South Korea HVAC Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

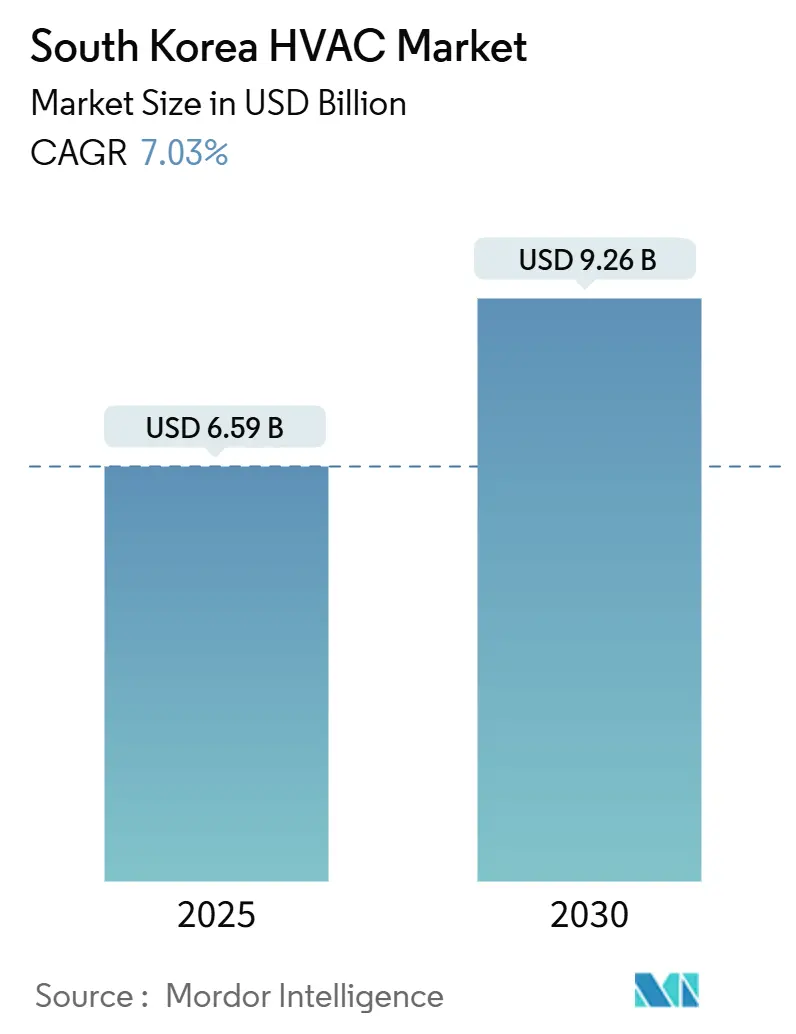

| Market Size (2025) | USD 6.59 Billion |

| Market Size (2030) | USD 9.26 Billion |

| Growth Rate (2025 - 2030) | 7.03% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea HVAC Market Analysis by Mordor Intelligence

The South Korea HVAC market size was valued at USD 6.59 billion in 2025 and is forecast to reach USD 9.26 billion by 2030, advancing at a 7.03% CAGR during 2025-2030. Expansion is being propelled by energy-efficiency mandates, digitalization of industrial facilities, and stringent refrigerant regulations that are reshaping product demand across residential, commercial, and industrial end users. High subsidy levels, rapid roll-out of heat pump technology, and accelerated retrofitting of an aging building stock have become the primary volume catalysts. In parallel, data-center construction and hydrogen-ready roadmaps are creating specialized equipment opportunities, while supply-side entrants are pursuing service-centric models to secure lifetime revenue streams. Competitive intensity is growing as Samsung and LG Electronics acquire specialist HVAC companies to address mission-critical applications.

