| By Region | Chungcheong |

| Gangwon | |

| Gyeonggi | |

| Gyeongsang | |

| Jeolla | |

| Jeju |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for the South Korea major home appliances market?

The South Korea major home appliances market size is USD 9.77 billion in 2026 and is projected to reach USD 12.14 billion by 2031, reflecting a 4.44% CAGR.

Which product categories are leading and which are growing fastest in South Korea?

Refrigerators lead with a 30.15% share in 2025, and dishwashers post the fastest 4.62% CAGR as compact and rental-ready formats gain traction.

How are energy-efficiency policies affecting appliance replacement in South Korea?

Minimum Energy Performance Standards and the 2025 Grade-1 rebate program are accelerating replacement of older stock and prioritizing high-efficiency units in public procurement.

Which channels are driving sales growth for appliances in South Korea?

Multi-brand stores hold the largest share at 38.72% in 2025, while online posts the fastest 5.84% CAGR, supported by logistics upgrades and mobile-first buying.

What regions are most important to appliance demand in South Korea?

Gyeonggi holds 35.38% of the 2025 demand, while Gyeongsang is the fastest-growing region with a 5.47% CAGR supported by industrial clusters and AI-focused investments.