Key Report Takeaways

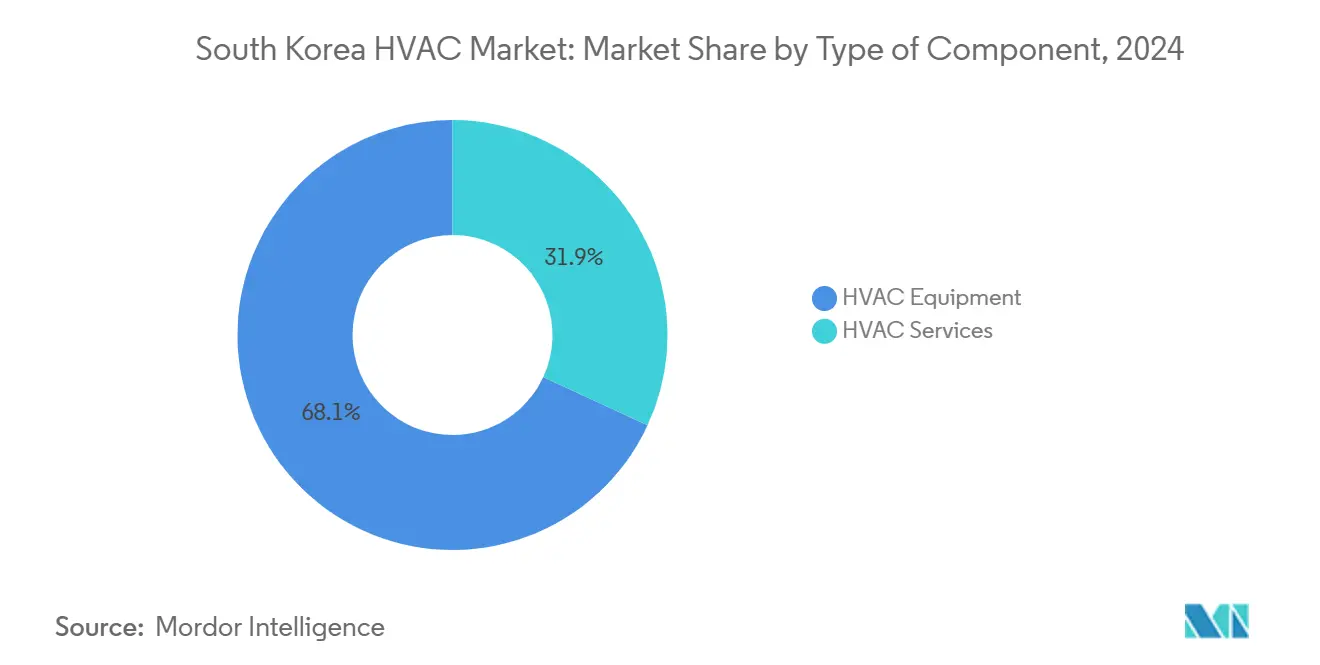

By component, HVAC equipment captured 68.1% of the South Korea HVAC market share in 2024; HVAC services are set to post the fastest 9.8% CAGR through 2030.

By end-user industry, the residential segment accounted for 45.5% revenue in 2024, whereas commercial buildings are expected to grow at 9.5% CAGR to 2030.

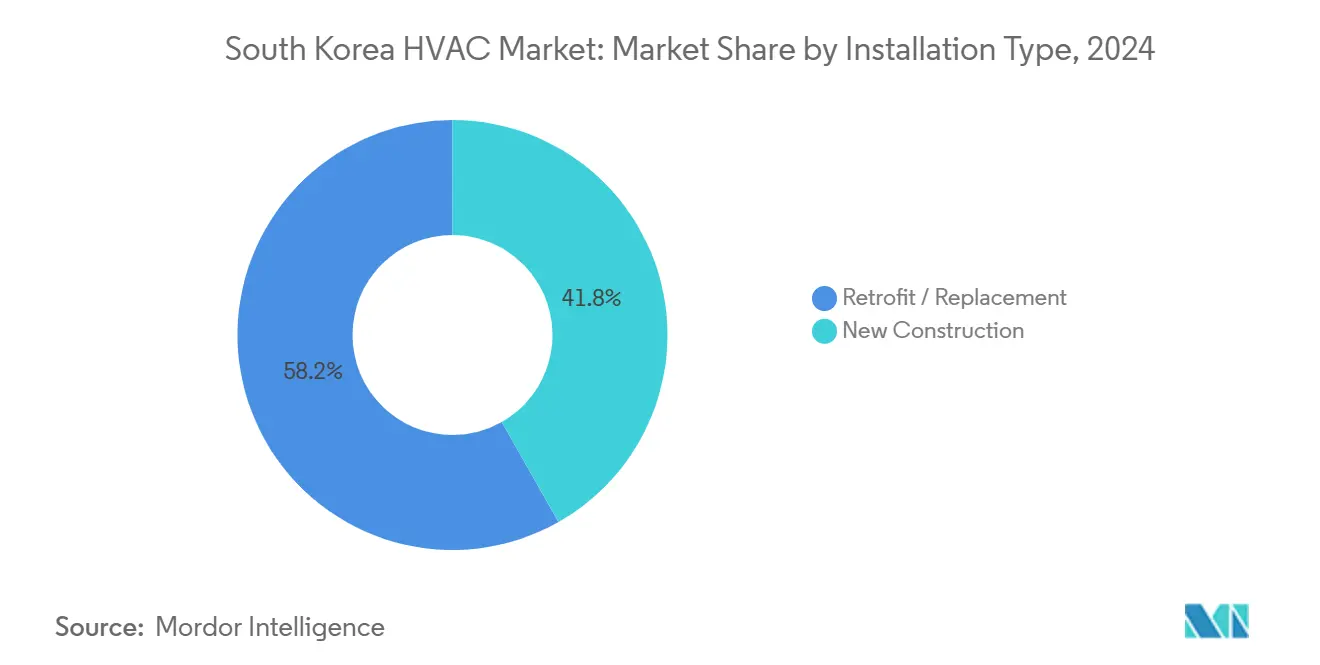

By installation type, retrofit projects held 58.2% of the South Korea HVAC market size in 2024, while new construction is projected to expand at a 7.4% CAGR between 2025-2030.

By capacity, 5-20 kW systems led with 32.1% market share in 2024; units up to 5 kW are forecast to rise at a 10.3% CAGR through 2030.

South Korea HVAC Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive government incentives (tax credits) | +1.8% | National, concentrated in metropolitan areas | Short term (≤ 2 years) |

| Increasing demand for energy-efficient devices | +1.5% | National, with stronger adoption in commercial sector | Medium term (2-4 years) |

| Construction boom and retrofits | +1.2% | National, with early gains in Seoul, Busan, Incheon | Medium term (2-4 years) |

| AI-data-center cooling demand surge | +0.9% | National, concentrated in Gyeonggi Province | Long term (≥ 4 years) |

| Hydrogen-ready heat-pump roadmap | +0.6% | National, pilot programs in industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supportive government incentives drive market acceleration

High-value subsidies reshaped HVAC economics over 2024-2025. The Ministry of Trade, Industry and Energy budgeted KRW 37.9 billion to reimburse 40% of efficient equipment costs for small businesses, improving payback periods to five years or below. [1]Ministry of Trade, Industry and Energy, “2025 Small Business High-Efficiency Equipment Support Project,” kharn.krSeoul added a geothermal replacement grant that covered 70% of capex up to KRW 150 million for systems older than nine years — a policy that stimulated retrofit orders across 1,200 buildings in 2024. R&D tax credits allowed SMEs to claim 25% of development spend, accelerating local design of low-GWP refrigerant platforms. These layered incentives not only reduced upfront costs but also created demonstration sites that influenced wider adoption across the South Korea HVAC market.

Energy-efficiency mandates reshape technology adoption

Zero Energy Building (ZEB) rules that started applying to private construction in 2025 pushed developers toward all-electric heating and cooling. Heat pumps deliver up to five-fold improvements in primary-energy performance versus gas boilers, making them the default compliance pathway. Building codes were updated with passive-survivability criteria to ensure thermal comfort during grid outages, raising minimum efficiency ratios for packaged units. Suppliers responded with products such as Samsung’s EHS line, which uses R290 refrigerant and trimmed annual power consumption by 15% compared with earlier designs. Regulatory certainty has therefore accelerated the switch to low-GWP, high-COP systems across the South Korea HVAC market.

Construction market dynamics create mixed growth signals

Total construction outlays declined 3% in 2024 and were projected to fall 4.2% in 2025, curbing near-term project pipelines. [2]Korea Development Institute, “Economic Outlook 2025,” kdi.re.kr Yet retrofit spending surged as owners upgraded buildings erected before 2010 to meet new performance thresholds. AI-driven data-center investments provided a countercyclical boost, with domestic operators commissioning hyperscale campuses requiring around-the-clock cooling redundancy. Factory Energy Management Systems were retrofitted into process plants, integrating HVAC controls with production scheduling to save up to 18% electricity.

AI-driven data-center cooling demands accelerate market growth

Global data-center cooling expenditure was expected to climb from USD 16.7 billion to USD 44.1 billion by 2030, and South Korea’s digital-hub status positioned local suppliers to capture premium projects. Samsung purchased Europe’s FläktGroup for EUR 1.5 billion to access adiabatic and indirect evaporative cooling technologies suitable for high-density racks. Gyeonggi Province alone approved eight new campuses in 2024-2025, each specifying triple-redundant chiller loops and AI-enabled airflow management. These projects are forecast to lift applied chiller shipments by 11% CAGR within the South Korea HVAC market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of efficient systems | -0.8% | National, more pronounced in rural areas | Short term (≤ 2 years) |

| Upcoming F-gas phase-down compliance costs | -0.6% | National, concentrated in commercial sector | Medium term (2-4 years) |

| Skilled HVAC technician shortage | -0.4% | National, acute in metropolitan areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High upfront costs challenge adoption despite long-term savings

Advanced heat pumps still commanded 2-3× higher list prices than legacy boilers in 2024, deterring smaller enterprises despite efficiency gains [3]International Energy Agency, “Heat Pumps 2024,” iea.org. While subsidies cover up to 40-70% of hardware, many buyers must self-finance the remainder. Payback periods often exceed five years, conflicting with shorter budgeting cycles. Commodity inflation raised equipment price tags by 9% between 2023-2024, prolonging return-on-investment horizons.

F-gas phase-down regulations impose transition costs

South Korea froze HFC production and import levels in 2024 and will cut volumes 10% by 2029 and 80% by 2045. From 2028, high-GWP refrigerants will be progressively banned in large commercial systems. Manufacturers must redesign equipment around HFO blends or natural refrigerants, while installers need extra safety training. Cold-chain operators voiced concern that retrofit bills could erode profit margins without supplemental grants.

Segment Analysis

By Type of Component: Services ascend amid equipment primacy

HVAC equipment retained 68.1% share of the South Korea HVAC market in 2024 because retrofits and subsidy-driven heat-pump rollouts sustained unit demand. Yet services revenue advanced at a 9.8% CAGR, reflecting the shift toward life-cycle optimization contracts. Energy-performance guarantees, predictive maintenance, and remote diagnostics delivered recurring cash flows for suppliers. LG Electronics’ Premier Service Champion initiative trained 600 technicians annually, boosting first-time fix rates and reinforcing customer loyalty. As zero-energy directives stiffened, building owners prioritized after-sales expertise, tilting value toward service teams rather than stand-alone hardware.

In 2025-2030, bundled equipment-plus-service propositions are forecast to dominate procurement. Manufacturers now engineer platforms for fast refrigerant retrofits to comply with Kigali timelines, capturing upgrade fees throughout the product life cycle. Consequently, services are expected to narrow the revenue gap with equipment, although hardware will still anchor the South Korea HVAC market size by 2030.

By End-User Industry: Commercial momentum narrows the gap

Residential buildings delivered 45.5% of 2024 revenue, buoyed by subsidy access for individual apartment owners. However, commercial premises are projected to post a 9.5% CAGR, outpacing other sectors through 2030 as offices, retail chains, and data centers upgrade to ZEB standards. The South Korea HVAC market size for commercial data centers alone is forecast to swell in tandem with AI rollouts, raising chiller and CRAH demand. Healthcare campuses upgraded isolation ventilation in response to pandemic lessons, while educational facilities replaced legacy split units with central heat pumps to cut operating costs.

Industrial customers integrated HVAC with Factory Energy Management Systems to stabilize thermal conditions without wasting energy, attracting investments under Korean Green New Deal frameworks. Although residential upgrades remain sizable, commercial buyers will increasingly dictate technology roadmaps and premium features in the South Korea HVAC market.

By Installation Type: Retrofit strength offsets construction lull

Retrofit activity held 58.2% revenue share in 2024 as owners modernized buildings erected before 2010. Seoul’s geothermal grant program triggered mass replacement of end-of-life water-source heat pumps, pushing retrofit order books to record levels. Conversely, new construction starts dipped on weak housing completions, yet large data-center and hospital projects maintained demand for high-capacity chillers. Between 2025-2030, new builds are expected to rebound with a 7.4% CAGR, driven by the government’s 2030 target of 30% ZEB penetration. Mandatory upgrades during major renovations will nonetheless ensure retrofit spending remains resilient, anchoring more than half of South Korea HVAC market revenue.

By Capacity Range: Small systems surge

Systems rated 5-20 kW captured 32.1% of 2024 sales by serving small commercial buildings. Units up to 5 kW, however, are expanding at the fastest 10.3% CAGR as single-family homeowners opt for room-scale heat pumps financed through low-interest green loans. Samsung’s WindowFit wind-free air-conditioner exemplified the segment’s focus on comfort and quiet operation while complying with evolving energy labels. The 20-50 kW band caters to midsize offices, whereas above-200 kW platforms address hyperscale data centers, hospitals, and semiconductor fabs that demand 24/7 uptime. Capacity diversification therefore mirrors South Korea’s heterogeneous building stock and shifting end-user investment priorities across the South Korea HVAC market.

Geography Analysis

Asia-Pacific commanded 81.3% regional share of South Korean HVAC exports in 2024, and intra-regional trade lifted unit volumes despite domestic construction softness. Seoul, Busan, and Incheon recorded the largest retrofit counts because their dense high-rise clusters were built before current efficiency codes. Gyeonggi Province emerged as the data-center epicenter, drawing global cloud providers and elevating demand for mission-critical cooling. Jeju Island’s tourism-driven hotel construction boosted VRF system uptake, while Ulsan’s petrochemical plants invested in explosion-proof chillers compliant with soon-to-be hardened F-gas quotas.

South Korean OEMs leveraged supply-chain proximity to Japanese inverter manufacturers and Chinese component makers, shortening lead times for custom equipment. Export volumes to the United States climbed sharply: air-to-water heat-pump shipments soared 667% in 2023 after new federal tax credits aligned with the high-efficiency profile of Korean products. [4]Hyun-soo Kim, “Korean Heat-Pump Exports Surge,” kotra.or.kr Regional climate volatility broadened the addressable base; intensified heatwaves in Southeast Asia prompted Singapore and Vietnam developers to adopt Korea-made low-GWP chillers with integrated AI controls. Consequently, geographic revenue diversity cushions suppliers from cyclical swings in the domestic construction cycle while amplifying the South Korea HVAC market’s international footprint.

Competitive Landscape

Competition intensified as electronics conglomerates deployed their balance sheets to secure specialist HVAC capabilities. Samsung’s acquisition of FläktGroup in May 2025 granted it access to industrial air-handling units, smoke-extraction systems, and data-center cooling lines that complement its heat-pump portfolio. LG Electronics earlier absorbed LS Mtron’s HVAC division, aiming to raise B2B revenue to 45% by 2030 through emphasis on export-grade chillers and modular AHUs.

Japanese incumbents Daikin and Mitsubishi Electric maintained share via brand reputation and well-established dealer networks, yet face rising pressure to localize production to avoid import duties. Carrier Global and Trane Technologies cultivated service contracts with multinational factories, offering predictive analytics layered onto bilingual cloud dashboards. Domestic mid-tier suppliers targeted niche opportunities in hydrogen-ready heat pumps and ammonia-based industrial refrigeration, betting that demanding refrigerant targets will open white-space as legacy R410A systems reach end-of-life.

Technology leadership has become the primary differentiator. Vendors race to roll out R32- and R290-ready lines ahead of the 2028 phase-down checkpoint, while embedding AI diagnostics to minimize truck rolls. Portfolio breadth, service reach, and refrigerant innovation therefore define competitive success in the South Korea HVAC market as 2030 approaches.

South Korea HVAC Industry Leaders

-

Daikin Industries Ltd.

-

LG Electronics Inc.

-

Samsung Electronics Co. Ltd.

-

Carrier Global Corp.

-

Johnson Controls International PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Samsung Electronics finalized its EUR 1.5 billion acquisition of FläktGroup to scale in industrial HVAC and data-center cooling.

- April 2025: The HVAC KOREA 2025 forum urged strengthened ZEB adoption tools and greater private-sector incentives.

- February 2025: The Ministry of Trade, Industry and Energy launched a KRW 37.9 billion subsidy covering 40% of high-efficiency HVAC equipment costs.

- February 2025: The Korean Environment Corporation unveiled a plan to cut HFC emissions by 20 million tCO₂e by 2035, mandating refrigerant reporting and recycling.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South Korea HVAC market as all heating, ventilation, and air-conditioning equipment plus associated installation, retrofit, and after-sales service revenues generated within the country's borders by resident and international brands. It covers room and central systems serving residential, commercial, and industrial buildings.

Exclusion: portable air purifiers and vehicle HVAC are outside scope.

Segmentation Overview

- By Type of Component

- HVAC Equipment

- Heating Equipment

- Heat Pumps

- Boilers, Radiators, etc

- Air-Conditioning and Ventilation Equipment

- Split Systems (Ducted and Ductless)

- VRF

- Air Handling Units

- Chillers

- Fans Coils

- Indoor Packaged and Roof Tops

- Others Types

- Heating Equipment

- HVAC Services

- Installation

- Maintenance and Repair

- Retrofit and Energy Management

- HVAC Equipment

- By End-user Industry

- Residential

- Commercial

- Office Buildings

- Retail and Hospitality

- Healthcare Facilities

- Educational Institutions

- Data Centers

- Public and Government Buildings

- Industrial

- Manufacturing Plants

- Oil and Gas and Energy

- Food and Beverage Processing

- Pharmaceuticals

- By Installation Type

- New Construction

- Retrofit / Replacement

- By Capacity Range (Cooling/Heating kW)

- Up to 5 kW

- 5 - 20 kW

- 20 - 50 kW

- 50 - 200 kW

- Above 200 kW

Detailed Research Methodology and Data Validation

Primary Research

Interviews with OEM engineers, facility managers, and installer networks across Seoul, Busan, and emerging provincial hubs validated efficiency premiums, average selling prices, and replacement cycles. Surveys of residential buyers clarified capacity preferences and willingness to pay, which sharpened service uptake assumptions.

Desk Research

We began with public datasets such as Korea Customs Service shipment records, Korea Energy Agency building-energy statistics, Ministry of Land, Infrastructure and Transport permit data, and Korea Refrigeration & Air-Conditioning Industry Association white papers. Company filings, investor presentations, and reputable press helped trace price trends and channel shifts.

To enrich financial signals, our analysts accessed D&B Hoovers for supplier revenue splits and Dow Jones Factiva for deal flow. These sources illustrated technology adoption, policy incentives, and construction pipelines; yet the list is not exhaustive, as many other references informed data checks.

Market-Sizing & Forecasting

A top-down reconstruction using national construction floor-area additions and stock replacement volumes set the 2024 baseline, which was then cross-checked with sampled ASP x unit estimates from distributor audits. Key variables like cooling-degree days, building code efficiency steps, split-system penetration, heat-pump import volumes, and retrofit share feed the model. Forecasts employ multivariate regression blended with scenario analysis to reflect policy-driven heat-pump acceleration. Gaps in bottom-up counts are filled by calibrated ratios from matched building archetypes before final alignment through one-time top-down and bottom-up reconciliation.

Data Validation & Update Cycle

Outputs pass anomaly scans, peer review, and variance checks against energy intensity benchmarks. Mordor analysts re-engage industry contacts when quarterly construction or tariff shifts exceed predefined thresholds. Reports refresh annually, with mid-cycle updates for material events.

Why Mordor's South Korea HVAC Baseline Commands Reliability

Published estimates often diverge because firms select different equipment mixes, treat services variably, or refresh models at uneven cadences.

Key gap drivers include narrower scopes limited to equipment only, aggressive straight-line growth without policy nuance, and currency conversions frozen to legacy rates; whereas Mordor's baseline folds in services, retrofit surges, and real-time won-USD moves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.59 B (2025) | Mordor Intelligence | - |

| USD 3.63 B (2023) | Regional Consultancy A | Excludes after-sales services and large industrial chillers; relies on static replacement cycle |

| USD 5.40 B (2024) | Trade Journal B | Omits installation revenue and applies fixed 2020 FX rate; uses linear growth |

| USD 0.32 B (2024) | Global Consultancy C | Focuses solely on hydronic systems, leaving ventilation and AC outside scope |

Taken together, the comparison shows that our disciplined scope, real-world variables, and annual refresh cadence deliver a balanced, transparent baseline clients can trace and replicate with confidence.

Key Questions Answered in the Report

What is the current size of the South Korea HVAC market?

The South Korea HVAC market stood at USD 6.59 billion in 2025 and is projected to reach USD 9.26 billion by 2030.

Which component segment is growing fastest?

HVAC services are expanding at a 9.8% CAGR as building owners seek lifecycle optimization and compliance support.

How will F-gas regulations influence equipment choices?

Starting 2028, high-GWP refrigerants face progressive bans, pushing buyers toward R32, R290, and natural-refrigerant systems that comply with the Kigali reduction timetable.

Why are data centers important for HVAC demand?

AI workloads generate high heat densities, so data-center cooling requires redundant, high-capacity solutions, lifting applied chiller sales at 11% CAGR.

What incentives are available for small businesses?

A KRW 37.9 billion national fund reimburses 40% of eligible high-efficiency HVAC equipment costs, with a maximum KRW 1.6 million per installation.

Which capacity range is growing quickest?

Units up to 5 kW are rising at a 10.3% CAGR, reflecting uptake in single-family homes and small commercial sites benefiting from targeted subsidies.

Page last updated on: